Don White/E+ via Getty Images

Originally posted on May 12, 2022

By Seema Shah, Chief Global Strategist

Inflation is the single biggest challenge that investors face today. The sudden and sustained jump in prices has inflicted a considerable shock to the economic system, sharply pushing up interest rates, while challenging corporations and equity markets. For individuals, inflation quietly erodes the purchasing power of savings and cash – a significant problem, regardless of time horizon. For institutional investors, higher-than-expected inflation reduces real returns and makes it difficult to generate long-term forecasts to meet objectives. In all cases, however, inflation – and the threat of persistent inflation that’s higher than expected – is a reason to reconsider the traditional asset allocations that only address market environments of the past.

Inflation has reached four-decade highs

Many factors have driven inflation over the past two years, with the industry spilling plenty of ink over the topic. In short, the rapid economic recovery from the pandemic, surging consumer demand, excessive government stimulus and ongoing supply chain disruptions have caught many economists off-guard. More recently, geopolitics have played an important role: the Russian invasion of Ukraine has pushed food and energy prices higher, directly affecting consumer pocketbooks.

To make matters worse, after falling desperately behind the inflation curve, the United States Federal Reserve (Fed) has finally recognized the urgent need to tighten policy.

Recall that after the Global Financial Crisis, stubbornly low inflation meant that the Fed’s dual mandate of price stability and maximum employment was effectively a single mandate. The Fed could focus on keeping employment high without worrying about an overheating economy – and they extended this approach even after the pandemic, with rates staying near zero and monetary stimulus ballooning the Fed’s balance sheet to $9 trillion. This erroneously patient approach has permitted price pressures to multiply, broaden, and intensify unhindered, pushing inflation up to a 40-year high.

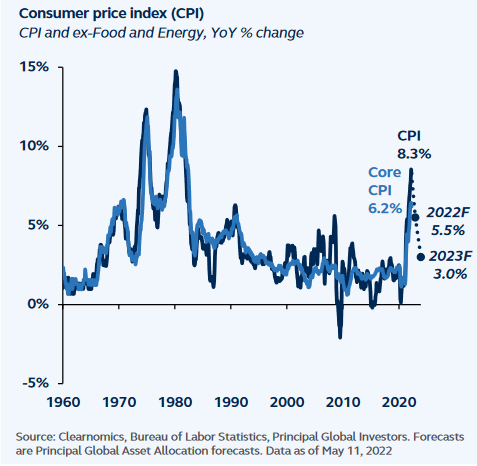

Customer Price Index (Core And Ex-Food And Energy)

Although inflation may have recently peaked, it is unlikely to subside rapidly. If higher prices, which have now broadened, are allowed to persist, they can become sticky. As experienced during the 1970s and early 1980s, a wage- price spiral, where rising wages beget rising prices, which cause further pressure on wages, certainly could allow inflation to be a challenge for longer than expected.

Perhaps the silver lining is that the economy is still fundamentally strong despite these challenges. After all, inflation is a problem created partially by robust consumer and business demand. Yet, while a Volcker-era wage-price spiral isn’t the base case, the economy can only stay strong for so long in the face of declining household purchasing power and rising interest rates. So, while the economy is on decent footing today, the risk of recession is likely to increase meaningfully in late 2023 and into early 2024.

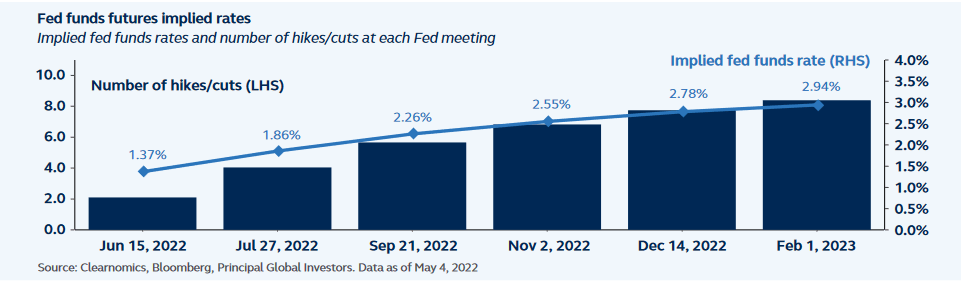

Fed Funds Futures Implied Rates

Traditional assets solve yesterday’s problems

The first real inflation shock in four decades means that many portfolios may not be properly positioned. In general, traditional asset classes aren’t ideally suited for high or rapidly rising inflation scenarios. This is especially true as interest rates increase in response.

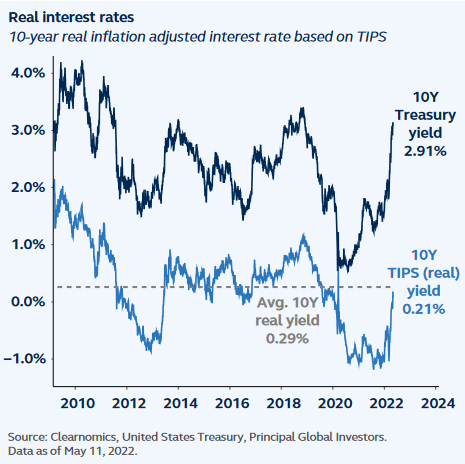

Already in 2022, the 10-year U.S. Treasury yield crossed the 3% threshold, a sharp increase from 1.5% at the start of the year and 0.9% at the start of 2021. With the Fed beginning to raise policy rates aggressively and quantitative tightening now underway, there are reasons to believe that rates will remain elevated, with bond yields ending the year around 2.5%.

Real Interest Rates

Today’s environment creates the perfect storm against fixed income. Bonds, by definition, are susceptible to rapidly rising nominal rates. The devastating combination of red-hot inflation and easy monetary policy has meant that real yields have been negative. Now, with policy rates moving sharply higher and inflation pressures receding very gradually, bonds will not only be susceptible to rising nominal yields but also to real yields moving back into positive territory.

As a result, the bond market has faced its toughest period since 1980, with the Bloomberg U.S. Aggregate Index declining 9.5% year-to-date.1 (For reference, in early 1994, after the Fed surprised the market with rate hikes, the bond market had a 6.6% peak-to-trough decline.)

Equities haven’t been immune to the ravages of inflation either. The S&P 500 has dropped over 15% year-to-date as investors have realized that high inflation can be problematic for the asset class. While stocks can perform well when inflation is moderate and rising steadily, since companies with pricing power can often pass on higher costs to their customers, pricing power has its limits.

Higher prices will eventually dampen consumer and business spending while also raising costs. Profit margins will be under increasing pressure this year, weighing on earnings growth. For financial markets, higher discount rates reduce the value of future cash flows today, depressing asset prices.

Thus, after decades of dormant inflation and falling interest rates, investors now need better ways to diversify portfolios and to enhance real returns. In today’s environment, this may require looking beyond the public market stocks and bonds that have been the main portfolio building blocks over the last 40 years.

Enter real assets

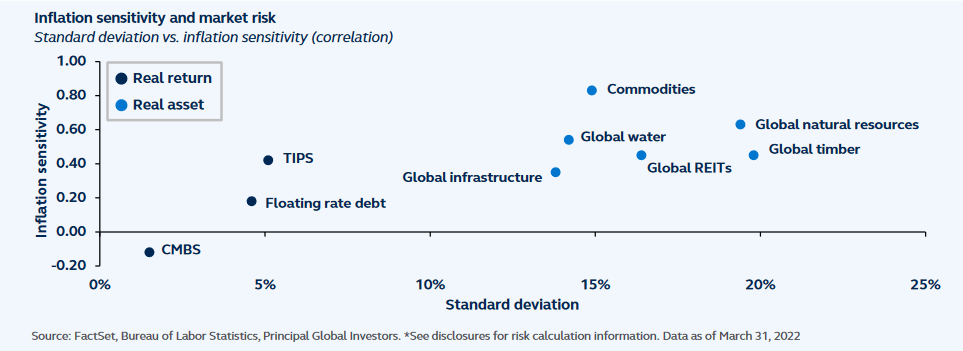

Fortunately, real assets are tailor-made solutions to these challenges, offering inflation risk mitigation as well as providing broad diversification benefits across market environments. The diverse set of asset classes that include real estate, agriculture, infrastructure, energy, commodities, natural resources, and timber – collectively, real assets – are securities whose underlying value is tied to a tangible asset or linked (inherently or contractually, implicitly or explicitly) to the rate of inflation.

When combined with the low correlations to traditional asset classes, the attractive real yields and often lower risk profiles of real assets mean that the asset class may enhance portfolio risk-adjusted returns. This is especially important if inflation is stickier and more stubborn than expected due to supply chains, consumer demand, and rising expectations, as investors are experiencing today.

Infrastructure investments are one of these attractive real assets that can outperform in the current environment. As demand for critical services is less sensitive to inflation, owners of certain infrastructure assets can sustain and increase prices without significantly impacting demand, offering important opportunity for inflation protection.

Furthermore, they typically have predictable cash flows associated with the long-lived assets and offer exposure to the global theme of decarbonization, which presents a multi-decade tailwind for utilities and renewable infrastructure companies.

In fact, certain regulated utilities even have a direct pass-through of inflation, making their revenue streams very attractive in today’s market. Certain user-pay assets, such as toll roads, have a similar sensitivity, whereby their prices are automatically adjusted for inflation.

Inflation Sensitivity And Market Risk

Real assets can also provide opportunities to access attractive investment themes beyond inflation mitigation. One of these themes is the possibility that the global economy is entering into a new commodities supercycle – an extended period of strong demand for commodities that’s distinct from the business cycle.

These periods create strong demand for commodities and natural resources, ranging from industrial metals to energy, since these are necessary inputs to economic growth.

While supply can grow, it often takes time to come on-line, thus driving prices higher in the meantime. Today, rapid growth in areas such as renewable energy, data centers, and consumer technology, alongside a robust economy and government stimulus, are driving the demand for commodities.

Many commodities also have natural supply limits, at least in the medium term. So-called rare earth metals, for instance, are necessary for a wide range of technology devices, including batteries, cellphones, and electric vehicles. While they’re not actually that rare, extracting and processing is difficult, geographically concentrated, and takes time to ramp up. Today, China is still the main supplier of rare earth metals, although there are efforts to boost production in the U.S. and elsewhere. This limited market supply means that strong demand could continue to drive up prices.

Whether there is a new commodities supercycle or not, the post-pandemic recovery and the war in Ukraine have already crimped the supply of energy, grains, timber, and other natural resources in the near term. Many commodities have remained in deep backwardation since mid-year 2021 – usually a signal of supply shortage concerns. These concerns look legitimate in today’s environment, as demand has strongly outpaced supply due to limited capital expenditure from major commodities producers. Additionally, given the unpredictability of geopolitical events, investors should prepare to be whipsawed in this environment. Diverting supply chains, or even substituting from alternative countries, is wrought with difficulties and delays. Therefore, even pockets of commodity shortages will likely result in prolonged price pressures.

The upshot is that commodity prices could remain elevated for the next year or so, until the next economic downturn naturally reduces demand. Thus, including commodities and natural resources in a portfolio may help to offset the inflationary pressures faced by other asset classes.

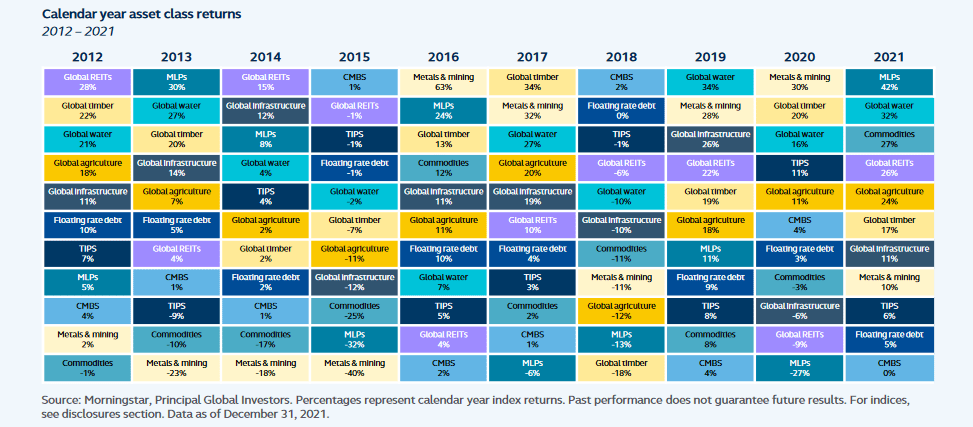

Calendar Year Asset Class Returns 2012-2021

Navigating the perfect storm with real assets

With the Fed so desperately behind the inflation curve, policymakers have finally recognized the urgent need to tighten policy. But having left it to so late, an aggressive hiking cycle is now required to bring inflation back to target, risking a sharp economic downturn in the process. Recession risk for 2022 is still muted given the strength of the consumer and corporate balance sheets, but risks are rising for 2023 and beyond.

Today’s perfect storm of historically high inflation, rapidly rising interest rates, and market uncertainty has left many standard portfolio allocations unprepared for the market environment. Additionally, capturing the upside of many structural long-term trends now often requires solutions beyond the traditional asset classes.

The standard commentary for investors during challenged market environments is to diversify portfolios, ensuring that they are appropriately allocated for their goals. In today’s market, allocation to real assets can help address those challenges.

Not only are real assets a natural inflation hedge, but they can also provide potentially attractive real yield with low correlations to traditional asset classes. Along with their inherent exposure to many of today’s long-term investment themes, real assets may help to boost risk-adjusted returns in a way that is tailored to the evolving market environment.

**********

1 As of market close, May 11, 2022

_____________

Risk considerations

Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results. Asset allocation and diversification do not ensure a profit or protect against a loss. Investments in natural resource industries can be affected by disease, embargoes, international/political/economic developments, variations in the commodities markets/weather and other factors. Investing in derivatives entails specific risks regarding liquidity, leverage and credit that may reduce returns and/or increase volatility.

Important Information

This material covers general information only and does not take account of any investor’s investment objectives or financial situation and should not be construed as specific investment advice, a recommendation, or be relied on in any way as a guarantee, promise, forecast or prediction of future events regarding an investment or the markets in general. The opinions and predictions expressed are subject to change without prior notice. The information presented has been derived from sources believed to be accurate; however, we do not independently verify or guarantee its accuracy or validity. Any reference to a specific investment or security does not constitute a recommendation to buy, sell,or hold such investment or security, nor an indication that the investment manager or its affiliates has recommended a specific security for any client account. Subject to any contrary provisions of applicable law, the investment manager and its affiliates, and their officers, directors, employees, agents, disclaim any express or implied warranty of reliability or accuracy and any responsibility arising in any way (including by reason of negligence) for errors or omissions in the information or data provided.

*From page 3: Standard deviation “risk” is calculated on a weighted basis over time with data as of March 31, 2022: 36-month rolling 50%, 12- month 25%, and 3-month 25%. The inflation sensitivity is calculated using 24-month rolling correlation to CPI-U non-seasonally adjusted as of March 31, 2022. Actual risk and actual correlations observed are used by the team for modeling.

From page 4: Bloomberg U.S. Treasury Inflation Protected Securities TR Index (TIPS); Bloomberg Commodity TR Index (Commodities); FTSE EPRA/NAREIT Developed TR Index (Global REITs); S&P/LSTA Leveraged Loan TR Index (Floating rate); S&P Global infrastructure Index (Global infrastructure); S&P Global Timber and Forestry TR Index (Global timber); S&P Global Water Index (Global water); S&P Global Natural Resources Index (Global nat res); BofA 0-3 YR US Fixed Rate CMBS Index (CMBS).

This material may contain ‘forward-looking’ information that is not purely historical in nature and may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

This material is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

© 2022 Principal Financial Services, Inc. Principal®, Principal Financial Group®, and Principal and the logomark design are registered trademarks of Principal Financial Services, Inc., a Principal Financial Group company, in the United States and are trademarks and services marks of Principal Financial Services, Inc., in various countries around the world. Principal Global Investors leads global asset management at Principal®.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment