{kind=link}

(Source)

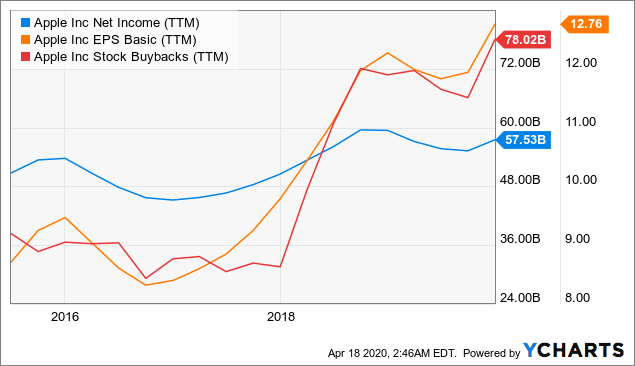

Apple Inc. (AAPL) is known for creating shareholder wealth year after year. But in the recent past, the company has found it difficult to grow meaningfully. Before you say earnings per share has grown at a stellar rate in the last few years, let me remind you that this was not driven by higher earnings, but share buybacks.

Data by YCharts

Data by YCharts

From 2015 to 2019, the net income of the company has increased at a CAGR of 0.86%, in comparison to a compound growth rate of over 6.5% for EPS. This is evidence of how buybacks have boosted the per share figures of Apple in the last few years. The company’s disappointing performance in high-growth countries such as India was behind the lackluster earnings growth. The launch of the new iPhone SE is a reflection of Apple’s mission to turn things around and capture meaningful market share in emerging markets. But now is not the time to be excited about the prospects of this new strategy, for reasons I will discuss in this analysis. I remain on the sidelines until I see an acceptable margin of safety to invest in Apple shares.

India is an important market, and the new iPhone SE is tailormade to capture growth

Apple is not doing well in India, a market that is at the center of any smartphone company’s success. India, in the fourth quarter of 2019, surpassed the United States to become the second-largest smartphone market in the world behind China. What makes India a very important market for the industry is the saturation of smartphone shipments on a global scale, which is depicted below.

(Source: Statista)

Companies have already run out of growth opportunities elsewhere, but India remains a hot spot for growth. Stellar economic growth in the last decade has led to the rise of a middle-class society in the country, and the internet penetration rate is improving as a result of billion-dollar infrastructure development projects carried out by the government. In March 2019, McKinsey wrote in a report:

Our analysis of 17 mature and emerging economies finds India is digitizing faster than any other country in the study, save Indonesia – and there is plenty of room to grow: just over 40 percent of the populace has an internet subscription. India will increase the number of internet users by about 40 percent to between 750 million and 800 million and double the number of smartphones to between 650 million and 700 million by 2023.

Even in the last 5 years, the smartphone market in India has grown in leaps and bounces. But Apple’s performance was disappointing, to the surprise of many investors. As someone who comes from an emerging country, this miserable performance was not a surprise to me, as Apple’s strategy so far has been to sell premium products at premium prices. This was never going to work in the developing regions of the world.

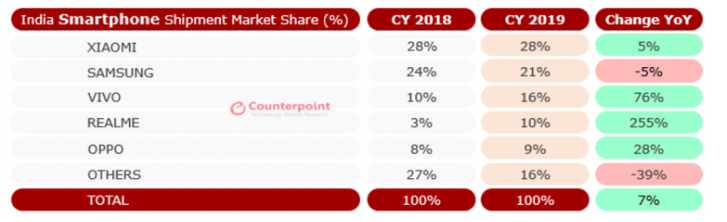

At the end of 2019, Xiaomi (XI) was at the helm of the Indian smartphone market, closely followed by Samsung (SSNLF).

(Source: Counterpoint Research)

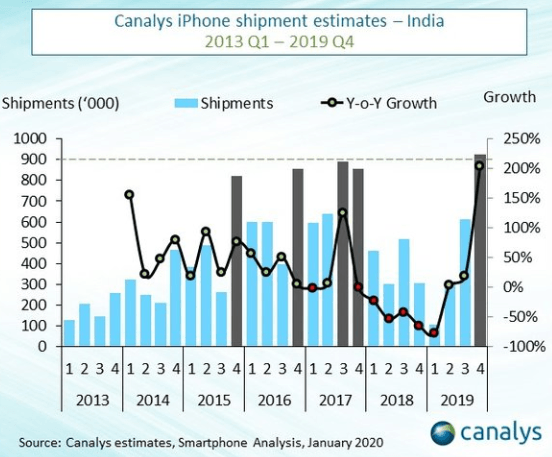

Apple, as you can see, was not even in the top 5 list. However, in every sense, 2019 was a banner year for Apple in India. It shipped 925,000 iPhones in the fourth quarter of 2019, marking the best quarter for the company in India.

(Source: Canalys)

Sales were literally going nowhere, but then came the iPhone 11 to the rescue. Since the launch of the iPhone 7, Apple’s strategy has been to bring expensive, premium devices to the market in a bid to offset the negative impact of declining unit sales. In an article published in December 2018, I discussed this strategy extensively. The pricing of the iPhone 11 in 2019, however, reflected a sudden change in this strategy, as the new device was introduced at a starting price of $699 – significantly lower than the $1,000 iPhones the company was marketing in the previous years.

The iPhone 11 did wonders in the Indian market, as the device was a perfect alternative to some of the pricey Samsung and Xiaomi devices that did not come with the brand value of Apple. From my first-hand experience in India and Sri Lanka, I can assure our readers that Apple devices are considered as premium in the South Asian region. Therefore, consumers would naturally pounce on any opportunity to buy the latest Apple devices at a reasonable price, even if they could purchase a better-functioning device from another brand name for the same price. The problem in the recent past has been the inability to buy the latest Apple devices without shelling upward of $800.

Canalys analyst Madhumita Chaudhary wrote:

Apple hit a home-run with its pricing strategy on the iPhone 11. The partnership with local bank HDFC made iPhones more affordable, with the entry-level iPhone 11 one of the cheapest ‘new’ iPhones in a while. The new iPhones have appealed not just to current iPhone users looking to upgrade, but also to value-conscious premium phone purchasers that are now presented with a formidable price alternative to the Samsung or OnePlus flagships.

The launch of the iPhone SE is another step forward in capturing growth outside the United States, especially in developing regions of the world. Many investors are excited about Apple’s growing services revenue, which, indeed, is a good thing for the company in its mission to transform into a services giant from a consumer technology company. But the success of Apple’s services segment will depend on the global installed base of its devices. Therefore, capturing the smartphone market share in high-growth regions will go a long way to ensure the sustainability of company earnings in the future. For instance, India will eventually determine who dominates the over-the-top content streaming industry, and a higher installed base of iPhone devices will help Apple TV+ gain traction faster in this region.

With the sudden change in Apple’s pricing strategy, the company is now in a better position to grow outside developed regions such as North America and Europe. However, there’s more to the story.

Why am I not excited still?

By December 2018, I had built a nice position on Apple with an average price of around $165. I’m a growth investor. I identified that the company was relying on buybacks to improve its EPS, which is something I did not, and do not, enjoy as a growth investor. Therefore, in December 2019, I decided to book my profits and sell the entire holding of Apple shares.

A few months later, now I’m starting to see a shift in the company’s strategy, which is a welcome sign. But would this pay the expected dividends? I do not doubt that Apple will gain traction in India and other important target markets steadily. However, 2020 might not be the year the company reaps the rewards of its change in business tactics.

The spread of COVID-19 is hurting almost every country in the world, and India is no exception. The country went into lockdown over 3 weeks ago, and the Indian Prime Minister decided to extend the shutdown of the country till May 3. Consumer spending in the country will take a massive hit as a result of the pandemic. Even though mobility restrictions might be lifted in a few weeks, the economic impact of the virus will most likely be felt for many months to come.

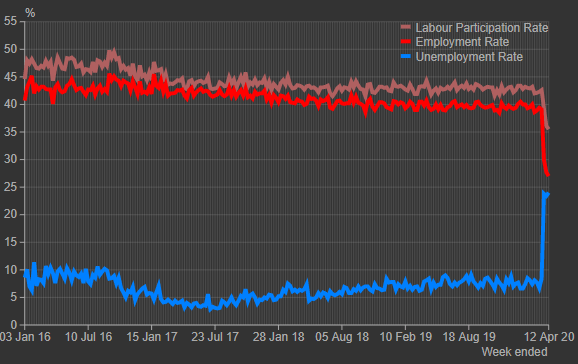

Axis Capital, on March 25, claimed that a month in lockdown could wipe $45 billion of discretionary spending in India, which is equivalent to 1.5% of the GDP. Now that the lockdown has been extended to well over a month, the result would be an even larger dent on spending. The unemployment level in the country has spiked to historic levels as well, and the path to recovery won’t be as swift as some investors believe.

(Source: Center for Monitoring Indian Economy)

Counterpoint Research, which is following the Indian smartphone market closely to gauge a measure of developing industry trends, has recently conducted a study to figure out how the Indian smartphone market would behave during a virus-induced economic recession. Counterpoint director of research Peter Richardson wrote:

Our conclusion is that we expect to see a sharp contraction as consumers withhold making discretionary purchases during periods of maximum uncertainty. The result is an extension in the replacement cycle.

There is a high level of uncertainty regarding when and how the spread of coronavirus will be contained. This makes me absorb Apple’s progress in India with caution.

The unfavorable macroeconomic environment is not the only thing that is keeping me from investing in Apple. The iPhone SE is not as pricey as some of the other flagship Apple devices, but its features do not give reason to boast as well. The iPhone 11 did well in India because the product was as premium as one could have imagined for that price. The world is excited about the upcoming 5G-enabled devices from Apple, but the iPhone SE lacks this feature. More than in India, selling this new handset in China will prove to be difficult as consumers are inclined toward purchasing 5G-enabled devices. Not to forget, China is one of the biggest markets for Apple. The lack of some important features such as 5G will prove to be a lag on SE sales, in my opinion. On the other hand, many investors are awaiting the launch of what would be called the iPhone 12 in September this year. The iPhone SE is not in the mainstream of devices the company will be launching in 2020, which is another reason for consumers to be less enthusiastic about the attractive price tag.

The expected decline in gross profit margins is another reason for me to stay on the sidelines. Low-cost devices will always be a drag on margins, but if Apple was able to reach its sales targets, the company would eventually benefit in the long run as the installed base would expand. However, there’s a very real possibility of Apple failing to achieve whatever the targets it has set for iPhone SE, as the outlook for the industry has changed in a matter of just a few weeks.

Finally, the closure of Apple Stores on a global basis will result in a decline in the expected revenue. Apart from a few stores in China and South Korea, many Apple Stores remain closed around the world, which is not good news for investors, especially at a time a new device has been launched.

Takeaway: The change in strategy is good, but now is not the time to be excited about the prospects

Apple is making important changes to its business strategy to capture growth in its target markets. In the long term, this change will reward investors. However, this is not the time, in my opinion, to be overly optimistic about the prospects of iPhone SE or any other inexpensive devices the company would launch this year. There are multiple headwinds for the company, leading to uncertainty about the success of these new products in 2020. Apple shares are trading at a price-to-earnings multiple of around 22, which is close to the 5-year highs of 25. Even when the revolutionary iPhone 6 was launched in 2014, shares did not trade at multiples this high. There seems to be an anomaly between the economic reality of the company and its market value. On the other hand, the way forward for Apple is not as smooth as it was in the last 5 years. The company would be implementing many strategies, and novel concepts would be tested to see how it can grow its earnings. It might take a while for Apple to find what works best. The share price, on the other hand, is still trading at a premium, and I do not see a margin of safety at the current market price of around $280.

If you enjoyed this article and wish to receive updates on my latest research, click “Follow” next to my name at the top of this article.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment