Orthosie/iStock via Getty Images

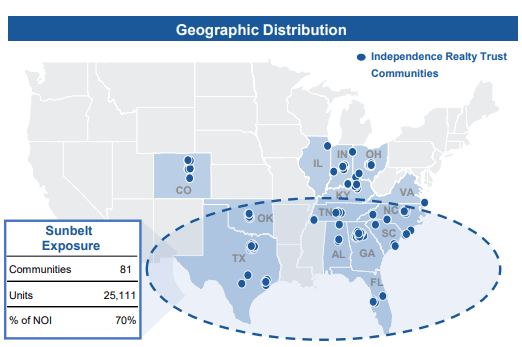

Independence Realty Trust (NYSE:IRT) is a Sunbelt-focused multifamily real estate investment trust (“REIT”) that owns and operates over 35K units in 122 communities.

70% of their net operating income (“NOI”) is generated in the Sunbelt region of the United States. Among their top markets are Atlanta, Georgia and Dallas, Texas, who together account for nearly 30% of total NOI.

November 2022 Investor Presentation – Map Of Geographic Operating Presence

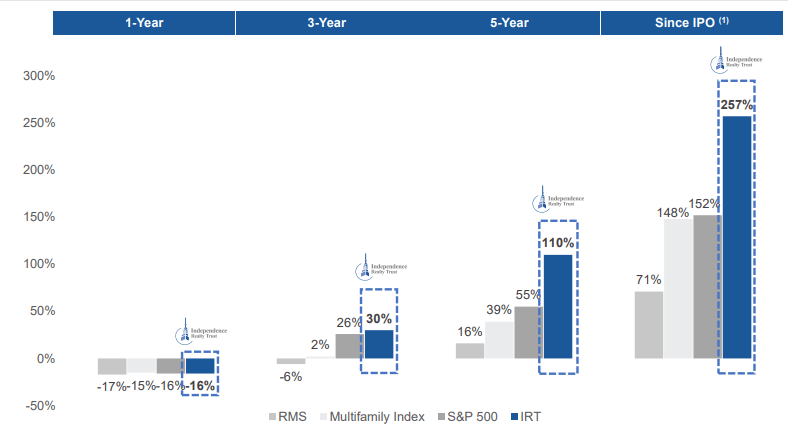

Relative to their peers in both coastal and non-gateway markets, IRT has outpaced industry growth over the past several years, with strong share price performance since their IPO in mid-2013.

November 2022 Investor Presentation – Historical Performance Of IRT Compared To Broader Indexes

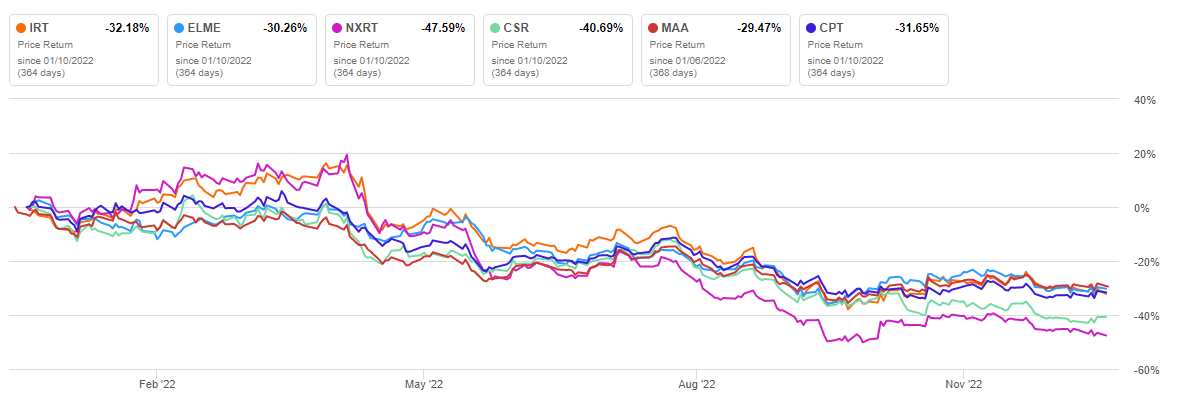

But similar to their peers, shares have struggled over the past year and are down over 30% during this time frame.

Seeking Alpha – IRT 1-YR Share Price Performance Compared To Competitors

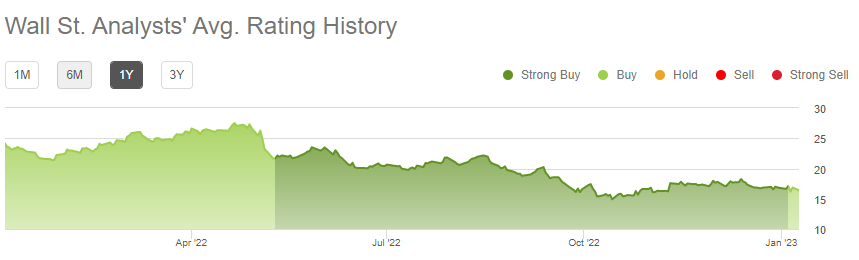

Seeking Alpha’s (“SA”) quant rating system currently rates the stock as a “strong buy”, with favorable grades on most metrics. Sentiment by analysts on Wall Street is also similar, with most analysts bullish on the stock.

Seeking Alpha – Graphical Display Of Wall Street Sentiment Of IRT Over Past One Year

At current trading levels, shares are certainly worth further circumspection. Recent performance, however, reflects a moderating rate environment in their multifamily operations. This is evidenced by lower leasing spreads and occupancy levels, as well through higher concessions. While shares do have significant embedded upside, it’s unlikely the stock will attain the upside in the near-medium term.

Recent Performance

In the most recent quarter ended September 30, 2022, IRT reported 33% YOY growth in core funds from operations (“FFO”). This was driven by a combination of growth in organic rent and NOI, as well as the earnings accretion relating to their merger with Steadfast Apartment REIT, Inc (“STAR”), which was completed in December 2021.

In the same-store portfolio, NOI grew 11.5% on revenue growth of 10.6%. Primarily driving revenues was a 13.3% increase in average rental rates to $1,479/month. It’s worth noting that this level of rate growth exceeded the 12% they posted in Q2.

The strongest contributing markets in the current quarter were Tampa and Myrtle Beach, which posted effective rent growth of 22% and 21%, respectively. In addition, Atlanta and Dallas also provided double-digit contributions of 15% and 14%, respectively.

And even in their weaker markets, such as in Chicago, Birmingham, and Houston, growth rates still averaged about 9%-10%.

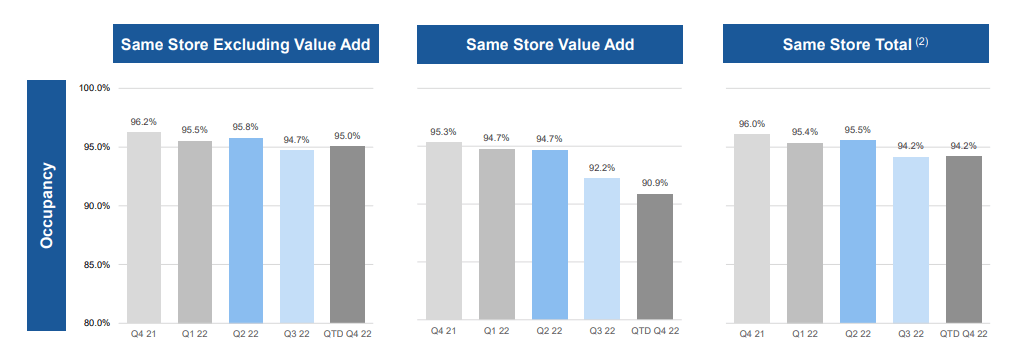

The rate increases did, however, result in a decrease in occupancy levels. This in-turn resulted in some upfront concessions to fill vacant units. These concessions did improve same-store occupancy levels, excluding value add, to about 95%, but this is still down from levels reported in prior quarters.

November 2022 Investor Presentation – Current Occupancy Trends

Despite the hit to occupancy, rates are still exhibiting growth, albeit significantly moderated. Preliminary Q4 figures cited 7.1% QTD growth on rates on new leases through November. Combined with renewal growth of 8%, overall blended rates were at 7.7% QTD. This is down from the double-digit blended spreads achieved in Q3 and well-below the 14% the company achieved in Q4 of 2021.

Retention also appears to have slipped in Q4. In Q3, retention stood at 57%. But at the date of their release, management noted Q4 QTD retention of 50%, though they did provide the caveat that the figure is likely to improve once their residents finalize their renewal decisions.

And on this, the company has the wind at their backs. Move-outs in the current quarter were 18%, which is down from the 21% reported in Q2. This is likely due to a combination of higher mortgage rates and record home prices, which is consequently constraining current move-out options for current residents. Higher average incomes of about $90K and favorable in-bound migration from other states further support the fundamentals in IRT’s operating markets.

Looking ahead to their full-year outlook, management maintained their same-store NOI targets but raised their core FFO/share expectations by half a penny at the midpoint. In 2023, rent growth is expected to further moderate, though the year is projected to bring another year of positive growth in NOI and core FFO/share.

Liquidity And Debt Profile

At September 30, IRT had total liquidity of +$326M, comprised principally of unrestricted cash and +$302M available on their revolving credit facility. In addition, the company has the ability, through their at-the-market (“ATM”) program, to sell shares of their common stock having an aggregate offering price of up to +$150M.

While there were no sale transactions under the program during the current quarter, the company did settle shares previously sold on a forward basis. As part of this settlement, IRT received net proceeds of about +$50M.

Together with reoccurring operating cash flows, which through nine months of the year stood at +$191.2M, the company has sufficient liquidity to meet their short and long-term obligations.

At present, their total debt load represents just over 40% of their total capitalization and stands at a multiple of 7.2x of EBITDA on a net basis. Though this is down from over 8x last year, it is still high in relation to peers.

Mid-America Apartment Communities (MAA), for example, sported a multiple of just under 4x at the end of Q3, while Camden Property Trust (CPT) similarly tracked in the low-4s range. IRT’s load, however, is comparable to similar sized peer, NexPoint Residential Trust (NXRT), whose current multiple is also in the upper single-digits.

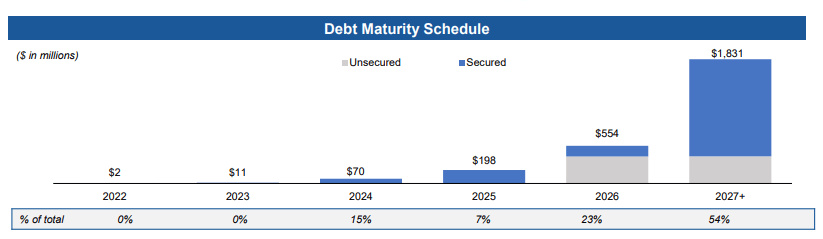

Offsetting their higher debt load is their favorable capital structure that is weighted about 90% to fixed-rate holdings and with minimal near-term maturities. Adequate interest coverage that remains consistent with prior periods further de-risks their current balance sheet position.

November 2022 Investor Presentation – Debt Maturity Schedule

Dividend Safety

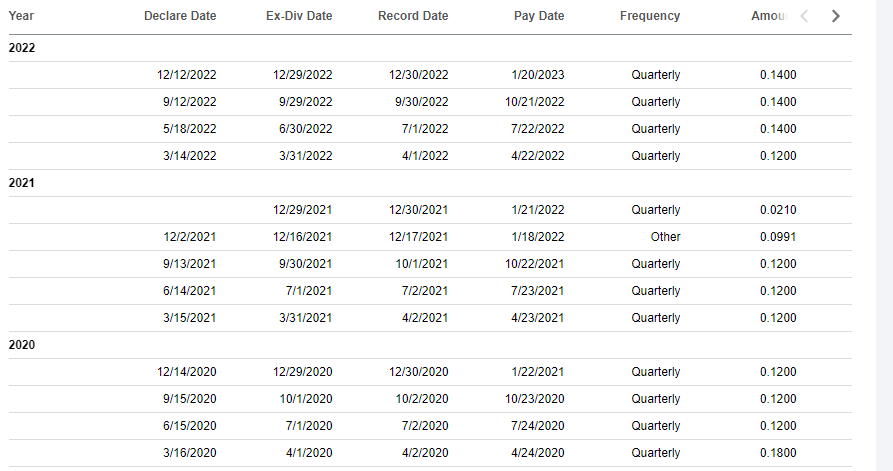

Shares in IRT currently offer a quarterly payout of $0.14/share. This is down from the $0.18/share provided prior to the onset of the COVID-19 pandemic, but it is up about 17% from the reduced payout provided at that time.

Seeking Alpha – IRT Dividend Payout History

At current levels, the payout yields approximately 3.3%. This is largely in-line with other peers in the sector, save Centerspace (CSR), which is currently yielding 4.84%.

Seeking Alpha – Current Dividend Yield Of IRT Compared To Competitors

At 50% of core FFO, the payout appears safe in its current form. In addition, through nine months of the year, their total payouts to common holders represented just under 40% of total operating cash flows. And net of these payouts, the company still had about +$116.8M to fund capital expenditures, which YTD, total +$55.6M.

Main Takeaway

IRT continues to benefit from the same economic tailwinds as other multifamily REITs, the biggest being the current affordability constraints of alternative housing options. And even though rents have steadily increased, their tenant base still remains well-positioned to absorb the increases. Average rent-to-income of their newest residents, for example, stands at 22%, well below the 30% that is often associated with “cost burdened” renters.

Despite the resiliency of the tenant base, there were signs of pushback in the most recently ended quarter (Q3FY22). In the earnings release, management noted declining occupancy levels and increased concessions. In addition, rent spreads have significantly moderated from the double-digit premiums they commanded earlier in the year.

While overall operating performance remains healthy, the best days of rate growth appear to be behind IRT. This is not to say that share price growth has peaked. On the contrary, shares appear underpriced compared to competitors. At 15.6x forward FFO, shares command a lower multiple than both CPT and MAA, who trade at 17.2x and 18.8x, respectively.

In addition, the company recently completed dispositions at a blended cap rate of 4.7%, while also acquiring properties at a stabilized rate of 5.2%. Shares, then, should be reasonably valued somewhere in-between their disposition and acquisition rates.

Instead, the stock is currently trading at an implied cap rate of 6.1% based on its annualized Q3 NOI and current capitalization. By comparison, shares fetched about 4.8% in Q3 of 2021. Assuming a 5.2% cap rate in the present period, shares would have upside of over 30% from current levels. This estimate is also in-line with consensus estimates from Wall Street analysts.

While the upside is significant, whether shares can attain that upside in the near-medium term is debatable. Slowing rate growth will be viewed bearishly. Furthermore, if the Federal Reserve is forced to cut interest rates later this year due to a policy mistake, then mortgage rates would follow in-kind, providing relief to prospective buyers who are currently constrained to the rental market.

Though a solid multifamily REIT, the low-yielding dividend payout combined with slowing growth prospects limit investor appeal in the near to medium term.

Be the first to comment