David Becker

As Alibaba (NYSE:BABA) has returned 30% year to date, I aim to explain in this article how the fundamentals of Alibaba have changed and whether valuations for Alibaba still offer an attractive risk/reward opportunity for investors going forward.

Investment thesis

My core investment thesis for Alibaba remains the same. The only change has been the progress the company has made since my last article and the changes in the regulatory and political landscape as well as the change in the Covid-19 policy stance in China. I think that Alibaba looks attractive on a risk/reward perspective despite having generated 30% returns in 2023 year to date as it has come from a low base and valuations still remain cheap. My core investment thesis for Alibaba is elaborated below.

Firstly. Alibaba is one of the key beneficiaries of China’s economy opening up as Covid restrictions are removed. On top of that, the China eCommerce business has a low base in 2022, which will lead to a stronger growth in 2023.

Secondly, the company has progressed well with its cost optimization efforts. There are visible effects seen on the bottom-line, generating beats for the company in the past few quarters. In particular, we are seeing more of Alibaba’s newer and faster-growing initiatives narrow their losses. I think the effects of the cost optimization efforts will continue in 2023.

Thirdly and lastly, the cloud computing segment continues to improve and lead the industry, and I expect greater momentum in 2023 as China reopens and the Chinese economy improves.

I have written other articles on Alibaba which can be found here. I also provide weekly updates on Alibaba on Outperforming the Market as it is part of The Barbell Portfolio.

Core commerce fundamentals improving

Upside from the Lunar New Year

The Lunar New Year is the biggest event in the Chinese calendar and with China’s shift away from its strict zero Covid policy, this brings an opportunity for Alibaba’s core commerce segment. According to Sina News, the national online retail sales for the first five days of this year’s 2023 national online New Year’s shopping festival reached Rmb208 billion. This was up 5% from the same period in the year prior. Categories that showed strong growth were the sales of imported fresh food, health supplements and gift boxes for the new year. In particular, it was stated that growth was particularly strong for new consumption models like live streaming and on-demand delivery.

For the 2023 Taobao and Tmall New Year shopping festival, it was reported by Ebrun that there were straight price reductions of 5% to 15% as part of the promotional activities on these platforms and that consumers on Taobao and Tmall did not need to obtain a certain level of spending before they could get these attractive promotions. This means that Alibaba’s core commerce segment is likely to beat on volume rather than on GMV as this would prioritize checkouts of any size rather than larger basket sized checkouts.

Tmall also reported that they saw an interesting trend for its fresh category this year. There was a consumption upgrading trend in the fresh category and Tmall also said that there was a higher demand for high-end food products this new year.

Improvement in supply of pandemic products

On the other hand, as a result of a shift in its Covid policy stance, the supply for pandemic related goods has recovered on Taobao and Tmall. This includes things like Covid-19 self-test kits, N95 masks and drugs for fever.

Hema turns profitable

Lastly, Freshippo’s grocery brand, Hema Xiansheng, reported its first profitable year in 2022. Freshippo was founded seven years ago, and it sells vegetables, seafood, dairy, and meat to consumers both online and in-store. It operates more than 300 Hema Xiansheng stores and nine Hema X membership stores in China.

Freshippo CEO Mr. Hou also stated that the company aims to serve more than one billion consumers and reach Rmb1 trillion ($145 billion) in sales between 2023 and 2033.

International commerce gaining traction

Capital injection into Lazada from Alibaba

It was reported that Lazada received capital infusion from Alibaba of $343 million in December 2022.

As a result of this additional investment, Alibaba has made a total of $1.6 billion investments into Alibaba since 2022.

In May 2022, Alibaba also injected $378 million in Lazada and in August of 2022, Alibaba injected another $913 million.

I think that these capital injections are part of a broader support from Alibaba Group into Lazada and its Southeast Asia operations.

Lazada Philippines had a successful 12.12 campaign

Lazada Philippines CEO Mr Carlos reported that the 2022 12.12 Grand Pamasko Sale was a big success. How was it a big success?

There was a 44x increase in gift cards compared to a normal day, resulting in gift cards being the best-selling product during this sale period.

There was a huge demand for the trendiest and most authentic makeup products like the Maybelline Superstay 24H Full Coverage Liquid Foundation, and skincare products were also highly sought after, with the Fairy Skin Sunscreen being sold out within the first 12 minutes of 12.12.

Consumers on Lazada also stocked up on holiday kitchen essentials like cheese, beverages and there was a 17x increase in new buyers for groceries during the first day of the sale.

There was also traction in the apparel and accessories category, as “Sandals for Women” was the most searched item for 12.12, followed by Gingham tops, summer shorts, and Korean accessories.

Most importantly, Lazada Logistics resulted in quick and reliable shipping as consumers in Metro Manila could receive items on the same day the order was placed. Even consumers in Cebu and Davao could get their items the next day after placing their order for the fastest shipped items.

Lazada Singapore partners with SingPost for deliveries

Lazada Singapore signed an agreement with SingPost late in 2022 where a new automated self-service drop-off box developed by SingPost called POPDrop box will enable customers of Lazada to return items easily and in a more sustainable manner.

There will be end-to-end tracking capabilities enabled through RFID and barcode scanners. While there is only one such box available in Singapore today, the two parties expect to install more boxes in 2023.

