Steve Jennings/Getty Images Entertainment

Coinbase (NASDAQ:COIN) is a controversial stock not only because it is powering cryptocurrencies, but also because of the high amount of earnings it is already generating. The company has earned so much from transaction fees that it generated $3.6 billion in net income in 2021, a staggering 46% net margin. The stock trades at less than 10x trailing net income, a curiously low multiple for a recently public tech stock, but bears counter that the transaction fee business model is antiquated in a commission-free world. While COIN may no doubt see great volatility in earnings over the next few years, I expect the company to play an important role as the underlying infrastructure for cryptocurrencies over the long term.

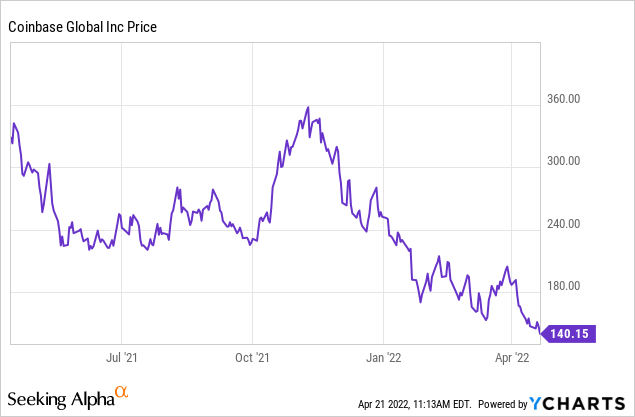

COIN Stock Price

Unlike many recent tech stocks which took advantage of rich valuations to raise money via an IPO, COIN came public via a direct listing in early 2021 and closed at $328.28 per share. The stock has since fallen by more than 50% to trade around $140 per share.

The current stock price sentiment appears overly pessimistic for what has been a true innovator and leader in the cryptocurrency space.

COIN Stock Key Metrics

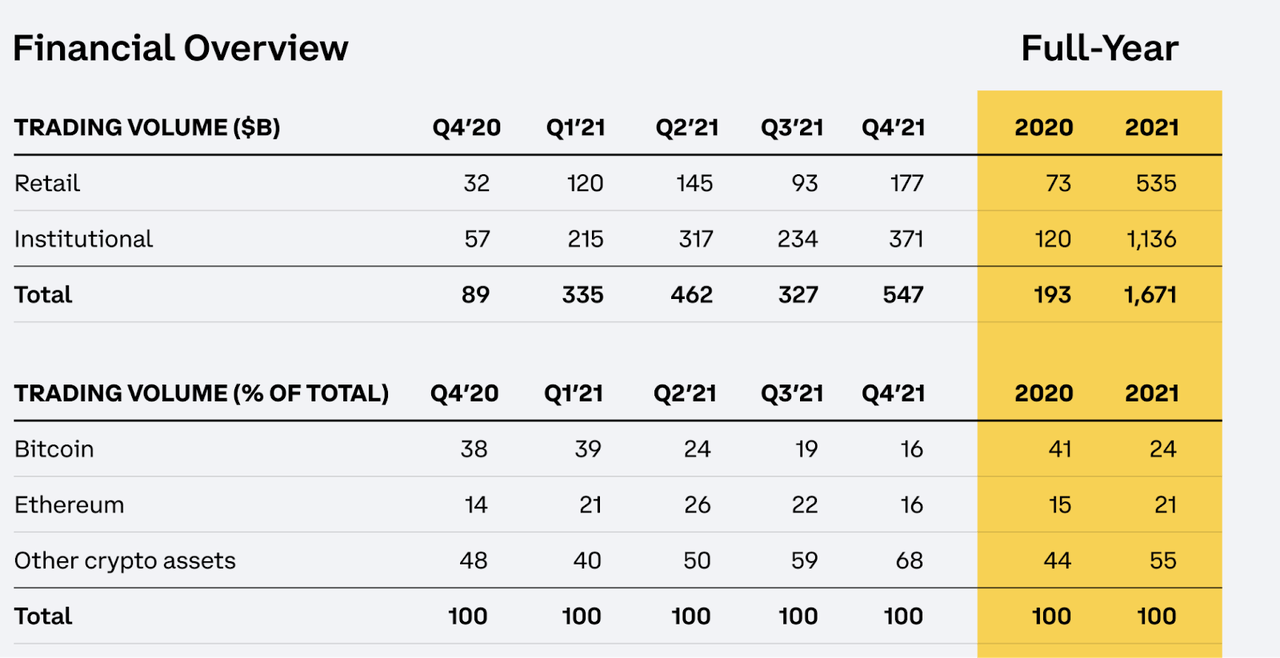

I suspect many investors focus primarily on trading volume, given that transaction revenue currently makes up the vast majority of overall revenue. COIN saw trading volume explode in 2021 versus 2020, with Bitcoin (BTC-USD) making up a lower percentage of overall volume.

Coinbase 2021 Q4 Shareholder Letter

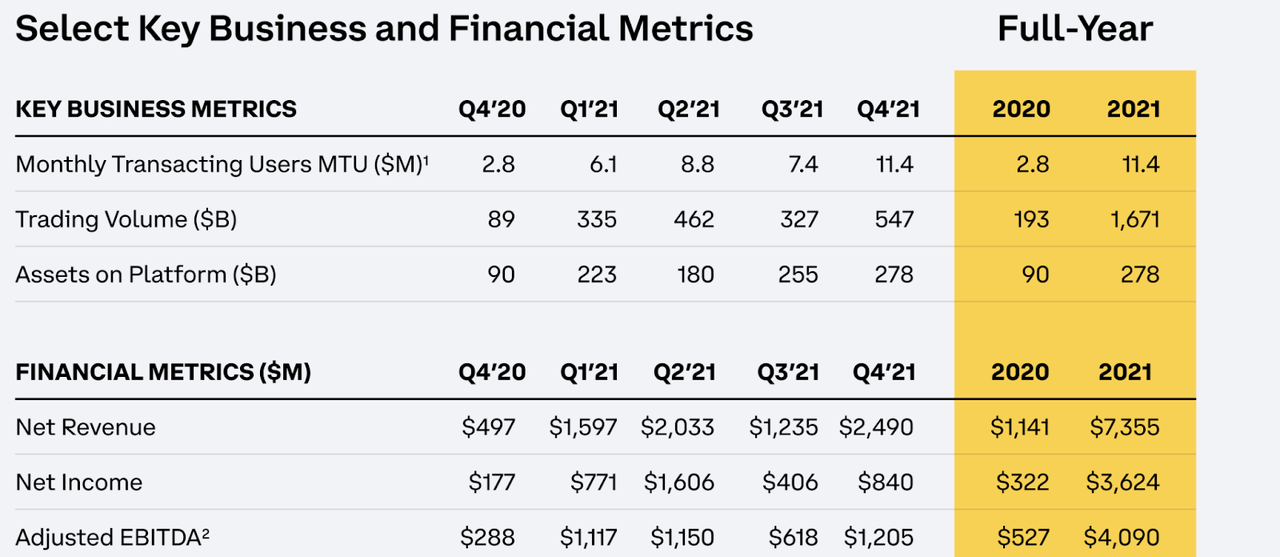

In the near term, trading volume is the main driver of earnings for the company. But in my view, the better metric to look at is the growth of monthly transacting users, which grew to 11.4 million in 2021. I note also that the company generated $3.6 billion of net income in the year. Perhaps that number will prove to be a peak as transaction revenues decline long-term, but the present-day cash flows can help the company build a strong balance sheet and invest for future growth.

Coinbase 2021 Q4 Shareholder Letter

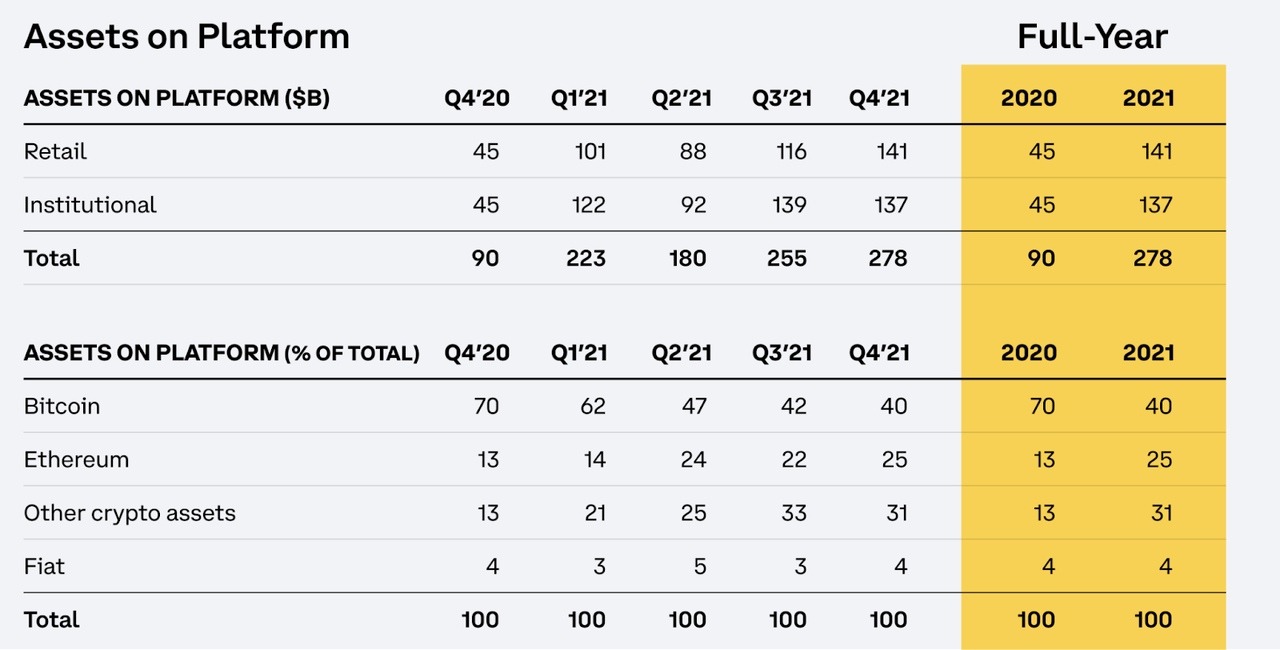

Assets on the platform have also grown robustly, though not as fast as users.

Coinbase 2021 Q4 Shareholder Letter

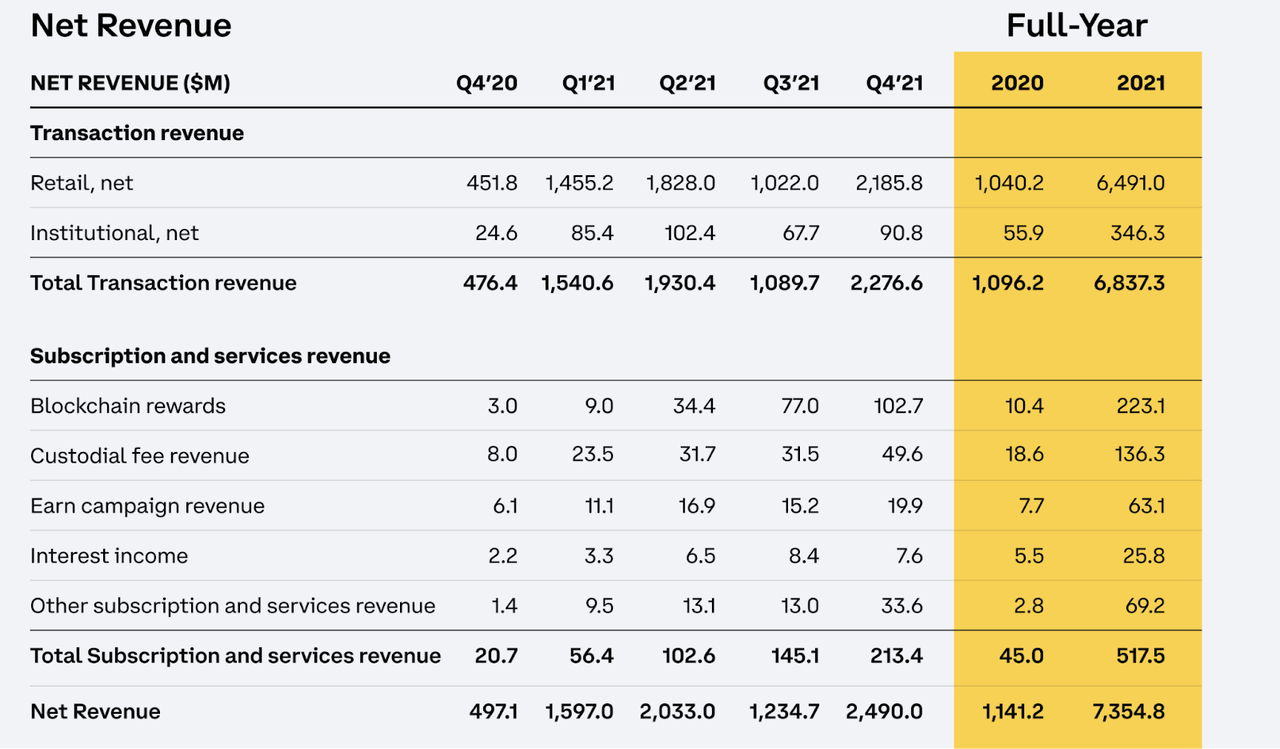

This makes sense because many of the new users are new to the space in general and aren’t immediately bringing in a lot of assets to the platform. Below we can see a breakdown of revenue.

Coinbase 2021 Q4 Shareholder Letter

COIN is rapidly growing its subscription and services revenue, which are less dependent on cryptocurrency volatility and trading volumes. Still, though, they represent only 7% of overall revenue.

COIN ended 2021 with $7.1 billion of cash versus $3.4 billion in long-term debt. The debt is made up of $1.44 billion of convertible notes due 2026 with a 0.5% interest rate and $478 per share conversion price (net of capped calls), $1 billion of 3.375% senior notes due 2028, and $1 billion of 3.625% senior notes due 2031. This looks like a strong balance sheet considering the $3.7 billion of net cash and low-yielding long-term debt. The company is generating cash flow and has stated that in the worst case, it should be able to manage its adjusted EBITDA loss to $500 million annually.

What Is The Future Of Coinbase Stock?

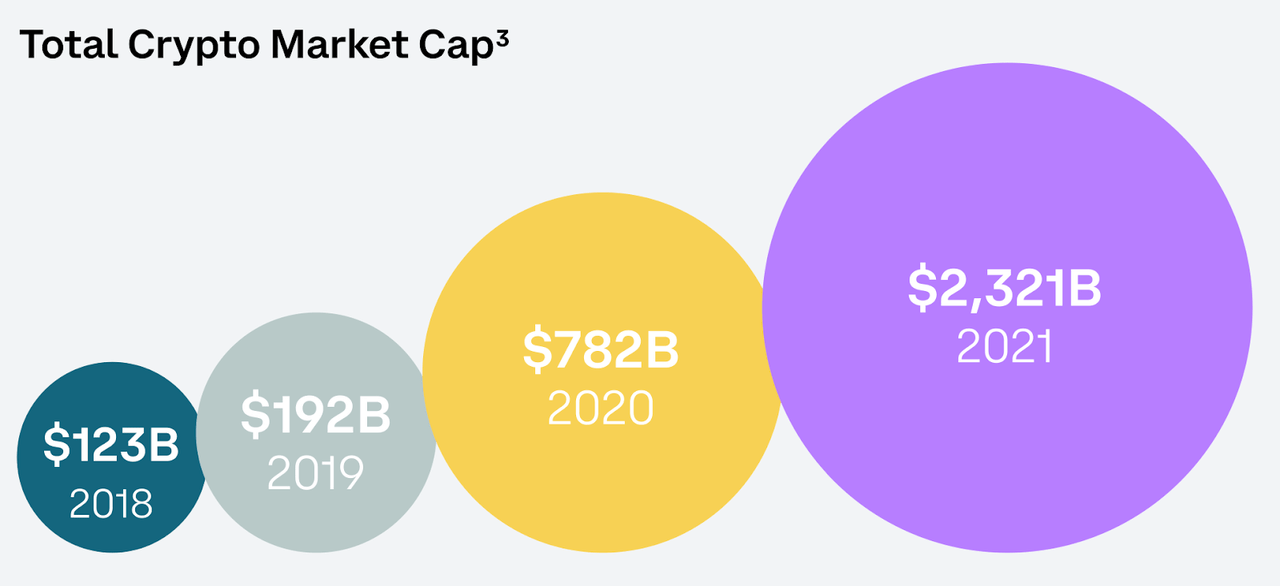

When thinking of Coinbase, it is tempting to just consider the long-term trajectory of cryptocurrencies. The total crypto market cap has grown rapidly over just the past several years.

Coinbase 2021 Q4 Shareholder Letter

I do not personally invest in cryptocurrencies. My personal view is that cryptocurrency investment is very similar to investment in gold and other similar assets. I am doubtful that Bitcoin or Ethereum (ETH-USD) or other cryptocurrencies will ever be used as real currency, but I still expect assets to flow into the sector in a similar fashion as how assets flowed into gold in the past. Many investors want diversification across asset classes, and cryptocurrencies offer an easy way to accomplish that.

Is COIN Stock A Fair Valuation?

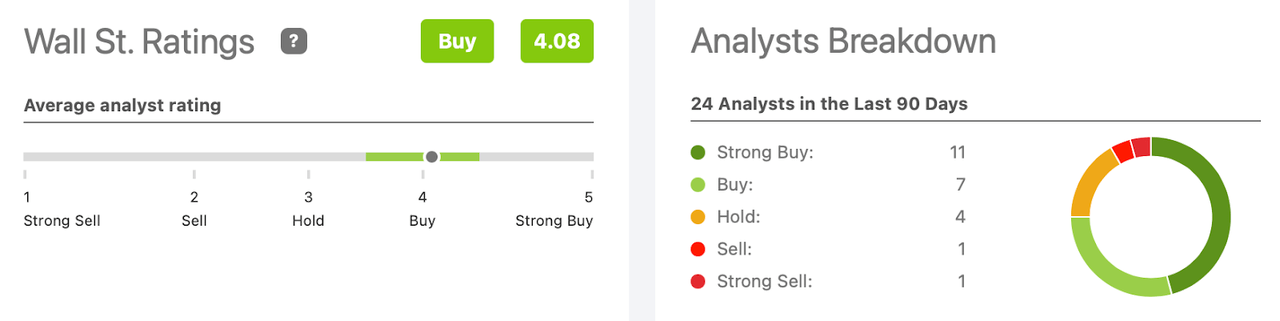

Wall Street analysts have a 4.08 average rating for the stock, though there are a couple of sell ratings among the 24 analysts covering the stock.

Seeking Alpha

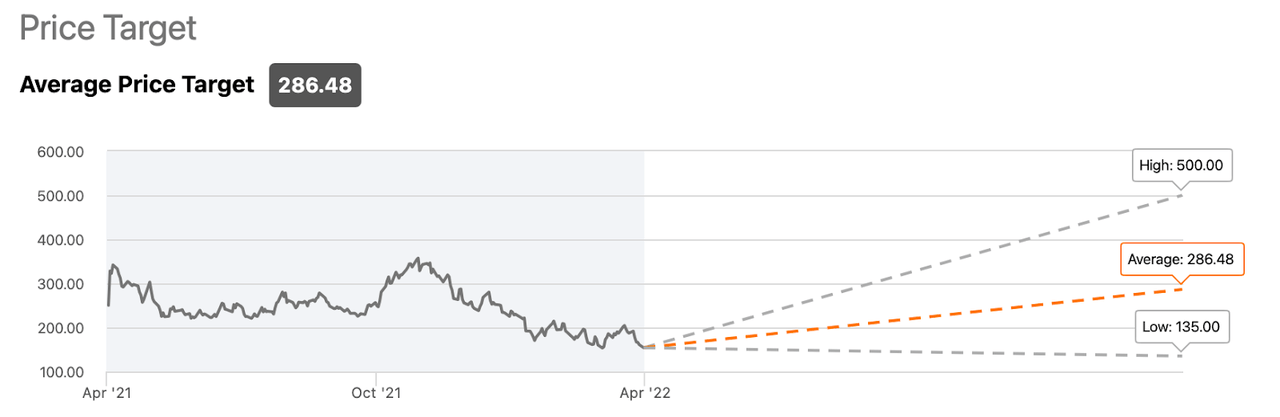

The average price target of $286.48 per share represents over 100% potential upside.

Seeking Alpha

Is Coinbase Stock A Good Long-Term Investment?

Long-term, Wall Street seems convinced that COIN’s current financials are too heavily reliant on transaction fees. With equity transaction fees completely free at many stock brokerages, it isn’t a contrarian view to believe cryptocurrency trading fees will also head in that direction. That kind of view makes one skeptical of the high net income and revenue currently generated by the company.

Even if one maintains a bullish long-term view of cryptocurrencies which should support long-term trading volume, there still remains the issue of what happens as transaction fees head toward zero. Wall Street is not giving the company credit for its achievements until now. COIN has emerged as the largest cryptocurrency wallet, which it has earned through name brand recognition and ongoing innovation. The company is investing heavily in improving its offerings including its pending NFT market. While there are no direct cryptocurrency ETFs as of the present day, I wouldn’t be surprised if COIN eventually creates a very successful ETF offering in the future (when regulatory conditions permit), which should be a consistent source of fee income.

Is COIN Stock A Buy, Sell, Or Hold?

Wall Street consensus estimates call for earnings to decline 74% in 2022.

Seeking Alpha

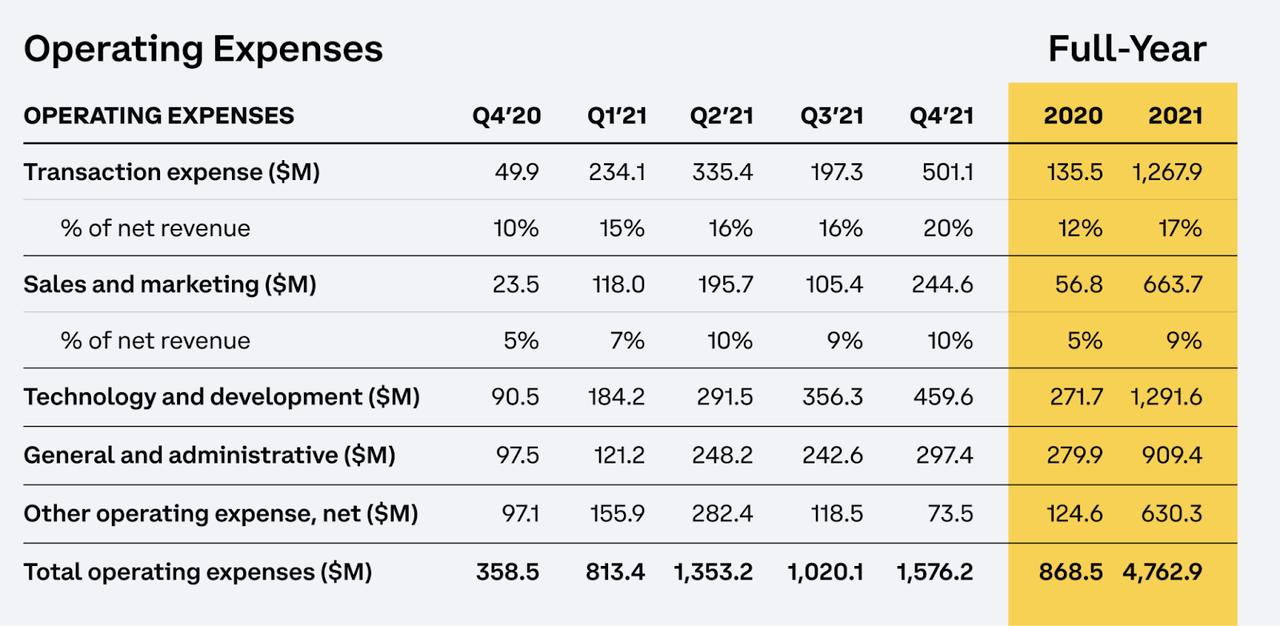

The stock still trades at 35x that earnings estimate, but let’s discuss why earnings are expected to fall so rapidly. We can see the operating expense structure for 2021 below:

Coinbase 2021 Q4 Shareholder Letter

COIN has guided for transaction expenses to tick up to around 20% of net revenue, sales and marketing expenses to tick up to 15% of net revenue, and technology and development & general and administrative expenses to tick up to $5.25 billion (with $1.5 billion being share-based compensation). Based on 2021 numbers, that would suggest expense growth of around $3.8 billion. That’s enough to completely wipe out GAAP net income, especially considering that revenue is not expected to grow in 2022:

Seeking Alpha

It looks like Wall Street expects the company to derive operating leverage elsewhere and still generate robust cash flows. I wouldn’t be surprised if COIN ends up underperforming earnings estimates, as the company appears to be more focused on investing for future growth rather than minting cash right now. That might prove to be a future headwind, though, with the stock trading at only 4.6x 2022e sales, the stock is cheap even if we assume the company is not currently profitable. COIN expects to increase its headcount from 3,730 at the end of 2021 by another 6,000 employees in 2022. This is a company that is aggressively investing in growth.

I expect both revenue and earnings to remain volatile as the company moves towards a zero-commission fee model. It will take time to offset transaction fees with subscription fees, though the ongoing strength in user gains suggests that transaction fees may not decline too rapidly. Even if we assume that the company will generate a conservative 30% net margin over the long term, the stock is trading at only 15x long-term earnings power. As it becomes clear that cryptocurrencies are a secular growth story, I could see COIN trading up to a 9x to 12x sales multiple, representing a stock price of between $305 to $400. That would represent a price-to-earnings growth ratio (‘PEG ratio’) of between 1.5x and 2x (assuming 20% revenue growth).

There are important risks to consider. It is possible that cryptocurrencies end up losing relevance. If the cryptocurrency market does not continue to grow, then I would expect COIN to struggle to achieve solid growth. Yet just as gold has remained a popular investment over the centuries, I expect cryptocurrencies to only grow in relevance. I expect both the fundamentals and stock price to experience great volatility, as the transition away from a transaction fee business model will not be smooth. Yet with the strong balance sheet and market position, the company is on a solid financial footing so that it should be able to weather any multi-year storm. On a final note, we can see below that there is high insider ownership in the stock. CEO Brian Armstrong owns around 39 million shares (he has since only sold 750,000 shares):

Coinbase S-1

With COIN, shareholders are investing alongside management with a lot of skin in the game. While that is no guarantee of strong forward returns, it is easy to understand how management will be much more incentivized to drive strong returns when they own so much of the company stock. COIN seems like a rare opportunity to invest alongside true innovators at a more than reasonable price. That kind of opportunity seems plentiful nowadays amidst the tech crash. Due to the cheap current valuation, strong balance sheet, and promising long-term opportunity, I rate the stock a strong buy.

Be the first to comment