shaunl/E+ via Getty Images

Introduction

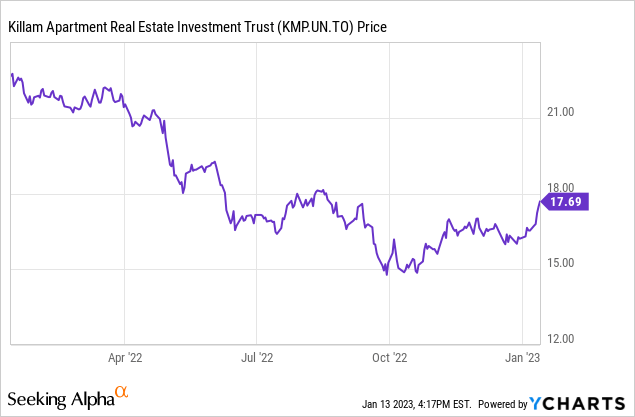

While residential REITs will always trade at a premium to pretty much every other real estate class out there, valuations have become more reasonable in the past six to nine months. As it has been a while since I last discussed Killam Apartment REIT (TSX:KMP.UN:CA) (OTC:KMMPF) I figured it’s time for an update as the stock has lost in excess of 20% in the past year while the AFFO per share increased by roughly 4%.

The FFO and AFFO continue to trend up

