John Moore/Getty Images News

In not such a surprise move, Albemarle (ALB) came public with a rejected deal on a new takeover offer to acquire to Liontown Resources (OTCPK:LINRF). The Australian lithium miner definitely has no reason to cash out of the lithium trade in the middle of constructing a new mine. My investment thesis is Bullish on the lithium sector due to surging electric vehicle and renewable energy demand requiring a huge increase in the supply of lithium.

Proposed Deal

On March 27, Albemarle announced a proposed deal to acquire Liontown Resources in an all-cash offer at A$2.50 or $1.66 per share. The deal values Liontown at A$5.2 or $3.4 billion on an enterprise basis.

Liontown Resources management quickly rejected the deal. Though, Albemarle points out the significant premiums to the previous prices, investors in Liontown aren’t necessarily interested in cashing out from a speculative lithium play. Not to mention, the stock has a recent high of $1.80, slightly above the latest offer price.

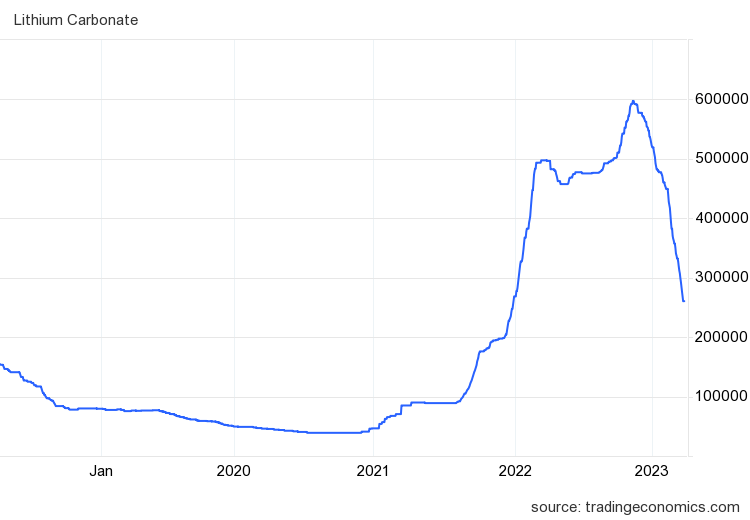

The company correctly points out that Albemarle has utilized the recent weakness in lithium prices to make an offer for Liontown. Lithium prices are down over 50% recently to below $40,000/t based on prices of 260,000 yuan in China.

Source: Trading Economics

The deal doesn’t exactly address the calculation of the effective enterprise value for Liontown. The Australian lithium miner has no outstanding debt with a cash balance of $384 million at the end of 2022, so the actual equity deal value is only in the $3.0 billion range.

Only Starting

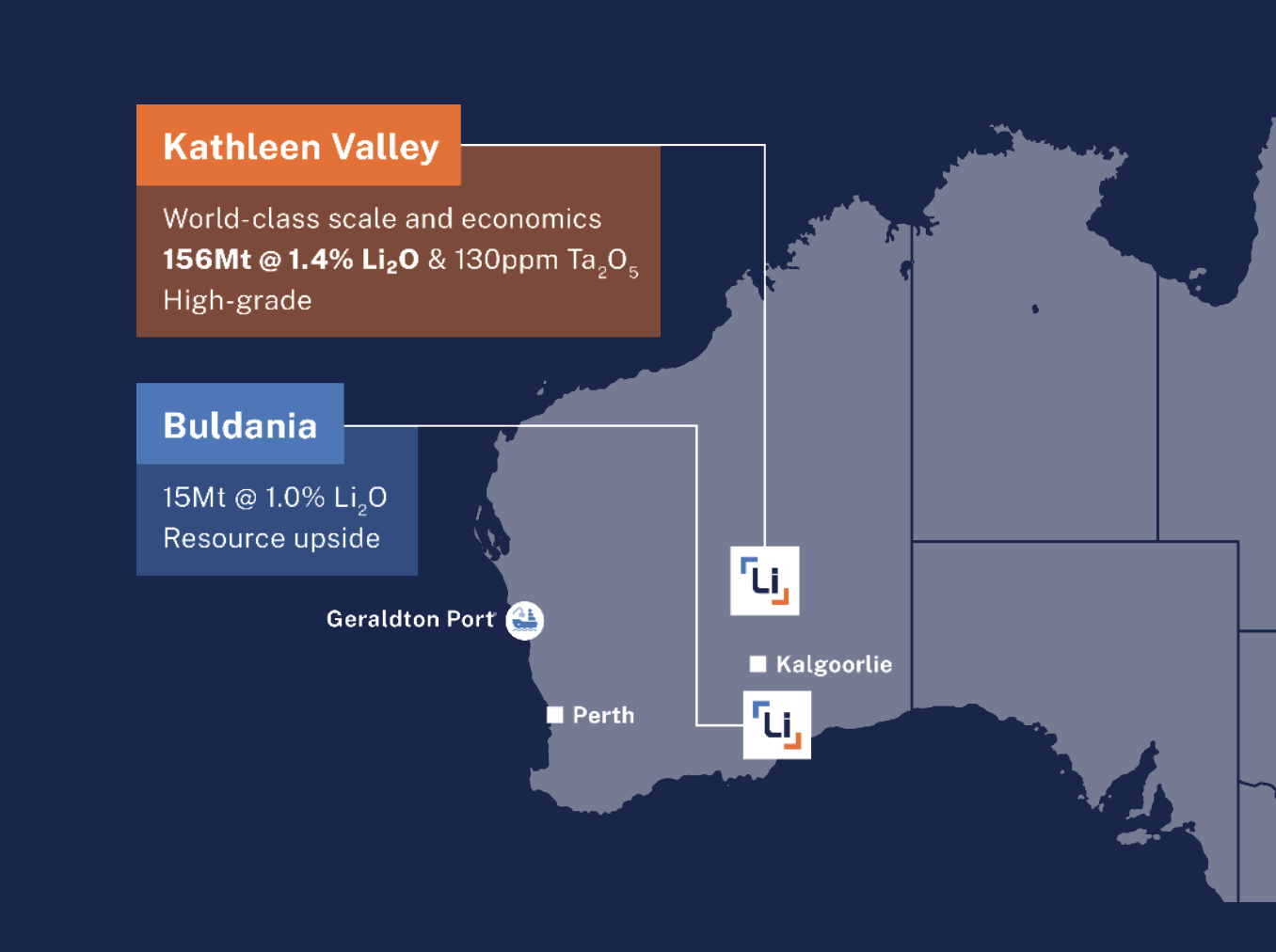

Liontown only recently started construction of the Kathleen Valley Lithium project in Australia. The company forecasts a total construction cost of ~$895 million with production starting in mid-2024.

Source: Liontown March ’23 presentation

The project already has off take agreements with LG Energy Solution, Tesla (TSLA) and Ford Motor Company (F). In fact, the major U.S. auto company agreed to extend a A$300 million debt facility to Liontown to ensure the company has the majority of capital to complete construction of the lithium mine.

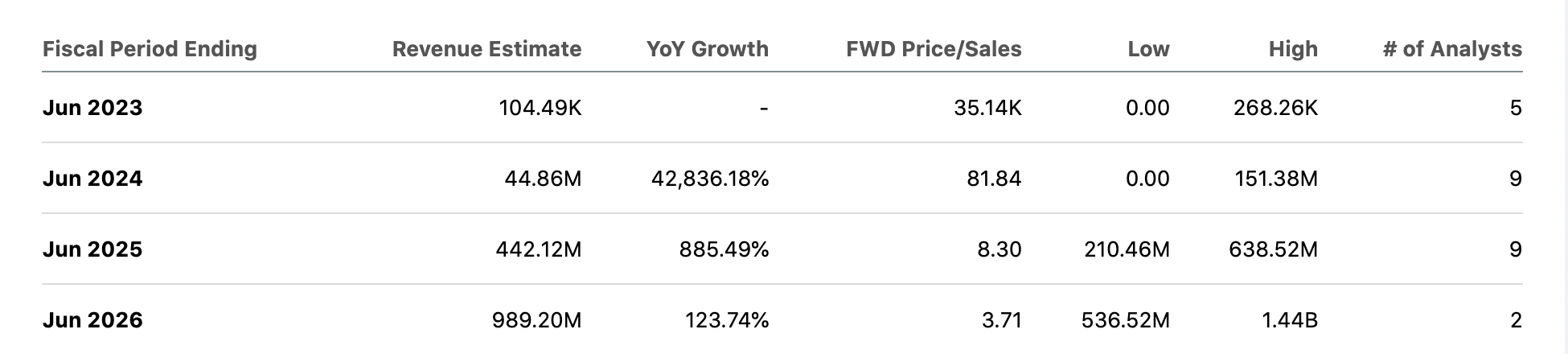

The lithium mine will have full production capacity of ~500ktpa of lithium with Kathleen Valley having a total reproduce of 156Mt. Analysts forecast 2025 revenues of $442 million jumping to nearly $1 billion in 2026.

Source: Seeking Alpha

The offer price doesn’t appear to fully factor in revenues surging in a few years solely from completing a new mine. In addition, Liontown has the Buldania mine in Western Australia as another growth driver with an indicated and inferred lithium deposit of 14.9Mt. The company is completing additional drilling holes and surveys to expand the resource total at this potential mine.

A lot of the revenue estimates in the sector are based on far lower lithium prices than the current price. The lithium market remains on track for significant structural deficits due to the surging EV demand.

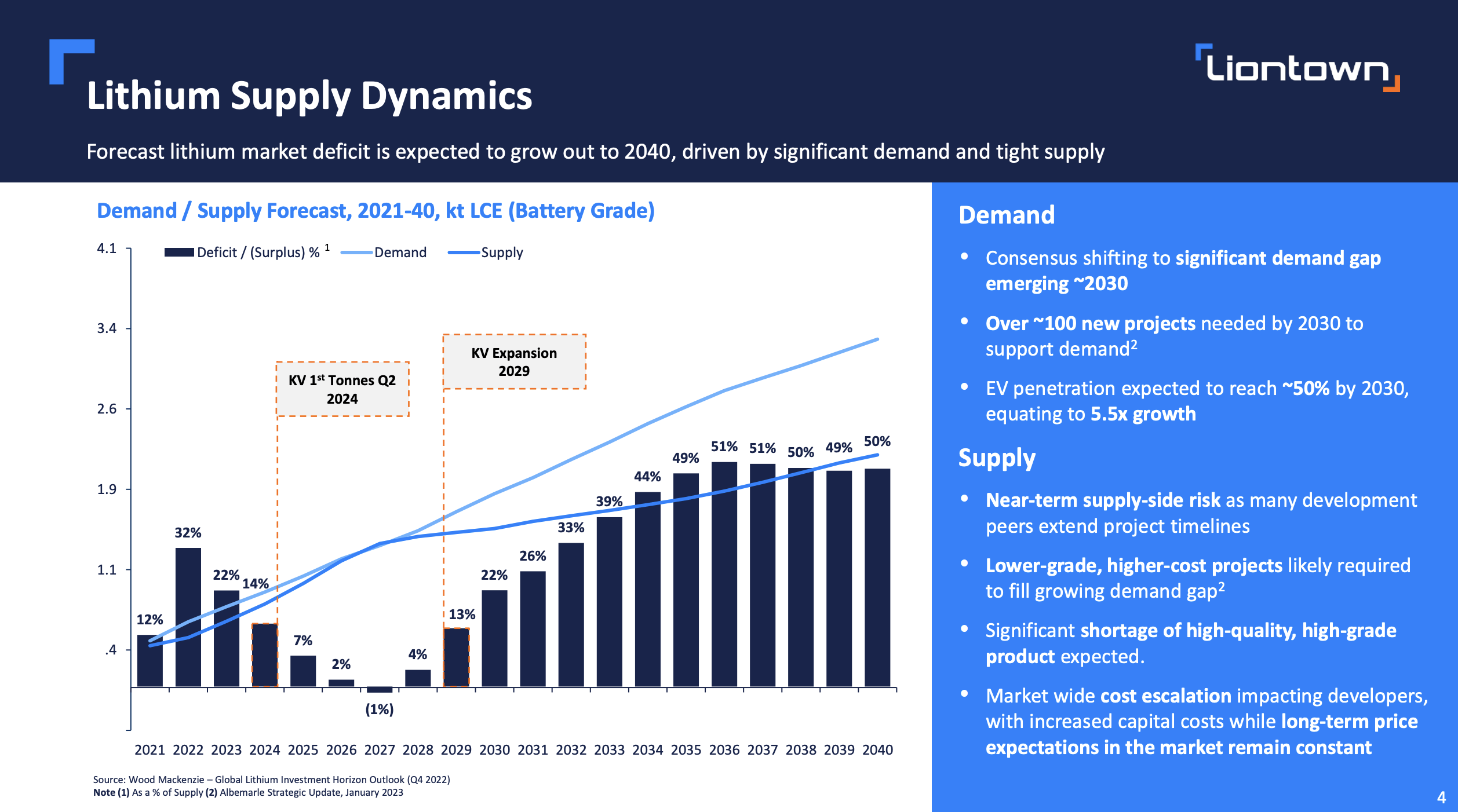

Analysts forecast ongoing supply shortages with a possible brief excess supply scenario in only 2027. The huge issue with supply is that so much of the new development projects are reliant on junior miners such as Liontown.

Source: Liontown March ’23 presentation

Liontown has no reason to cash out after the current offer price knowing so many of the 100+ small lithium projects are likely to struggle to reach production on time. Clearly, Albemarle management has internal forecasts supporting solid returns based on the projected lithium prices over time. So much so, the company started buying shares in the open market reaching a position of 2.2%.

Takeaway

The key investor takeaway is that Liontown has no reason to cash out at these prices. Lithium assets are in high demand and should only increase over the next decade leading to Albemarle likely increasing the offer price.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment