guvendemir

Value investors have a lot options at present, with most asset classes being down in recent months. While it can be tempting to buy into beaten down technology growth names, ambiguity over the direction of inflation and interest rates may further put pressure on the discount rate with which growth stocks are measured, and can result in further share price declines.

That’s why it may pay to stick with tried and true blue-chips like Lockheed Martin (NYSE:LMT), which have demonstrated their wealth compounding effects over the long-term.

The stock has performed well since I last covered it in October last year, returning 26% (28% including dividends) since then, far surpassing the 15% decline of the S&P 500 (SPY) over the same timeframe. LMT is now trading off its recent highs, and in this article, I highlight what makes LMT an attractive long-term pick at present, so let’s get started.

Why LMT?

Lockheed Martin is a global defense company that’s strategically headquartered in Bethesda, Maryland, just north of America’s capital. It has a leadership position in high-end military aircraft, including the signature F-35 fighter jet program. Beyond fighter aircraft, LMT’s other businesses include mission systems, including Sikorsky helicopters, missile defense, and space systems.

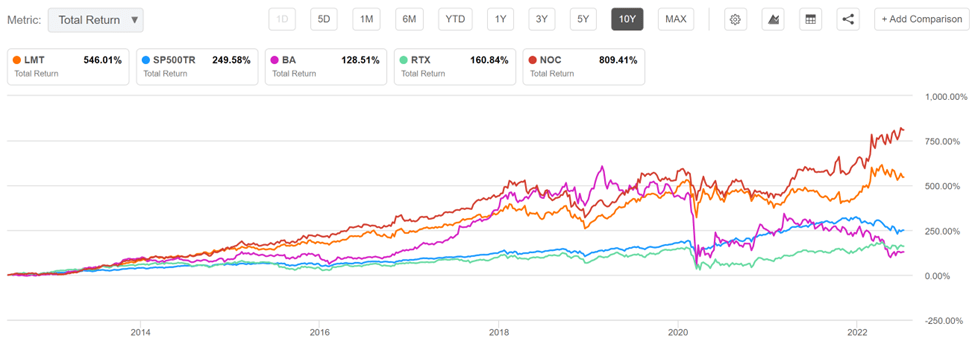

LMT has produced solid shareholder returns over the long-term, with fundamental growth and capital returns in the form of share buybacks and dividends in its arsenal. As shown below, LMT’s 546% total return beats that of the S&P 500 (SPY) and competitors Boeing (BA) and Raytheon Technologies (RTX), bested just by Northrop Grumman (NOC).

LMT Total Return (Seeking Alpha)

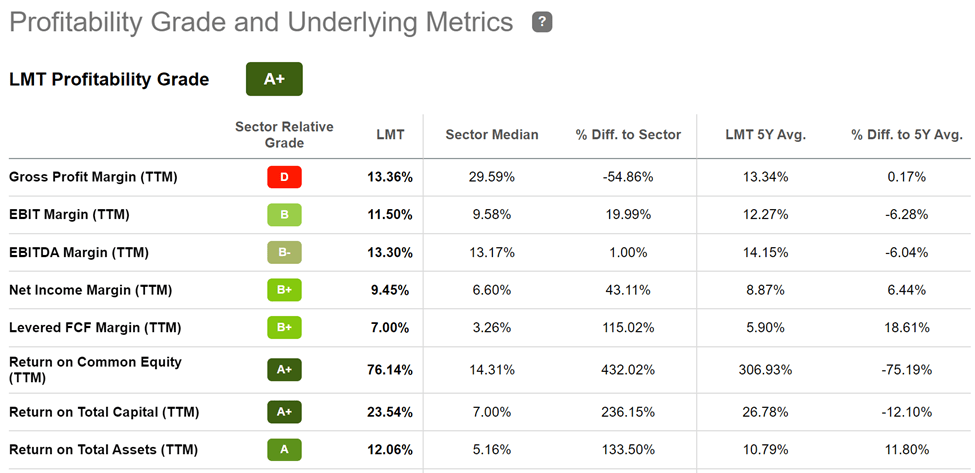

It also generates strong profitability, earning it an A+ grade, with a sector leading net income margin of 9.5%, far surpassing the 6.6% sector median. As shown below, LMT also generates an impressive 76% return on equity, which is a result of aggressive share repurchases over its history.

LMT Profitability (Seeking Alpha)

LMT expanded its strong margins during the first quarter, with total operating margin rising by 30 basis points YoY, to 11.1%. This helped to buffer against the 8% YoY revenue decline, with earnings per share declining by just $0.02 to $6.44. Nonetheless, management has maintained its full year 2022 outlook despite a slower than expect start.

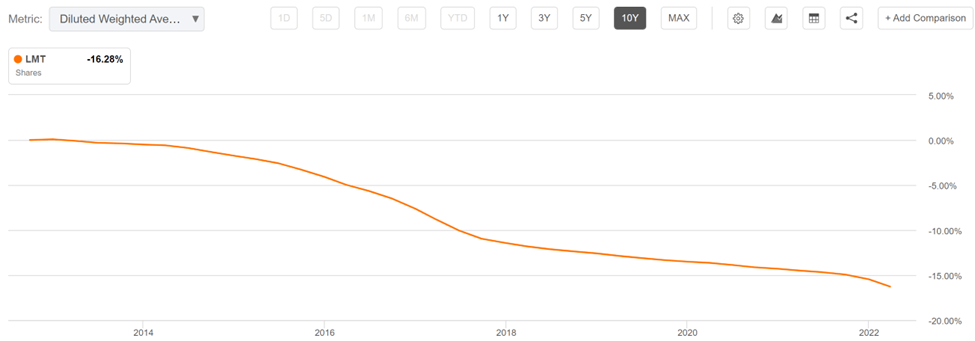

Meanwhile, LMT remains solidly profitable, generating $1.1 billion in free cash flow and executed on a $2 billion accelerated share repurchase during the first quarter. Moreover, management remains shareholder friendly, and aims to deliver 100% of its free cash flow to stockholders over the course of the year including dividends. This includes a total $4 billion in share repurchases over the full year. As shown below, LMT has reduced its share count by a respectable 16% over the past decade.

LMT Shares Outstanding (Seeking Alpha)

Risks to the investment thesis include LMT’s obvious dependence on U.S. defense spending, and budget sequestration can result in across-the-board spending cuts if Congress and the White House agree on targeted cuts.

However, LMT has a number of tailwinds behind it, especially considering the global unrest brought upon by the war in Ukraine. This includes the popular F-35 fighter aircraft, which now has the F-35C version that’s operational on aircraft carriers. Moreover, LMT is boosted by international shipments to foreign allies, as noted by management during the recent conference call:

Turning to the F-35 program. Germany recently announced their intent to procure 35 aircraft. Lockheed Martin will support our U.S. government Joint Program Office in this process, as we look to partner with Germany to provide this unique capacity and capability for its national defense.

The government of Canada has also announced it will enter into the finalization phase of their procurement process with the United States government and Lockheed Martin to purchase 88 F-35 fighter jets for the Royal Canadian Air Force. Canada is one of the original eight partner countries on the F-35 program, and we’re very pleased to have the opportunity to provide this unrivaled plane to strengthen Canada’s national defense.

The German and Canadian announcements followed similar award decisions last year from Switzerland and Finland. And these four competitive wins have the potential to add 223 F-35s to our backlog when all are finalized. All four of these recent announcements underscore that the F-35 fighter jet remains the most capable, survivable and highly connected platform in production as well as the best value available today for our war fighters.

I’m also encouraged to see that LMT is de-risking itself of pension obligations by transferring $4.3 billion worth of pension obligations to Athene (ATH), and it maintains a strong A- rated balance sheet. This lends support to its 2.7% dividend yield, which comes with a low 39.8% payout ratio, a 9% 5-year CAGR, and 20 years of consecutive growth.

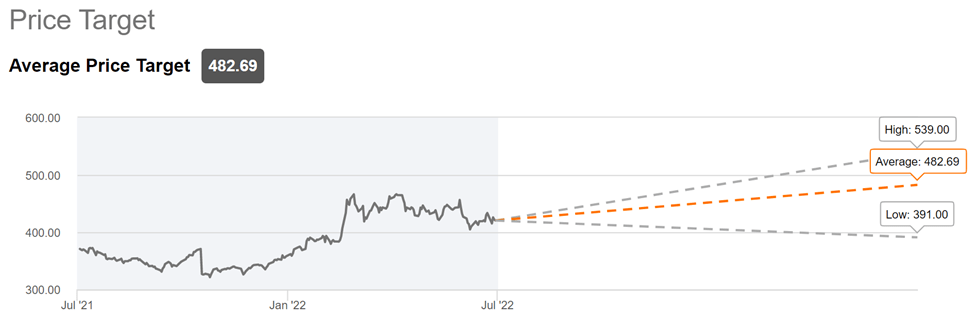

LMT isn’t particularly cheap at the current price of $420, with a forward PE of 15.8, but it still sits below its normal PE of 16.8 over the past decade. I see this valuation as being deserved, considering the moat-worthy nature of the enterprise and forward growth prospects. Sell side analysts have a consensus Buy rating, with an average price target of $483, implying a potential one-year 18% total return including dividends.

LMT Price Target (Seeking Alpha)

Investor Takeaway

Lockheed Martin is a high quality aerospace & defense giant that should benefit from global tensions, as well as the F-35 fighter aircraft. It’s delivered very strong shareholder returns over the long-term, and management is set to return large amounts of capital to shareholders this year in the form of buybacks and dividends. While LMT doesn’t scream cheap, I view it as being a wonderful company that can be bought at a fair price.

Be the first to comment