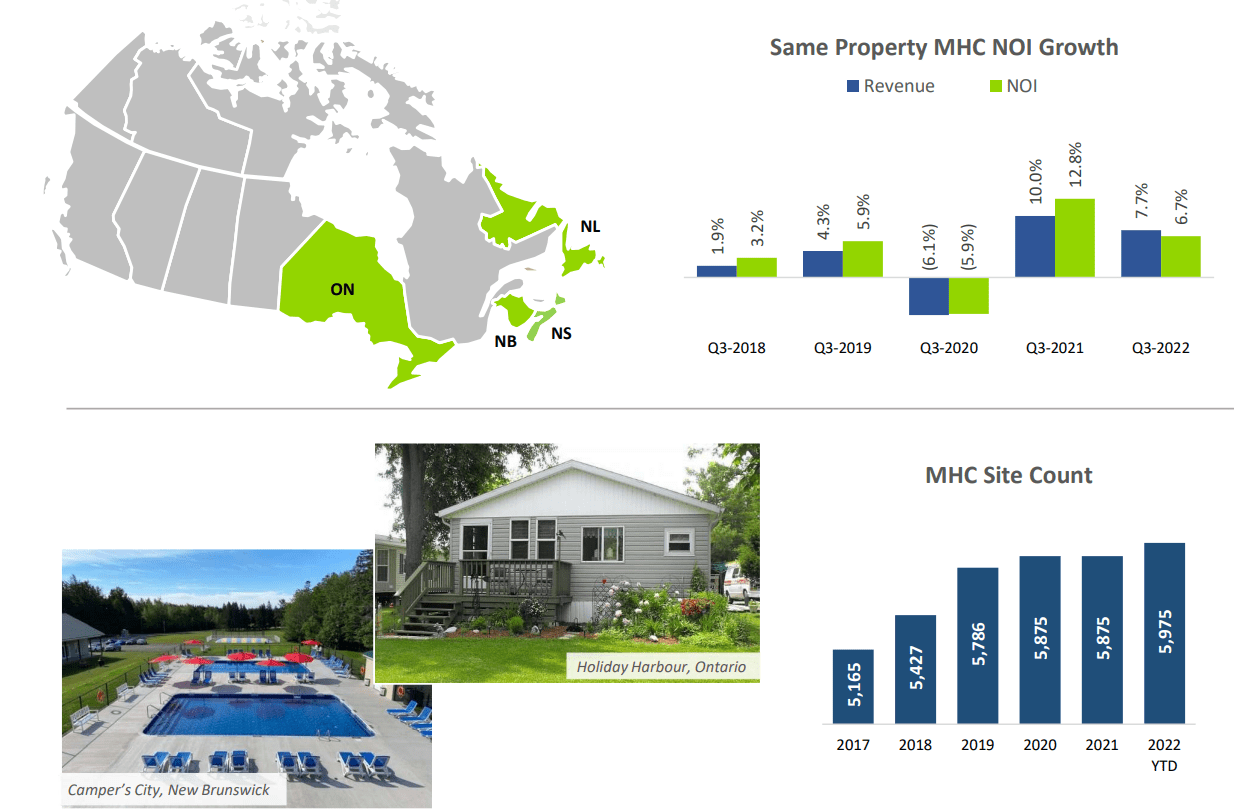

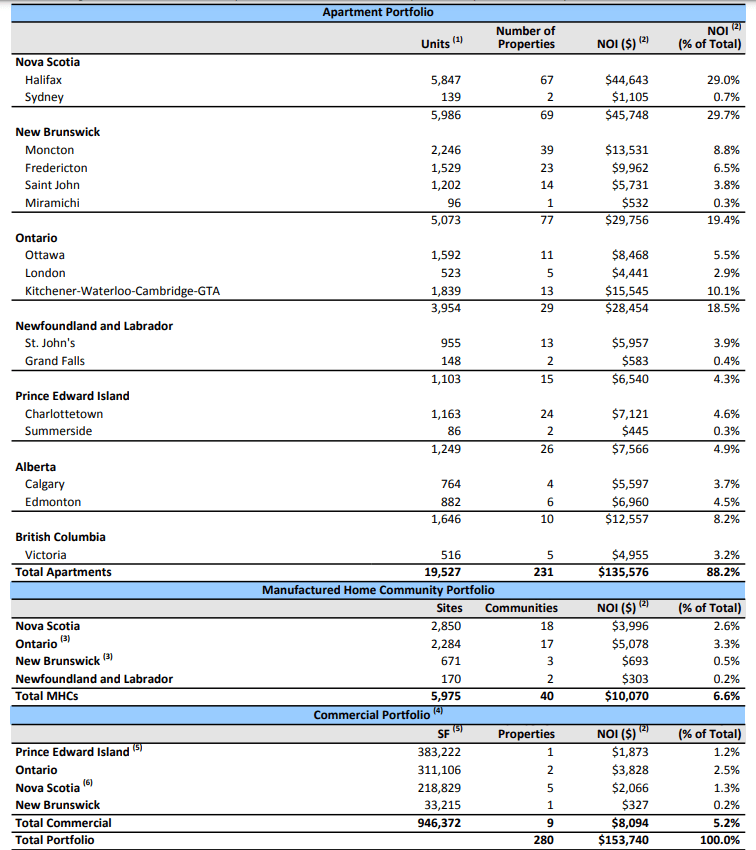

Killam Apartment REIT is mainly focusing on Canada’s east coast as the provinces of Nova Scotia and New Brunswick account for almost 60% of the total amount of apartments while a similar percentage of sites in the MHC portfolio can be found in those two provinces.

Killam Investor Relations

If you also would add in PEI and Newfoundland, almost 70% of the units in the apartment portfolio are located on the East Coast (excluding Ontario).

Killam Investor Relations

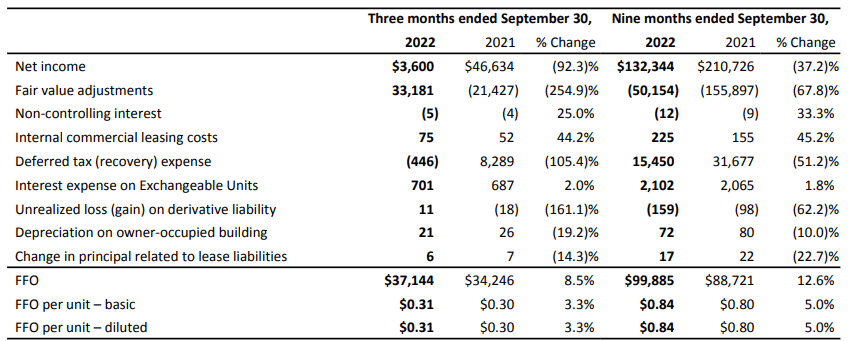

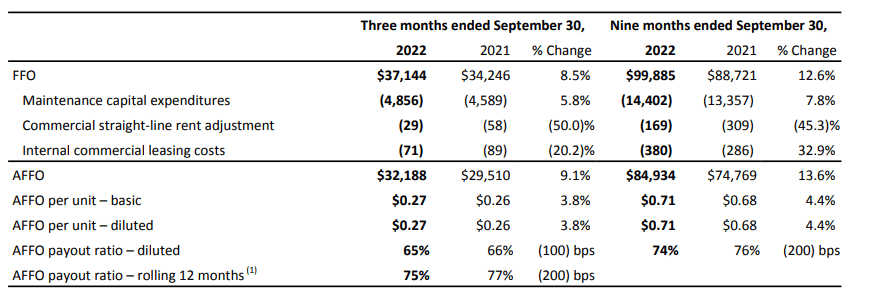

Looking at the REIT’s FFO performance, we see Killam generated about C$37.1M in FFO during the third quarter. While that’s an increase of 8.5% compared to the third quarter of the previous financial year, keep in mind the share count increased by just over 5% which means the FFO per unit increased by only 3% to C$0.31.

Killam Investor Relations

I’m generally more interested in the AFFO performance of a REIT, as that includes the maintenance capex. As you can see below, Killam incurred just under C$5M in maintenance capex on its buildings, resulting in an AFFO of C$32.2M. And while that is an increase of 9.1% compared to the third quarter of 2021, the higher share count means the AFFO per share increased by less than 4% to C$0.27.

Killam Investor Relations

That obviously still is a good result as it indicates Killam’s annualized AFFO is closing in on C$1.08 per share and the REIT remains on track to generate close to C$1 in AFFO per share in 2022 (it only generated C$0.44 per share in the first half of the year) and it should exceed that level in 2023.

A closer look at the book value per share

One element I wanted to have a closer look at is the REIT’s book value and its debt structure. The book value is of course important as it provides investors with some sort of ‘backstop’ as a REIT should not solely be valued based on an FFO or AFFO multiple. The debt structure is important to see how hard Killam would be hit by increasing interest rates.

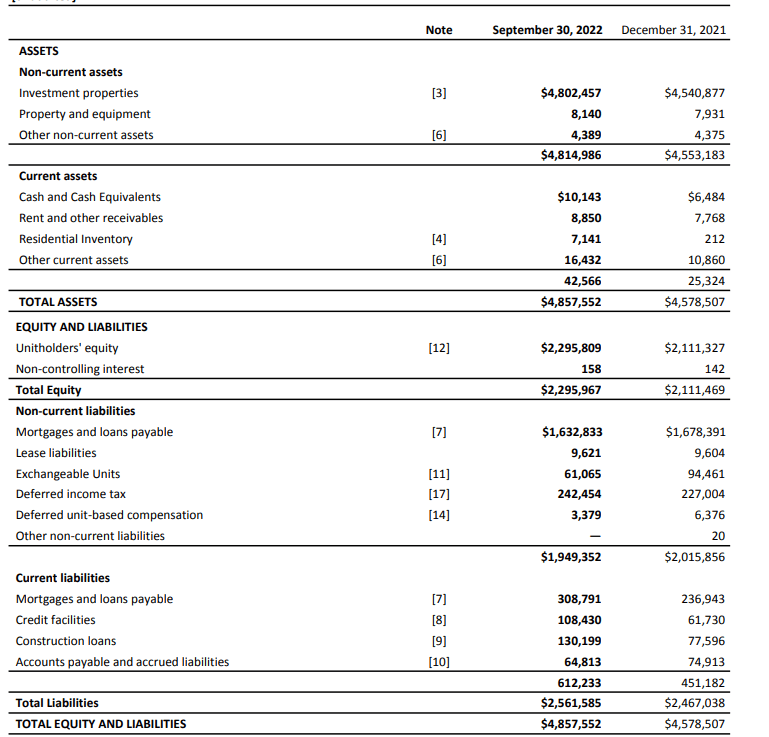

The balance sheet looks pretty robust. The total amount of assets is almost C$4.9B, with C$2.3B contributed by equity. If you include the exchangeable units, the equity level on the balance sheet would be even higher.

Killam Investor Relations

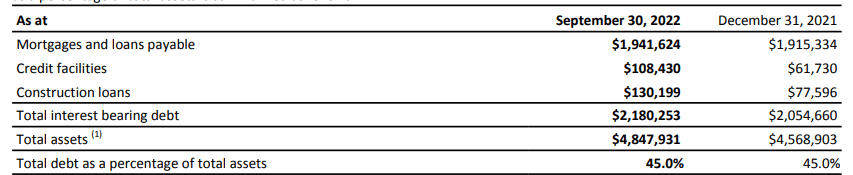

As of the end of September, the total debt level (debt versus assets, but excluding the cash position) was approximately 45%.

Killam Investor Relations

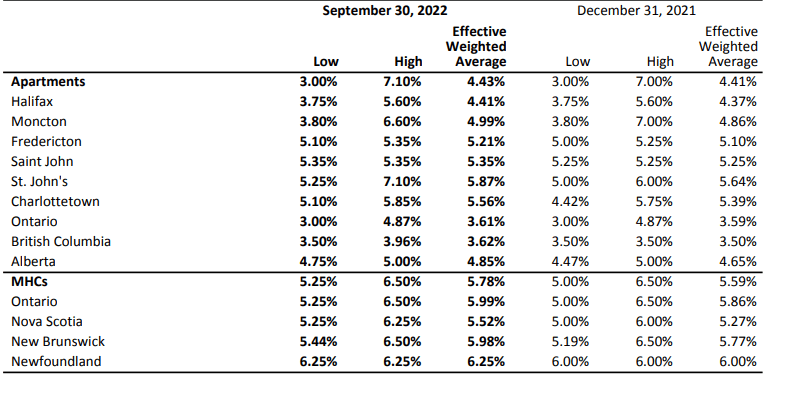

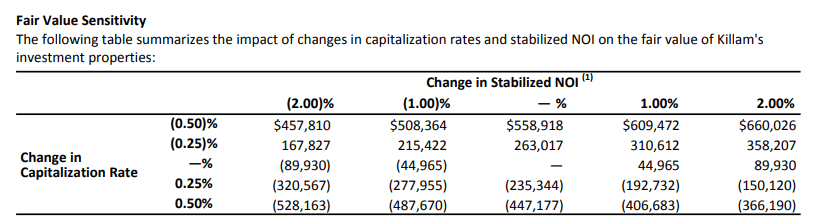

That’s great, but an important factor here is to figure out how the real estate assets were valued. Fortunately, the footnotes to the financial statements provide an update on the used capitalization rate and how the fair value would evolve based on changing cap rates. Killam even provides a nice breakdown of the capitalization rates it uses for the different geographic areas it is active in.

Killam Investor Relations

An increase of approximately 0.50% in the capitalization rate would reduce the fair value of the assets by C$447M. With 120.3M units outstanding (including the exchangeable units), the fair value per share would decrease by C$3.72 from almost C$20 to less than C$16.

Killam Investor Relations

That being said, every 2% increase in the NOI (which will be inflation-fueled) would add about C$90M in fair value to the properties. Should we see a simultaneous shock of a 75 basis point increase in the capitalization rate in combination with a 5% increase in the NOI, the total negative impact on the fair value would still be around C$3.75. And as I don’t expect a sudden 75 basis point increase in the cap rate, I think we should expect the C$16 level to be a backstop for Killam. The NOI will likely increase thanks to inflation-related rent hikes while the increase in the cap rates will likely remain limited to 50 basis points to just over 5% on a weighted average basis.

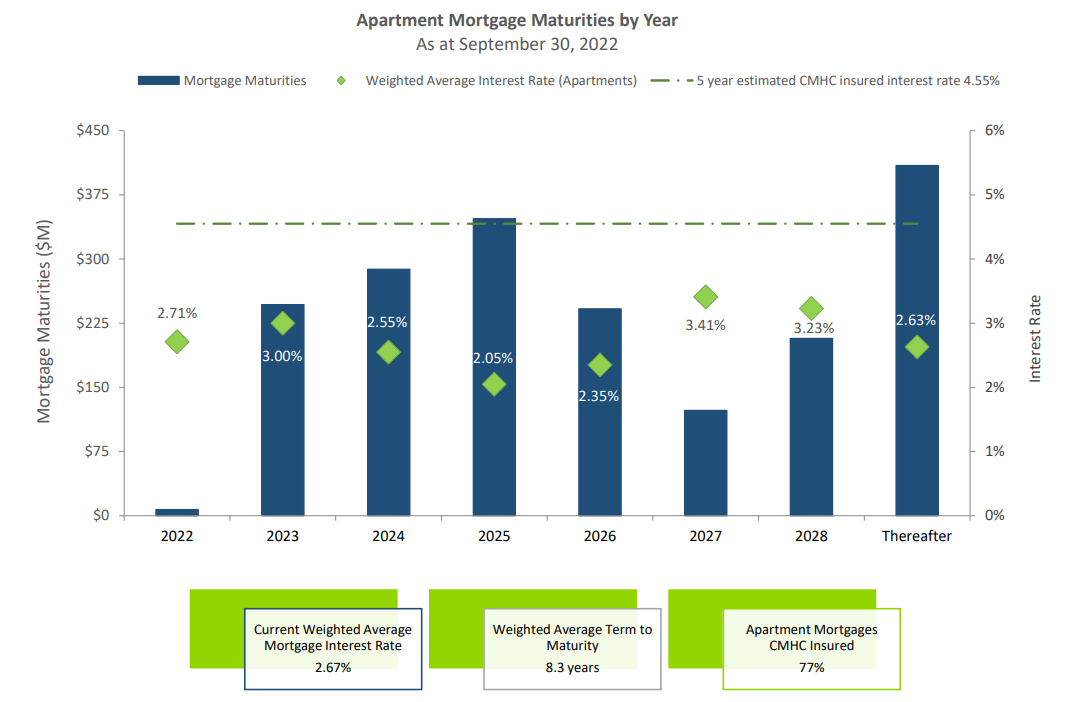

The main culprit for a weak AFFO increase in 2023 and 2024 will be the upcoming debt refinancings. In 2023, the REIT will have to refinance about C$247M in mortgage debt while in 2024 a more difficult exercise of C$290M in refinancings will have to be completed.

Killam Investor Relations

While I have zero doubt Killam will be able to refinance the mortgages, we will likely see the average interest rate increase by 150 basis points (if not more) which would increase the interest expenses by approximately C$8M. This will have a negative impact of approximately C$0.07 per share on the AFFO level. This does not mean I expect the AFFO per share to decrease in 2023 and 2024 as Killam should be able to increase its rental income as well. A 4%-5% increase in the NOI over the next two years should mitigate the impact of higher interest rates. And if Killam would for instance be able to hike the average rent by 8% in that two-year period, the AFFO per share would increase by C$0.07 per share. That would provide a welcome budder ahead of 2025 when a very cheap mortgage will have to be refinanced.

Investment thesis

I missed out on buying Killam when the stock was bottoming out in September and October, but I have no hard feelings. During those months, most REITs were slaughtered, and I decided to invest in a bunch of other real estate investment trusts. This doesn’t mean I’m snubbing Killam as I think that even after its recent 15% share price increase, the stock is still not outrageously expensive at just over 17 times AFFO. While that would be expensive for a commercial real estate REIT, it actually is good value for a residential REIT.

Notwithstanding the increasing interest rates and the anticipation of increased interest expenses, Killam should be able to continue to increase its AFFO albeit at a low single-digit pace (3-5% per year). By the end of next year, I expect Killam to be able to report an AFFO of closer to C$1.10 as new development projects will also start to contribute.

This means Killam is still attractive as I don’t think the REIT will see a major net impact from increasing interest rates. Killam currently pays C$0.70 in distributions on an annual basis in twelve equal monthly payments. The dividend yield is approximately 4%.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment