Jonathan Kitchen/DigitalVision via Getty Images

JPMorgan Equity Premium Income ETF (NYSEARCA:JEPI) is a covered call exchange-traded fund (“ETF”) that invests in low volatility stocks and distributes monthly income it receives from stock dividends and option premiums collected from covered calls. Many of you are probably familiar with options and the covered call strategy, but for those of you who are not –

Covered Calls

A covered call is a contract you enter into when you hold a stock and sell the right to a third party to buy the stock at a certain price (Strike price) and by a certain date (Expiration date).

Typically, 1 option accounts for 100 shares of stock, so if you sell 1 covered call then you would need to hold 100 shares of the stock to cover the call you are selling.

You, as the seller of the call option, receive a payment (premium) in return for the obligation to sell your shares at the strike price by the expiration date if the option is called.

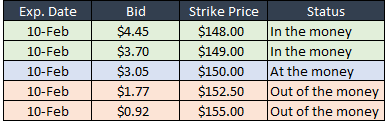

So, to put this as an example, say you bought 100 shares of Apple Inc. (AAPL) stock at a market price of $150.00 per share for a total purchase price of $15,000.

To generate some income, you decide to sell a covered call at a strike price of $150.00, which in this example is the same as the market price and would be considered “at the money.”

The Bid amount listed is the premium you receive per share, so for an option sold at the money you would receive a premium of $305.00 ($3.05 x 100 shares).

Nasdaq (compiled by iREIT)

If by the expiration date the shares are still trading at $150.00, the option buyer probably won’t choose to exercise the option since they can buy the stock for the same price on the open market. In this case, you would keep the shares and the premium you received.

If by expiration the shares are trading at $149.00, it is unlikely the option buyer will choose to exercise the option because they can buy shares for less on the open market than the strike price of $150.00.

In this case you would keep the shares and the premium you received. The loss of $100.00 would be offset by the premium of $305.00 and you would have made a gain even though the stock price went down.

If the stock had a good run and is now trading at $160.00, then the option buyer will almost always exercise their right to call the stock away from you at the strike price of $150.00 because they can turn around and sell it at the market price of $160.00.

In any event, the seller of the call option gets to keep the premium, but if the stock is trading above the strike price, the seller forfeits any gain past that level.

The option seller could choose to sell the covered call several strikes out of the money and receive the premium plus some upside potential.

Assuming the market price was $150.00, if you sold a covered call with a strike price of $155.00 and the market price went to $160.00 then you’d receive $15,500 plus the premium of $92.00 for a total gain of $592.00 vs $1,000.00 if you held the stock without selling an option on it. However, if the stock fell in price to $145.00 then your loss would be offset by the premium received.

There is a lot more involved with options but suffice it to say that selling cover calls provides income while hedging against a drop in price, but also limits gains at the selected strike price. Cover calls tend to work best in a flat to slightly rising markets.

While not many people find it enjoyable to read about options, it is important to understand the basic mechanics to understand how a cover call ETF works.

JEPI Objectives

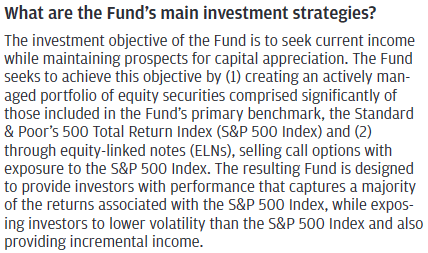

JPMorgan Equity Premium Income ETF aims to provide current income while maintaining prospects for capital gains. The ETF is designed to capture a portion of the returns of the S&P 500 (SP500) but with lower volatility and higher yields. In order to accomplish these objectives, their strategy involves active stock selection, seeking stocks with lower volatility, and selling covered call options through Equity-Linked Notes (“ELN”).

JEPI – Summary Prospectus

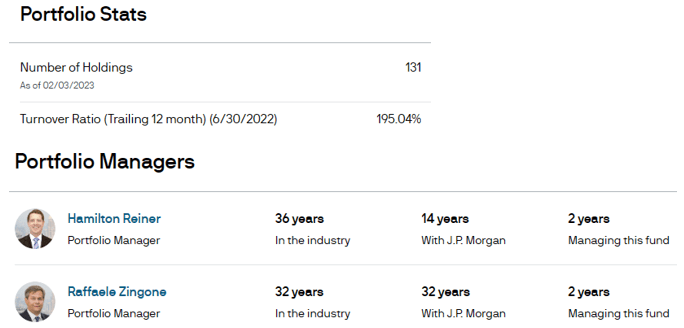

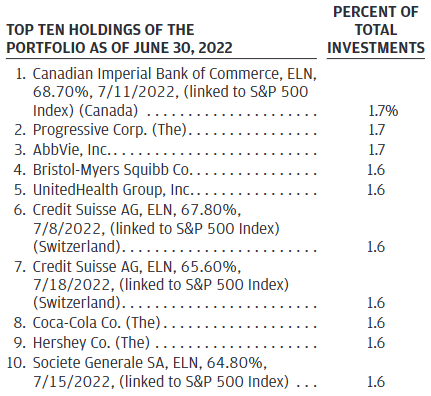

While they describe the S&P 500 as JEPI’s primary benchmark, the fund is actively managed and can hold securities outside of the S&P 500. The number of holdings in JEPI is much different than the S&P 500, with 131 holdings as of February 3, 2023.

Their weightings are very different as well, with JEPI’s top ten holdings bearing no resemblance to that of the S&P 500. JEPI is actively managed, so while they primarily hold stocks in the S&P 500, they rely heavily on stock selection and overall portfolio composition to compete with the index. For the trailing 12 months as of June 30, 2022, they had a turnover ratio of 195.04%.

JEPI

JEPI Holdings

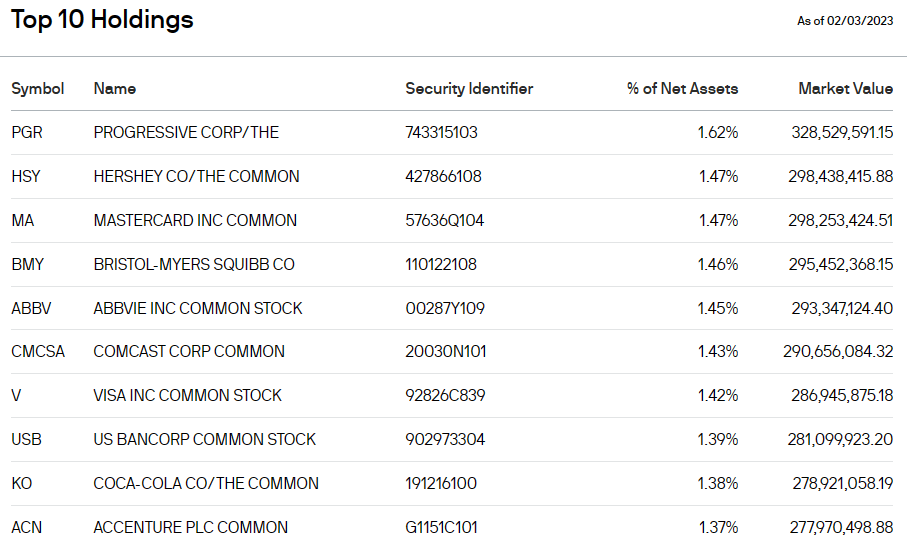

JEPI is well-diversified, with low concentration in its top 10 stock holdings. On average, each position in its top 10 is 1.446% of their overall portfolio. Combined, their top 10 stock holdings make up 14.46% of their total holdings.

Although JEPI is an income fund, it selects its holdings to maximize risk-adjusted total return and does not select its holdings based on current yield, as most of the distributions paid by JEPI come from selling covered calls.

JEPI

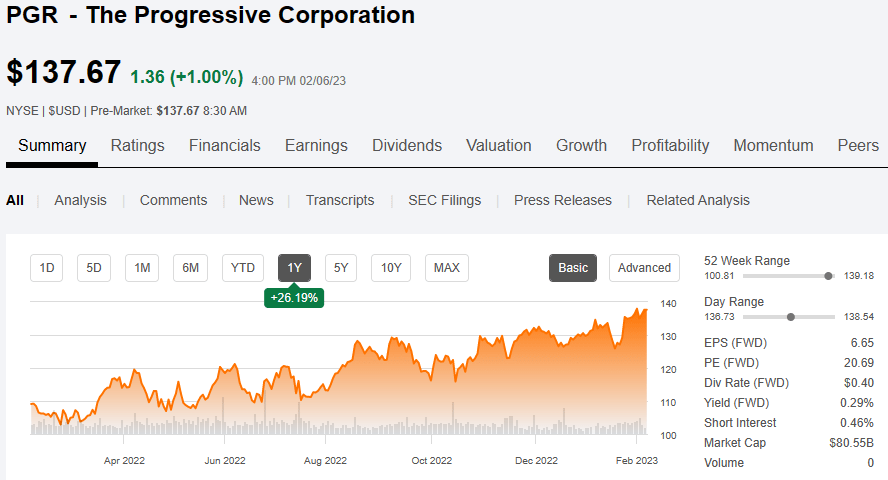

The Progressive Corporation (PGR)

Progressive Corp is an insurance company with a total market cap of $80.55 billion. PGR pays a dividend yield of 0.29% and has a Forward P/E ratio of 20.69x with a 5-year Beta of 0.48. Over the past year, PGR has returned +26.19%.

Seeking Alpha

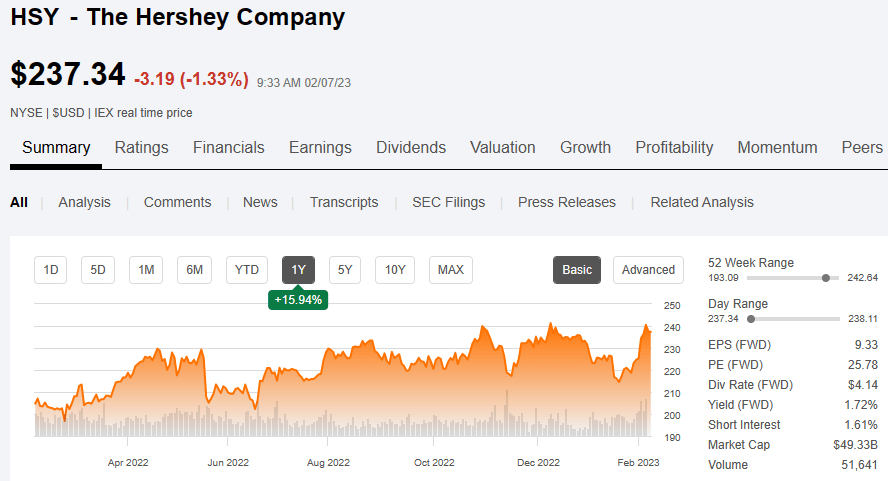

The Hershey Company (HSY)

Hershey Co is classified as a confectioner and has a total market cap of $49.33 billion. HSY pays a dividend yield of 1.72% and has a Forward P/E of 25.78x with a 5-year Beta of 0.35. Over the past year, HSY has returned +15.94%.

Seeking Alpha

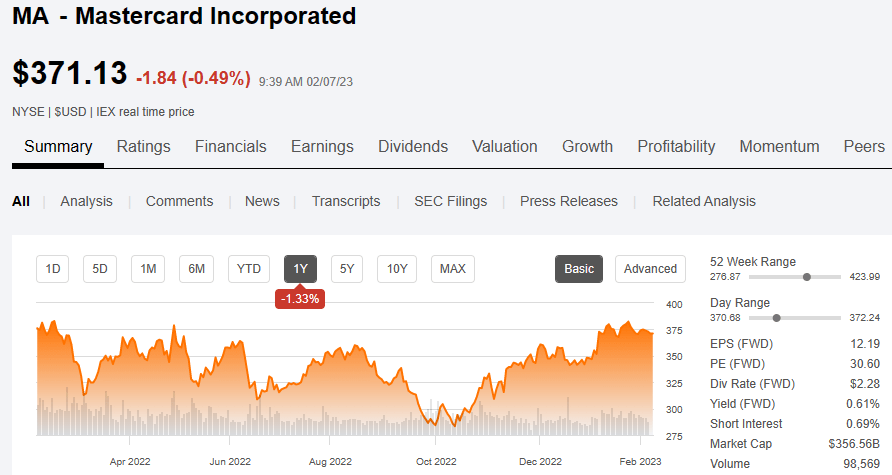

Mastercard Incorporated (MA)

Mastercard is in the Financial Services sector and has a total market cap of $356.56 billion. MA pays a dividend yield of 0.61% and has a Forward P/E of 30.60x with a 5-year Beta of 1.08. Over the past year, MA has returned -1.33%.

Seeking Alpha

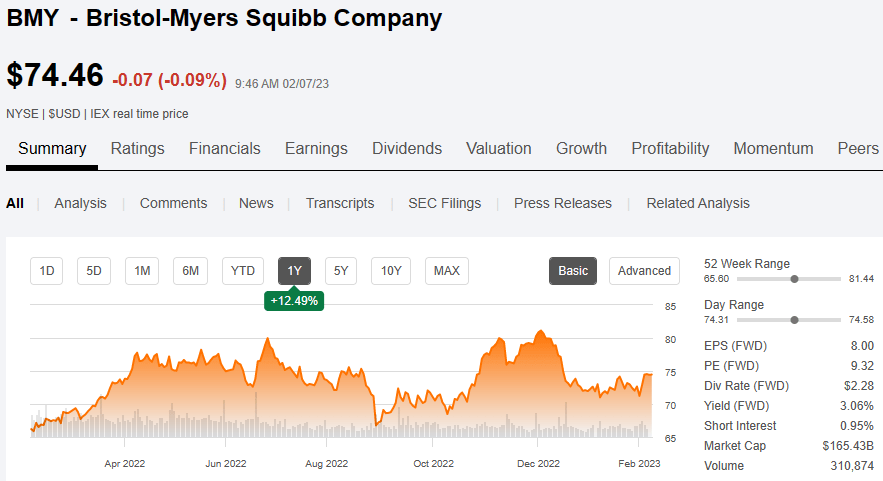

Bristol-Myers Squibb Company (BMY)

Bristol-Myers Squibb Co is a multinational pharmaceutical company with a total market cap of $165.43 billion. BMY pays a dividend yield of 3.06% and has a Forward P/E of 9.32x, with a 5-year Beta of 0.43. Over the past year BMY has returned +12.49%.

Seeking Alpha

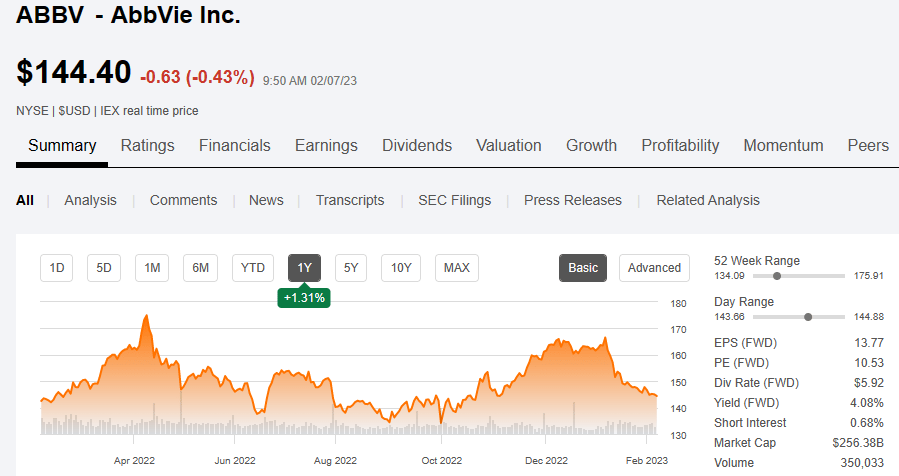

AbbVie Inc. (ABBV)

AbbVie Inc is a biopharmaceutical company with a total market cap of $256.38 billion. ABBV pays a dividend yield of 4.08% and has a Forward P/E of 10.53x with a 5-year Beta of 0.61. Over the past year ABBV has returned +1.31%.

Seeking Alpha

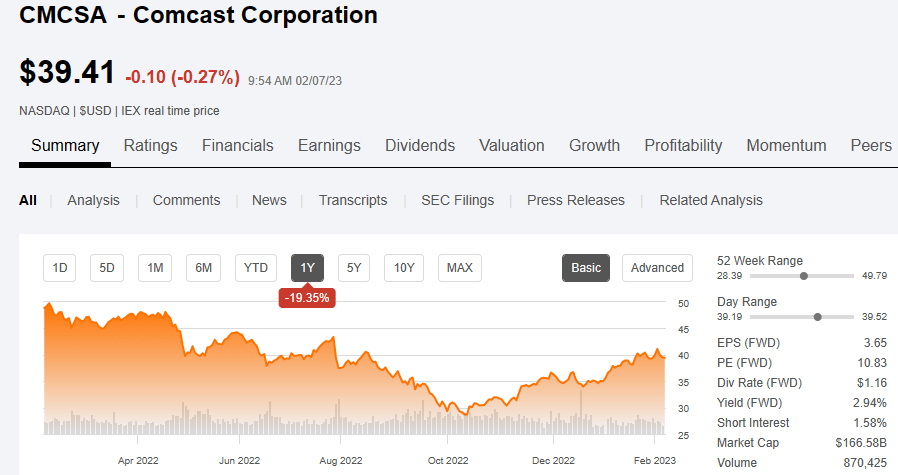

Comcast Corporation (CMCSA)

Comcast Corporation is telecommunications conglomerate with a total market cap of $166.58 billion. CMCSA pays a dividend yield of 2.94% and has a Forward P/E of 10.83x with a 5-year Beta of 1.02. Over the past year, CMCSA has returned -19.35%.

Seeking Alpha

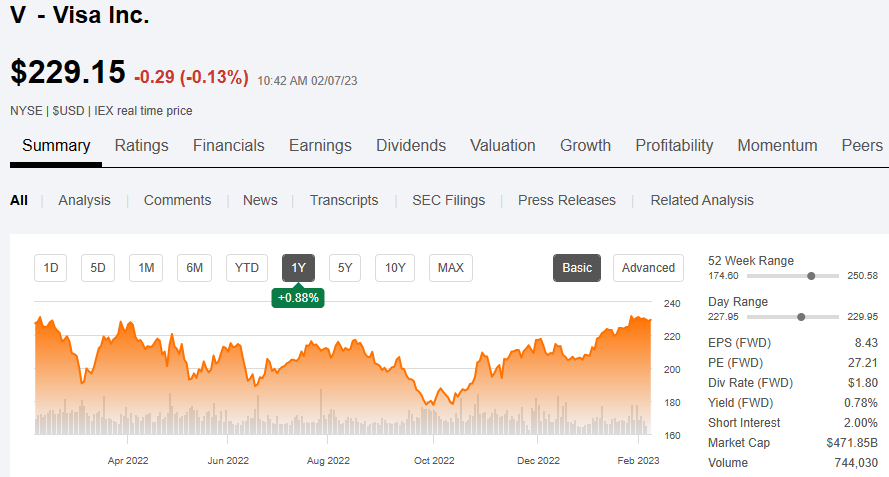

Visa Inc. (V)

Visa is a multinational financial services corporation with a total market cap of $471.85 billion. Visa pays a dividend yield of 0.78% and has a Forward P/E of 27.21x with a 5-year Beta of 0.96. Over the past year, Visa has returned +0.88%.

Seeking Alpha

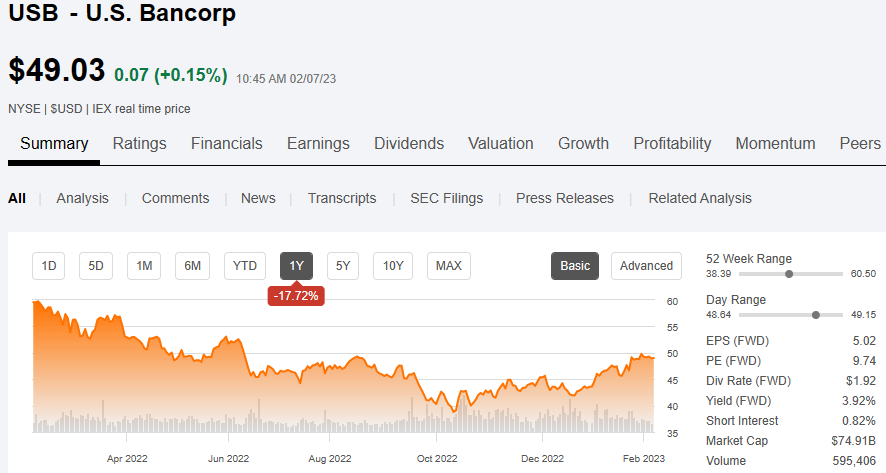

U.S. Bancorp (USB)

US Bancorp is an American bank holding company with a total market cap of $74.91 billion. USB pays a dividend yield of 3.92% and has a Forward P/E of 9.74x with a 5-year Beta of 0.98. Over the past year, USB has returned -17.72%.

Seeking Alpha

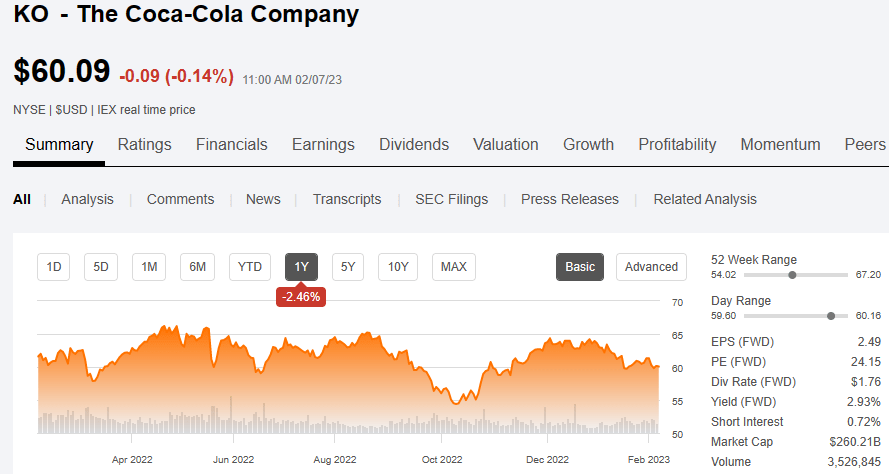

The Coca-Cola Company (KO)

Coca-Cola Co is a multinational beverage corporation with a total market cap of $260.21 billion. KO pays a dividend yield of 2.93% and has a Forward P/E of 24.15x with a 5-year Beta of 0.55. Over the past year, KO has returned -2.46%.

Seeking Alpha

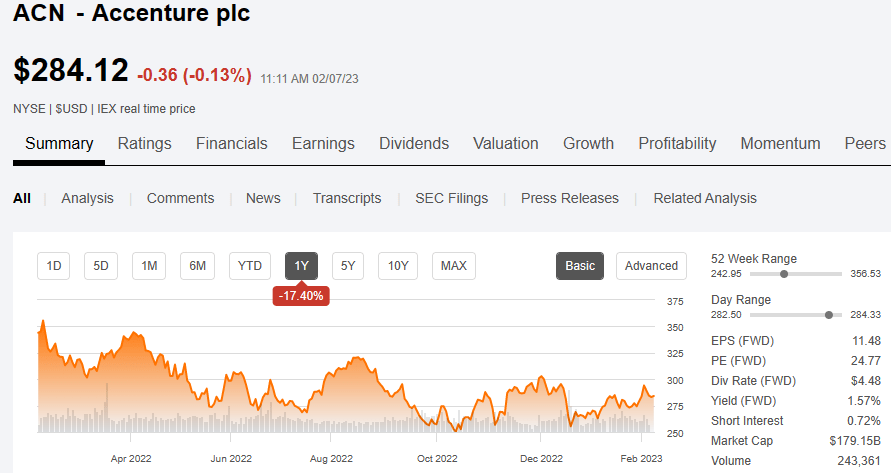

Accenture plc (ACN)

Accenture Plc is a professional services company specializing in IT services and consulting with a total market cap of $179.15 billion. ACN pays a dividend yield of 1.57% and has a Forward P/E of 24.77x with a 5-year Beta of 1.23. Over the past year, ACN has returned -17.40%.

Seeking Alpha

JEPI’s Cover Call Strategy

The first thing to note is that JEPI sells “out of the money” call options. This is an important point because it allows JEPI to catch some of the upside if the stock or index gains in price.

One of their closest competitors, Global X S&P 500 Covered Call ETF (XYLD) sells cover calls “at the money,” which provides a larger premium but limits the upside potential.

Along with their active stock selection, this is another way JEPI seeks to capture a portion of the total return of the S&P 500. By selling “out of the money” call options JEPI receives less premium / income but has more room to appreciate in a rising market.

JEPI

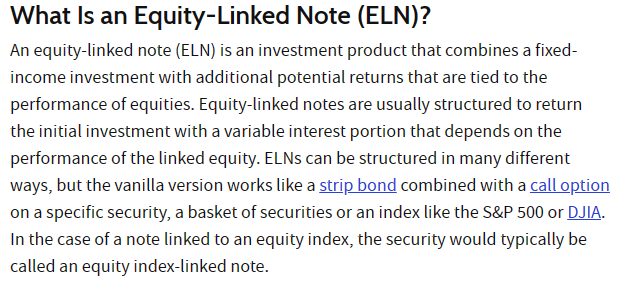

The second thing to note is that JEPI uses Equity-Linked Notes (“ELNs”) as a vehicle to sell cover calls. Equity-linked notes are a type of structured product that combines characteristics of a debt instrument with an underlying equity component, in this case covered calls.

ELNs and structured products in general can come in many different varieties. Unfortunately, JEPI does not disclose how their ELNs are designed since it is proprietary information.

An example of a generic ELN would be buying a zero-coupon bond for $800 with a face value of $1000 due at maturity. The extra $200 the borrower would normally pay at maturity is used instead to buy a basket of stocks or a single stock with a built-in covered call feature that is combined with the bond.

So, the lender gave up the interest payment in lieu of the basket of stocks with the built-in call feature. At maturity, the lender would receive their initial principle of $800 and possibly more depending on the performance of the underlying equity component. If the equity component does not perform well, the investor might have done better just to keep the interest and principle payment at maturity.

I want to stress that the generic example above does not reflect how JEPI structures its ELN’s. Because it is considered proprietary JP Morgan does not disclose how they structure their ELNs so we cannot know what all the moving pieces are.

Investopedia

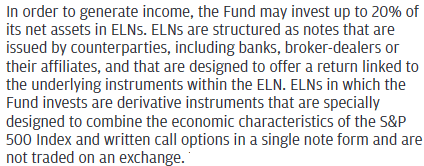

JEPI may invest up to 20% of the funds’ net assets in ELNs. Again, we don’t know how JP Morgan structures their ELNs, but typically the biggest risk involved in structured products is counterparty default, just like with a regular bond. If the bank(‘s’) issuing the ELN goes bankrupt, then JEPI’s performance would be significantly impacted.

JEPI – Summary Prospectus

From their latest annual report, we can see that JEPI has several ELNs listed in their top holdings as of June 2022. Although up to 20% of the funds’ net assets can be invested in ELNs, JEPI has the notes spread across several different counterparties which should mitigate the risk if a single bank were to fail.

JEPI – Annual Report

JEPI Stats & Performance

JEPI

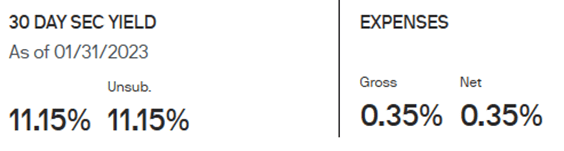

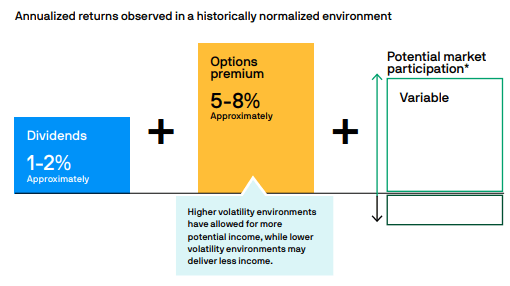

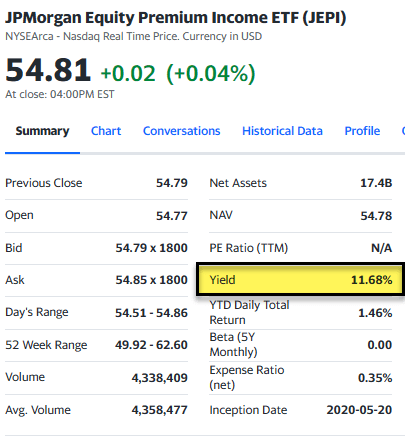

JEPI has a 30-day SEC yield of 11.15% as of 1/31/2023. On average JEPI expects to receive a 1 to 2% yield from dividends on their long positions and a 5 to 8% yield on the option premiums received. It’s important to note that JEPI’s distributions are variable, so one month’s payout will be different than another.

JEPI – Fund Story

JEPI has an expense ratio of 0.35% which is decent for an actively managed fund. As a point of reference, Vanguard S&P 500 ETF (VOO) which is passively managed, has an expense ratio of 0.03%, while Global X S&P 500 Covered Call ETF has an expense ratio of 0.60%.

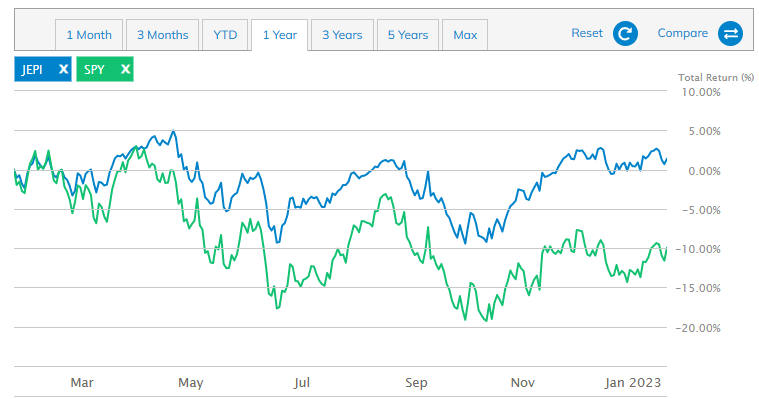

In terms of performance, JEPI did very well in 2022 compared to the broader market. Over the last year JEPI has had a total return of +1.39% (with dividends reinvested) vs. a decline of -9.95% for the S&P 500 (using SPY as a proxy).

It should be noted that, in a bull market, JEPI is likely to underperform the S&P 500 due to the call options employed that limit capital gains.

etf.com

JEPI Pros & Cons

Negative aspects

JEPI’s inception was in May 2020, which makes it a fairly new fund, so we don’t have a lot of history to go off of to gauge past performance. JEPI is also likely to underperform the broader market over the long term due to the limited capital gains it can participate in due to selling covered calls.

Another negative is that the distributions are variable so an investor won’t know how much they will receive month to month. In my opinion the largest negative is that it does not disclose how they structure their ELNs, so it’s not possible to fully know the risk profile involved in their option writing.

Positive aspects

Even though its yield is variable, JEPI pays a very high yield. Its expense ratio is reasonable for an actively managed fund, and its long holdings are well diversified. JEPI also has a very reputable sponsor in JP Morgan, which alleviates some of the concern on how they are structuring their ELNs.

JEPI is a good counterbalance for an income portfolio that is overweight on fixed income, MLPs, BDCs, and REITs.

It provides equity exposure while providing a high monthly income stream and is a good complement to other income producing asset classes. The biggest positive in my opinion is how well it performed in 2022. While most asset classes went down significantly in 2022, JEPI held its ground and outperformed many ETFs and the broader market as a whole.

Of course, as the title to my article suggests…

JEPI Is The Name, High Yield Is The Game

Yahoo Finance

Be the first to comment