KangeStudio

Commentary1

The Mittleman Global Value Equity Fund (MGVEF) declined 17.6% in Q2, vs. a decline of 7.9% in the MSCI ACW Net Total Return Index.

A new position in MGVEF, Heritage Crystal Clean was the only positive contributor to performance. MIM initiated the position at the end of June.

The bottom three performing stocks, from a contribution standpoint were AMA Group (OTCPK:AMGRF) -55.8%%, Greatview Aseptic (OTCPK:GRVWF) -29.4% and Aimia Inc (OTCPK:AIMFF) -11.5%.

|

Fund details |

|

|

Index |

MSCI All Country World Index (ACWI) Net Total Return in AUD |

|

Fund inception date |

June 2017 |

|

Class P inception date |

October 2017 |

|

Performance2 – 30 June 20224 |

|||

|

MGVEF Class P |

Index (AUD) |

Excess return |

|

|

1 month |

(2.2%) |

(4.5%) |

2.3% |

|

3 months |

(17.6%) |

(7.9%) |

(9.7%) |

|

1 year |

(31.6%) |

(8.0%) |

(23.5%) |

|

2 years p.a. |

6.2% |

8.4% |

(2.2%) |

|

3 years p.a. |

(4.6%) |

6.9% |

(11.5%) |

|

Since inception3 |

(3.3%) |

9.1% |

(12.4%) |

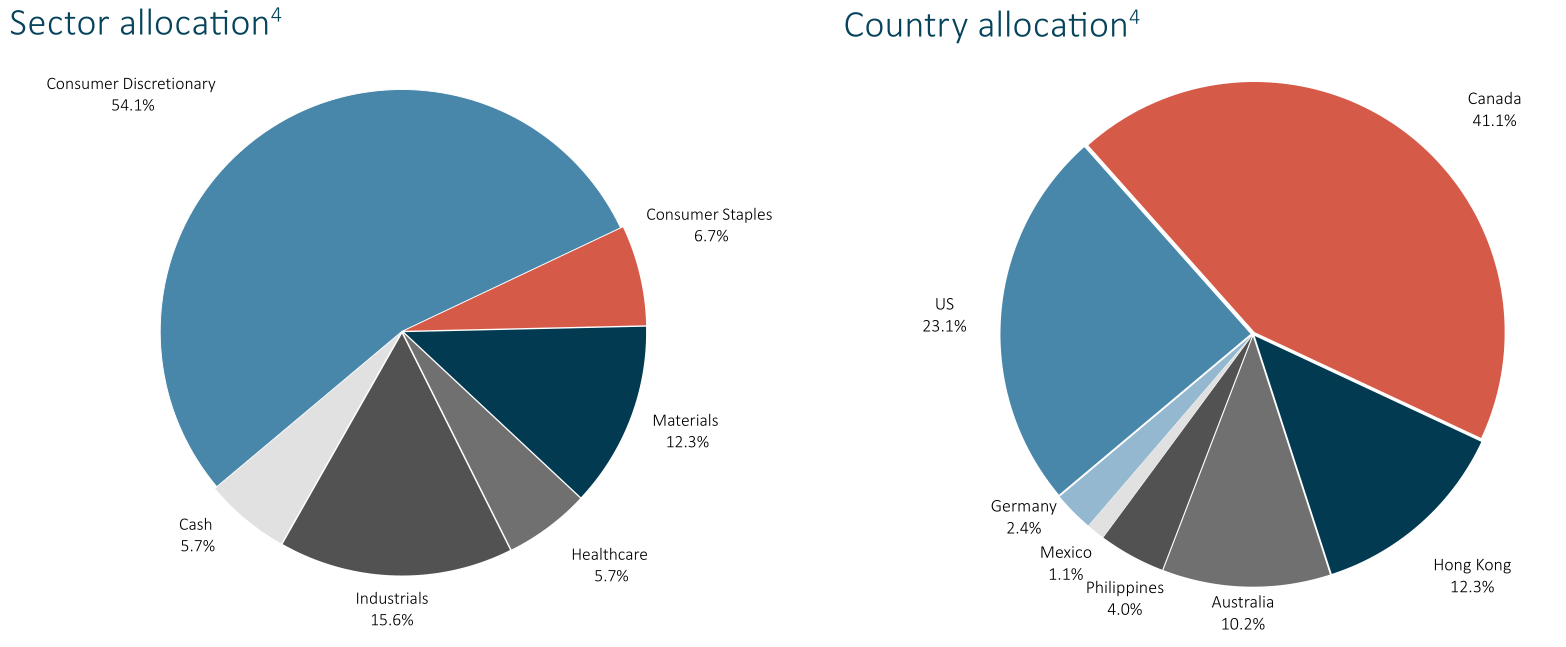

Top 10 holdings5 (As at 30 June 2022)

|

Portfolio statistics6 (As at 30 June 2022)

|

Quarterly investment review7

The first half of 2022 was not fun. The S&P 500 was down 20.0%, its worst first half since 1970 (-19.5% YTD at 30 June 1970, but rose 29.1% to close 1970 at +3.8% for the year). The Russell 2000 dropped 23.4%, its worst first half since its inception on 31 December 1978. MIM also had its worst first half performance ever, at -34.8% for the Mittleman Investment Management Composite (MIM Composite).

That still leaves the MIM Composite 18.3% above the 31 October 2020 level, at the apparent start of a shift back to value investing in November 2020 which saw the MIM Composite rise 100.6% over 7 months from 31 October 2020 to 31 May 2021, then give back 41.0% of that over the past 13 months from 31 May 2021 to 30 June 2022.

Even after that brutal pullback, the MIM Composite is roughly matching the performance of the S&P 500 (+18.7% since 31 October 2020) and significantly outperforming the Russell 2000 (+13.1% since 31 October 2020), and the MSCI ACWI (+12.1%). More importantly, the implied upside potential from the current market prices of MIM’s holdings to its estimates of fair value was +149% as of 30 June 2022, a magnitude we have not seen since it was 151% on 30 September 2020, just before the 100%+ move up from November 2020 to May 20218.

