Matson, Inc. (NYSE:MATX) is investing a lot of money in capital expenditures, which may increase future capacity. Management is also offering new services, and may enter new regions in Asia. In my view, the company has cash in hand to conduct some acquisitions to boost growth. In any case, I believe that the company is somewhat undervalued right now. In my view, the guidance given for the year 2022 implies higher price marks.

Matson Is Investing A Significant Amount Of Money To Renovate Its Facilities

Founded in 1882, Matson offers ocean transportation and logistics services. The company primarily operates in Hawaii, Alaska, and Guam, but also offers services in Okinawa, Japan, China, and Southern California.

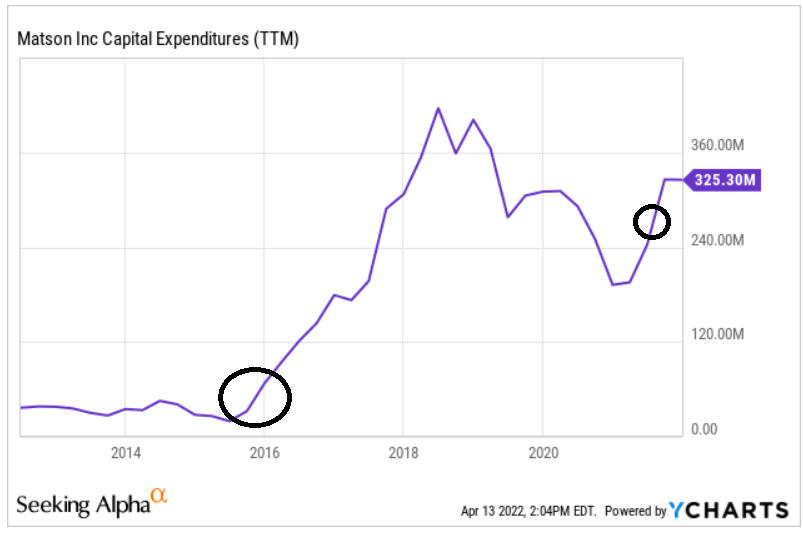

I believe that it is a great time to review the company’s business model. Keep in mind that Matson significantly increased the total amount of capital expenditures from 2018. Also, the eventual increase in capacity will likely lead to an increase in services and revenue reported by Matson:

Ycharts

In 2020, the company renovated its facilities in Hawaii, and from 2022 to 2024, management expects to make further expansion. In my view, further capital investments may retain the attention of investors, which may lead to demand for the stock:

During 2020, Matson completed the first phase of its program to modernize and renovate its terminal facility at Sand Island, Honolulu, Hawaii.

During 2021, as part of the second phase, Matson completed the installation, energization and transition to a new redundant main switchgear.

Matson expects to expand into Pier 51A and portions of Pier 51B after Pasha Hawaii (“Pasha”) relocates to the newly constructed Kapalama container terminal facility planned for 2024. From 2022 to 2024, Matson will be performing surveying, planning and design work in preparation for this expansion. Source: 10-k

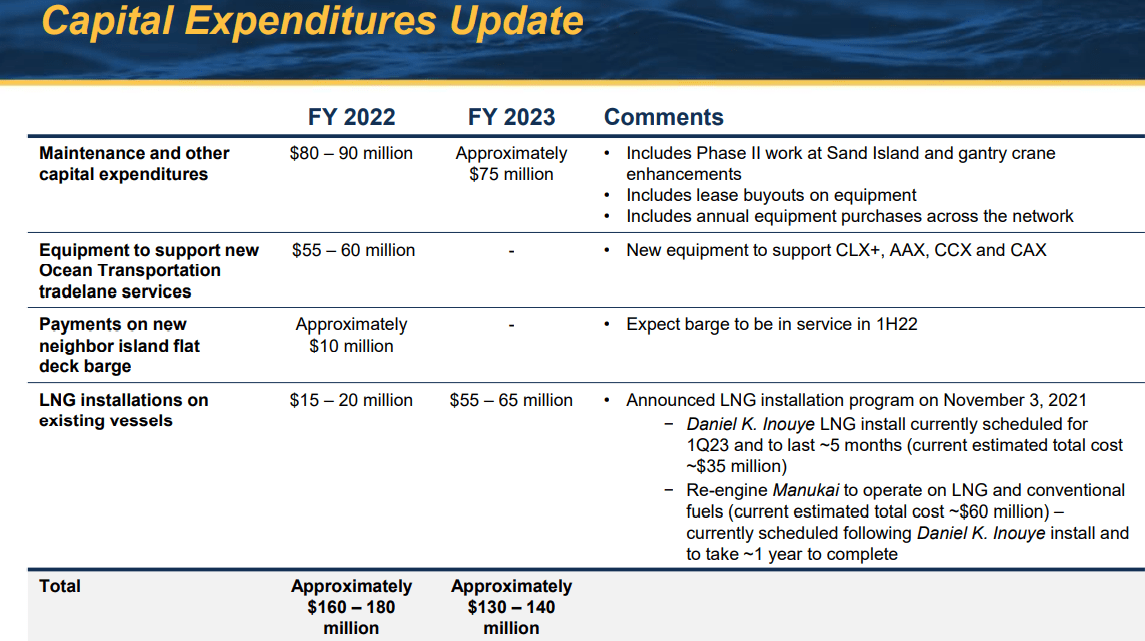

Management noted that in 2022 and 2023, it expects to invest close to $180 million and $140 million respectively for a new LNG installation program, new equipment, and further enhancements:

Fourth Quarter 2021 Presentation

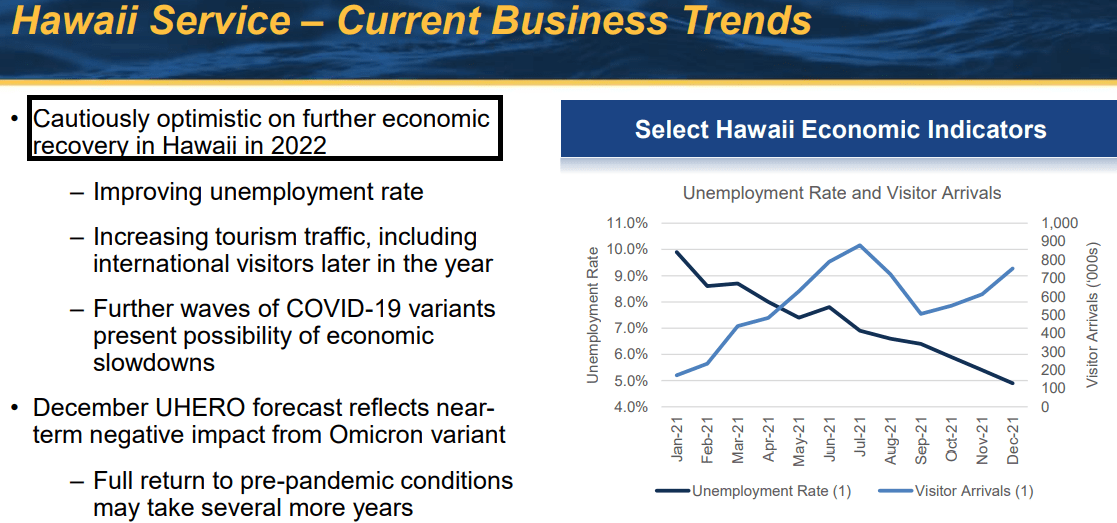

With the previous announcements, it is quite appealing that management expects continued rebound in tourism in Hawaii, which would lead to further increase in sales growth in 2022. Most analysts agree with the optimism exhibited by Matson as they expect a significant sales growth in 2022:

Continued rebound in tourism and Hawaii economy despite slowdown early in the quarter due to state’s efforts to address COVID-19 Delta variant. Source: Fourth Quarter 2021 Presentation

Fourth Quarter 2021 Presentation

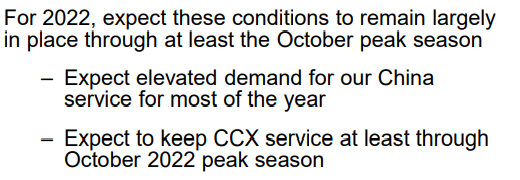

Finally, it is also quite beneficial that management expects economic conditions to evolve positively in China, where demand is expected to remain elevated for 2022:

Fourth Quarter 2021 Presentation

Analysts Expect Significant Acceleration Of Growth In 2022

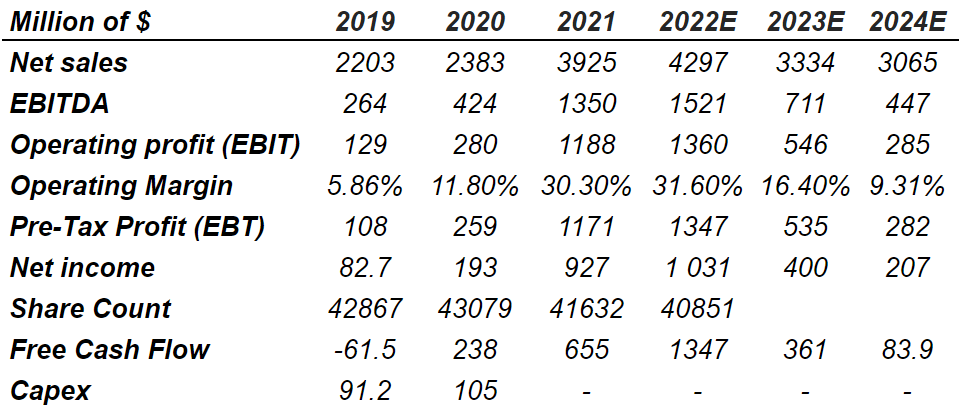

After a 65% increase in sales in 2021, estimates include sales growth in 2022, and certain decline in growth in 2023 and 2024. In sum, by 2024, investors expect $3 billion in sales. The EBITDA margin will likely stay between 35% and 15% from 2022 to 2024. Finally, let’s note that Matson is expected to deliver positive net income in 2023 and 2024, and free cash flow will also remain larger than zero.

Marketscreener.com

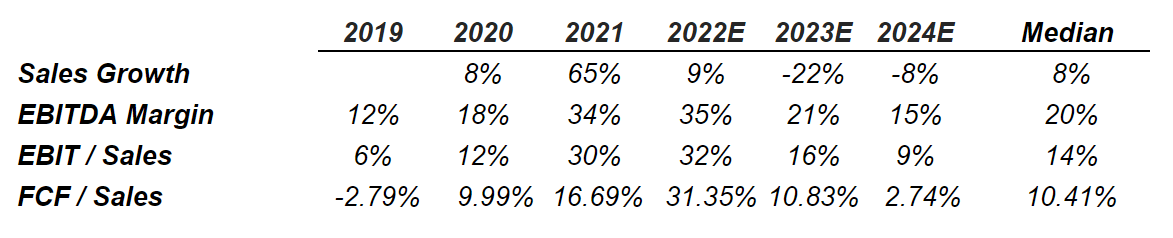

I obtained some statistics that served me in my financial modeling. The median sales growth from 2020, including the expectation of analysts, was equal to 8%. The median EBITDA margin is equal to 20%, and Matson’s free cash flow margin is equal to 10%. In sum, I believe that in the long run, stats show that Matson is a profitable entity.

Author’s Compilations

Conservative Assumptions Indicate An Implied Valuation Of $98

Under normal circumstances, I expect management to launch new services in Asia like the Alaska-Asia Express or the China-California Express. With a significant amount of cash in the balance sheet, Matson will also be able to invest in new regions. New initiatives and more investments in capacity will most likely lead to revenue growth.

In September 2020, Matson launched its Alaska-Asia Express (“AAX”) service that provides carriage of dry and frozen seafood from Dutch Harbor, Alaska to Ningbo and Shanghai, China.

In July 2021, Matson launched a temporary, third expedited service to the U.S. West Coast with the China-California Express (“CCX”) service to meet continued high market demand. Source: 10-k

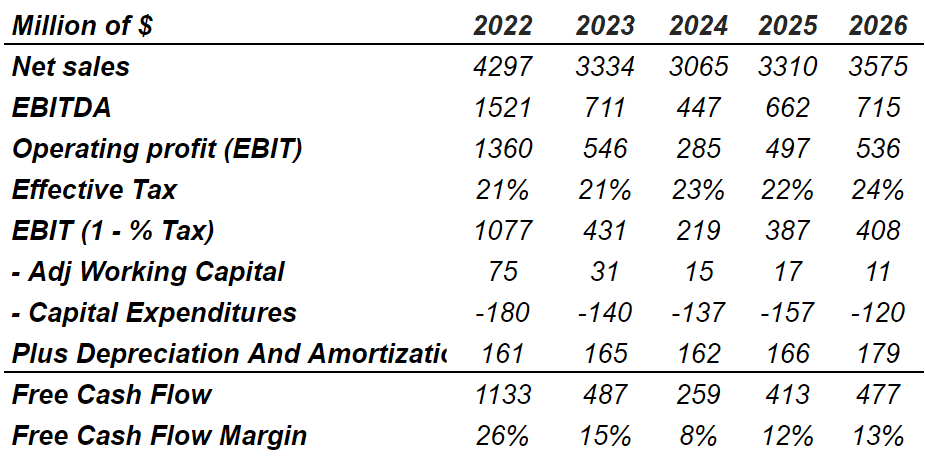

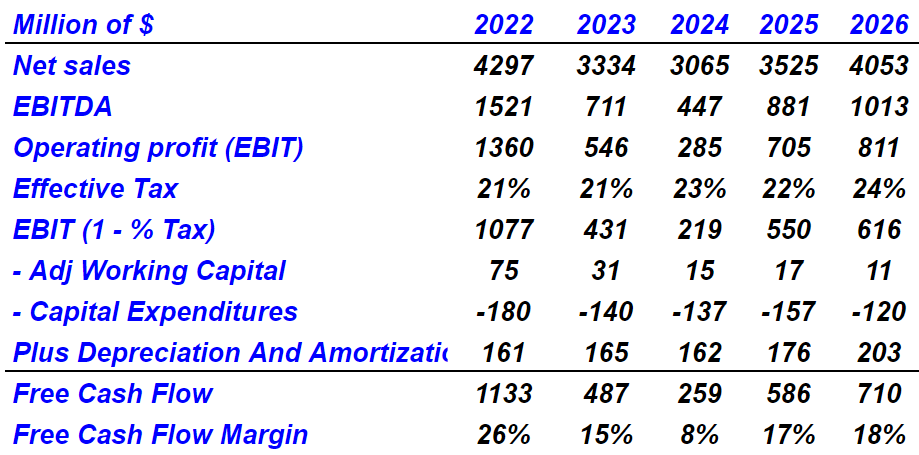

Under my base case scenario, I assumed 2026 sales of $3.57 billion, 2026 EBITDA margin of more than $711 million, and growing effective tax. Also, with capital expenses around $180 million and $120 million, and changes in working capital of -$75 million and -$11 million, the free cash flow will likely be between $1.2 billion and $257 billion:

Author’s Compilations

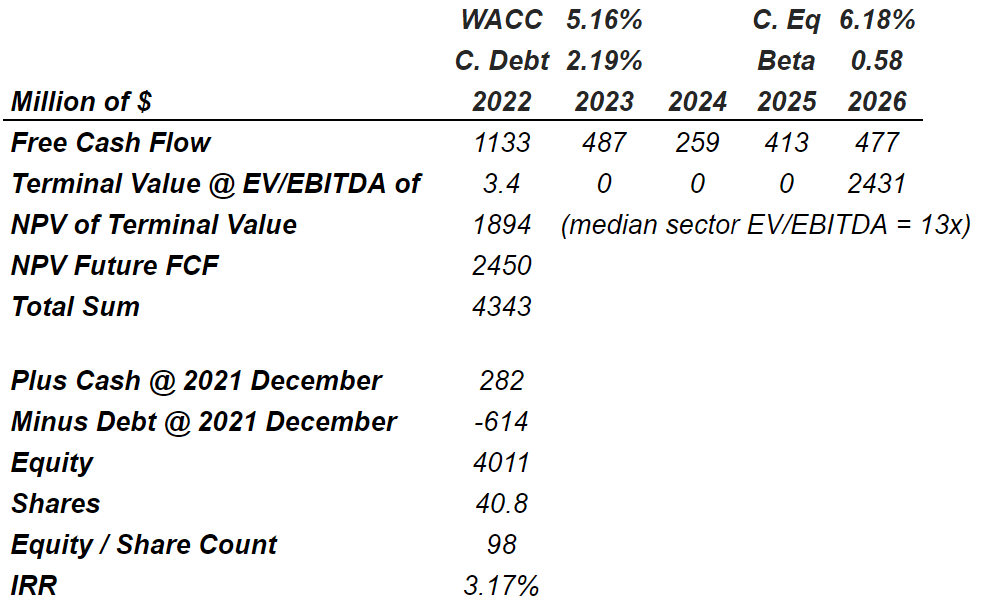

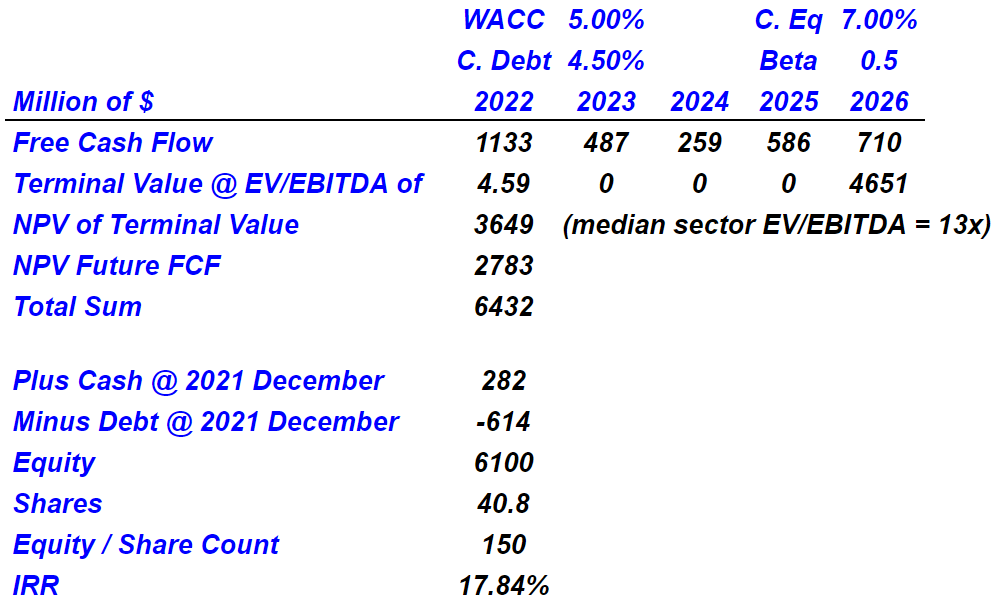

My capital asset pricing model also included a cost of equity of 6.18%, cost of debt of 2%, and a beta of 0.58. In my view, other investors may use different assumptions, but their weighted average cost of capital will not be that different from that of mine.

The company is currently trading not far from 3x EBITDA with the median EV/EBITDA in the industry being at 13x. There seems to exist a certain lack of liquidity that is pushing the company’s valuation down. I used an exit multiple of 3.4x, which I assumed conservative. My results included an implied market capitalization of $98 per share.

Author’s Compilations

Very Optimistic Case Scenario Leads To A Valuation Of No More Than $150

Under the best case scenario, I would expect increases in capacity and new services in Asia. I also expect new vessel management services with governments like that from the United States or any other country in the world. Let’s note that the company is already working with the U.S. Department of Transportation Maritime Administration:

Matson contracts with the U.S. Department of Transportation to provide vessel management services to manage and maintain three Ready Reserve Force vessels on behalf of the U.S. Department of Transportation Maritime Administration. Source: 10-k

Besides, under this particular case, I would also expect a lot of inorganic growth, which will likely lead not only to more sales growth, but also more free cash flow margin. Matson already reports a lot of goodwill in the balance sheet, and M&A is among the company’s core strategies. Hence, I believe that management has expertise of integrating new teams:

The Company’s growth strategy includes expansion through acquisitions. Source: 10-k

Under the previous optimistic assumptions, I obtained 2026 sales of $4.05 billion, 2026 EBITDA of $1 billion, and 2026 free cash flow of $710.5 million.

Author’s Compilations

I also assumed a weighted average cost of capital of 5%, along with an exit multiple of 4.5x, which implied an implied enterprise value of almost $6.5 billion. The implied equity valuation would most likely stay around $150 per share.

Author’s Compilations

The Worst Figures That I Could Imagine Lead To A Valuation Of $61

Changes in the regulation and agreements between countries with regards to the way ports are operated could have a material adverse effect on Matson. Trade negotiations with respect to the Jones Act are right now the largest concern for management:

If maritime cabotage services were included in the General Agreement on Trade in Services, the United States-Mexico-Canada Agreement, or other international trade agreements, or if the restrictions contained in the Jones Act were otherwise altered, the shipping of cargo between covered U.S. ports could be opened to foreign-flagged or foreign-built vessels and could have other adverse impacts to our business.

The Company’s business would be adversely affected if the Company were determined not to be a U.S. citizen under the Jones Act. Source: 10-k

New entrants in the industry could make free cash flow margins decline, or Matson may lose market share. In either way, the competition could be quite detrimental for the company’s bottom line and Matson’s valuation:

For example, in 2020 and 2021, in response to rising demand, several new carriers entered the China tradelane in competition with the Company’s China service. The entry of a new competitor or the addition of new vessels or capacity by existing competition on any of the Company’s routes could result in a significant increase in available shipping capacity that could have an adverse effect on the Company’s volumes and rates. Source: 10-k

Finally, Matson’s income statement could suffer substantially if fuel prices increase to a sufficient level. The company may react by not operating a bit less because its activity may not be that profitable, which may reduce future sales, and may lead to a reduction in the company’s valuation:

Increases in the price of fuel may adversely affect the Company’s results of operations. Increases in fuel costs also can lead to increases in other expenses, such as energy costs and costs to purchase outside transportation services. Source: 10-k

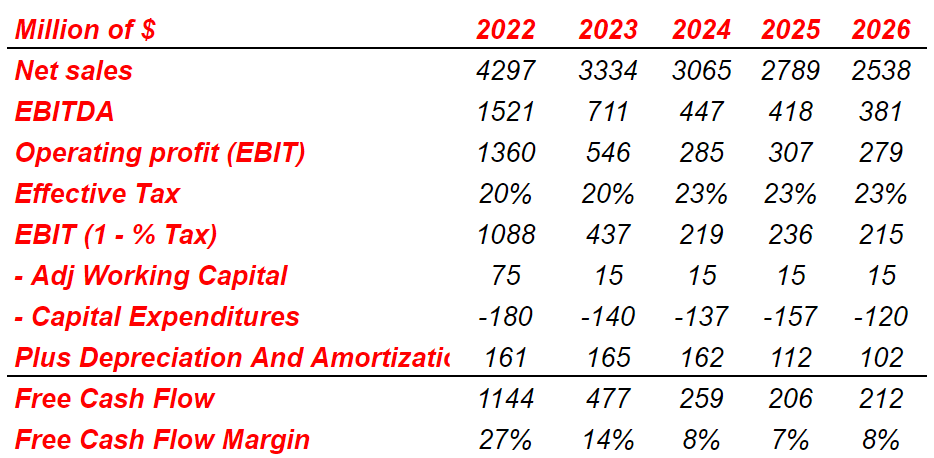

Under the worst conditions, I assumed that revenue would decline from $4 billion in 2022 to less than $2.6 billion in 2026. Also, the 2026 operating profit should stay close to $279 million, and the free cash flow margin should not grow from 8% from 2024 to 2026.

Author’s Compilations

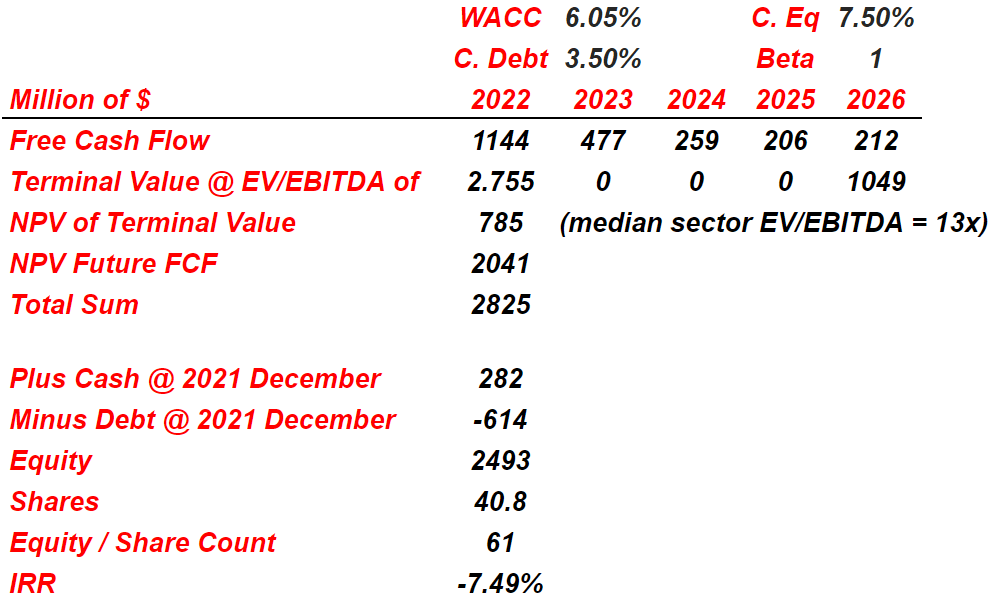

Under a more pessimistic capital asset pricing model, I obtained a terminal value of $786 million with an implied valuation of $2.82 billion. Finally, the implied share price should stay close to $61:

Author’s Compilations

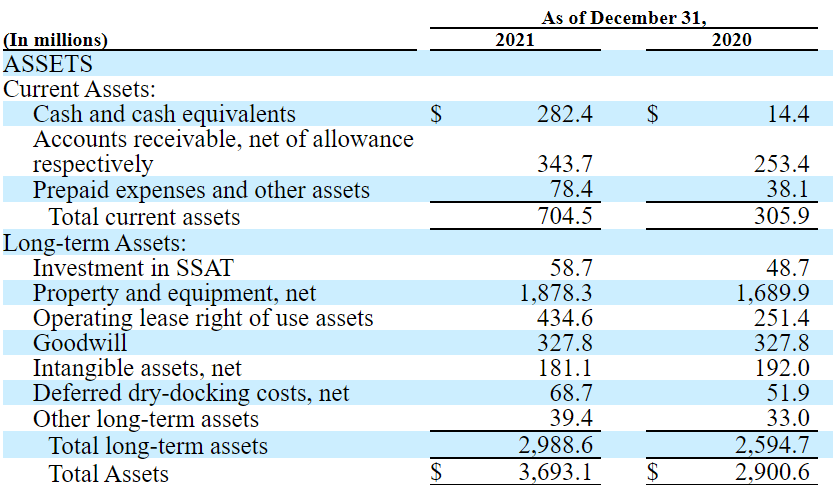

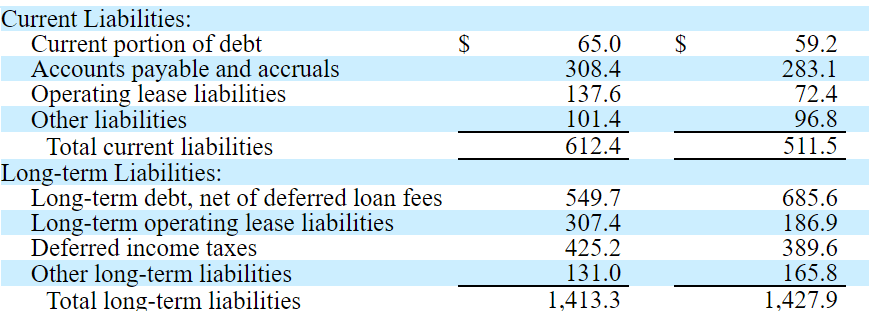

Balance Sheet: Long Term Debt Declined While The Total Amount Of Assets Is Increasing

With an asset/liability ratio of 2x-3x, $282 million in cash, and $1.87 billion in property and equipment, Matson’s financial health appears beneficial.

10-k

It is also quite appealing that the long-term debt declined from $685 million in 2020 to $549 million in 2021. Further reductions in debt will likely be celebrated by the market. As a result, the company’s EV/EBITDA multiple may increase as the financial risk would lower.

10-k

My Takeaway

Matson is reporting a lot of new capital expenditures, which will likely accelerate revenue growth as capacity increases. Besides, if management also continues to offer new services in new regions, and conducts M&A acquisitions, investors will likely take a look at the business model. With all this in mind, right now, I believe that we could see significant stock price appreciation when more investors learn about the guidance for 2022. My DCF model showed that there is likely undervaluation in the stock.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment