Wirestock/iStock via Getty Images

While 2022 was supposed to be MAG Silver’s (NYSE:MAG) year, with commercial production expected to be reached at Juanicipio, 2022 was instead a little disappointing. This was because we saw much lower throughput rates as the plant awaited its connection to the national power grid. Fortunately, its partner Fresnillo (OTCPK:FNLPF) made room for ore at its Saucito and Fresnillo plants, allowing MAG Silver to report positive earnings in FY2022 despite the hold-up. In addition, the company didn’t rest on its laurels, making a strategic move to acquire Gatling Exploration, a company with an intriguing project in the Abitibi region of Canada, just east of the Kirkland Lake Camp.

Fortunately, despite the connection hiccup, MAG Silver outperformed its peer group from a share-price standpoint, and it’s now entered the new year with two projects and a mine vs. one previously. In addition, the much-awaited connection to the grid is finally complete, meaning that investors have lots to look forward to, including higher production rates, a sharp increase in earnings, and drill results across its portfolio. Given MAG Silver’s unique position as having a carried interest in a world-class mine and the ability to self-fund its exploration properties while building a strong cash balance, I continue to see the stock as a top-3 name in the silver space.

Juanicipio Mine (Company Presentation)

Q3 Results

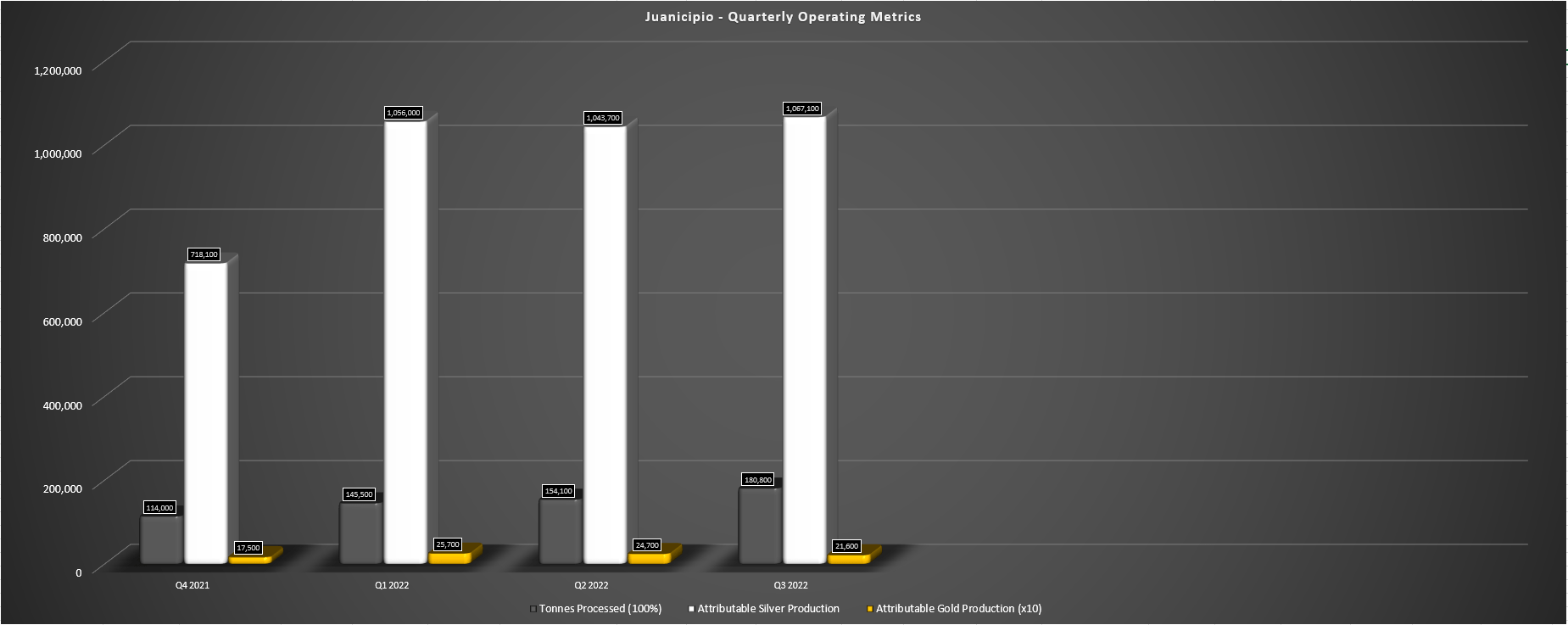

MAG Silver reported another solid quarter in Q3, with more than 1.05 million attributable ounces of silver produced and 2,100+ ounces of gold produced. Meanwhile, throughput on a 100% basis for Juanicipio ore was ~180,800 tonnes (stope and development material), a meaningful increase on a sequential basis which more than offset the lower mined silver grade in the period (513 grams per tonne). The result was that the operation enjoyed a solid quarter financially, with $25.2 million in gross profit for the mine on a 100% basis despite it running at just half of its planned throughput levels (~2,000 tonnes per day vs. ~4,000 tonnes per day).

Juanicipio – Quarterly Operating Metrics (Company Filings, Author’s Chart)

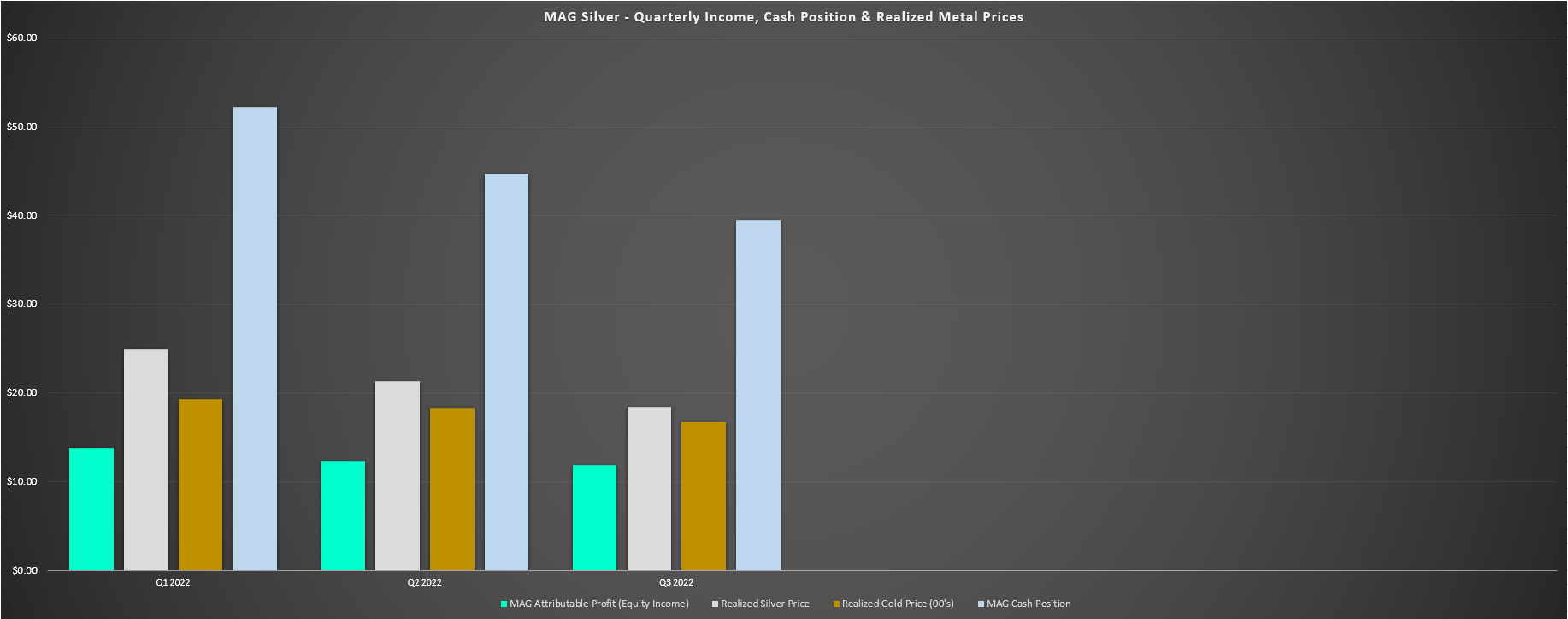

Looking at MAG Silver’s share of the mine’s profit, we can see that MAG Silver reported a net income of $8.2 million ($0.08) in Q3 based on ~$11.8 billion in equity income from its 44% stake in the operation. The result was that the company continued to maintain a strong balance sheet with over $42 million in working capital and $39.5 million in cash, and this was all despite gold and silver prices being crushed in the period, with an average silver price of just $18.36/oz and a gold price of $1,677/oz. Since metals prices have recovered nicely since then, and we can look forward to higher throughput beginning in Q1, I would expect a stronger Q4 and an even better Q1/Q2 2023.

MAG Silver – Quarterly Income, Cash Position & Metals Prices (Company Filings, Author’s Chart)

However, while these results were solid especially considering the sharp decline in metals prices, the major news in the quarter was that the electrical connection to the national power grid was finally completed and energized with full load commissioning underway. This is significant news for Juanicipio, given that its plant can process ~360,000 tonnes per quarter based on nameplate capacity, and Fresnillo hopes to reach full nameplate capacity during Q2. As the chart above shows, this would double the company’s throughput rate, resulting in annual attributable production of 8.0+ million ounces of silver this year, depending on how smooth the ramp-up is to commercial production levels.

Even assuming conservative metals prices, this should result in MAG Silver generating up to $100 million in free cash flow this year and annual EPS of more than $0.90 per share. Hence, MAG Silver is in a position to increase production and annual earnings on a year-over-year basis, and this significant increase in cash on its balance sheet might lead to the company considering some form of a return of capital to shareholders in 2024, assuming we do see a decent year for Juanicipio and metals prices in 2023. Plus, given that mining has already been ongoing for over a year, and the critical item was flipping the switch on the Juanicipio plant (vs. toll-milling to Saucito/Fresnillo), I would be surprised to see any real challenges.

Deer Trail & Larder Drill Programs

While it may have gone unnoticed by some investors, given that Juanicipio has been getting all the attention, MAG Silver signed an option agreement to acquire 100% of the massive Deer Trail Project in Utah, a 5,600-hectare project that includes the Deer Trail Mine (past-producing carbonate replacement deposit), and the Alunite Ridge Area, where gold-quartz and alunite (aluminum) veins were prospected and mined until 1945. However, in addition to looking for carbonate replacement deposit [CRD] mineralization, the company is optimistic that there could be a porphyry center nearby.

Deer Trail CRD Project (Company Presentation)

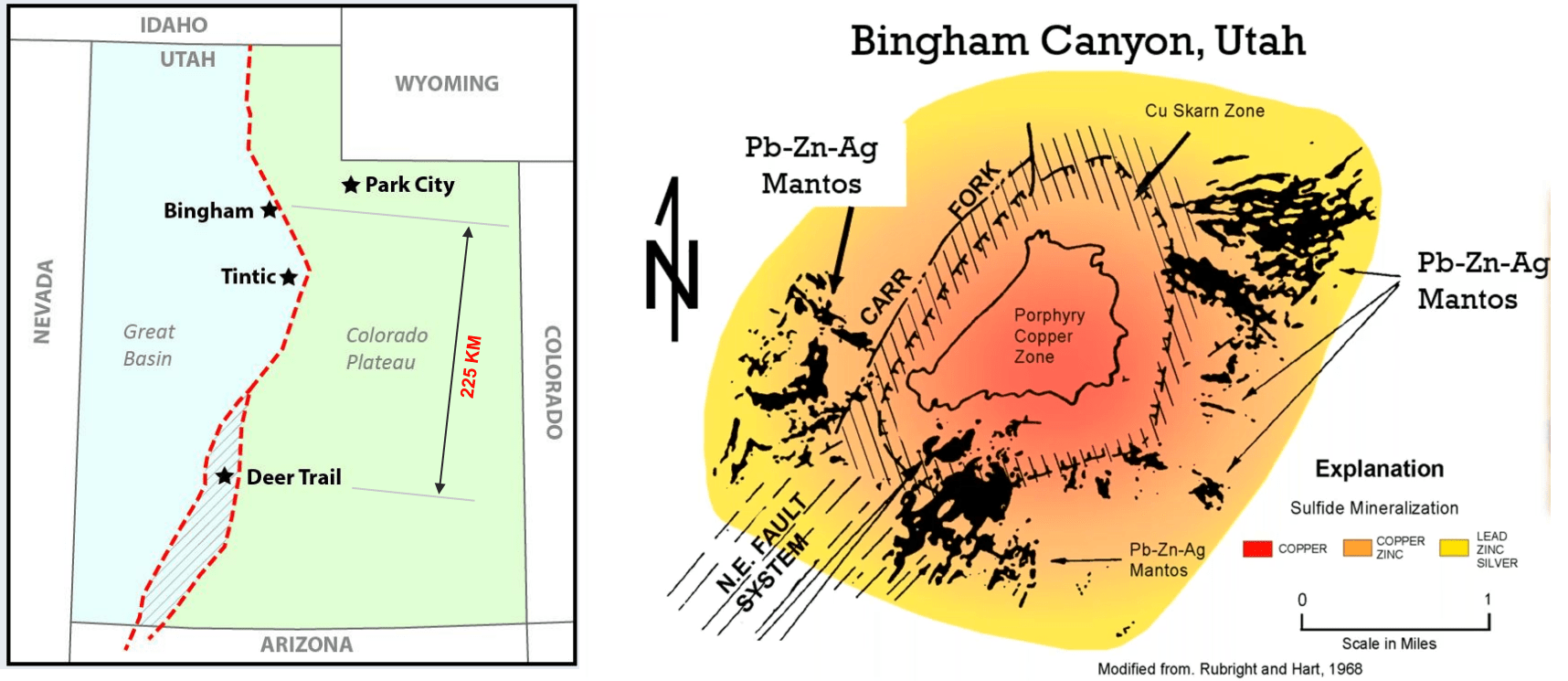

Notably, the company is applying the same overall strategy as Juanicipio and Larder at Deer Trail, which is hunting for a potential second mine next to monster deposits from a grade or scale standpoint. In Larder’s (Gatling Exploration) case, the area is known for its high-grade mineralization with Macassa and Upper Beaver to the west/northwest and other past-producing mines in the vicinity (Kerr-Addison). Meanwhile, Juanicipio lies next to the prolific Fresnillo District in Zacatecas, Mexico. In Deer Trail’s case, its address is arguably just as impressive, south of the famous Bingham Canyon Mine, Park City, and the Tintic District in Utah.

Deer Trail Location & Bingham Canyon CRD/Porphyry Hub & Spoke Model (Company Presentation)

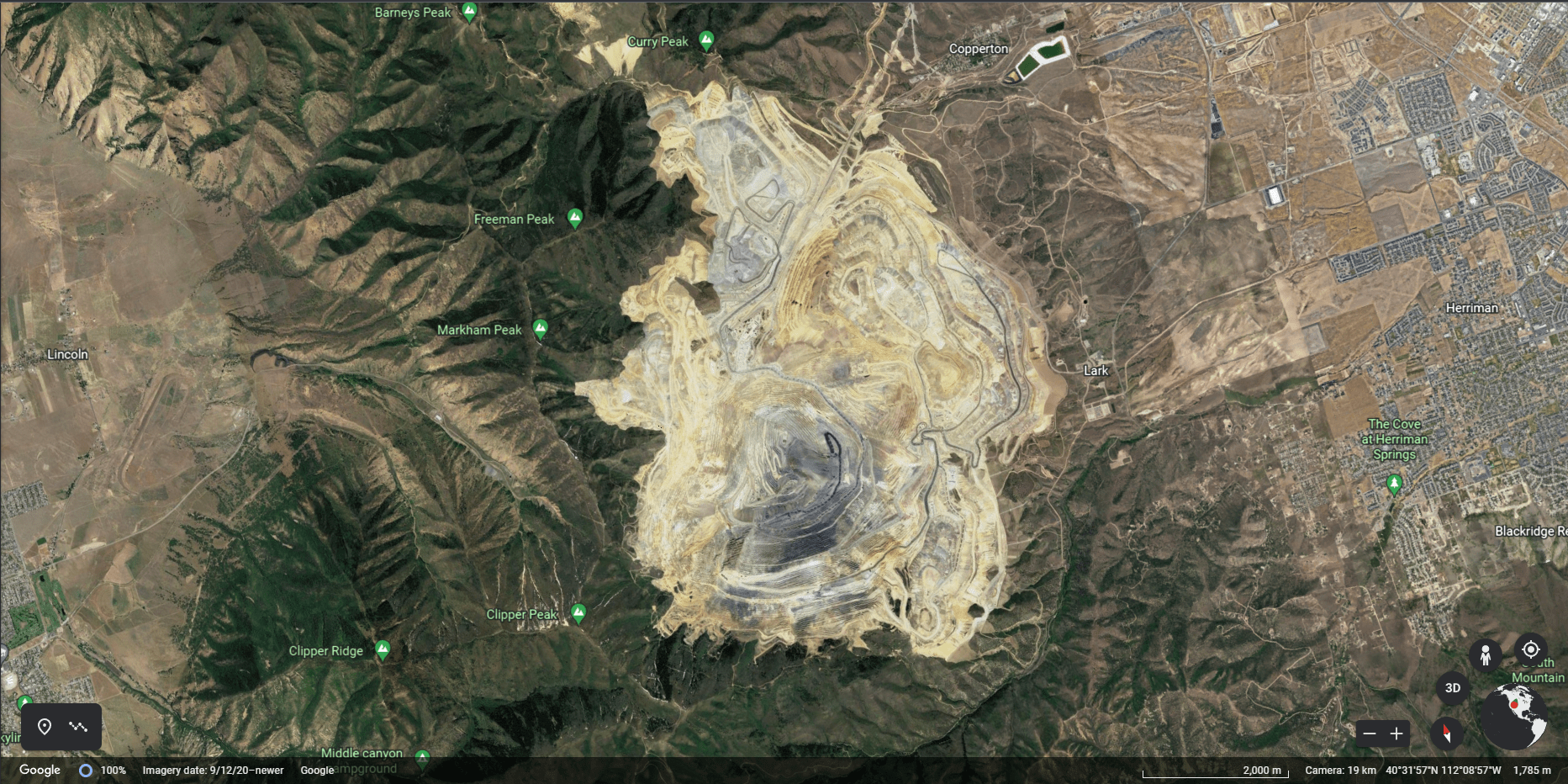

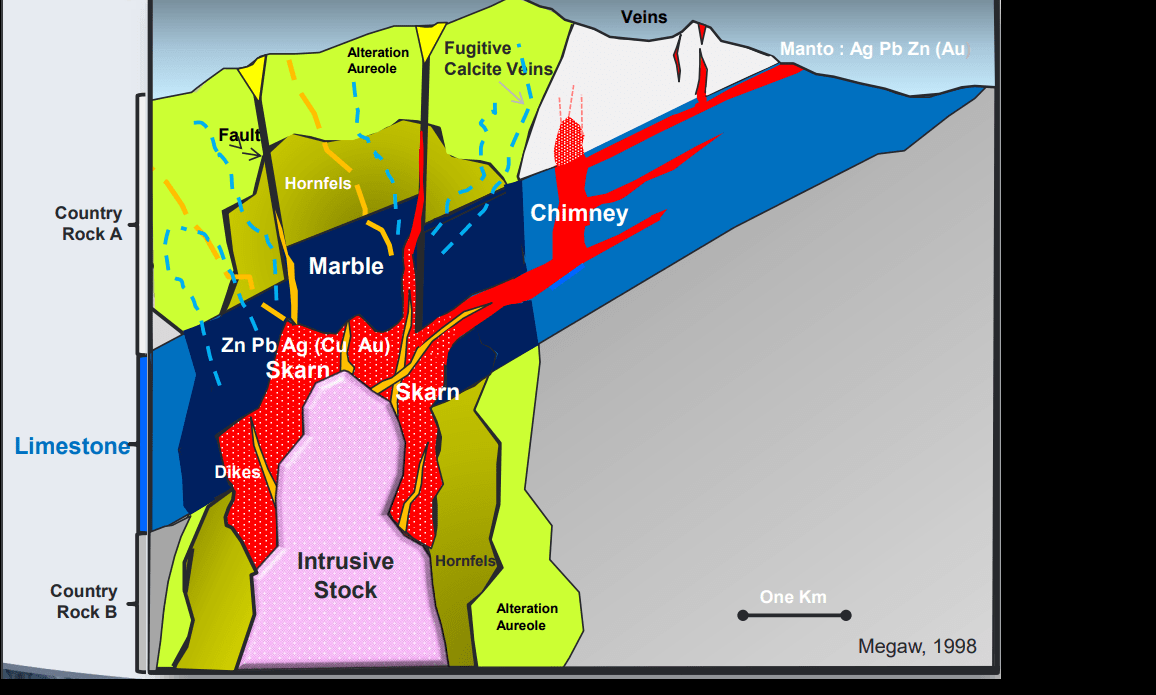

As shown in the images above, the Deer Trail Project is on the Bingham Trend, and MAG’s current focus is on delineating silver-rich carbonate replacement deposits in the Redwall Limestone, but the model for CRDs is that there is typically a major porphyry at depth feeding this rich mineralization (skarns, CRDs), which is similar to the Bingham Canyon model. In fact, while Bingham Canyon is known for its massive mineral endowment as a copper mine, the initial discovery was of oxidized lead and zinc and silver, lead, and placer and lode gold production continued into the late 19th century. Today, the mine is famous for being the world’s deepest open-pit mine today which can be seen from space.

Bingham Canyon Mine (Google Earth)

So, what’s the opportunity here?

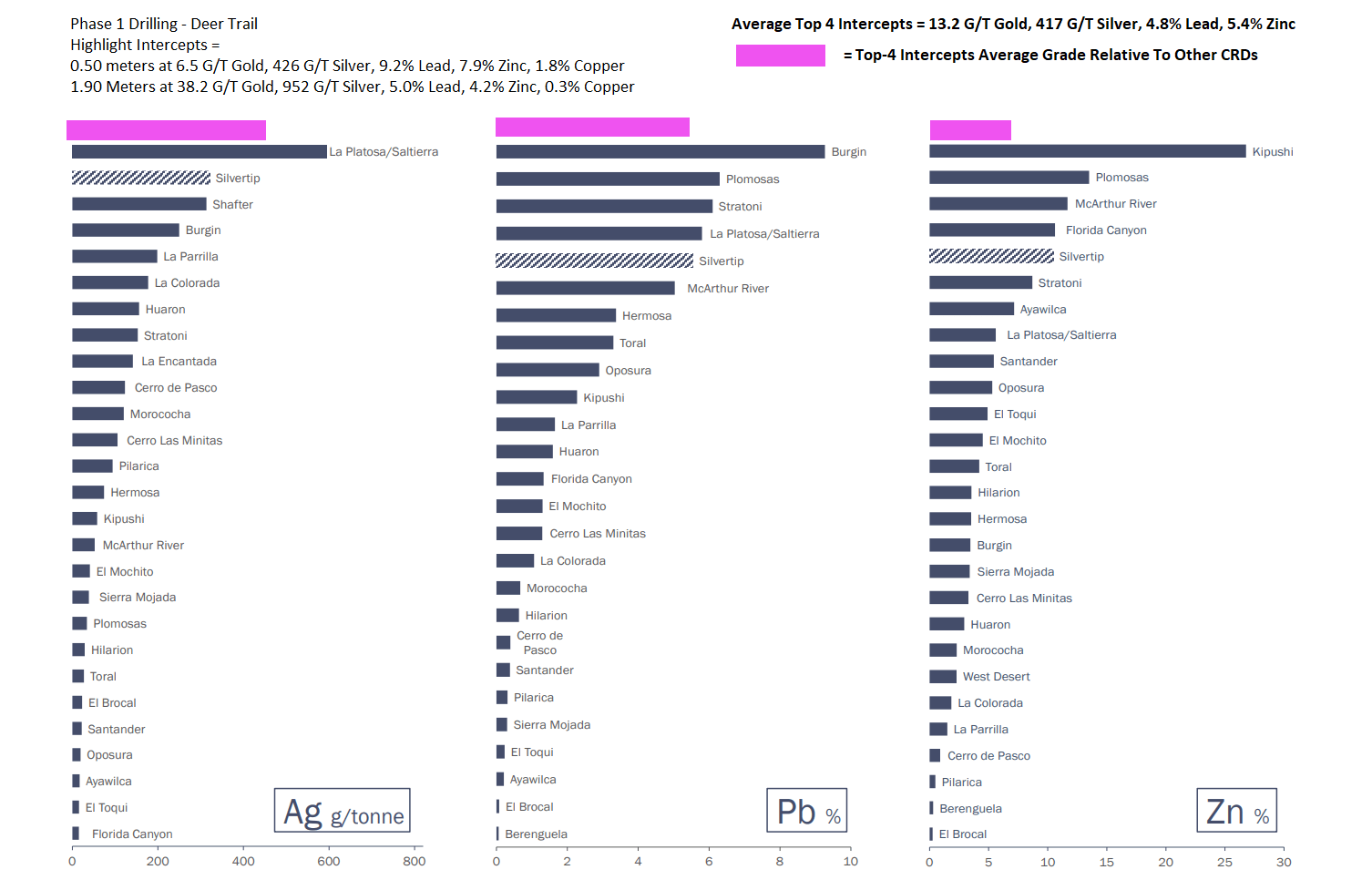

While MAG is focused on high grades (predominantly silver) and less so on a massive copper porphyry that could lie at depth, the company believes there could be a porphyry here that could significantly increase the value of the Deer Trail Project. Hence, to date, the focus has been on drilling beneath previously mined areas, and while a small program, its Phase 1 drill campaign certainly yielded some solid results and confirmed that Deer Trail has impressive grades, which included the following highlights:

- 0.50 meters at 6.5 grams per tonne of gold, 426 grams per tonne of silver, 17.1% lead/zinc, and 1.8% copper

- 1.90 meters at 38.2 grams per tonne of gold, 952 grams per tonne of silver, 4.2% zinc, and 0.30% copper

- 2.6 meters at 1.5 grams per tonne of gold, 147 grams per tonne of silver, and 0.2% lead/zinc

CRD/Skarn/Porphyry Continuum (Company Presentation, Megaw, 1998)

These hits were over relatively narrow widths but were very high grade, and follow-up drilling will be required to understand the potential better. That said, if we compare these results (top-4 intercepts) to existing carbonate replacement deposits globally, we can see that they stack up very nicely with an average grade of 400+ grams per tonne of silver, 13.2 grams per tonne of gold, 4.8%, 5.2% zinc, and additional copper credits. Notably, the substantial gold credits are unusual for CRDs but have been seen in some deposits in the United States, like the Eureka District in Nevada, where the area benefits from a Carlin overprint. To put these grades in perspective, the top-4 intercept’s average grade is above 20.0 grams per tonne gold equivalent, which is exceptional for a project benefiting from nearby infrastructure (roads, power).

Deer Trail Top-4 Intercepts by Grade vs. Other CRDs (Coeur Presentation, Author’s Notes/Drawing)

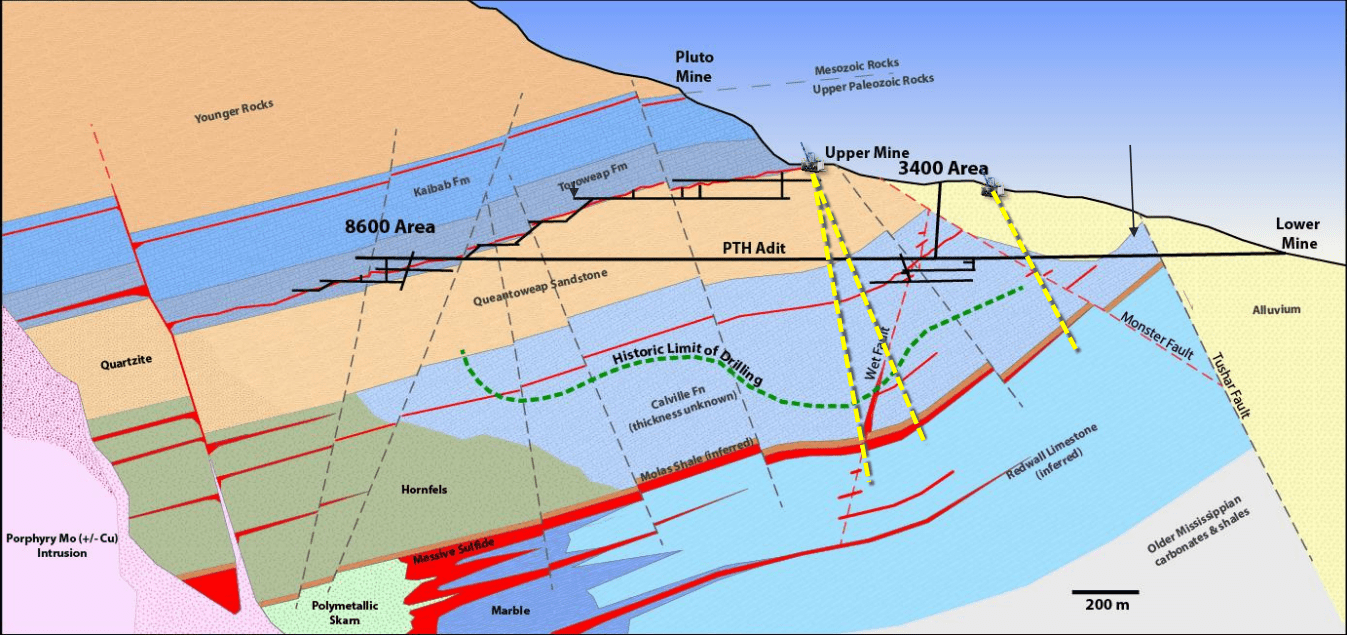

In more recent developments at Deer Trail, investors can look forward to releasing Phase 2 assay results this year, where six holes have been completed as part of a follow-up 5,000-meter drill program. The first hole was a 200-meter offset of drill hole DT21-02 to test the Red Fissure Structure within the Redwall Limestone. Meanwhile, the second and third holes were drilled to test an offset of DT21-05 to test the Wet/Monster fault intersection at depth and to cut the Wet fault deeper where it cuts through the Redwall Limestone. Assuming this drill program successfully delivers more high-grade intercepts (400+ grams per tonne silver with 5%+ plus lead/zinc), this would be a bonus to the MAG investment thesis and could result in the market placing some more value on this project.

Deer Trail – Target Area (Company Presentation)

Finally, in terms of the Larder Project (Gatling acquisition) near the Ontario/Quebec border, we should see new results from this property with the current Phase 1 drill program focused on mineralization below and lateral to previously identified mineralization at Larder. For those unfamiliar with the project, the previous operator’s focus was on delineating more near-surface mineralization, opening up the potential for MAG to take a closer look at the potential well below 500 meters depth, where some of the richest grades have been found in the Kirkland Lake Camp (35 kilometers west) and at Kerr-Addison (7 kilometers east).

As it stands, it’s difficult to assign more than $100 million combined to these two projects, even if they have the right address and interesting geological characteristics. That said, MAG Silver is in a unique position in that it should generate up to $100 million in free cash flow this year, allowing it to drill these two projects without any share dilution as well as hunt down new resources at Juanicipio with its partner. It also places it in a position where it could consider a regular or special dividend in 2024 as its cash position grows. Hence, investors should have lots to look forward to over the next twelve months, including the announcement of commercial production at its flagship asset (44% interest).

Valuation & Technical Picture

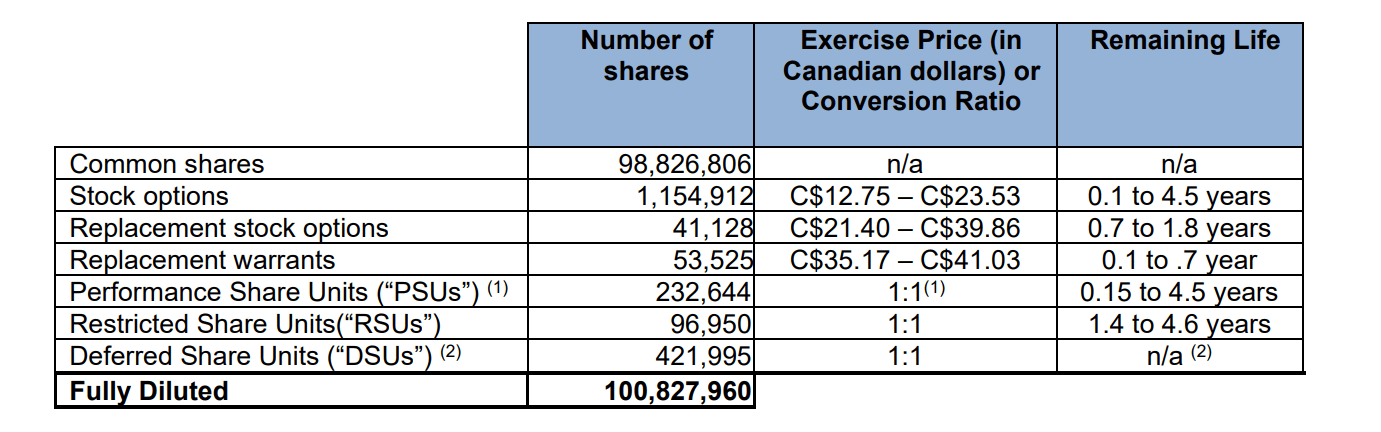

Based on ~101 million fully diluted shares and a share price of $16.70, MAG Silver trades at a market cap of ~$1.69 billion. If we compare this figure to an estimated net asset value of $1.19 billion, MAG Silver is trading at 1.42x P/NAV, a significant premium to NAV despite being a single-asset producer. However, the company is unique in the fact that it has a minority interest in one of the most impressive projects in North America with considerable exploration upside, and while it is in Mexico (a Tier-2 jurisdiction), Zacatecas is arguably one of the most mining-friendly states and one of the most well-endowed geologically within the country. Hence, I don’t think it should lose many points on jurisdiction despite its Mexico address.

MAG – Share Count (Company Filings)

Given that MAG Silver has an interest in a world-class project with minimal capital requirements and a strong team led by President & CEO George Paspalas (COO of Silver Standard, President & CEO of Placer Dome Africa) to allocate its growing cash position responsibly, I believe the stock can easily trade at a premium to its peer group. In fact, I would argue that a fair multiple for the stock is 1.50x P/NAV. However, even using this premium multiple, I see a fair value for the stock of $1,785 million or US$17.70 per share. While this does point to some upside, the stock is now approaching what I would consider a conservative price target.

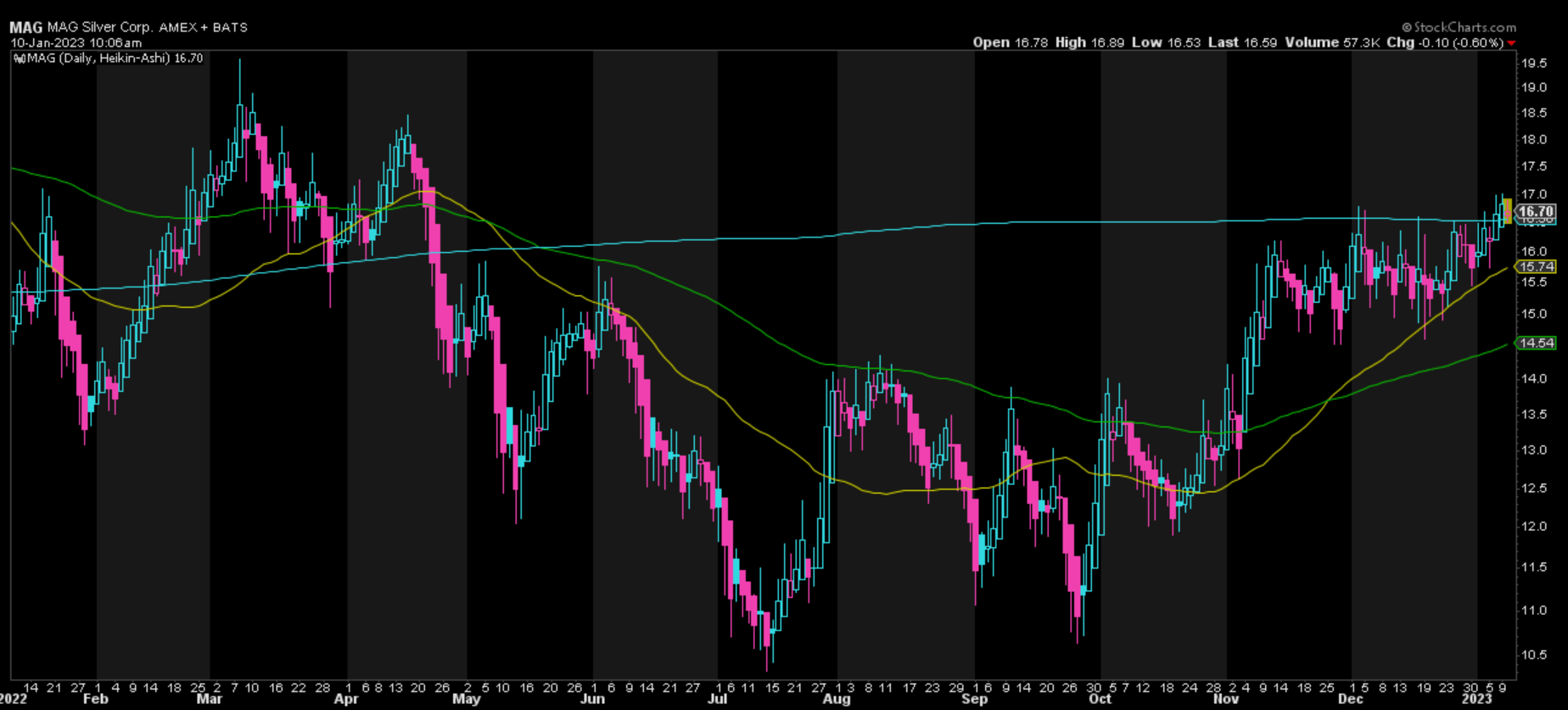

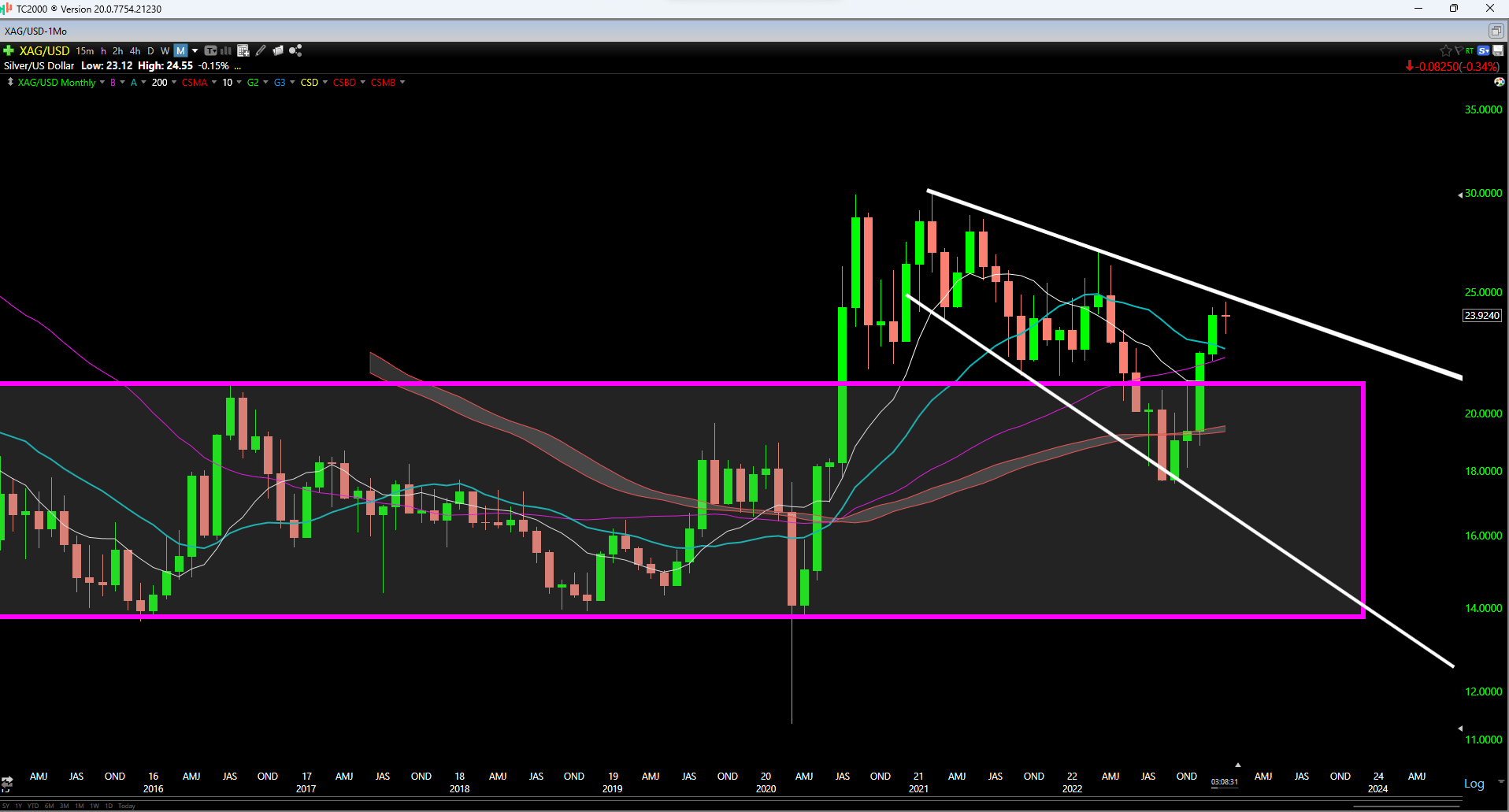

Meanwhile, from a technical standpoint, MAG Silver is now in the upper portion of its trading range, with strong support at US$10.75 and strong resistance at US$19.05. This translates to a reward/risk ratio of 0.34 to 1.0 when measuring its potential upside to resistance vs. potential downside to support, which is an unfavorable ratio. That doesn’t mean that the stock can’t head higher, but with the silver price also running into some resistance near $25.00/oz, it’s difficult to justify paying up for the stock here. Instead, I think the better course of action is waiting for sharp pullbacks to top up positions or initiate new positions.

MAG 1-Year Chart (StockCharts.com) Silver Monthly (TC2000.com)

Summary

MAG Silver has a very exciting year ahead as investors await drill results from multiple properties, the commencement of commercial production at Juanicipio, and a significant increase in production as the company benefits from much higher throughput rates at the Juanicipio plant. If we were to see blockbuster exploration results from one of these three properties, this could help justify a higher price target. That said, the stock is now sitting within 5% of what I consider fair value, within 10% of potential resistance, and silver is also banging its head into resistance. To summarize, while I love the story and think MAG Silver is a top-3 name in the silver space, I don’t see any way to justify paying up for the stock here above US$16.70.

Be the first to comment