wildpixel

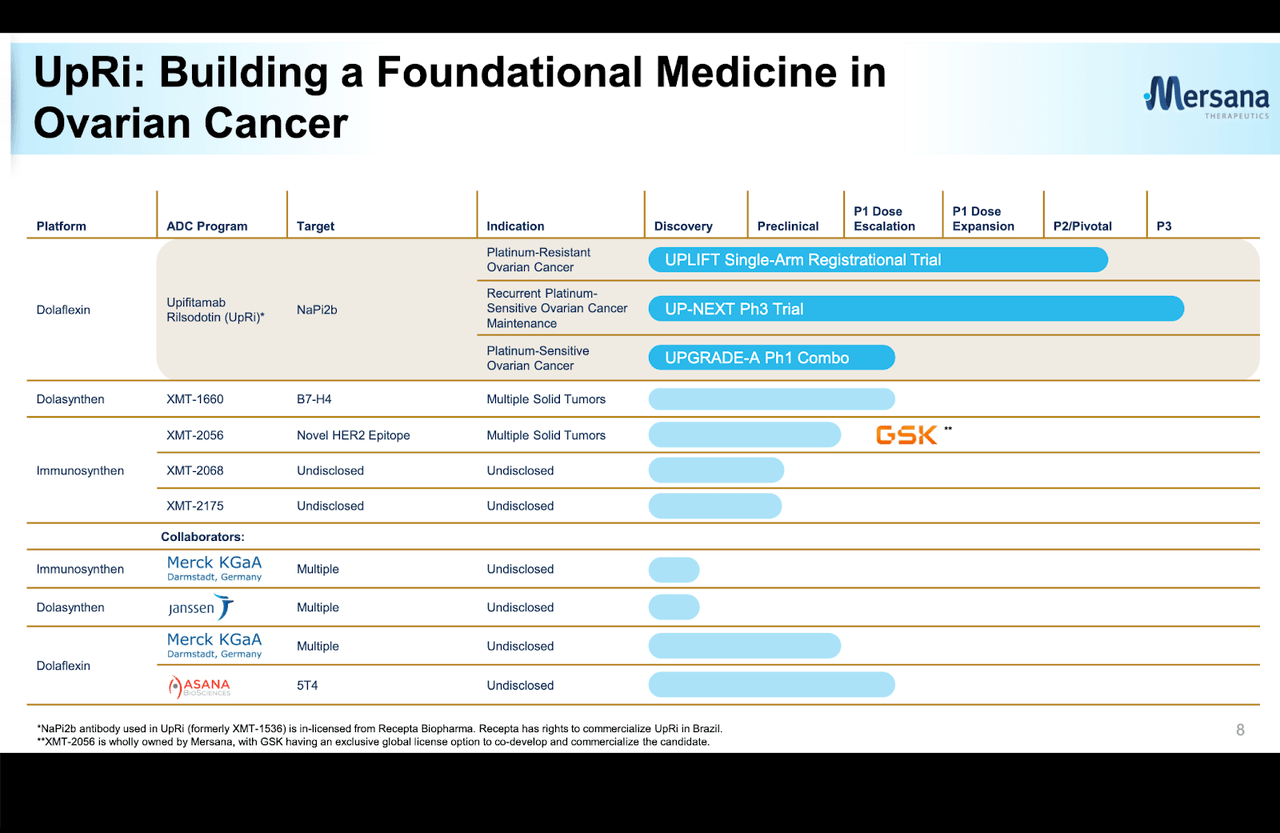

Mersana (NASDAQ:MRSN) is a small-cap developer of antibody drug conjugate molecules targeting oncology indications. Mersana has a number of major partnerships with big pharma, including with Merck KgaA (OTCPK:MKGAF), the world’s oldest pharmaceutical company, and Janssen (JNJ). The pipeline has some late stage assets. Lead candidate is Upifitamab Rilsodotin (UpRi) in a registrational trial targeting platinum resistant ovarian cancer. Here’s how the pipeline looks:

Mersana Pipeline (Mersana website)

Their technology platforms are called DolaLock, Dolaflexin, Dolasynthen and Immunosynthen. ADCs are a mainstay of cancer therapy. In traditional ADC, a monoclonal antibody with a cancer cell targeting capacity is conjugated to a cytotoxic payload, which gets released when the molecule enters the tumor cell, killing the cell. There were two limitations here; one, off-target toxicity, and two, only cytotoxic payloads. Mersana tries to overcome both limitations by using its platforms to develop more targeted therapies, and also create the ability for ADCs to carry immunostimulatory payloads instead of cytotoxic payloads.

DolaLock is a novel technology which blocks the so-called bystander effect, where the cytotoxic payload released into the tumor cell crosses into, and kills, the neighboring cell. The company uses a proprietary auristatin cytotoxic molecule that retains its cytotoxic properties but is unable to cross the cell membrane, effectively locking itself inside the target cell.

DolaLock also inhibits multi-drug resistance (MDR) pumps, such as PgPs, from pumping out the ADC molecule from the tumor cell. MDR pumps are otherwise effective mechanisms by which cancer cells protect themselves from cell killing drugs.

Thirdly, the company says that DolaLock’s auristatin payload in preclinical models has also shown “to cause immunogenic cell death and to stimulate the immune system through dendritic cell activation.”

The second platform, Dolaflexin, overcomes another limitation of ADCs. Traditional ADCs have their payloads directly linked to the mAb. This limits drug solubility, pharmacokinetics and immunogenicity, and also limits the number of molecules the ADC can carry. Dolaflexin uses a highly biosoluble, biodegradeable polymer (Fleximer) as a bridge. The cytotoxin attaches to the Fleximer scaffold through a cleavable linker, and the Fleximer attaches to the antibody through a non-cleavable linker. This overcomes many of the above limitations.

The company lists some of the advantages (quoted):

-

Proprietary DolaLock Payload: Dolaflexin is loaded with our proprietary auristatin chemotherapeutic drug, which is a highly potent anti-tubulin agent selectively toxic to rapidly dividing cells, with the advantages of the DolaLock controlled bystander effect.

-

Higher Drug-to-Antibody Ratio (DAR): Historically, ADCs have been limited to a DAR of 3-4. The Dolaflexin platform can deliver ADCs with DAR of about 10 allowing for greater efficacy while also maintaining pharmacokinetics and drug-like properties.

-

Expanded Range of Addressable Tumor Targets: The higher DAR enabled by Dolaflexin results in more chemotherapeutic drug released into the tumor cell for every ADC internalized. As a result, Dolaflexin ADCs have efficacy against tumor targets with lower levels of antigen expression where traditional ADCs have not been effective.

Dolasynthen takes up the DAR discussed above and creates specific DARs for different situations. Different antigens need different amounts of cytotoxins, and this platform allows for precise DARs between 2-18+.

The last platform is used to produce immune response through ADCs. It is best described through the company material:

Immunosynthen, Mersana’s proprietary STING agonist platform, generates systemically administered ADCs that locally activate STING signaling in both tumor-resident immune cells and in antigen expressing cells, unlocking the anti-tumor potential of innate immune stimulation. Through the delivery of a novel immunomodulatory STING agonist, ADCs created with our Immunosynthen platform have the potential to address the challenges of efficacy, delivery and tolerability.

These technologies have been able to attract a number of R&D departments of big pharma. In February 2022, Mersana signed a collaboration deal with Janssen, using the latter’s antibodies for up to three antigens with Dolasynthen ADCs, with Janssen leading development, manufacturing and commercialization worldwide. The Merck KgaA deal came about in 2014, utilizing Dolaflexin for up to six target antigens. The Janssen deal produced an upfront fee of $40mn, and may result in development milestone payments of $501mn and regulatory milestone payments of another $530mn for all three antigens, plus mid-single digits to the low-double digits on future net sales of ADCs. The Merck deal had $12mn (see 10K page 12) in upfront payment (it was an early deal for Mersana, and corporate presentation says $30mn), $3mn in milestone payments so far, and may generate another $777mn in milestone payments, including development and regulatory. Royalties are low- to mid-single digit percentages on net sales. A new deal with GSK was signed last year, with $100mn upfront, $1.3bn in milestones and royalties. The GSK deal is for STING compounds, which is a space that has not had much solid data after the failure of Aduro’s operations. GSK has a small molecule STING agonist called GSK3745417, so there’s a lot of synergy here. Other companies with STING molecules include Takeda and Codiak. For a good discussion, see here.

As the company progresses, however, you can see that they are able to command better deal values for themselves.

Lead candidate UpRi has a registrational UPLIFT trial top-line readout in platinum-resistant ovarian cancer in mid-2023. If successful, the company will submit its first BLA at the end of 2023.

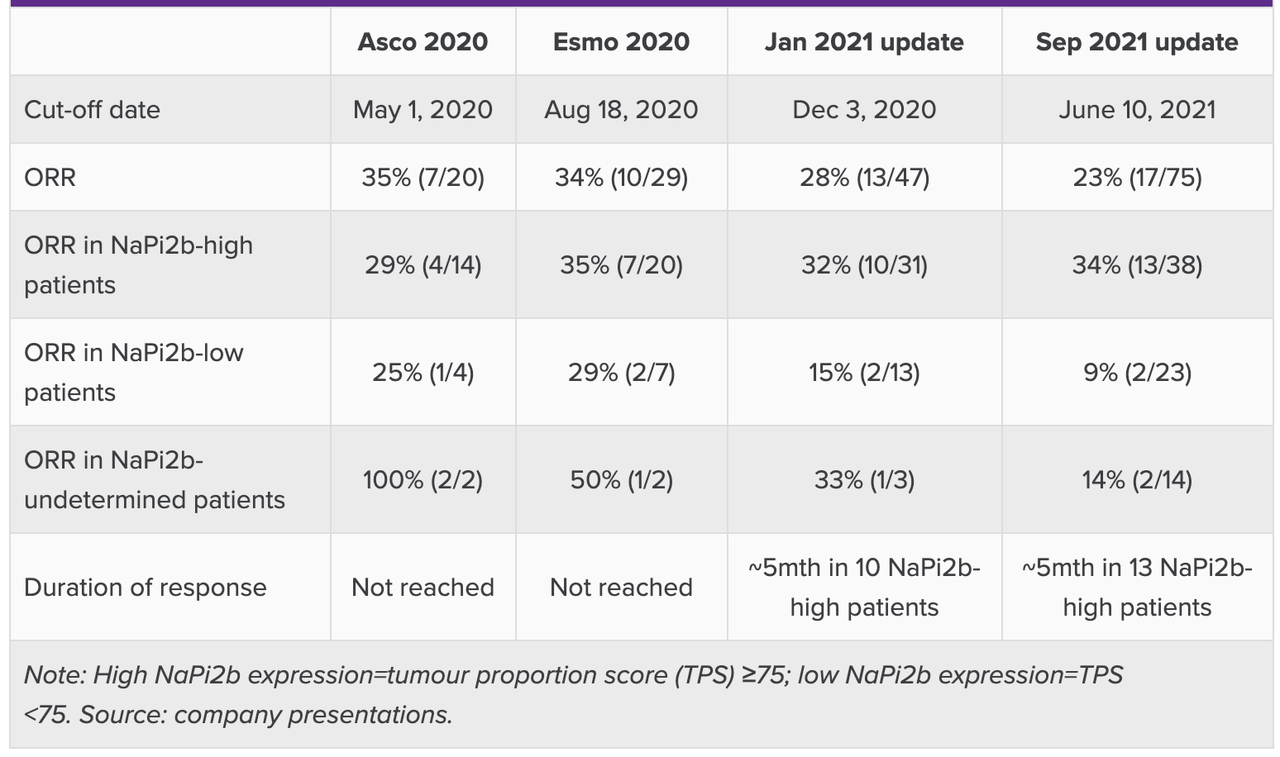

In 2021, data from UpRi was published, which caused the stock to drop significantly because the data was lackluster in the overall population, with ORR actually going down over time at the highest dose of 43 mg/m2. However, if we take the high NaPi2b expressers (which is logical because UpRi is a NaPi2b targeting molecule), and if we take the 36mg/m2 dose (no particular logic), then the data in this population of heavily pretreated ovarian cancer patients is very competitive. Here’s the data:

UpRi trial data (Evaluate)

Recall that this trial is being done in patients who have not seen benefit after four lines of therapy. According to Evaluate, “The current standard of care for this population is single-agent chemotherapy, and the prognosis is not good, with response rates of 4-12%, median progression-free survival of three to four months, and median overall survival of less than one year.” In that respect, the data is very competitive, although duration of response could have been better. Evaluate also says, “However, the data look unimpressive versus the 5.5-month duration of response seen with Roche’s now-abandoned NaPi2b-targeted ADC, RG7599 (lifastuzumab vedotin).”

Safety also was a concern, with two treatment-related deaths from pneumonia, which caused a now-lifted trial hold in 2018. This was a very sick patient population, so perhaps the safety profile is acceptable, but it is barely so, and investors could have done with a better safety profile.

Financials

MRSN has a market cap of $562mn and a cash reserve of $290mn. Research and development (R&D) expenses for the third quarter of 2022 were $50.6 million, while general and administrative (G&A) expenses were $14.6 million. That gives them a cash runway of another 4-5 quarters.

Bottomline

I started out liking Mersana’s science (which is why I spent some text discussing it), however, biotech being as unpredictable as the human body, its trial data so far hasn’t exactly lived up to the promise. This happens; maybe a few years down the line, another indication being explored will hit it off with the technology. But all these deals have taken the stock up quite a bit. I think this is fairly valued at these prices for what we have seen so far. The value does not take in the promise as much as the company would have liked, I am sure; but what proof we have of the concept, this looks correctly valued. I will continue looking at Mersana with interest, and if data derisks the stock, I will buy. I will not buy because some other big pharma comes down and spends another hundred million on the promise. They can afford to do that; I am a poor retail investor, and I don’t have that luxury.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment