Lari Bat/iStock via Getty Images

(This article was co-produced with Hoya Capital Real Estate)

Introduction

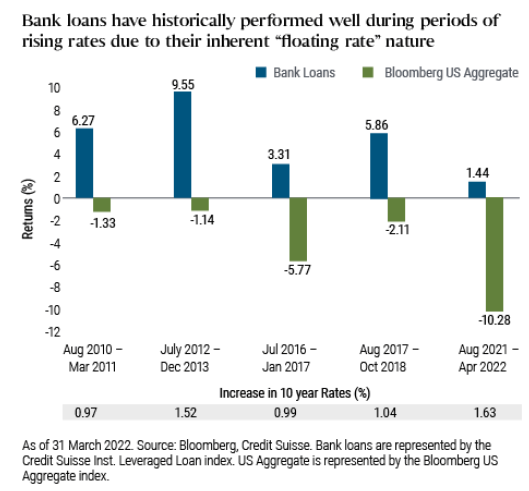

The Senior Loan Active Exchange-Traded Fund (LONZ) is less than a month old. While PIMCO has a low durations ETF, the Enhanced Low Duration Active Exchange-Traded Fund (LDUR), the new ETF has a duration 60% shorter and focused on senior loans. LDUR uses only US Government and Investment-Grade debt; LONZ adds MBS assets to the mix. The next chart shows the reasoning PIMCO probably used to justify launching a new ETF.

PIMCO.com

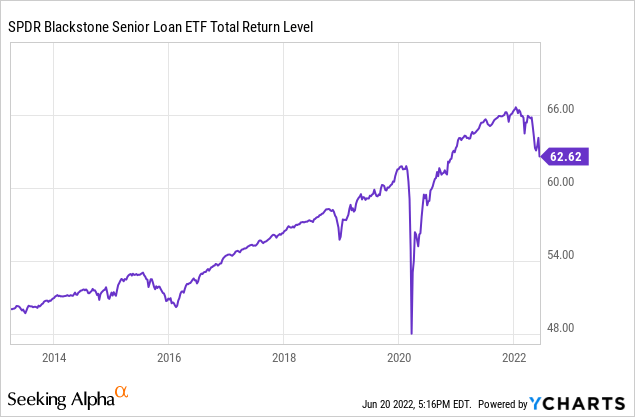

I did find another ETF, the SPDR Blackstone / GSO Senior Loan ETF (SRLN) that uses the same Index.

You can see that SRLN has suffered, maybe not as much, also since the start of the year. Since it started in 2013, SRLN has provided investors with a meager 2.45% CAGR. That should help set expectations for the LONZ ETF.

Exploring The PIMCO Senior Loan Active Exchange Traded Fund

PIMCO describes their new ETF as:

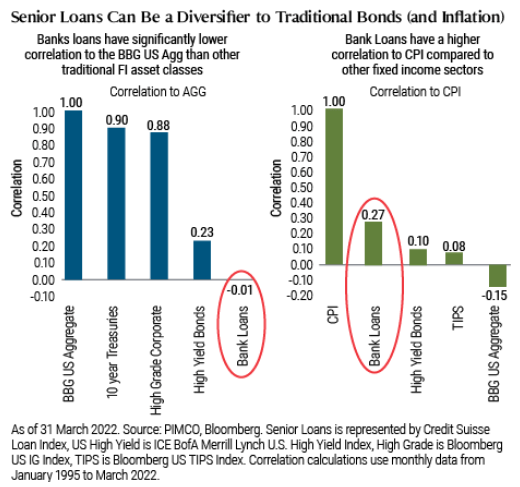

The Fund seeks current income, consistent with prudent investment management. Bank loans are a hedge against rate increases as the offer low durations. Bank loans also have a low correlation to other core fixed income sector but a higher correlation to inflation. Bank loans occupy a higher place in the corporate structure, offering more default protection than other fixed income assets.

Source: pimco.com LONZ

PIMCO provided these two charts to illustrate the correlationships mentioned.

PIMCO.com LONZ

The Prospectus provided the principal investment strategies for LONZ:

The Fund seeks to achieve its investment objective by investing, under normal circumstances, at least 80% of its assets in a diversified portfolio of Senior Loans, which may be represented by forwards or derivatives such as options, futures contracts or swap agreements. “Senior Loans” include senior secured floating rate bank loans, also referred to as leveraged loans, bank loans and floating rate loans, that are first or second lien loans. The Fund may also invest in collateralized loan obligations and high-yield corporate debt securities, which may also be represented by forwards or derivatives such as options, futures contracts or swap agreements.

The Prospectus provides the guideline used with respect to the ETF’s duration compared to the Index, which also lets investors know, while using the Index for various purposes, LONZ’s portfolio does not need to mimic its holdings.

The average portfolio duration of the Fund will normally vary within one year (plus or minus) of the portfolio duration of the securities comprising the Markit iBoxx USD Liquid Leveraged Loan Index, as calculated by PIMCO, which as of March 31, 2022 was 0.18 years.

The fund is allowed to allocate 20% of its assets into preferred stocks and 20% in non-USD securities; neither of which has happened yet.

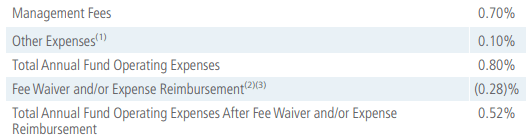

The current fees are capped until November 2023 and comprise the following:

pimco.com/documents

As reference, SRLN charges 70bps in fees.

Understanding The Index

LONZ invests based on the iBoxx USD Liquid Leveraged Loans Index, which has the following description:

The iBoxx USD Leveraged Loan index family represents the main sections of the USD leveraged loan market. Index constituents are derived using selection criteria such as loan type, minimum size, liquidity, credit ratings, initial spreads and minimum time to maturity.

Index calculations incorporate our independent loan pricing data as well as our up-to-date loan reference and transaction information.

The iBoxx USD Liquid Leveraged Loan index comprises approximately 100 of the most liquid, tradable leveraged loans. In addition, we offer three sub-indexes based on realized gains, unrealized gains and interest and fees. Indices are rebalanced monthly, using a transparent roll mechanism.

Source: ihsmarkit.com

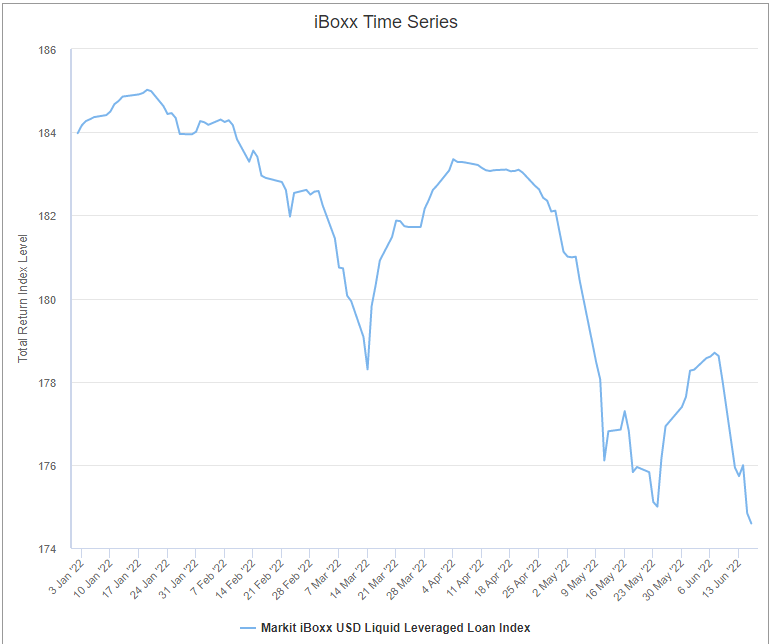

I found a chart showing 2022 Index performance and some Index data points.

markit.com markit.com Index Summary Statistics

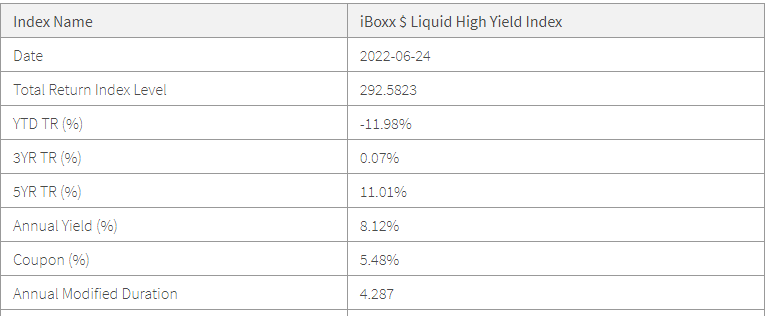

Assuming LONZ performs like the Index, the above table provides historical returns out to five years.

Holdings Review

Limited data is available from PIMCO on their new ETF. This is what I found and could compile.

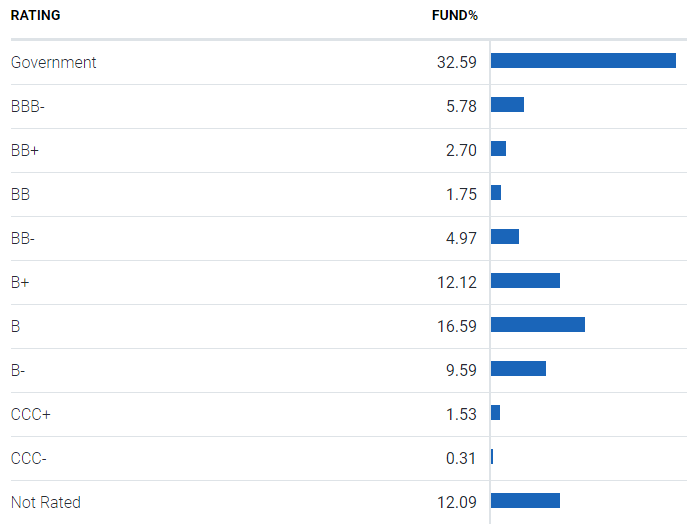

PIMCO.com LONZ ratings

All the government debt is Investment-Grade, thus just over 38% is so rated. Very little is CCC-rate, where default rates are much higher than even B-rated debt; but having 38% rated between B+/B- would become a concern if the US economy slips into a recession. All assets are priced in USD. The Portfolio currently has an effective duration of .56 years and effective maturity of 4.32 years. Since the Index duration is close to .18 years, I would expect LONZ’s to drop as it becomes fully invested, unless they choose otherwise.

PIMCO.com; compiled by Author

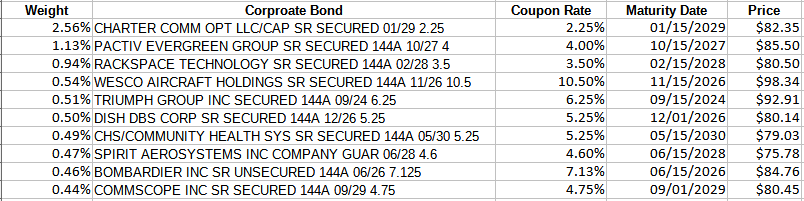

This is a complete list of the corporate bonds held.

PIMCO.com; compiled by Author

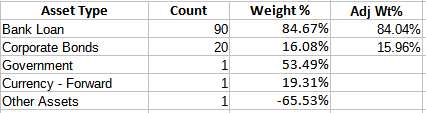

The WAC is 4.37%, WAM is 5.6 years, with an average bond price of $83.63. Every bank loan coupon was listed at 1%. They have a WAM close to 4.4 years and the average price is $94.30. About 20% of the portfolio matures in the next three years, providing an opportunity to buy higher coupon debt. Holdings that mature within that window also provides price appreciation (assuming no negative issues occur) of 5-6% based on current prices.

I did not find any sector allocations or YTM data.

Distribution Review

LONZ has yet to declare a payout, but the Prospectus does describe the policy that will be used:

The Fund distributes substantially all of its net investment income to shareholders in the form of dividends. The Fund intends to declare and distribute income dividends monthly to shareholders of record. The Fund’s first distribution to shareholders is expected to occur after its first full calendar month of operations. In addition, the Fund distributes any net capital gains earned from the sale of portfolio securities to shareholders no less frequently than annually. No dividend reinvestment service is provided by the Trust.

Source: pimco.com Prospectus

Once declared, I will update the article to list what the first payout was.

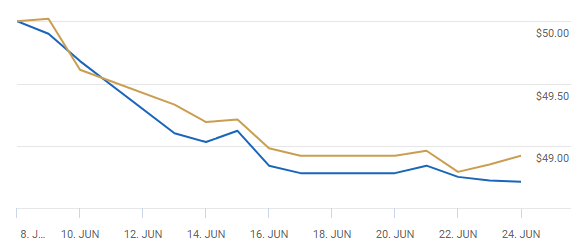

Short Trading History Review

PIMCO.com LONZ

Since shortly after its 6/8/22 start, LONZ has traded at pennies below its NAV. Being an ETF, a large spread rarely happens, as large investors can buy/sell full units and capture the difference.

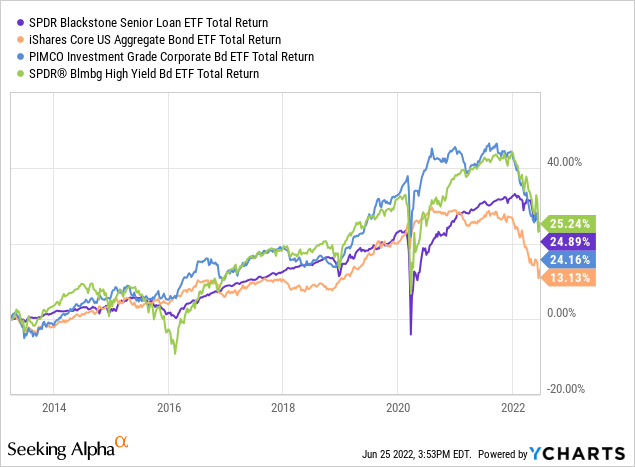

Portfolio Strategy

The point here is, using short-duration funds should do better when rates are climbing. Using SRLN in place of LONZ, I compared its Total Return against ETFs with longer durations. As the asset mixes differ, the comparison comes with that caveat. ETFs used include (with duration listed):

- iShares Core U.S. Aggregate Bond ETF (AGG): 6.78 years

- PIMCO Investment Grade Corporate Bond Index ETF (CORP): 7.38 years

- SPDR Bloomberg Barclays High Yield Bond ETF (JNK): 4.15 years

SRLN shows a .18 year duration, matching the Index used by LONZ.

SRLN has performed best in 2022. What is surprising is its second place finish since 2013, a period until 2022 that saw level to declining rates. Using PortfolioVisualizer.com data, SRLN’s shorter duration did not provide investors with a smoother ride except compared to JNK; while the best performer, it had the highest StdDev.

Final Thought

Since SRLN uses the same Index, SRLN might be the better play for now. That said, SRLN has over 300 assets and uses an additional Index for benchmarking that might explain the large asset count.

Be the first to comment