I think that this represents a long-term partnership with SingPost and will allow Lazada to tap into SingPost’s logistics infrastructure, including the use of newly announced POPDrop boxes, the existing POPStations and its fleet of delivery vehicles.

Cloud computing

Organization change at Alibaba Cloud Intelligence

There were material changes in management of Alibaba Cloud Intelligence and also at the Alibaba Group level.

In an internal letter, it was announced that Mr. Jianfeng Zhang will no longer serve as President of Alibaba Cloud Intelligence. Mr. Daniel Zhang will take over for Jianfeng Zhang as President of Alibaba Cloud Intelligence and he will directly manage DingTalk. Mr. Jingren Zhou will serve as the CTO of Alibaba Cloud Intelligence and will continue to serve his current role as Vice President of Damo Academy.

In addition to organizational change in Alibaba Cloud Intelligence, there were managerial changes in Alibaba Group, where Mr. Zeming Wu will now serve as Group CTO while Ms. Jane Jiang will serve as Group Chief People Officer (CPO).

Daniel Zhang emphasized that the keyword for 2023 is progress and that the organizational change is the first step for Alibaba’s progress in 2023. I think that this change in managerial positions will bring new and innovative operational strategies that will drive the long-term success of the company as they try to explore new growth engines.

AliCloud continues to be in the Gartner leaders magic quadrant for cloud database management system for third consecutive year

AliCloud is once again regarded as a leader in the magic quadrant for cloud database management systems by Gartner for the third consecutive year. AliCloud is also the only Chinese player entering the leaders magic quadrant which is evaluated by 15 major KPIs.

Alibaba Cloud states that it was ranked number one in the database market in China. Apart from its leadership in the domestic market, Alibaba Cloud has also expanded globally, to foreign markets like Southeast Asia.

AliCloud is the leader in the finance cloud market in China

According to IDC, Alibaba Cloud was the number one player in China’s finance cloud market in the first half of 2022, with the market share expanding slightly to 19%. AliCloud was also the number one player in several other sub-categories like the finance cloud infrastructure sub-category with 22% market share, public cloud infrastructure with 43% market share and finance cloud solutions at 14% market share.

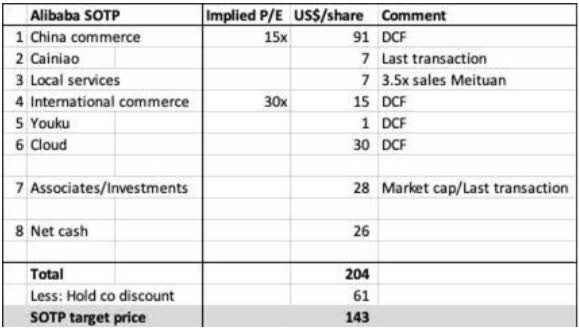

Valuation

To derive a valuation for Alibaba, I use a sum of the parts valuation model. Each part of Alibaba’s business is valued accordingly:

- For the China eCommerce segment, I have the view that we will see the segment return to growth on the back of relaxation of Covid restrictions in China, which has been my base case for the segment. As a result, this upside has been taken into account for my forecast for 2023.

- Second, for Local Services, Cainiao and other investments and associates held by the company, these segments are valued based on their latest transaction values and market capitalizations of the respective companies.

- Lastly, for Youku, International Commerce and Cloud, I value these segments using DCF, taking into account the long-term growth opportunities for the International Commerce segment and the robust growth opportunities for the Cloud segment.

When I put all these together and after applying a 30% holding discount, my SOTP target price for Alibaba is $143, implying around 31% upside from current levels.

Alibaba SOTP valuation (Author generated)

Risks

Competitive pressures

While Alibaba has strong leadership positions in the Chinese e-commerce and cloud computing market, it remains in a position of being the disrupted. There are many other players in the Chinese e-commerce space like JD.com (JD) and Pinduoduo (PDD) that compete with Alibaba for market share. In addition, Alibaba’s efforts in the international e-commerce space is met by strong competition from established international e-commerce players like Amazon (AMZN) and Sea Limited’s (SE) Shopee.

Regulatory and political risks

While the recent news about Alibaba seems to imply that the worst looks to be over for its regulatory headwinds given reports that Alibaba’s founder Jack Ma has come out of hiding and has been found in Tokyo and Thailand, there are still risks for Alibaba if Beijing or Xi Jinping wishes to make it more difficult for Alibaba to do business.

Cloud risks

There is the risk that Alibaba’s leadership in the cloud computing segment may be threatened. As Alibaba is looking to bring in more business from the non-Internet sectors as demand from the Internet sectors remain weak, there is a risk that other cloud computing players in the market may take advantage of the dislocation in the market. There are other established cloud players like Tencent (OTCPK:TCEHY), Huawei and China Telecom.

Conclusion

Even after the 30% returns generated in 2023 so far, as evident from the improving fundamentals of Alibaba as well as the relatively depressed valuations the company continues to trade at, I think that the risk/reward perspective for Alibaba remains attractive. As elaborated above, the core commerce segment’s fundamentals are improving and benefitting from the removal of Covid-19 restrictions in China. The international commerce segment remains to be a structural long-term growth driver for Alibaba as they continue to invest in Lazada. Lastly, the cloud computing segment of Alibaba continues to take the top spot in the industry in China as Alibaba grapples with regulatory, political and business headwinds. My SOTP target price for Alibaba is $143, implying around 31% upside from current levels.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment