hapabapa

Thesis

Lucid Group, Inc.’s (NASDAQ:LCID) Q2 earnings card demonstrated how tough it is for an electric vehicle (“EV”) upstart to scale high-volume manufacturing in a harsh macro environment. Despite garnering 37K reservations through Q2, the company only produced 1,405 vehicles in H1’22, underperforming its guidance and the Street’s consensus by a wide margin.

Notwithstanding, we explained in our previous article that LCID had formed its long-term bottom in May, which supported its recovery through its earnings release. Consequently, despite management slashing its FY22 production guidance by 50% to 6.5K (midpoint), LCID has held its August lows remarkably well. Therefore, we are increasingly confident that the market used the initial post-earnings sell-off as an “excuse” to shake out some weak hands, helping long-term dip buyers to accumulate further.

Investors need to remember that Lucid has a cornerstone back in Saudi Arabia’s Public Investment Fund (PIF) which has maintained its steadfast support despite its production challenges. It recognizes that these challenges are likely transitory and would not represent a structural threat to Lucid’s ability to ramp manufacturing. Furthermore, Lucid’s project launches remain on track, corroborating management’s confidence in meeting its ramp targets moving forward. Therefore, we are confident that LCID’s recent price action suggests that the market sees such hurdles as transitory, which should improve subsequently.

Accordingly, we reiterate our Buy rating on LCID and urge Lucid investors to accumulate with the market.

Saudi’s PIF Maintains Support Despite Near-Term Production Challenges

Lucid updated recently that its cornerstone investor, Saudi Arabia’s PIF, has maintained its confidence despite Lucid’s cutting its production targets for the second time in FY22. The company highlighted:

[The PIF] understands the challenges around supply chain issues and costs. The company is not seeing pressure from investors. The PIF have been very supportive. When the world re-emerges from the pandemic and the supply chain catches up, we will be ready. The company is on target to deliver cars to customers in Riyadh in the second quarter of next year. – Bloomberg

Therefore, we believe the PIF’s confidence and support suggest that Lucid investors need to consider its long-term thesis to reap the benefits from their investments. As a result, near-term downside volatility could represent tremendous opportunities for investors who share the PIF’s long-term vision to add exposure. Lucid’s medium-term market opportunity to leverage the Saudi Arabian and Middle East markets should also not be understated.

Lucid Has Not Shifted Its Medium-Term Goalposts

It’s easy to focus on near-term production misses, especially for an upstart like Lucid. We are not trying to suggest that production issues are not critical. But, we must highlight that Lucid’s mid-decade’s (FY25) project milestones have not shifted, which was seldom touched upon by the bears.

Furthermore, management assured investors that it had taken the necessary steps to remediate its recent production challenges by bringing its logistics operations in-house, seeking to eliminate the logistical bottlenecks which hobbled its production.

Management also reminded investors of the company’s medium-term potential, as it articulated:

The reservation number of over 37,000, represents potential future revenue of approximately $3.5B, and that’s before including the up to 100K vehicle deal with Saudi Arabia and the future reservations for the Gravity since we’ve not yet opened the order book for our upcoming SUV. Our Phase 2 expansion at our Casa Grande, Arizona factory is progressing. When complete, we expect our installed capacity to increase to 90K units per year by early 2023. As we exit mid-decade, we expect to reach an annual installed capacity of 350K units in Arizona and 150K annual units of installed capacity in Saudi Arabia and that gets you to an annual installed capacity of 500K shortly after mid-decade. (Lucid FQ2’22 earnings call)

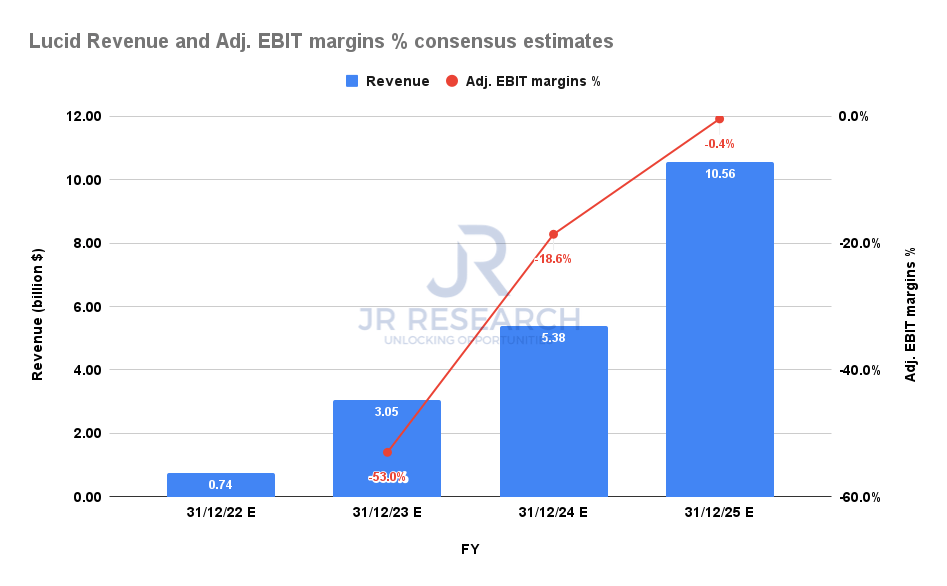

Lucid revenue and adjusted EBIT margins % consensus estimates (S&P Cap IQ)

The consensus estimates (bullish) also suggest that Lucid should be able to continue ramping significantly through FY25, with revenue reaching $10.56B and close to adjusted EBIT breakeven. However, the estimates for FY22 have been cut by almost 50% to reflect its near-term challenges. Still, the impact is expected to be transitory.

Is LCID Stock A Buy, Sell, Or Hold?

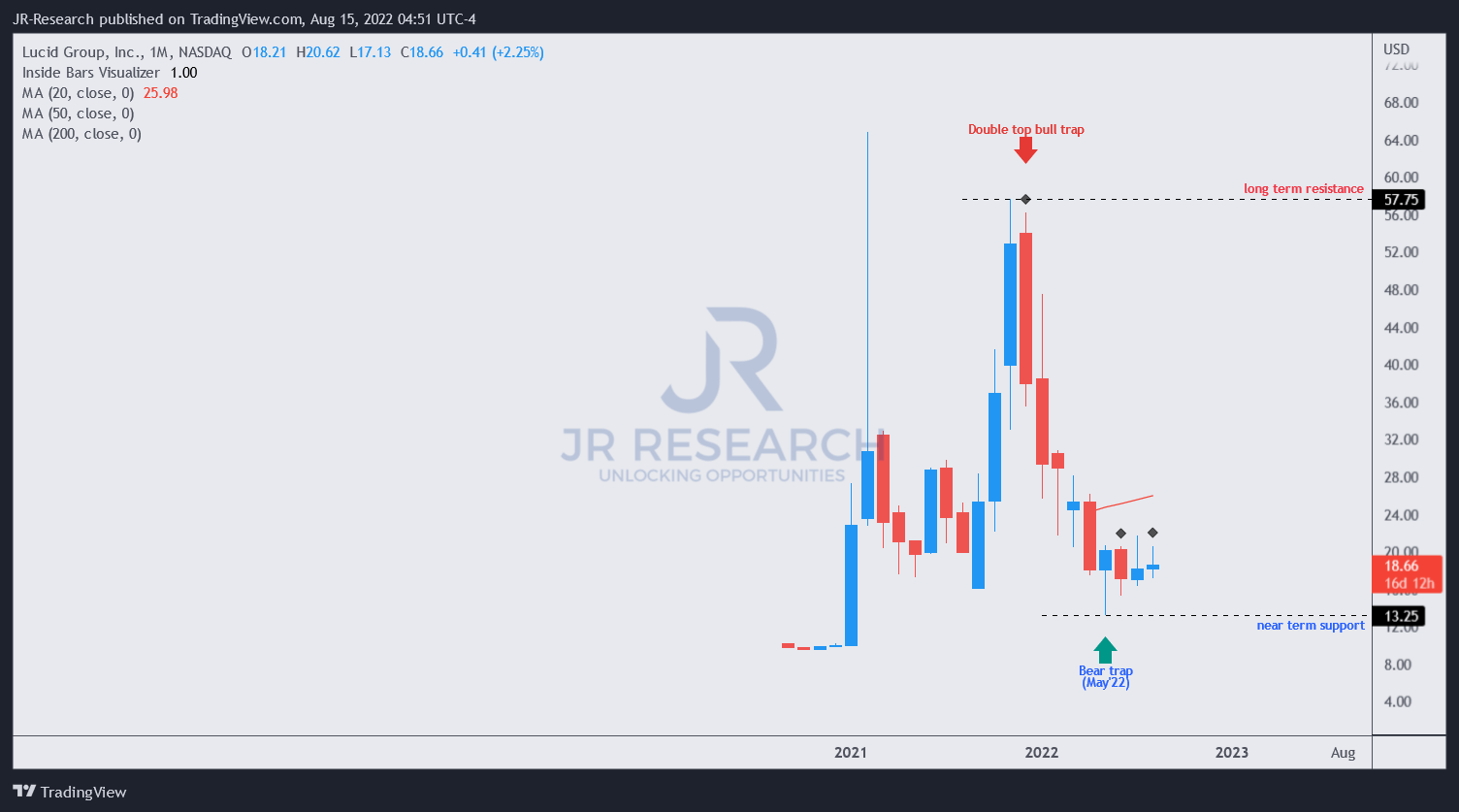

LCID price chart (monthly) (TradingView)

We observed that the market supported the post-earnings sell-off resiliently above its May bear trap (indicating that the market rejected further selling downside decisively). In addition, the selling momentum also did not break below July lows, suggesting robust near-term support.

We view the near-term downside volatility as a solid opportunity for long-term dip buyers to add exposure.

Therefore, we reiterate our Buy rating on LCID, with a medium-term price target of $25.

Be the first to comment