Introduction

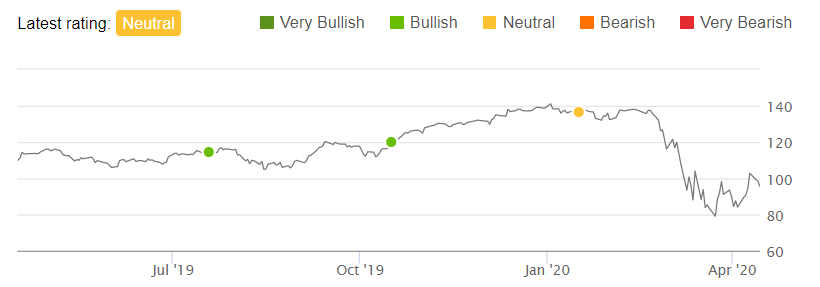

We had been a long-time bull on JPMorgan (JPM) and kept a Buy rating on the stock through 2019, but downgraded it to Neutral in January. Since then, the shares have fallen by more than 30%, as the COVID-19 lockdown continues:

|

Librarian Capital Ratings on JPM vs. Share Price Source: Seeking Alpha (14-Apr-20). Note: Valuation data in this article are based on JPM share price of $90.90, as of 12 noon EST on 15-Apr-20. |

Following a review of the 20Q1 results published yesterday, we upgrade our rating to Buy, as we believe the downside risk is now priced in.

COVID-19 Impact Not Fully Visible in 20Q1

COVID-19’s impact is not yet fully visible in 20Q1 results, having been a material event in Western economies only in the latter part of March.

While Net Income fell by 68.8% ($6.3bn) year-on-year in 20Q1, the decline can be entirely attributed to the $6.8bn in provisions for credit losses. Net Revenues fell by only 2.6% ($782m) year-on-year, primarily the result of markdowns in derivatives ($951m) and bridge loans ($896m), which are reported as part of Non-Interest Revenues; apart from these, revenues were relatively unimpacted in aggregate for the quarter:

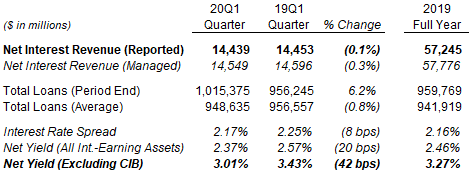

On a reported basis, Net Interest Revenue fell by only 0.1% year-on-year (0.3% on a managed basis), as U.S. rate cuts in 2019 continued to flow through JPM’s Interest Rate Spread. Average loans fell 0.8% year-on-year due to the sale of some Home Lending loans, otherwise they would have risen 3%. However, the end-of-period total loans balance was up 6.2% year-on-year (and 5.8% quarter-on-quarter), as companies drew down their credit facilities or took up new loans while COVID-19 fears reverberated through markets:

|

JPM Interest Revenue & Loans (Reported Basis) (20Q1)

Source: JPM results supplement (20Q1). |

Strong Balance & Liquidity

JPM continues to enjoy a “fortress” balance sheet. CET1 ratio was 11.5% at the end of 20Q1, within the 11-12% management target (which in turn contains a large buffer over the regulatory minimum). The 90 bps fall in the CET1 ratio from 19Q4 was mostly due to a 64 bps impact from Risk Weighted Assets (“RWA”) growth, which included the effect of more lending as well as market volatility; the impact from credit provisions was only 21 bps:

JPM also continues to enjoy strong liquidity. Despite the rise in loan balances mentioned above, deposit balances rose even faster as consumers and businesses sought the safety that JPM offers, which meant the Loan / Deposit Ratio fell to 55% from 61% in 19Q4.

At the current share price of $90.90, JPM is trading on 1.5x Price / Tangible Book Value (“P/TBV”) ($60.71 per share). The P/E is 7.6x relative to 2019 Net Income, and the latest Dividend Yield is 4.0% ($3.60 per share).

Further Reserve Build & Revenue Declines Likely

While the full impact of COVID-19 remains hard to quantify, there will almost certainly be more reserve build and revenue declines in the rest of 2020.

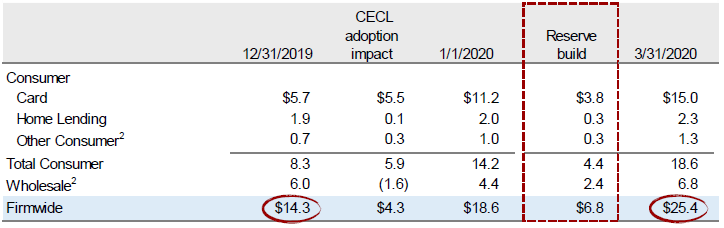

The $6.8bn reserve build in 20Q1 was primarily in Consumer Card ($3.8bn) and Wholesale ($2.4bn) (especially in oil & gas and retail):

|

JPM 20Q1 Reserve Build by Area ($bn)

Source: JPM results presentation (20Q1). |

However, these provisions were based on management expectations of what will happen, not actual loan delinquencies; as the CFO said on the call, JPM “haven’t actually seen the stress emerge as of yet” in loan books. In the Consumer & Community Banking (“CCB”) segment, charge-off and delinquency ratios had seen no material changes in 20Q1 (with the increase in Card charge-offs being a long-term trend due to seasoning):

The assumptions behind the reserve build in 20Q1 were as of the end of the quarter. However, these expectations have already been superceded by more negative views (40% GDP decline and 20% unemployment), which means that more reserve build is likely in the rest of 2020. As the CFO stated on the call:

“This reserve increase assumes in the second quarter that U.S. GDP is down approximately 25% and the unemployment rate rises above 10%, followed by solid recovery over the second half of the year … We have also assumed that the stress in oil and gas continues with WTI remaining below $40 through the end of 2021.

After we closed the books for the quarter, our economists updated their outlook, which now reflect a more significant deterioration in U.S. GDP and unemployment. If that scenario were to hold, we would be building in the second quarter and builds could be meaningfully higher in aggregate over the next several quarters relative to what we took in the first quarter”

Jennifer Piepszak, JPM CFO (20Q1 earnings call)

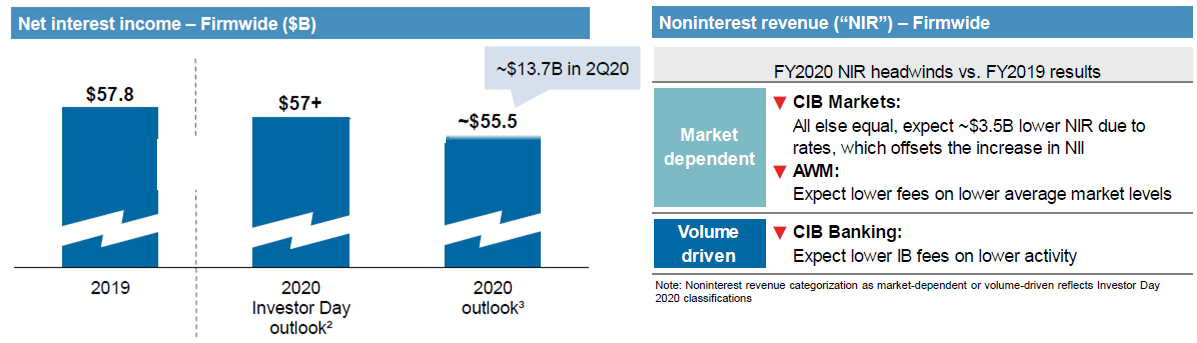

While 20Q1 revenue was relatively stable (outside derivative and bridge loan mark-downs), revenue guidance for the rest of 2020 was significantly reduced. Net Interest Income is now expected to be $55.5bn (implying a 4% year-on-year decline), compared to $57bn+ at the investor day in February, due to lower interest rates. Similarly, Non-Interest Revenues are expected to be at least $3.5bn lower in Corporate & Investment Banking (“CIB”), also due to lower rates; they will be lower in Asset & Wealth Management (“AWM”) due to lower market levels for client assets, and lower in CIB again due to less investment banking fees:

|

JPM Revenue Outlook (2020)

Source: JPM results presentation (20Q1). |

Worst Case TBV Per Share & ROTCE

As it is impossible to determine the duration of the COVID-19 lockdown, we believe the way to evaluate the attractiveness of JPM shares is to make estimates of its TBV after 2020 credit losses and of its long-term Return on Tangible Common Equity (“ROTCE”).

For TBV, JPM has run its own “extremely adverse” scenario, which is tougher than the Federal Reserve’s stress test, and serves as a reasonable “worst case” scenario. As CEO Jamie Dimon explained in his annual shareholder letter:

“In the Fed’s scenario, we would be profitable in every quarter … Additionally, we have run an extremely adverse scenario that assumes an even deeper contraction of gross domestic product, down as much as 35% in the second quarter and lasting through the end of the year, and with U.S. unemployment continuing to increase, peaking at 14% in the fourth quarter. Even under this scenario, the company would still end the year with strong liquidity and a CET1 ratio of approximately 9.5% (common equity Tier 1 capital would still total $170 billion)”

Jamie Dimon, JPM CEO (JPM 2020 shareholder letter)

The $170bn TBV figure (approx. $56 per share) for 2020 year end in this scenario implies a decline of roughly 8% from the current figure of $185bn ($60.71 per share), which we will take as our “worst case” TBV.

For ROTCE, for the last few years, management has targeted a 17% across-the-cycle figure (15% before the U.S. tax cut), and management comments had indicated that this is an average figure that included cyclical downturns:

“I can get overdue in the pressure in the banking industry … We have had growth in the United States for the better part of 10 years, and I say that the credit is extraordinarily good. So if you look at consumer credit, commercial credit, wholesale, NCO, it’s all extraordinarily good. It can only get worse if there is a cycle. So our 17% (ROTCE target) … we always try to plan this through the cycle … we are at the over-earning part of the cycle in credit today; at one point we will be at the under-earning part on credit.”

Jamie Dimon, JPM CEO (19Q3 earnings call)

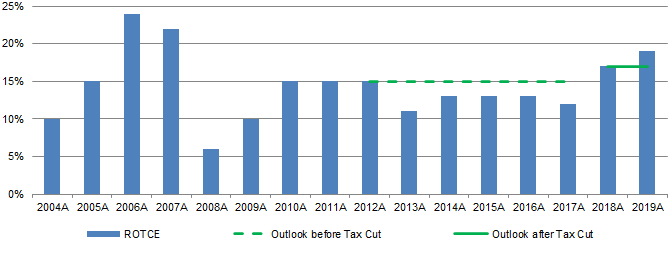

JPM had achieved ROTCE of 10%+ every year since Dimon joined, except for one year (2008) when it was 6%; ROTCE was positive even for 2008 and 2009, and recovered to 15% within 2 years of the Great Financial Crisis:

|

JPM ROTCE vs. Medium-Term Outlook (2005-19)

Source: JPM results supplements. |

We believe that long-term ROTCE will likely be at least 10% even in the “worst case”, and is most likely to be much closer to the original 17% target. As outlined in our initiation article in February 2019, large U.S. retail banks like JPM are favored by their scale and a benign competitive landscape; the track record and culture built by Jamie Dimon over the last 15 years also provide strong reasons to believe in a high long-term ROTCE.

Even in the “worst case” scenario, with a $56 TBV per share and a 10% ROTCE, the implied long-term EPS of $5.60 would give a 16.2x P/E and a 6% Dividend Yield relative to the current share price (assuming JPM continues to distribute all its earnings).

Illustrative Returns Sensitivity Analysis

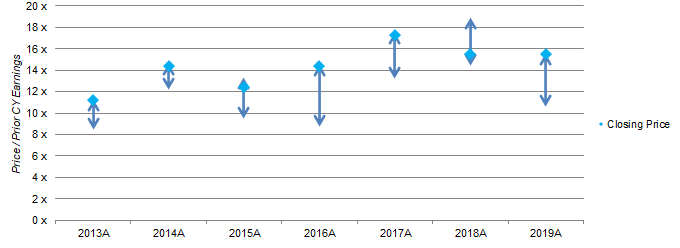

In this section we look at the range of potential investor returns from different TBV and ROTCE figures. We assume a 12x P/E, which is lower than the range in most of 2017-19, and is at roughly the midpoint of the range in 2013-16:

|

JPM Historic P/E Range (2013-19A)

Source: JPM company filings. |

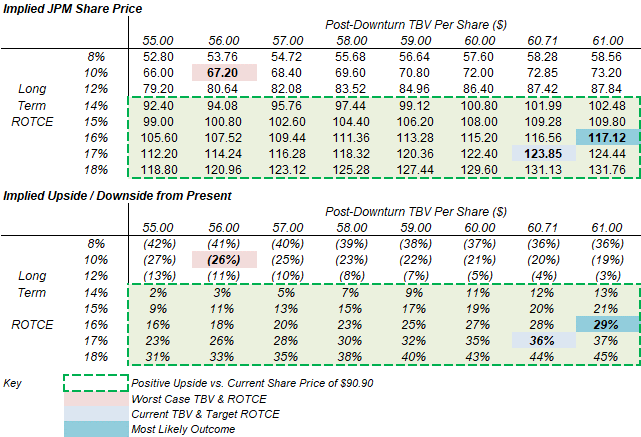

The range of upside/downside for various TBV and ROTCE is shown below; we have conservatively assumed no dividends for the next 2 years. For example, in our “worst case”, with a TBV per share of $56 and a ROTCE of 10%, thus a long-term EPS of $5.60, the shares will be worth $67.20, which implies a 26% downside from the current share price of $90.90. On the other hand, if JPM emerges from the downturn with a flat TBV ($60.71) and achieves its 17% ROTCE target, then the share price will be $123.85 (implying a 36% upside):

|

JPM Share Price vs. Post-Downturn TBV & ROTCE (on 12x P/E)

Source: Librarian Capital estimates. |

{kind=link}

As shown above, ROTCE is the primary driver of upside/downside in this set of scenarios. If JPM could return to a 14% ROTCE, then even in the “worst case” TBV of $56 per share, investors would have a small (3%) positive total return.

We believe the most likely outcome is for JPM to emerge from the downturn with a flat or slightly up TBV per share ($61) and a 16% ROTCE in 2 years’ time, implying a share price of $117.12 and a 29% total upside, i.e. a double-digit annualized return.

We believe that the risk/reward is weighted towards the upside, and upgrade our rating on JPM to Buy accordingly. (We currently have a Buy rating on Bank of America (BAC); we have no coverage on Citi (C), U.S. Bancorp (USB) and Wells Fargo (WFC)).

Conclusion

COVID-19’s impact is not fully visible in JPM’s 20Q1 results, and we expect further reserve build and revenue declines in the rest of 2020. However, with shares now more than 30% lower since our downgrade, we believe the downside has been priced in.

Management’s own “extremely adverse” scenario serves as our “worst case”, setting a floor for TBV / share; investor return would be positive even in this “worst case” if ROTCE could recover to 14%.

We believe the most likely outcome is for JPM to emerge from the downturn in 2 years’ time with a flat or slightly up TBV per share, and a 16% long-term ROTCE. In this scenario, applying a 12x P/E, the shares are worth $117.12.

Relative to the current share price of $90.90, this implies a 29% total upside and a double-digit annualized return. We upgrade JPM to Buy.

Note: A track record of my past recommendations can be found here.

Disclosure: I am/we are long BAC,JPM. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment