guvendemir/E+ via Getty Images

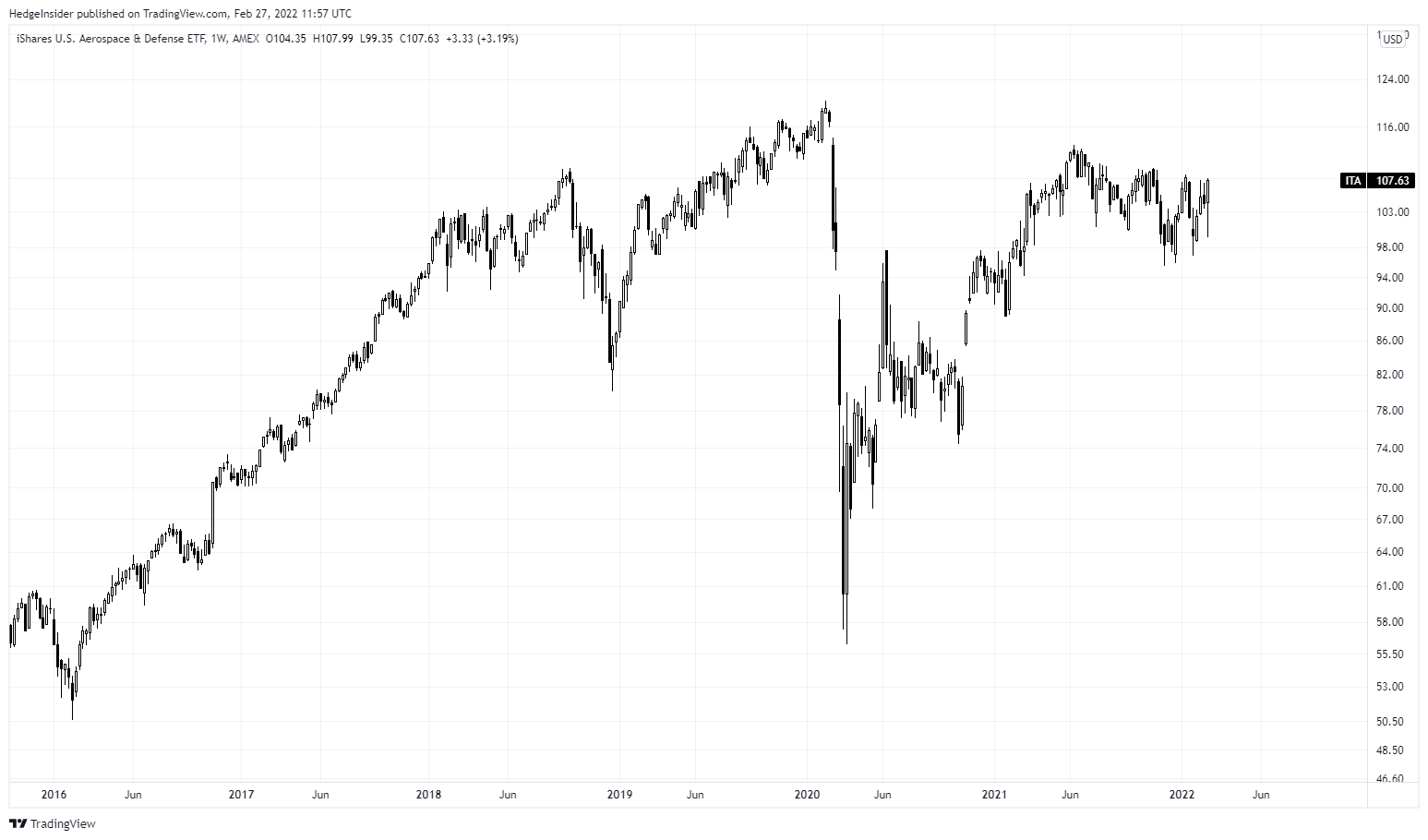

iShares U.S. Aerospace & Defense ETF (BATS:ITA) is an exchange-traded fund offering investors exposure to “U.S. companies that manufacture commercial and military aircrafts and other defense equipment”, with an expense ratio of 0.42% (not cheap, but in line with similar strategic equity funds). The fund’s benchmark index is the Dow Jones U.S. Select Aerospace & Defense Index, and had assets under management of $2.64 billion as of February 25, 2022, which reflects a fairly high level of popularity. The fund is also concentrated in just 33 holdings (as of February 24, 2022).

Interestingly, in spite of the Russo-Ukrainian War, which has notably escalated this month in February 2022 (with further Russian invasions from the north, east and south of Ukraine, in the latter case from Crimea, which was annexed by Russia in 2014), ITA has not even taken out its pre-pandemic highs.

TradingView.com

In fairness, the war in Ukraine is primarily a European war, and while NATO countries have been assisting Ukraine, a full-scale level of military support could trigger Article 5 of the NATO treaty. This is the key section of the treaty that essentially says that an attack on one NATO member is an attack on all, which would risk a “World War 3” scenario. Ukraine is not a NATO member. NATO does however include 30 countries, two of which include the United States and Canada in North America. The other 28 members are European.

Nevertheless, the recent tensions should support military spending and exports. Just recently, German Chancellor Olaf Scholz announced that German defense spending would be increased to 2% of GDP. With major powers like Russia invading large populations such as Ukraine (with a population of over 44 million as of 2020), a case can easily be made for increased defense spending and other provisions. That is, especially in Europe, but the entire global sector could find increased sales and “earnings surprises” in the years to come (hopefully mostly on the back of prudence and preparations, not on the back of actual wars).

In any event, funds like ITA that are directly invested in aerospace and defense might serve as a concentrated form of War-specific insurance within a portfolio. Stocks do tend to bounce back from wars, shrugging off conflicts in most cases. This is likely to be the case especially with the Russo-Ukrainian war, as it is local rather than worldwide (at least at present). But sanctions on Russia will almost certainly affect the West in other ways, such as via inflation due to reduced supply/flows of certain commodities (natural gas being one; a major export of Russia). So, it is conceivable that ITA might not out-perform while the entire market, including ITA, could still suffer from a stagflationary scenario of higher commodity prices and low/no “real growth”.

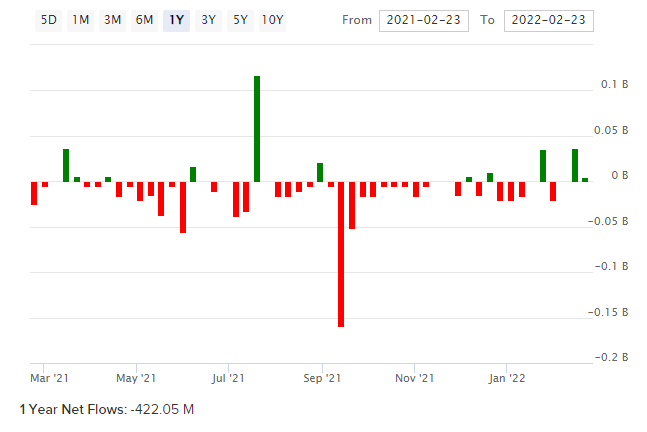

Bear in mind that the market has, so far at least (into late February 2022) not placed large bets on ITA. Recent net flows have been positive, but only after a net exit of funds from ITA over the past year (negative circa $422 million).

ETFDB.com

ITA still remains popular, as noted earlier, with assets under management of $2.64 billion. But this follows net outflows, so ITA is probably still somewhat of a contrarian bet. The trailing dividend yield at present is circa 80 basis points too, so ITA’s weak price action is good supporting evidence of the weak net fund flows as illustrated above.

Still, ITA could be defensive in more ways than one, with the U.S. probably entering into late-stage territory of its current business cycle. If/when economic growth slows down, it is likely that certain government spending such as on defense will remain more stable.

Fidelity.com

On the other hand, ITA is a risky hold. In March 2020 when stock prices crashed globally, ITA’s local peak-to-trough produced a decline of just over 50%, while major U.S. indices dropped by about a third. So, you could assume downside beta of circa 1.5x in a repeat scenario, while upside beta is evidently not as strong, since ITA still has not exceeded its pre-pandemic highs.

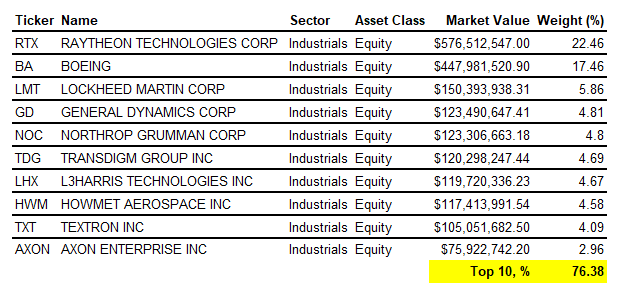

As mentioned earlier, ITA is also concentrated, with its top 10 holdings (as listed below) reflecting 76% of the portfolio as of February 24, 2022. The largest holding is Raytheon Technologies Corp (NYSE:RTX) with a weight of over 22%.

Data from iShares.com

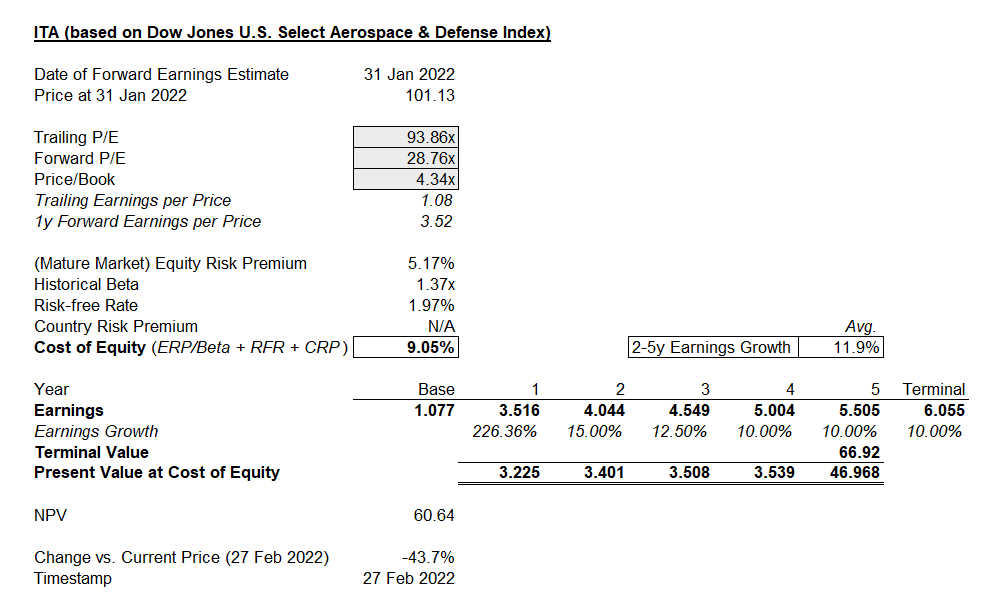

A recent factsheet (accessible online) for ITA’s benchmark index, whose performance it is essentially seeking to replicate, gives us data as of January 2022 month-end for valuation purposes. The trailing price/earnings ratio was poor, at 93.86x, which is unreflective of underlying earnings power in long term (absent disruptions to earnings due to significant factors such as the pandemic). The projected price/earnings ratio was 28.76x, with a price/book ratio of 4.34x. Dividing the latter into the former gives us a forward return on equity of 15.1%, which is decent for a mature sector. However, the price/book ratio is not inexpensive.

Current estimates from Morningstar for three- to five-year earnings growth, on normalized numbers, are for 11.72% earnings growth rates. Earnings estimates are subject to change although they tend not to change too materially. After the first year “bounce” (that is implied by virtue of the low trailing price/earnings ratio, which heavily distorts first-year earnings growth), I assume growth between year two and year five in my analysis in the region of Morningstar’s 12% directional estimate.

To discount those earnings, I use Professor Damodaran‘s current mature market equity risk premium estimate of 5.17%. For the risk-free rate, I am going to use the U.S. 10-year that currently prevails of 1.9652%. The five-year beta calculated by Yahoo! Finance is 1.37x, which I will start with; I use this to scale our ERP of 5.17% upward by 37%. However, as suggested earlier, this may understate downside beta and overstate upside beta, so we will return to this shortly.

The conclusion to all the above inputs is that ITA is likely overvalued if we assume a cost of equity of circa 9.05% (per my calculations).

Author’s Calculations

If we reduced beta to 1.00x, i.e., if we added no risk onto the equity risk premium, the valuation would still indicate downside potential of -27%. What’s more, if we scaled up our beta to at least 1.50x in line with possible elevated downside beta in a major drawdown scenario, ITA might offer downside potential (at present valuations) of as much as -48%.

On the other hand, long-term equity risk premiums often fall within the range of 3.2-4.5%. Damodaran’s recent ERP estimate of over 5% reflects risk aversion in Q1 2022. If I dropped the equity risk premium all the way down to 3.2%, but still scaled this up by 1.50x, has set the U.S. 10-year at 2.54% instead (in line with present 10-year inflation expectations), my adjusted cost of equity would be 7.34%. This would lend to downside, still, of circa -29%.

So, no matter which way you look at it, ITA is overvalued, and/or the market is more accurate in assessing the portfolio’s long-term earnings trajectory (being more optimistic than analyst estimates). Personally I would prefer not to buy into funds that fit some kind of geopolitical dynamic or theme (such as increased defense spending) at the expense of valuation. I would not be bearish though, as clearly a case can be made for increased military spending. On balance, I would remain neutral on ITA. I think meager fund flows over the past year are probably justified.

Be the first to comment