da-kuk

Let China sleep, for when she awakes, she will shake the world. – Napoleon.

Introduction

As pointed out in the “Leaders-Laggers” section of my subscription research, a ratio measuring the strength of emerging markets and U.S. stocks is at its highest point in 5 months. Given this ongoing momentum, some of you may be interested in looking at products in this space.

One of those products is the iShares MSCI China Small-Cap ETF (NYSEARCA:ECNS), an exchange-traded fund (“ETF”) that offers international investors access to small companies in China. Given their relatively low base, small caps in general are perceived to have a much more attractive growth runway compared to large caps, who also have to deal with a growing sense of saturation. For instance, according to YCharts, the portfolio of ECNS currently offers investors long-term earnings growth of ~12%, around 1.4x the level of earnings you could get from the large-cap-based iShares MSCI China ETF. Prima facie, ECNS is an attractive proposition, but there’s a lot more than one needs to consider before plunging into this product.

Chinese conditions

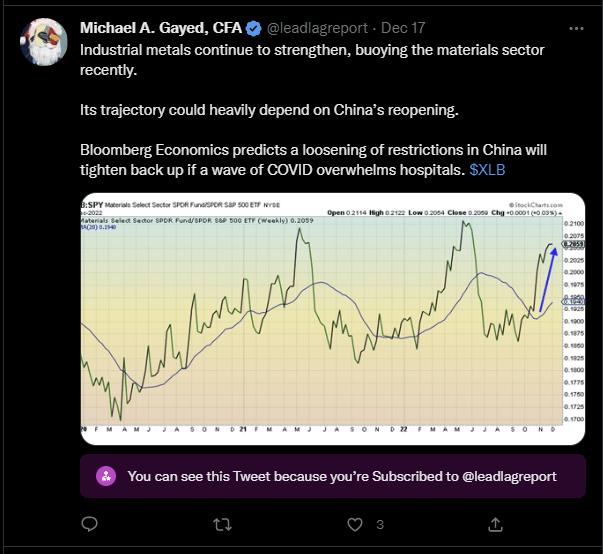

The big talking point in China centers around the loosening of its COVID restrictions, and a lot hinges on this. The ramifications are not restricted to just China alone; as noted in The Lead-Lag Report, the recent strength in industrial metals has been driven by China reneging on its long-standing zero-Covid policy.

Twitter

In fact, Gerald Celente, the founder of Trends Research Institute, was recently on Lead-Lag Live, and he spoke about how China was initially on course to become the number 1 economy in the world in just 7 years, but their “zero-Covid” approach has likely pushed this back by a few years.

Twitter

Nonetheless, as things stand, the Chinese government has decided to open the floodgates with its COVID management policies. This has certainly prompted a lot of analysts to reorient their estimates for the Chinese economy in 2023. Bloomberg Economist Chang Shu now believes that the country may well be free of all restrictions by the end of Q1.

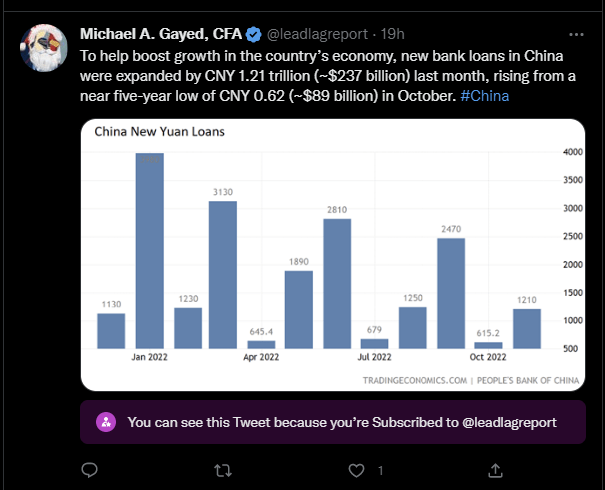

Supplementing the re-opening narrative, you also have some encouraging developments from the central economic work conference (CEWC) held last week, where the government looks set to put the consumer at the forefront of its economic agenda in 2023. One is likely to see initiatives like consumer vouchers and tax exemptions take on greater prominence as the government seeks to restimulate the economy. The property sector is another terrain that will likely receive greater support through expanded bank credit and bond financing. As noted recently in The Lead-Lag Report, new bank loans recently grew by nearly 3x month on month.

Twitter

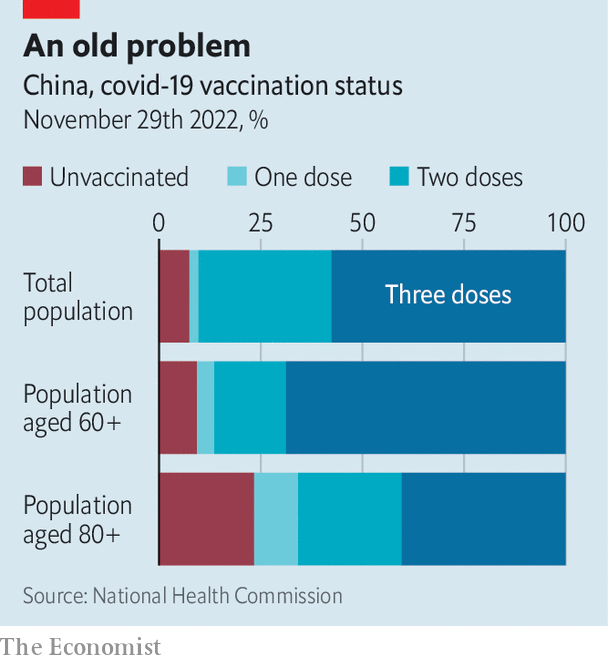

While all this is a step in the right direction, you have to wonder if China has the wherewithal and the infrastructure to cope with a spike in cases. As part of their base case, Bloomberg believes that in the first 6 months of reopening, China would admit close to 32000 patients a day in ICUs, but what if this spirals over? Note that the total ICU beds are only estimated to be around 48000. Besides, China’s low elderly vaccination rates only compound the risks.

The Economist

All in all, I suspect China’s reopening story is unlikely to be smooth sailing, and the authorities there may be prompted to dial back certain initiatives. If we see China shut down again, I worry about the prospects of these small-cap names cause their fortunes are closely tied to the export market. As discussed in the “Global” section of this week’s edition of The Lead-Lag Report, this would put off a lot of global companies who may likely seek to pivot away from China to regions such as India. For instance, Morgan Stanley believes that Apple has already been making plans to move some iPhone production away from China to India, with India expected to account for 5% of iPhone production volume by spring 2023.

Conclusion

Stockcharts.com

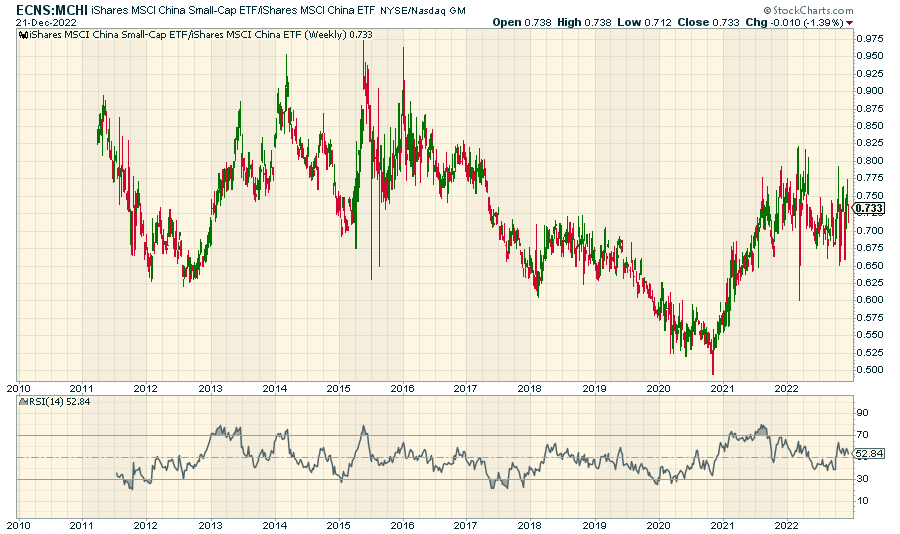

If you look at a relative strength chart measuring the performance of Chinese small-caps and the flagship iShares MSCI China ETF (MCHI), it’s fair to say that one isn’t likely to witness any significant edge by moving into either one of those products, as that ratio is at par levels. However, if one switches to the respective forward valuation comparison, that’s a different story altogether, with the equation tilting in favor of ECNS. ECNS currently only trades at 6.2x, forward P/E, 42% lower than the valuation multiple of MCHI.

Twitter

While the valuations of ECNS are tasty enough, investors may need to take a broader perspective and also consider risk dynamics in the financial markets, which could put small-cap and emerging market products in a dicey state. All of the inter-market risk signals of The Lead-Lag Report continue to signal risk-off, and I suspect the high-risk conditions witnessed over these recent weeks will likely carry into the new year.

Anticipate Crashes, Corrections and Bear Markets

Anticipate Crashes, Corrections and Bear Markets

Sometimes, you might not realize your biggest portfolio risks until it’s too late.

That’s why it’s important to pay attention to the right market data, analysis, and insights on a daily basis. Being a passive investor puts you at unnecessary risk. When you stay informed on key signals and indicators, you’ll take control of your financial future.

My award-winning market research gives you everything you need to know each day, so you can be ready to act when it matters most.

Click here to gain access and try the Lead-Lag Report FREE for 14 days.

Be the first to comment