JHVEPhoto

After the market closed on July 20th, the management team at energy infrastructure and pipeline company Kinder Morgan (NYSE:KMI) released financial results covering the second quarter of the company’s 2022 fiscal year. In addition to beating on both its top and bottom lines relative to what analysts anticipated, the company posted strong cash flows and even went so far as to raise guidance for the current fiscal year. These are all positive developments that should encourage investors who currently own the stock while quelling the concerns of those bearish on it. At present, shares of the company are very cheap on an absolute basis and look affordable even relative to some other similar firms. Though not the best opportunity in this space, the enterprise does seem to offer some nice upside potential moving forward, causing me to retain my ‘buy’ rating on the firm.

Kinder Morgan Q2 Earnings – Great news all around

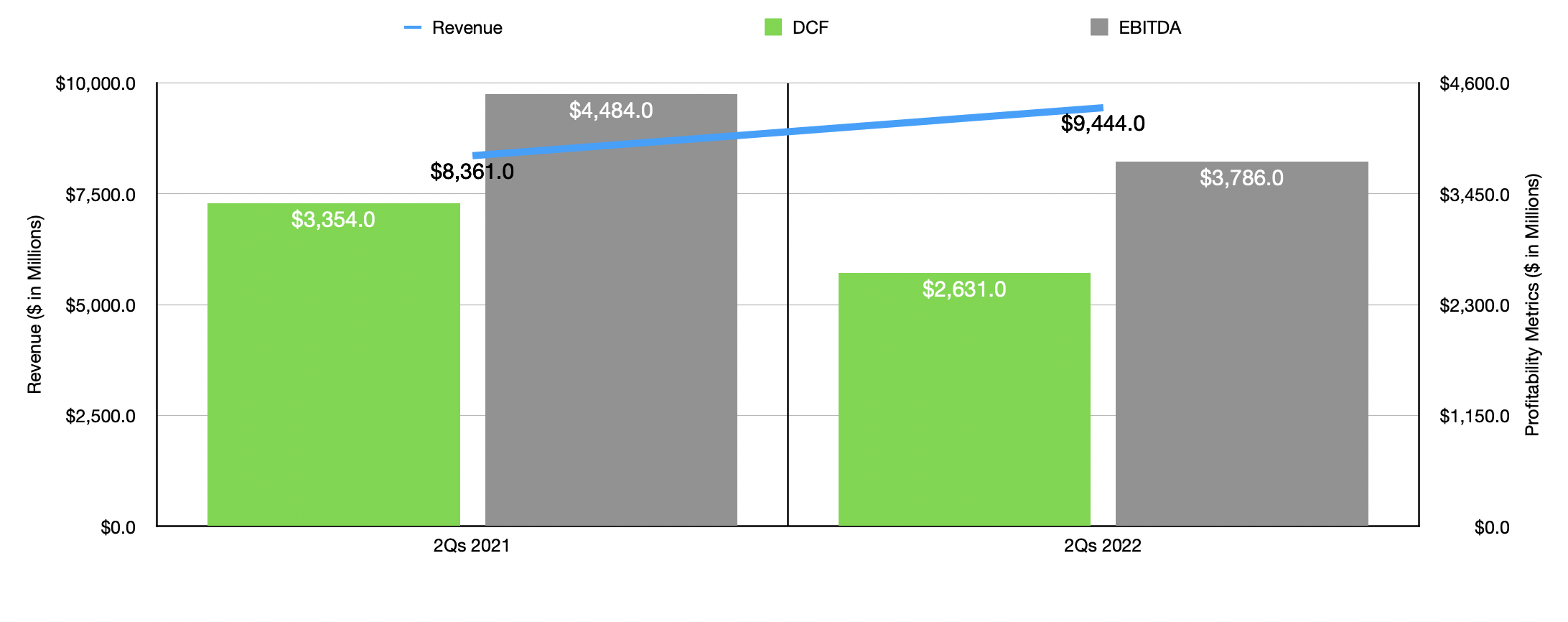

The headline news reported by Kinder Morgan was, in and of itself, a net positive for investors. Revenue of $5.15 billion was 63.5% higher than the $3.15 billion reported one year earlier. It also beat analysts’ expectations to the tune of $1.34 billion. Earnings per share were also attractive, coming in at $0.28 which was in line with what analysts expected. However, the adjusted earnings per share of $0.27 beat expectations by $0.01. Management attributed this strength to a few factors, including stronger than expected commodity prices and favorable operating results from its Natural Gas Pipelines and CO2 segments, some of which was offset by higher costs elsewhere. Although it is good that management fared so well compared to what the market anticipated, I generally do not put much value into revenue and earnings data for a company like this. Instead, I pay more attention to its cash flow figures.

Author – SEC EDGAR Data

Unfortunately, as of the time of this writing, we don’t know how much operating cash flow or free cash flow the company ultimately reported. This is because the firm has yet to release its 10-Q and what data it did reveal did not disclose its cash flow statement. But we do have some good proxies for that. One of these is the DCF, or distributable cash flow, of the company. In the latest quarter, this came in at $1.18 billion. This is 14.7% higher than the $1.03 billion reported just one year earlier. Another good proxy is EBITDA, which, in the latest quarter, came in at $1.82 billion. This is 8.9% above the $1.67 billion the company reported in the second quarter of its 2021 fiscal year. Because of these positive results and management’s expectation that strength will continue, the firm proudly boasted that it repurchased 16 million shares in the year-to-date period at an average price of $17.09 each. That ultimately cost investors $273.4 million. But given how cheap shares are, I see this as a great deal.

Author – SEC EDGAR Data

This strong quarter ultimately led the company to increase guidance for the current fiscal year. Previously, DCF was forecasted to be about $4.7 billion. Management now expects this to be about 5% higher than their previous target. That would translate to roughly $4.94 billion. The same 5% increase applies to EBITDA, taking that from $7.2 billion to $7.56 billion. No guidance was given when it came to operating cash flow. But if we assume that it will follow a similar trajectory, we should anticipate a reading of $5.57 billion. Stripping out maintenance or what management calls sustaining capital expenditures, which are those that are required to keep current operations running, we get what I refer to as true free cash flow. Based on my calculations, this figure should be roughly $4.67 billion.

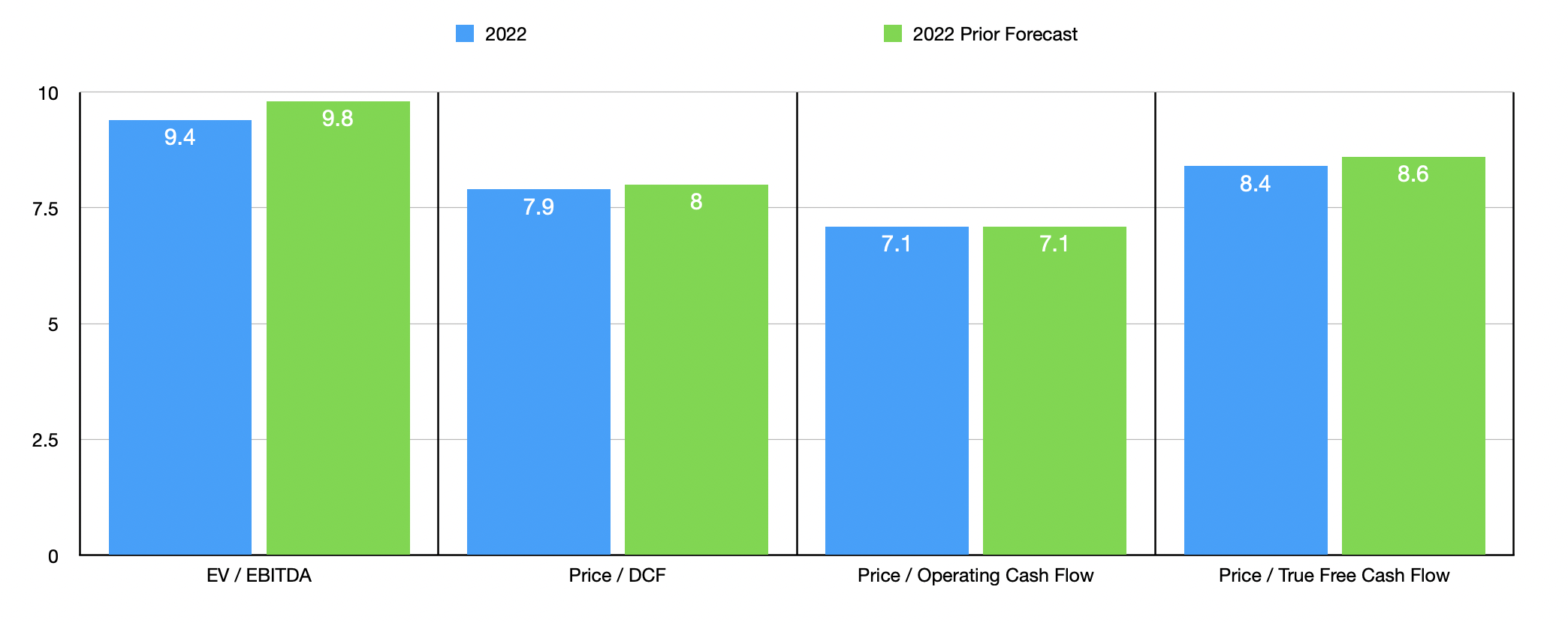

Taking this data, it becomes very easy to value the company. On a forward basis, the firm is trading at a price to adjusted operating cash flow multiple of 7.1. This compares to the 7.1 reading that I got when I last wrote about the business. This is in spite of the fact that shares are currently trading 1.7% higher than when I wrote my earnings preview on the company just the other day. The price to true free cash flow multiple, meanwhile, should be 8.4. This is down from the 8.6 in my prior article. The price to DCF multiple has also fallen, dipping from 8 to 7.9. And the EV to EBITDA multiple has fallen from 9.8 to 9.4.

Author – SEC EDGAR Data

To put the pricing of the company into perspective, I did decide to compare it to five similar firms. On a price to operating cash flow basis, these companies range from a low of 3.6 to a high of 9.6. In this scenario, three of the five companies were cheaper than Kinder Morgan. Using the EV to EBITDA approach, meanwhile, we end up with a range of between 8.3 and 391.2. In this scenario, only two of the five firms were cheaper than our prospect.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Kinder Morgan | 7.1 | 9.4 |

| The Williams Companies (WMB) | 9.6 | 12.6 |

| Energy Transfer (ET) | 3.6 | 8.3 |

| Cheniere Energy (LNG) | 8.5 | 391.2 |

| MPLX LP (MPLX) | 6.4 |

9.8 |

| TC Energy Corporation (TRP) | 9.4 |

13.3 |

Takeaway

Although it’s far from being the most popular player in the midstream space, Kinder Morgan does seem to be doing quite well at this time. Management continues to buy back stock when shares are cheap on an absolute basis and more or less fairly valued compared to similar firms. Guidance has recently increased and the overall fundamental condition of the business is robust. Because of all of these factors, I do believe the firm will likely generate returns that outpace the broader market moving forward, leading me to retain my ‘buy’ rating on the firm for now.

Be the first to comment