MIM owns almost nothing in common with the popular market indices, so how the latter perform should not be determinative of how MIM’s portfolio performs. That said, the context provided by benchmarking against indices is helpful in support of the emotional aspect of investing, in which losses may feel less painful, or at least more endurable, with the knowledge that many others suffer alongside you. And endurance of losses is usually a prerequisite for the subsequent enjoyment of gains.

A professed value investor quoting Buffett or Munger in his or her quarterly letters is a pervasive cliché against which we fight hard not to succumb, but alas, sometimes it is just necessary. In this time of war, inflation, rising energy prices, rising interest rates, and a likely recession, we should not let the macro turmoil of this moment distract our decision-making or overwhelm our discipline in the business of investing:

From Warren Buffett, Berkshire Hathaway 1994 annual letter:

“We will continue to ignore political and economic forecasts, which are an expensive distraction for many investors and businessmen. Thirty years ago, no one could have foreseen the huge expansion of the Vietnam War, wage and price controls, two oil shocks, the resignation of a president, the dissolution of the Soviet Union, a one day drop in the Dow of 508 points, or treasury bill yields fluctuating between 2.8% and 17.4%.

But, surprise – none of these blockbuster events made the slightest dent in Ben Graham’s investment principles. Nor did they render unsound the negotiated purchases of fine businesses at sensible prices. Imagine the cost to us, then, if we had let a fear of unknowns cause us to defer or alter the deployment of capital. Indeed, we have usually made our best purchases when apprehensions about some macro event were at a peak. Fear is the foe of the faddist, but the friend of the fundamentalist.

A different set of major shocks is sure to occur in the next 30 years. We will neither try to predict these nor to profit from them. If we can identify businesses similar to those we have purchased in the past, external surprises will have little effect on our long-term results.”

MIM did purchase a couple of new holdings on sale after the protracted sell-off. MIM bought a 2.5% weighting in a leading environmental services company that Chris Mittleman has admired for many years, Heritage-Crystal Clean Inc. (HCCI), at an average cost of $26.77 in the waning days of June, with ~49% upside to MIM’s estimate of fair value at $40.

