sl-f/iStock via Getty Images

Apartments REITs have traded materially down over the past year, offering long-term value investors a great opportunity to pick up high quality names in the sector. While AvalonBay Communities (AVB) and Essex Property Trust (ESS) offer strong exposure to the coasts, Mid-America Apartment Communities (NYSE:MAA) gives investors diversification and exposure to growing secondary markets, where it sees less competition from institutional players.

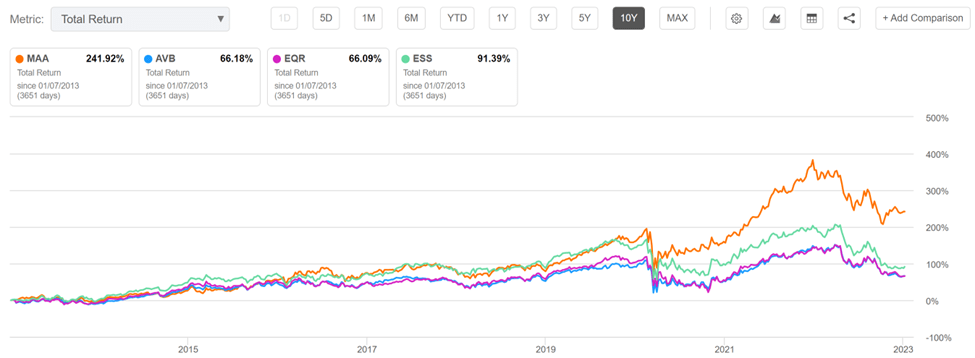

As shown below, MAA is down by 28% over the past year, and in this article, I highlight what makes MAA a solid choice for dividend growth investors, so let’s get started.

MAA Stock (Seeking Alpha)

Why MAA?

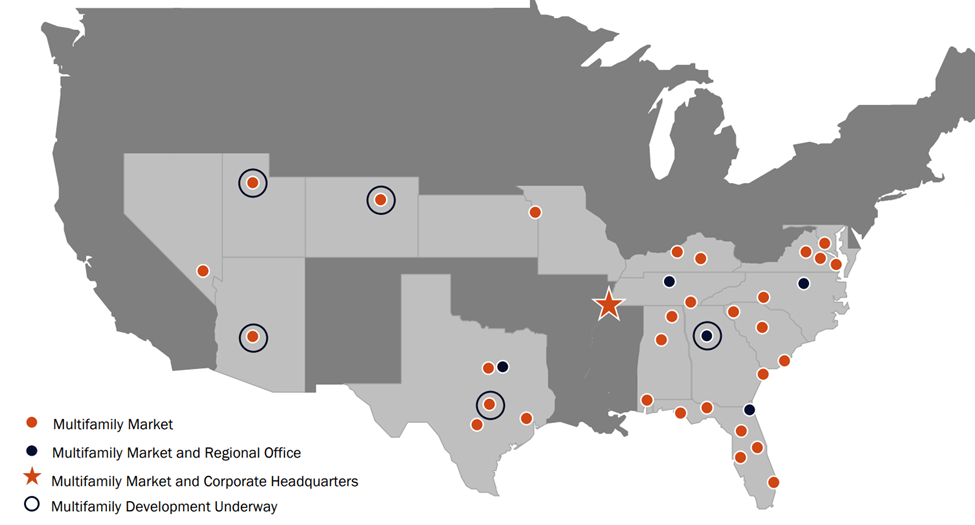

Mid-America Apartment Communities is an S&P 500 (SPY) company and owns and operates 282 communities spread across 16 states. Unlike its larger peers, who have heavy exposure to coastal gateway markets, MAA’s properties primarily lie in the Southeast, Texas, and Mid-Atlantic regions. Its top three markets of Atlanta, Dallas, and Tampa comprise 29% of its total NOI. Here’s a snapshot of the property portfolio.

MAA Property Map (Investor Presentation)

MAA’s focus on less competitive and growing markets is a key factor for its success over the long-term. This has translated into outsized shareholder returns. As shown below, MAA’s 10-year total return of 242% has handily beaten that of peers AvalonBay, Equity Residential, and Essex Property.

MAA Total Return (Seeking Alpha)

Meanwhile, MAA appears to be beating inflation, as it produced same property revenue growth of 14.6% YoY during the third quarter. It’s also demonstrating positive operating leverage, as same property operating expense grew by just 10.1%, resulting in faster net operating income growth of 17.4% at the property level. This speaks to the quality of the underlying properties and the supply-constrained nature of MAA’s core markets.

Management has also shown adept at redeveloping properties, including the completion of over 2,300 apartment units in the last reported quarter, capturing average rental rate increases of 10% above non-renovated units.

Notably, MAA carries a strong balance sheet and recently received a credit rating bump from BBB+ to A- from the S&P last August. This is supported by a very safe net debt to adjusted EBITDAre ratio of 3.97x. MAA also carries plenty of dry powder, as it had $1.2 billion of combined cash and available capacity under its revolving credit facility as of the last reported quarter.

This could go a long way in funding its development program looking forward, which management expects to achieve monthly rents that are 22% above the average rent in its current portfolio. This includes 6 communities currently under development comprising 2,254 apartment units. MAA can easily fund these projects, as they require just $375 million in remaining funding, sitting well below the aforementioned liquidity MAA has on hand.

Moreover, MAA is seeing healthy growth trends in its core markets, driven by their higher level of affordability and warmer climates. This was reflected by management during the recent conference call:

We’ve not seen any evidence of weakness in the drivers of demand for apartment housing as it applies to our Sunbelt portfolio. Of the leases written in the third quarter, 15% of our new residents were relocating to the Sunbelt from coastal markets. This is comparable to the trends we saw last year. It’s also worth noting that the move-outs we had in the third quarter, only 5% were moving out of the Sunbelt. This is also consistent with last year’s trends.

Additionally, on average, we are achieving growth rates on signed renewals of around 10% for the fourth quarter. Despite projections that supply will likely remain elevated in 2023, that we think at similar levels to 2022, various demand indicators remain strong and we expect our region of the country to continue to benefit from population, household and job growth.

Importantly for income investors, MAA recently raised its quarterly dividend rate by 12% last month to $1.40 per share. The dividend is very well covered by a 64% payout ratio, based on FFO per share of $2.19 during the third quarter.

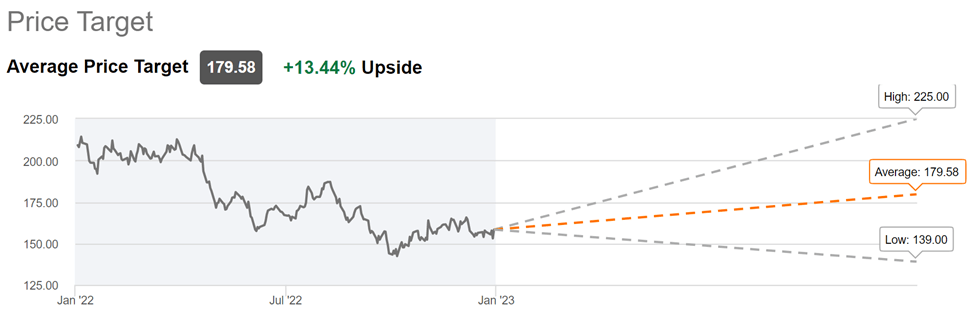

Turning to valuation, I find MAA to be reasonably attractive after falling by 28% over the past year. At the current price of $158, it trades at a forward P/FFO of 18.8. While this doesn’t necessarily screen cheap on a value investor’s radar, I believe it’s deserving of this valuation considering the very strong balance sheet, strong lease spreads, development potential, and the 9.3% FFO per share growth rate that analysts expect this year.

Notably, Analysts have a consensus Buy rating on the stock with an average price target of $180, calculating to a potential 17% total return including dividends.

MAA Price Target (Seeking Alpha)

Investor Takeaway

MAA is a high quality apartment REIT with a great balance sheet and potential for growth. It’s seeing strong operating leverage with property revenue growth outpacing expense growth, and is seeing favorable population growth in its Sunbelt markets. Plus, development and redevelopment opportunities provide another avenue for lease-up potential. MAA isn’t cheap, but it’s reasonably priced for potentially strong long-term returns.

Be the first to comment