Mongkol Onnuan

National Retail Properties (NYSE:NNN) invests in single-tenant, net-leased retail properties throughout the U.S., and currently has an interest in over 3,300 properties. This portfolio is geographically diversified in 48 states and includes more than 380 national and regional retail tenants.

Among their top classes of tenants are convenience stores, automotive service, and restaurants, who together represent nearly 50% of annualized base rents. Furthermore, their top tenants include 7-Eleven, Mister Car Wash, and Camping World Holdings (CWH). Though their top 25 tenants represent 50% of annualized rents, no single tenant accounted for over 5%.

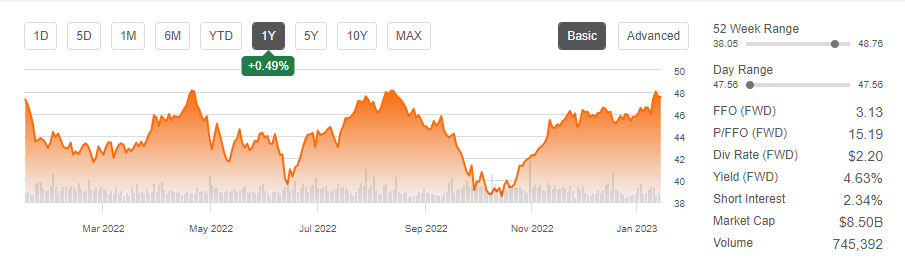

Over the past one year, shares have been remarkably stable and are essentially little changed, despite broader market volatility. Though the stock hasn’t produced the outsized gains hoped for by some, it has provided stability and buffeted portfolios from steeper losses.

Seeking Alpha – NNN Basic Trading Data

With shares near a 52-week high and at a price point that was recently justified for an equity raise, one can reasonably view shares as fairly valued. While the stock does have some further room to run, the upside may not be enough for those seeking to capitalize on more dislocated opportunities.

Recent Performance

NNN posted strong results in the quarter ended September 30, 2022. These results were also paired with a further increase in full-year guidance for core funds from operations (“FFO”).

High occupancy levels that continue to track above their long-term averages and nearly 100% collections of rent due were two contributors to the quarterly strength. In addition, the company also benefitted from the continued repayment of deferred rents relating to the COVID-19 pandemic.

While deferred rent repayments have been a contributing factor to growth in AFFO, the impacts continue to wean off peak levels reported in 2021. In the current quarter, for example, AFFO/share came in at $0.81 when including the repayments and $0.80/share excluding.

The inclusive effects, therefore, are negligible. And looking ahead to 2023, repayments are expected to be just +$3.3M, which would be down significantly from the +$9.1M in 2022.

Recent acquisitions, thus, are likely to figure more greatly into earnings growth in the periods ahead. And on this, NNN continues to be highly active in the market despite ongoing price discovery challenges.

In Q3, they acquired +$220M of properties. And through nine months of the year, NNN has invested +$585M in acquisitions. This already exceeds their 2021 volume of +$550M. As a result, annual base rents ended the quarter at over +$750M, which is a first for the company.

Liquidity And Debt Profile

Even though NNN has significantly expanded their portfolio, they’ve done so without sacrificing their balance sheet. At quarter end, for example, they had just under +$50M outstanding on their +$1.1B credit facility. This is despite nearly +$590M in YTD acquisitions.

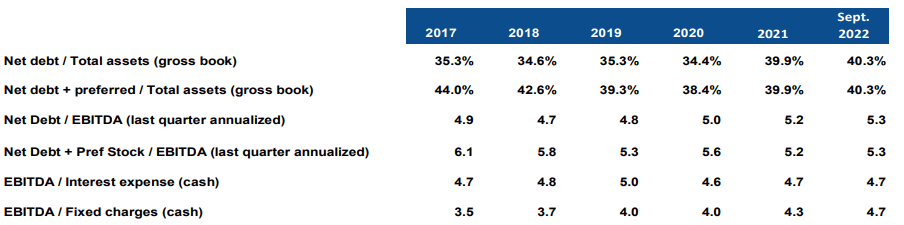

In addition to ample liquidity, they also have a manageable overall debt load that represents about 40% of their total assets.

Net debt as a multiple of EBITDA, at 5.3x, is also consistent with figures reported in recent years, though it is elevated from pre-COVID levels. This is offset by a fixed coverage ratio that is improved from prior levels on strong earnings growth.

November 2022 Investor Presentation – Comparative Summary Of Select Leverage Metrics

NNN also benefits from having a favorable debt ladder that carries a weighted average maturity of 14 years. With no meaningful debt maturities until mid-2024, the company faces limited near-term repayment risks. Additionally, all their debt outstanding, save the small balance on their revolver, is fixed rate, resulting in minimal risks relating to volatile interest rates.

NNN also has readily available access to capital via equity raises and property dispositions. Through nine months of 2022, NNN has raised +$130M in common equity and has received +$49M in disposition proceeds. Most recently, they issued +$97M in equity in Q3 at the $47/share level and obtained +$21M in proceeds on the disposition of eight properties.

Dividend Safety

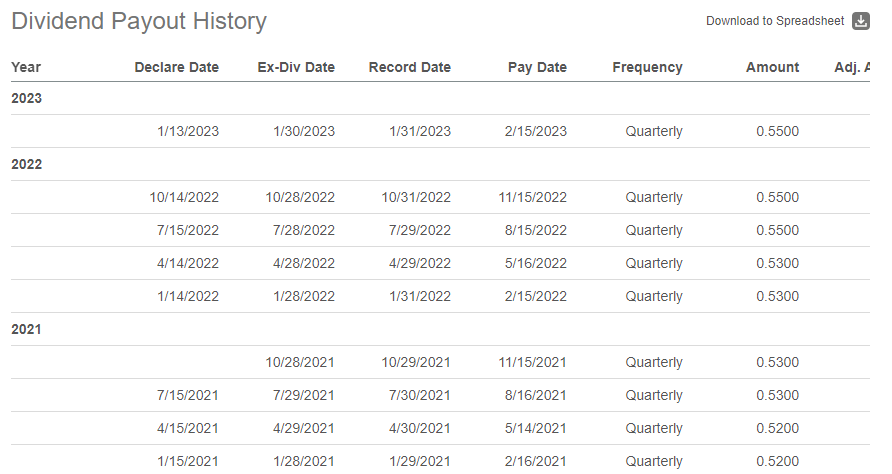

The credibility of NNN’s dividend payout is cemented by 33 consecutive annual increases. This is the third longest of all publicly traded REITs and 99% of all public companies.

While this does not guarantee continuity of the payout into perpetuity, it should provide a high degree of assurance to income investors seeking not only reliable quarterly receipts but also modest annual increases.

Currently, the annualized payout yields 4.6% at current pricing and is growing at a five-year compound rate of 3%. Most recently, the quarterly payment was increased 3.8% in mid-2022.

Seeking Alpha – NNN Recent Dividend Payout History

As of Q3, the payout ratio stood at just 67% of AFFO. This compares favorably to the sector average of about 75%. In addition, the payout is also better covered than close peer, W.P. Carey (WPC), who currently has a payout ratio of about 80%.

Furthermore, the company ended the quarter with +$141M in retained AFFO after the full payout of all dividends. And through nine reported months in 2022, the company has generated just over +$180M in free cash flow post-dividends. Annually, it is expected to be approximately +$190M.

Though the current yield may not be tempting enough for yield-starved investors, the solid track record and coverage levels provides an additional level of backing to the company’s portfolio and financial position.

Main Takeaway

NNN has provided existing shareholders with much-needed stability in an otherwise volatile market environment. This is due in part to the quality of their current portfolio, which is currently 99.4% occupied by over 380 national and regional tenants.

The company does have exposure to a higher degree of non-investment grade tenants, which increases the risk profile of their portfolio. Yet, occupancy has continuously remained above 96.4% every year since 2003, a feat that cannot be said of the broader REIT industry.

At 15x forward FFO and at the upper end of their 52-week range, shares would at first glance appear fairly valued. At current pricing, however, shares trade at an implied cap rate of about 6%. But recent dispositions were completed at about 5.8%. Though not wildly off, there is some level of disconnect.

At a 5.7% cap, shares would be worth about $51/share. This would present upside of about 7%, excluding dividends. While this is respectable, it may not be enough for many investors seeking to make up for a poor overall year in 2022. Though a solid long-term holding for existing shareholders, new investors may be better off waiting for a better buy-in.

Be the first to comment