As at 1 August the shares are $34, up recently on a stronger than expected quarterly report announced on 27 July, and a large insider buy of 150,000 shares on that same day at $27.00 ($4.05M), bringing CEO Brian Recatto’s total shares directly held to 820,505 ($28M).

MIM’s estimate of fair value for HCCI of $40 is based on a $901M EV = 8.6x EBITDAaL (est. for CY2022) of $105M (17.5% margin on $600M sales) = 18x FCF est. of $50M. Closest competitor, Clean Harbors / Safety-Kleen (CLH $90) trades at 8.5x EBITDA (est. 2022) and 18x FCF (CLH has roughly same EBITDA margin as HCCI, despite being 8x larger).

Below a description of the company from the most recent 10-Q:

Heritage-Crystal Clean, Inc., a Delaware corporation and its subsidiaries (collectively the “Company”), provide parts cleaning, hazardous and non-hazardous containerized waste, used oil collection, wastewater vacuum, antifreeze recycling and field services primarily to small and mid-sized industrial and vehicle maintenance customers. The Company owns and operates a used oil re-refinery where it re-refines used oils and sells high quality base oil for use in the manufacture of finished lubricants as well as other rerefinery products.

The Company also has multiple locations where it dehydrates used oil. The oil processed at these locations is primarily sold as recycled fuel oil. The Company also operates multiple non-hazardous waste processing facilities as well as antifreeze recycling facilities at which it produces virgin-quality antifreeze. The Company’s locations are in the United States and Ontario, Canada.

The Company conducts its primary business operations through Heritage-Crystal Clean, LLC, its wholly owned subsidiary, and all intercompany balances have been eliminated in consolidation.

The Company has two reportable segments: “Environmental Services” and “Oil Business.” The Environmental Services segment consists of the Company’s parts cleaning, containerized waste management, wastewater vacuum, antifreeze recycling activities, and field services. The Oil Business segment consists of the Company’s used oil collection, recycled fuel oil sales, used oil rerefining activities, and used oil filter removal and disposal services.

No customer represented greater than 10% of consolidated revenues for any of the periods presented. There were no intersegment revenues. Both segments operate in the United States and, to an immaterial degree, in Ontario, Canada. As such, the Company is not disclosing operating results by geographic segment.

For those seeking more detail, the company’s website is highly informative: www.crystal-clean.com

This is a growth/cyclical business, with about 40% of sales from re-refining of used oil, and 60% from less cyclical environmental services. MIM thinks the valuation is penalised too much by the cyclical exposure with not enough credit for the great track record and prospect of continued growth.

The oil re-refining business is operating at an all-time high for HCCI recently, so that is likely to flatten out and with the obvious risk that it might more severely revert to the mean. But then again, if energy prices stay somewhat elevated the better than normal spread HCCI’s re-refining business has enjoyed recently might persist for some time. The cost of the used motor oil that HCCI collects from its various customers has risen, but not as much as the re-refined products which HCCI sells, mostly Group 2 Base Oil that goes into various lubricants.

Also, IMO 2020 (International Maritime Organization) regulations implemented on 1 January 2020 impose stricter sulfur limits on marine fuel, which increases demand for HCCI’s clean (low sulfur) fuel output.

MIM’s willingness to endure the risk that the oil re-refining business is unsustainably over-earning is because the environmental services side of the business (60%) holds a more than offsetting amount of appeal, both from organic growth expectations and from acquisitions, like the $156M purchase of Patriot Environmental Services announced on 30 June 2022.

On the 28 July Q2 earnings report conference call, HCCI’s management quantified the valuation paid for Patriot Environmental as 5.5x actual 2021 EBITDA, but 9x normalised 2021 EBITDA (excluding one big unusual contract). But, after cost saving synergies expected in year 1 of $7M, the post-synergies multiple paid drops back to 6.5x. A seemingly smart deal that is a continuation of their 22-year track record of growing organically and with accretive M&A.

