Justin Sullivan

Our view

McDonald’s Corporation (NYSE:MCD) is known globally for its famous golden arches, delicious fries and, most of all, its value for money menu. It’s share price, however, would definitely look out of place on its savers menu.

The business characteristics of McDonald’s are an investor’s dream: a truly globally recognizable brand, a franchise model which limits downside but captures upside, and free cash flow conversion that allows it to return bucket-loads of cash to investors through an ever-increasing dividend and share repurchases.

There is no doubt that McDonald’s is everything we like to see in a business. However, the quality of the business is only one side of the equation in any investment decision. Equally, or more important, is the price you pay. As Warren Buffett famously said: “Price is what you pay. Value is what you get.”

In the case of McDonald’s, we just don’t think there is enough of the latter to justify the former. Whilst we appreciate that a high quality company like McDonald’s should command a premium valuation, we do not feel the current valuation provides a sufficient margin of safety in the context of the company’s growth prospects.

As value investors, our number one priority is to maximize long-term capital appreciation by investing in business where we are certain they are undervalued. In the case of McDonald’s, we are not confident that we would be compensated with a level of return which we consider satisfactory. We would prefer to retain the ability to deploy our capital in other highly probable high return opportunities. For that reason, we rate the share as a “sell”.

Each investor must consider this in the context of their own investment objectives. For investors who value capital preservation and income above all else, we accept that McDonald’s is an attractive proposition with its recession-proof business model and robust dividend history. In that case, we can see the justifications for continuing to hold.

Business review

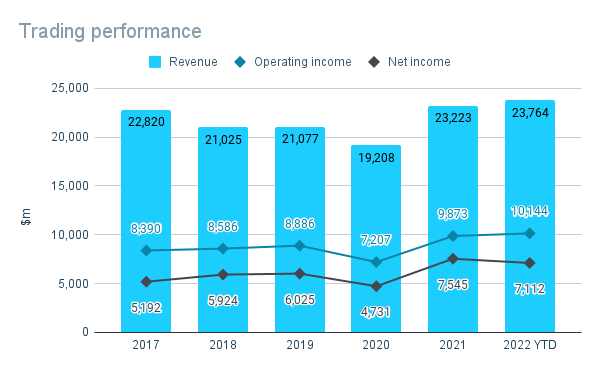

Improving margins

Prepared by author. Data from company reports

Prior to 2021, McDonald’s had been experiencing a period of declining or flat revenues. And as the world felt the impact of the global Covid-19 pandemic in 2020, even McDonald’s wasn’t immune with revenues falling a further 9% that year. However, the company emerged from the pandemic stronger and 2021 marked the beginning a recent growth revival. Revenues grew in excess of 20% in 2021, exceeding levels not seen since prior to 2017.

Despite the disappointing revenue growth in recent years, net income has grown by around 45% in the four years to FY21 – equivalent to a CAGR of 10%. A key driver of this increased has been the transition from company-operated restaurants to franchised restaurants, which contribute significantly higher margins (see below), as well as in increase in the volume of sales at existing restaurants.

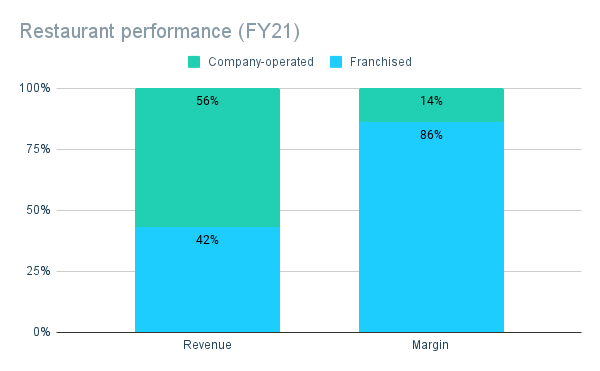

The fantastic franchise

Prepared by author. Data from FY21 annual report

McDonald’s generates revenue from two key areas: (i) its company-operated restaurants and (ii) its franchised restaurants. Despite over 90% of McDonald’s restaurants being operated under a franchise, they account for less than half of the company’s total revenue. However, due to the structure of these franchise agreements, franchise restaurants provide McDonald’s with revenue with very little incremental costs, meaning they contribute almost 90% of the company’s margin.

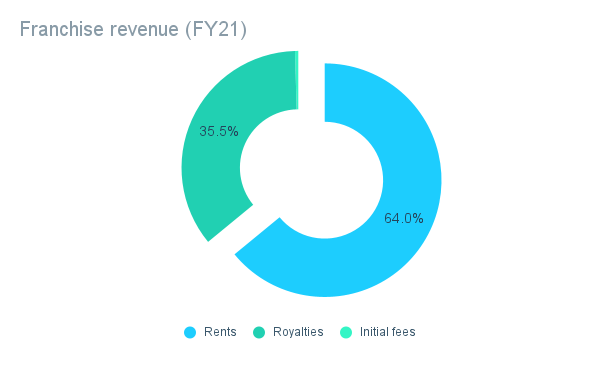

Ronald The Landlord

Prepared by author. Data from FY21 annual report

The fees paid to McDonald’s by franchises include an initial fee, rent, and royalties. Rent includes a fixed element and a variable element based on revenues, whilst royalties are entirely revenue-dependent.

A majority of franchise restaurants are under a “conventional” franchise, whereby McDonald’s owns or leases the land and building from which the franchise operates. The rent payment received from franchisees actually represents the most significant element of the revenue received by McDonald’s from its franchises, accounting for over 60% of revenue from franchises in 2021 – or more than one third of the total revenue of the McDonald’s company.

The benefit of this model is that it gives McDonald’s some of the characteristics of a real estate business, providing visible and stable income streams over long time frames – typically 20 years under a typical franchise agreement. Minimum rental payments for the period 2022-2026 are around $3 billion p.a., equivalent to 13% of revenue (based on FY21 levels).

Of course, franchised restaurants need to be financially viable in order to be able to meet these contractual payments, but the franchising arrangement limits some of the company’s downside risk through a fixed rental payment, whilst allowing it to benefit from upside through the variable fee elements.

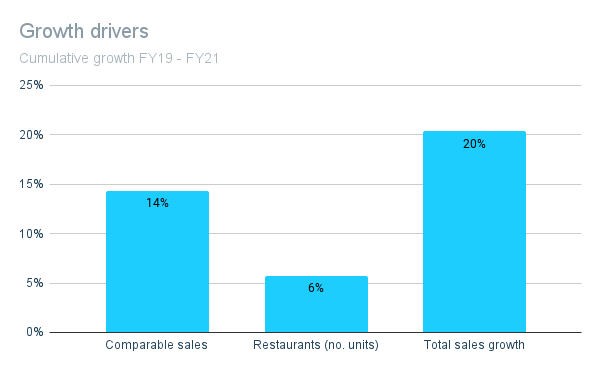

Driving the growth

Prepared by author. Data from company reports

Whilst overall revenue growth over the last five years has been muted, revenue is up around 20% since FY19. This recent growth has been broad-based, driven by increased sales at existing restaurants as well as continued expansion of the number of restaurants.

The growth has been supported by the new growth strategy Accelerating the Arches launched in 2020. Under this program, there is a focus on the MCDs: Marketing; Core menu; and Digital.

The latter – which includes the MyMcDonald’s app, drive-through, and McDelivery – has become an increasingly important part of the McDonald’s experience. Sales from digital channels across the company’s top six markets have increased from nearly 20% of sales to nearly 33% of sales in as reported in the results for Q2 of 2022.

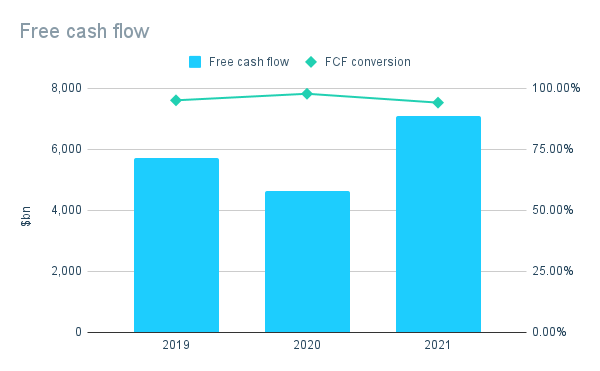

Cash cow

Prepared by author. Data from company reports

The free cash flow generation and conversion of McDonald’s is an investor’s dream. Unlike many business where a significant proportion of profits need to be reinvested to maintain the company’s competitive position, almost 100% of the profits generated by McDonald’s convert into free cash flow which can be returned to shareholders through dividends and/or repurchases.

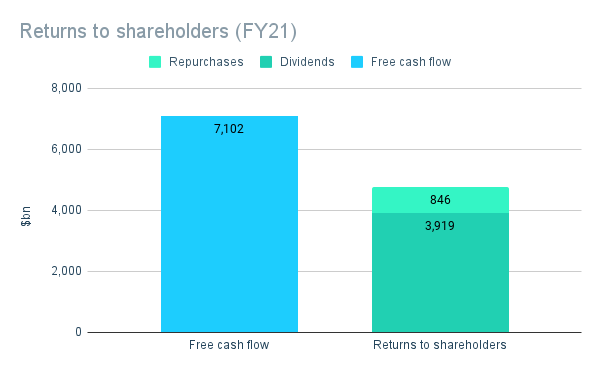

Prepared by author. Data from FY21 annual report

In FY20 and FY21, the company returned almost 80% of its net income to shareholders. The majority of this was by way of dividend, which the company has continually paid in increasing amounts for over 40 years.

The remainder was through the current share repurchase program. Authorized by the Board in December 2019, it permits the company to repurchase up to $15 billion of its outstanding shares. Repurchasing activity has so far been limited, with $13.3 billion – equivalent to 7% of the company’s current market capitalization – still to be completed as of the end of Q2 2022.

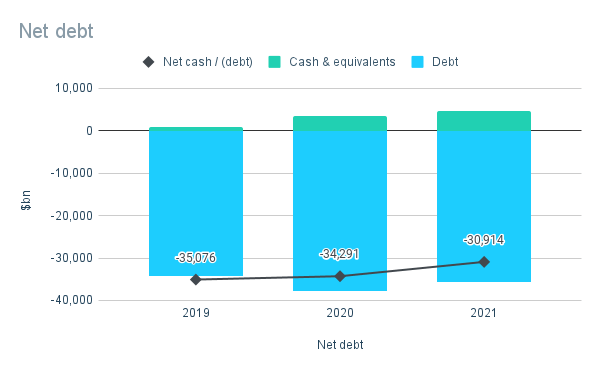

Net liabilities?

Prepared by author. Data from company reports

A notable aspect of the balance sheet of McDonald’s is that it has negative shareholders’ equity or net liabilities i.e. its liabilities are greater than its assets. In many cases, this would be a warning sign of the poor financial health of a company. However, in the case of McDonald’s, it is actually an indicative of the remarkable strength and resilience of the business.

In effect, the creditors of the company are funding the entire capital requirements of the business, leaving shareholders free to entirely withdraw any capital that was invested in the business. Accordingly, the company employs a large amount of debt with almost $31 billion in net debt (excluding lease obligations) as of 31 December 2021. However, the company generates consistent and significant free cash flow generation, which would be sufficient to repay all of its debt in around five years (at FY21 levels).

The net liability position presented on the company’s balance sheet is actually a product of accounting policies rather than economic reality. All of the land and property owned by the company is valued at cost less depreciation on the balance sheet, meaning it is almost certain that the company’s property assets are significantly understated on its balance sheet. If these were to be revalued today, it is likely that the company would be in a significant net asset position.

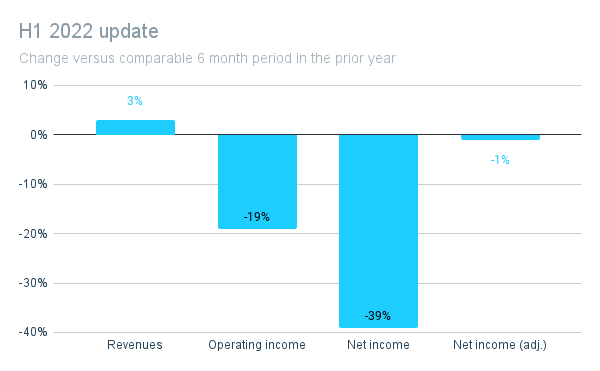

H1 FY22 update

Prepared by author. Data from Q2 2022 earnings release

On 26 July 2022, the company reported mixed performance for the six months to 30 June 2022. Despite continued revenue growth, operating income was down nearly 20% whilst net income was down nearly 40%.

As you might expect, the headline figures don’t tell the whole story. During the first half of 2021, the company took the decision to cease operations in Ukraine and Russia. This was followed by the decision to sell the Russian business, which resulted in a pre-tax charge of $1.2 billion. Excluding the impact of this and other non-recurring items, the net income for the period was largely flat versus the same period in the prior year.

On a positive note, the company continued to leverage its digital capabilities, with the share of total restaurant sales from Digital continuing to grow, up from around 25% in FY21 to over 33% in Q2 FY22.

Risks

We see the key risks to investors to include:

Health conscious consumers

McDonald’s has come to be a by-word for unhealthy food. As consumers become increasing health conscious, the company will need to evolve to avoid losing market share to healthier alternatives. That being said, the company has continued to evolve and cater to changing consumer preferences for decades and we would expect that it continues to do so.

Inflation/macroeconomic factors

Even a recession-resistant business like McDonald’s won’t be completely immune to a highly inflationary or otherwise adverse macroeconomic environment. McDonald’s has already increased its prices in some key markets such as the United Kingdom. Reduced consumer demand and/or increasing prices could reduce sales and profits. However, as a budget-friendly option, McDonald’s may actually benefit from a transition by consumers away from more expensive eating out options.

Valuation

Our valuation approach centers around determining the true underlying earnings power of the business – or “owner earnings”. In the case of McDonald’s, we consider reported net income to be a reasonable proxy as almost 100% of it converts to free cash flow.

The current share price of $262 gives the company a total market capitalization of $194 billion as of 4 August 2022. This represent a price-to-earnings multiple of 26x based on FY21 net income – or 27x based on year-to-date earnings at the end of Q2 2022.

We do not believe valuations are an exact science or that a business has a distinct calculable intrinsic value. Instead, our approach is to consider the implied return under a given scenario and apply a judgement or weighting regarding our confidence in the likelihood of it being achieved.

Since 2017, the company has grown its net income at a CAGR of 10%. For the purpose of our analysis, we have assumed this growth continues for the next 10 years. We have also assumed that the company maintains its current dividend payout ratio of 65% and that the announced share repurchase plan is completed.

We believe it is important not to assume that historical valuation multiples, particularly those witnessed in low interest rate environments, will continue indefinitely. In the case of McDonald’s, we feel that a price-to-earnings multiple of 18x is a reasonable assumption, which recognizes the strength of the business without assuming inflated valuation multiples will persist.

Under this scenario, investors at the current price would see a total return, including dividends and repurchases, of 127% over a 10-year period – and implied compound annual return of only 9%. Whilst we maintain a positive outlook for continued growth over the long-term, we do not feel that the current growth prospects are adequate to justify the current premium price.

Conclusion

There are many reasons for investors to love McDonald’s and we would love to own a slice of the business. Unfortunately, the current valuation seems to be inflated by demand for a stable business amidst global macroeconomic uncertainty.

As value investors, we feel that retaining the ability to deploy our capital in other opportunities with a better risk/reward profile outweighs the benefits of buying stability and income at an inflated price.

Before you go, we need to ask you for a favor. As a new contributor to Seeking Alpha, we would really value your feedback on our content. Please leave a comment to let us know if there are any aspects which you do or don’t like about or analysis, or if you would like to us to elaborate further on any particular area.

Be the first to comment