There is also a large valuation gap, not just between HCCI and its larger peer, CLH, but between their sector and the large solid waste companies, which do have much higher EBITDA margins but still the valuation gap seems excessive. MIM’s suspect larger solid waste haulers may seek to buy out specialty environmental services companies like HCCI and CLH.

Lastly, controlling shareholder, Heritage Group Inc. (Fred Fehsenfeld Jr., 71 years old), which owns 20.6% of the HCCI shares outstanding, registered their shares for sale last year. That may be meaningless, but it might indicate an openness or preparation for potential sale. Fehsenfeld also controls Calumet Specialty Products (CLMT), which is somewhat similar to HCCI’s oil re-refining business. His 20.7% stake in HCCI is worth $168M, and his 15% stake in CLMT is worth $146M, both at today’s (August 1st) share prices.

MIM’s second new position was bought in mid-July, so a full write-up will be provided in the Q3 letter, but to summarise it briefly here, MIM initiated a 2.5% weighting in the ADRs of Tremor International (TRMR). Tremor International is a leading advertising technology company that Chris has come to know only over the past year or so, and was purchased at an average cost of $9.71, with an estimated fair value of $20 implying just over 100% upside potential.

Tremor International is a fast growing, FCF generative, ad tech business with a net cash balance sheet. MIM bought TRMR (the ADRs, the main listing is London) at just under $10 on average, and view fair value as 8x EBITDA of $175M, plus $118M in net cash, which equals just over $20 per ADR. If the historical growth rate continues that number will prove vastly too conservative. If a severe recession occurs and ad spending collapses, it may seem optimistic for the next year or so. Given the pristine balance sheet, and the inherently cash-generative nature of this business, MIM is willing to take the risk that the macro winds might blow against it in the short to intermediate term. Long term, MIM thinks digital advertising, and the way in which ad tech companies like Tremor facilitate it, provides a long growth trajectory to exploit.

Tremor is headquartered in Tel Aviv, Israel, which is second only to Silicon Valley in terms of the concentration of tech startups and talent there. Tremor has grown quickly via acquisitions and organically.

See Tremor’s IR website to learn more about this unusual combination of growth and value.

The top two detractors in Q2, AMA Group (OTCPK:AMGRF) and Greatview Aseptic (OTCPK:GRVWF) were discussed at length in the last quarterly letter and not much has changed beyond their stock prices dropping further.

On 30 June 2022 Greatview pre-announced weaker than expected results for the first half of 2022, on higher input costs, and China locking down again. But the aseptic packaging they produce is a proven secular growth story, so MIM continues to think a normalisation in margins will be achieved in a reasonable time as excess capacity in China is absorbed. But even if normalised margins remain elusive for another year or two, the growth in sales, gross margin dollars, and thus EBITDA and free cash flow should be strong enough to offset and exceed that headwind.

There is still a long way to go until China sees per capita consumption of such packaged products near western levels, and Southeast Asia is at a much earlier stage of development there. So, MIM continues to be very bullish about the long-term prospects for Greatview Aseptic.

AMA Group actually pre-announced slightly better than expected results recently and while it didn’t seem to help the stock price it is encouraging news. MIM continues to think it is just a matter of time until AMA gets the pricing relief that a company of their scale and market position (the largest collision repair company in Australia and New Zealand, 6x the next biggest player) is due and thus dramatically better margins. This was nearly a 10% EBITDA margin business in 2018 and 2019, it should be again soon (2023-2024). (Defining EBITDA the old way, pre-AASB-16, or after operating lease expenses).

Aimia remains MIM’s largest position by far, and on 30 June 2022 it closed the sale of its 49% stake in PLM to Aeromexico (OTC:GRPAF), receiving CAD 531M in cash, which is C$5.78 per share in cash (on 91.9M shares outstanding). That cash per share influx of C$5.78 per share is 25% higher than Aimia’s C$4.60 stock price as of 30 June 2022, without considering the remaining net assets (minority stakes in Clear Media (OTC:CRMLF), Trade X, and other public and private investments) which should substantially exceed the value of Aimia’s perpetual preferred stock.

How Aimia redeploys that cash will the critical determining factor for future performance. Given the backdrop of generally weakening asset prices lately, Aimia’s cash infusion may have been fortuitously worth the wait as the opportunities have multiplied to deploy capital at the prospectively high hurdle rate of return that we as Aimia shareholders expect.

Lastly, MIM has already communicated regarding the Revlon bankruptcy filing on June 15th, see this link if you missed it, as MIM’s opinion here is unchanged.

Revlon has since traded up from the pre-bankruptcy filing low of $1.08 on 13 June to above $9.00 on a couple of occasions, on 22 June and again on 1 August, and during those two trading sessions, MIM sold a good portion of its position at just over $9.00/share, given Chris’ reduced estimate of fair value is $10 (down from the mid-20s).

If the bankruptcy process results in an auction of the assets the realisation could be far in excess of $10 per share by simply applying the range of current market multiples. But, bankruptcy introduces significant costs, uncertainties, and risks that could confound fairness, so reducing the weighting into these periodic price spikes makes sense.

MIM continues to think there are plenty of buyers for these assets who could easily pay the 2x sales and 14x EBITDA needed (by Chris’ math) for the equity to recover about $10 per share in value. 15x EBITDA would be nearly $16 per share. 16x would be $22. And there are some new unexpected potential buyers, too.

For example, on a July 27 earnings conference call, luxury fashion giant Kering SA (OTCPK:PPRUF), said they were considering entering the beauty business directly for the first time. They currently operate under a license model, with Coty Inc. (COTY) handling Gucci, Alexander McQueen and Bottega Veneta; and L’Oréal holding the rights for Saint Laurent, and Interparfums in charge of Boucheron.

Given that Kering focuses exclusively on prestige brands, they would likely only be interested in the Elizabeth Arden business that Revlon owns. But, they could pay a lot for it and it would still be highly accretive for Kering given the sizable cost and revenue synergies that one could easily imagine there.

Anyway, if MIM’s base case is realised, and done as asset sales (not a buy-out of the common stock which would likely destroy tax assets), it would leave REV with about $500M in cash (around $10 per share), and over $1B in NOLs. Ironically, Revlon started out in just that way, a formerly bankruptcy public holding company, Pantry Pride (was a supermarket chain), with cash and a huge NOL, that Perelman got control of and used to buy Revlon in 1985.

If there is an argument to be made against Revlon’s existing equity retaining value, MIM thinks it has to start with how 2x sales and 14x EBITDA is somehow an unreasonable expectation for these assets. Given that such a valuation would be immensely accretive to almost any strategic buyer imaginable, particularly post-synergies, MIM thinks it’s a reasonable expectation.

This is a once-in-a-generation opportunity for any buyer to make a significant leap in market share, distribution, and on-shore manufacturing capacity, so there is strategic value here beyond the normal capitalisation of cash flows.

Estee Lauder (EL) is doing amazingly well in prestige cosmetics, but they have no mass market brands (L’Oreal has both) and in 2008 Estee Lauder saw sales drop 11.6% while Revlon experienced only a 1.5% sales drop as mass market brands held up better during the hard times.

Chris owned Maybelline in 1994-1995 around $17 when it was down (from $40+) and out of favour, just before L’Oreal bought them at $44 (2x sales, 14.7x EBITDA) in early 1996 and made them the #1 mass market brand. Chris thinks Estee Lauder has a similar play to make here with Revlon if they are opportunistic enough to see it that way, and thus nearly doubling their total addressable market (the mass market being almost as big as prestige).

MIM’s client retention ratio was a rock solid 96.2%* YTD through 30 June 2022, despite the harrowing losses in account values. Much as it was in 2008 at 92.6%, despite a peak to trough drawdown of 77.1% from 31 May 2007 to 28 February 2009, just before MIM rose 13.75x over the ensuring 5.5 years (28 February 2009 to 31 August 2014: 5.5 yrs. +61.3% CAGR (13.75x), taking MIM from a negative inception to date result over the 6+ years ended 28 February 2009 to 23% CAGR over 11.66 yrs. (11.01x).

Whether or not MIM can mount a similarly spirited comeback from this much longer, albeit much less deep drawdown, remains to be seen. As you should know, MIM remains all-in for the attempt, and view this recent setback no differently than all of the prior ones, including the 50% swoon into March 2020 on the COVID crash, before finishing the year up slightly.

There are vast opportunities on display here for the taking, so you should feel energised by that, if not excited, as MIM sincerely does. As we did in March 2020, as we did in February 2009, and as we did in many scary moments prior, we’ve always come out stronger on the other side. MIM looks forward to seeing us all again well rewarded for our mutual endurance through these trials.

Investment strategy

Mittleman Investment Management, LLC (MIM) is an SEC-registered investment advisor based in New York that pursues superior returns through long-term investments in what it deems to be severely undervalued securities, while maintaining its focus on limiting risk. It invests in businesses that it believes are proven franchises with durable economic advantages, evidenced by a well-established track record of substantial free cash flow generation over complete business cycles, and only when the very low valuation at which the investment is made provides a significant margin of safety. MIM’s value-oriented strategy is to invest in a concentrated portfolio (usually between 10 to 20 securities) of primarily common stocks, unrestricted as to market capitalisation, and in both developed and emerging markets.

Footnotes

|

1The securities herein identified and described do not represent all of the securities purchased, sold or recommended for MGVEF. The reader should not assume that an investment in the securities identified was or will be profitable. There is no assurance that any securities discussed herein will remain in the portfolio at the time you receive this report, or that securities sold have not been repurchased. There can be no assurance that investment objectives will be achieved. All dollar amounts within this report are in USD unless otherwise stated. The performance of the top and bottom three performing stocks are calculated in USD. 2Performance figures are presented in AUD on a net, pre-tax basis and assume the reinvestment of distributions. Past performance is not indicative of future results. Figures in the table may not sum correctly due to rounding. 3Since inception returns are annualised and calculated from 13 October 2017. Past performance is not indicative of future results. 4Portfolio holdings, country allocation and sector allocation of MGVEF are as of 30 June 2022 and are subject to change and should not be considered as investment recommendations to trade individual securities. Country allocation does not include cash. 5Portfolio holdings, country allocation and sector allocation of MGVEF are as of 30 June 2022 and are subject to change and should not be considered as investment recommendations to trade individual securities. Country allocation does not include cash. The securities herein identified and described do not represent all of the securities purchased, sold or recommended for MGVEF. The reader should not assume that an investment in the securities identified was or will be profitable. There is no assurance that any securities discussed herein will remain in the portfolio at the time you receive this report, or that securities sold have not been repurchased. There can be no assurance that investment objectives will be achieved. 6Portfolio statistics are reported in USD and are as at 30 June 2022. The statistics are updated in the report as at the end of each quarter. 7The securities herein identified and described do not represent all of the securities purchased, sold or recommended for MGVEF. The reader should not assume that an investment in the securities identified was or will be profitable. There is no assurance that any securities discussed herein will remain in the portfolio at the time you receive this report, or that securities sold have not been repurchased. There can be no assurance that investment objectives will be achieved. All dollar amounts within this report are in USD unless otherwise stated. 8The estimates reflect various assumptions by MIM concerning anticipated results that are inherently subject to significant economic, competitive, and other uncertainties and contingencies and have been included solely for illustrative purpose. Aimia Inc. fair value estimate shown is an average of Aimia price targets from TD Securities and RBC Capital brokerage firms’ most recently published reports on Aimia (CAD 7.00, converted to USD 5.42) as summarised by Bloomberg as of 30 June 2022. No representations, expressed or implied, are made as to the accuracy or completeness of such assumptions, estimates or projections. *Client retention rate is calculated based on 2022 beginning assets under management (“AUM”) less outflows attributable to closed accounts for the year to date period (based on their 2022 beginning net asset values) over total Firm beginning AUM for 2022. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment