8vFanI

Over the last five years, Impinj (NASDAQ:PI), which operates a cloud connectivity platform, has been on a tear, climbing from a low of approximately $11.00 per share on April 30, 2018, to its 52-week high of $137.13 on January 18, 2023.

After making a nice run where the company was up over 3x from $11.00 per share from July 1, 2019, through February 17, 2020, it dropped to about $11.50 per share on March 16, 2020, before starting a prolonged run that led to its recent high.

TradingView

It’s been an impressive run considering the overall market conditions it has been operating in, as well as the supply chain constraints that have limited its growth potential.

Even so, it has been prone to significant pullbacks, such as started on January 17, 2022, where it plunged from approximately $89.00 per share to about $40.00 per share on May 9, 2022. Since then, it is up over 3x on January 18, 2023.

The major reason for the recent 52-week high was the recent upwardly revised outlook for revenue in the fourth quarter of 2022, which was guided to surpass $76 million, up from prior guidance of $71.5 million to $73.5 million.

In this article, we’ll look at the most recent numbers from the last earnings report, and why I think the stock is primed for another correction.

Some of the numbers

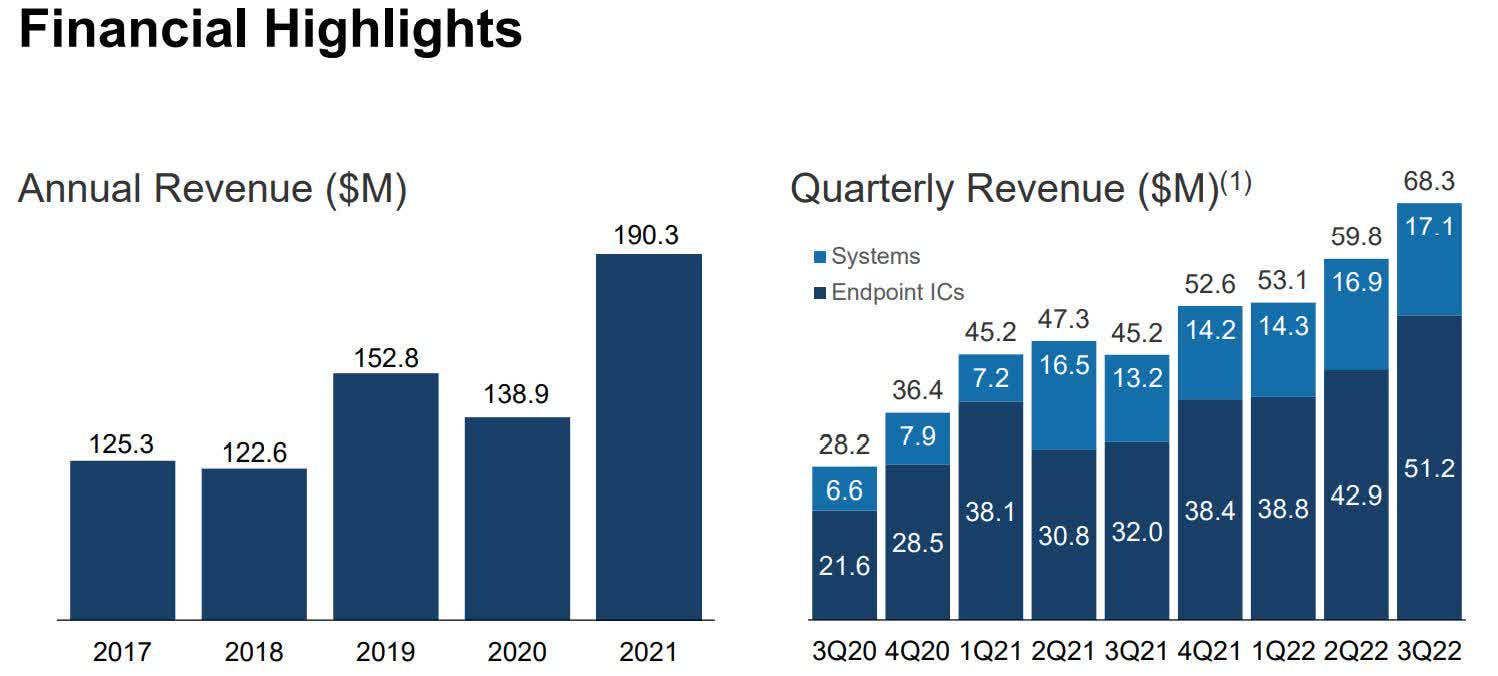

Revenue in the third quarter of 2022 was $68.3 million, compared to revenue of $45.1 million in the third quarter of 2021. Revenue in the first nine months of 2022 was $181.2 million, compared to revenue of $137.7 million in the first nine months of 2021.

Investor Presentation

Gross profit in the reporting period was $37.4 million, with total operating expenses of $39.2 million, resulting in a loss from operations of $1.74 million. That was compared to gross profit of $23.00 million in the third quarter of 2021, with total operating expenses of $35.4 million, resulting in a loss of $12.4 million.

Gross profit in the first nine months of 2022 was $97.7 million, with total operating expenses of $117.3 million, resulting in a loss of $24.2 million, compared to a gross profit of $69.9 million, with operating expenses of $99.3 million, resulting in a loss of $29.6 million in the first nine months of 2021.

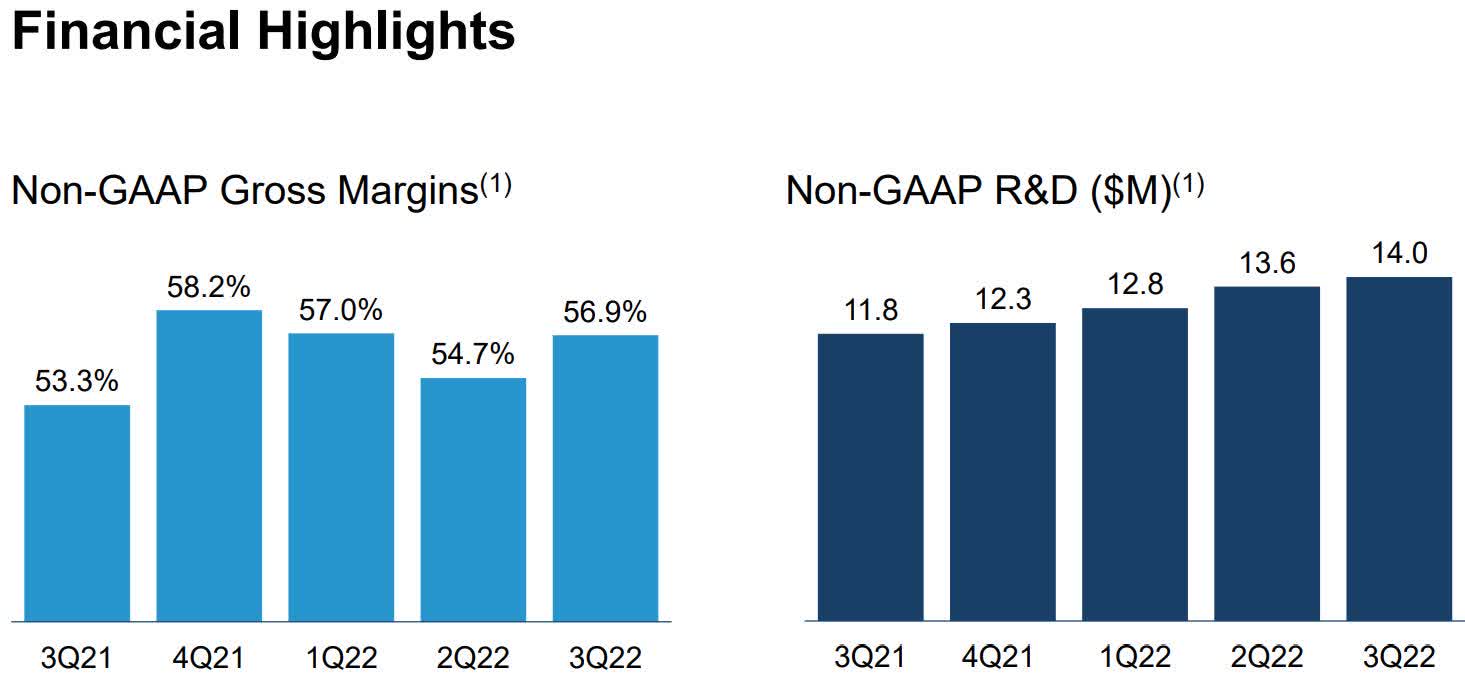

The company has been struggling with expenses and margin, but the trend, as shown in the numbers above, appears to be incremental improvement, as least for 2022.

Investor Presentation

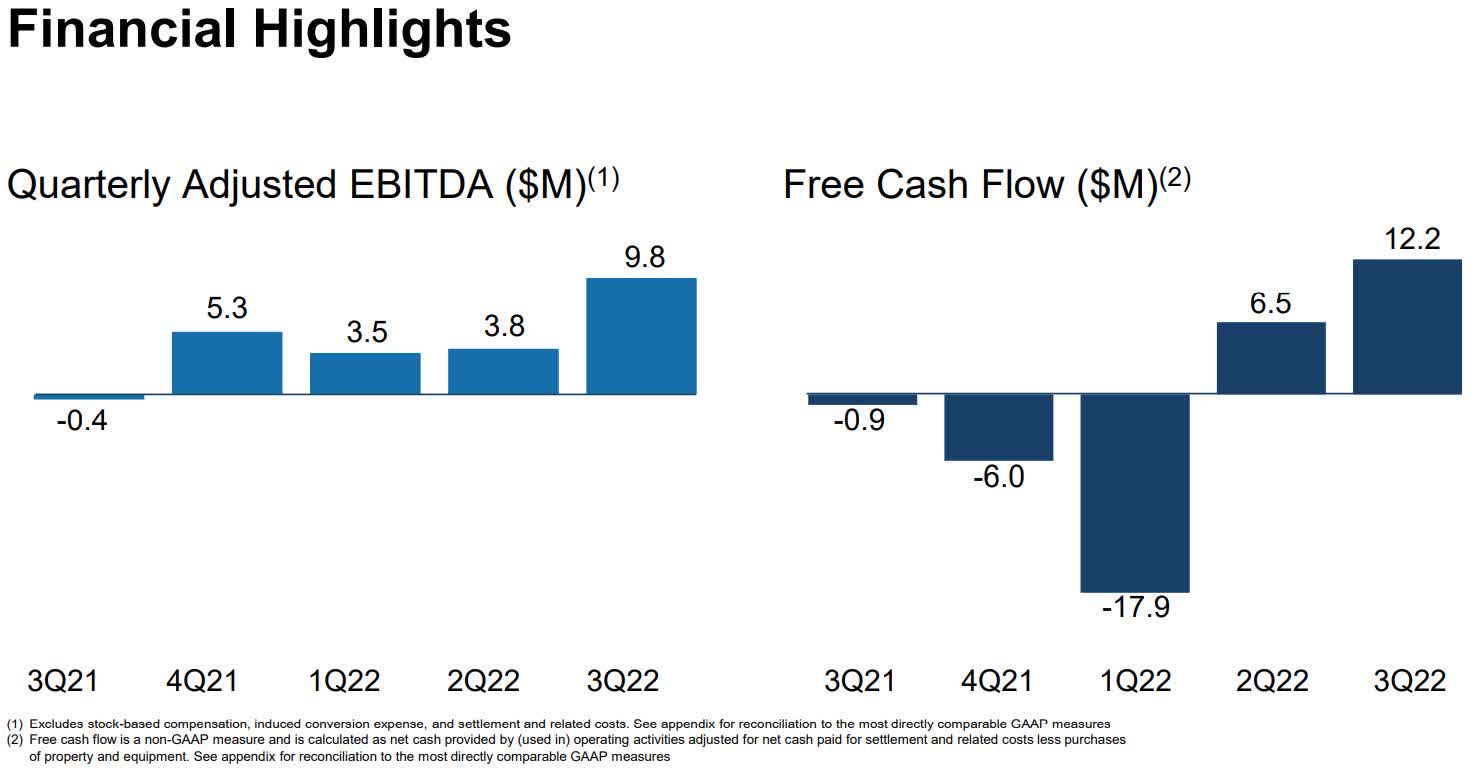

Adjusted EBITDA in the third quarter of 2022 was $9.8 million, compared to adjusted EBITDA of $3.8 million in the second quarter of 2022, and an adjusted EBITDA loss of $400,000 in the third quarter of 2021.

Net loss in the quarter was $(2.2) million, or -$(0.09) per diluted share, compared to a net loss of -$(12.9) million in the first three months of 2021. Net loss in the first nine months of 2022 was -$(24.2) million, or -$(0.95) per share, compared to a net loss of -$(31.2) million, or -$(1.30) per diluted share in the first nine months of 2021.

Again, this shows an improvement in the bottom line throughout 2022. That needs to continue to improve significantly in order to justify the price level the company is trading at.

Cash and cash equivalents in the reporting period were $39.3 million, compared to $123.9 million at the end of calendar 2021. Free cash flow in the third quarter was $12.2 million.

At the end of the third quarter of 2022 the company held $279.8 million in long-term debt.

The challenges it faces

The major revenue driver of IP has been Endpoint ICs, where for six straight quarters it has increased revenue on a quarterly basis. From the third quarter of 2020, when the segment generated revenue of $21.6 million, it has steadily increased to $51.2 million in the third quarter of 2022.

That said, management did say an increase in demand for specialty and industrial ICs in the third quarter exceeded expectations. With that expecting to return to normal volumes in the fourth quarter, the company is likely to struggle to repeat its performance there.

One of the biggest challenges the company faces is in regard to supply chain constraints. For example, a lack of components resulted in shortfalls in its shipments of reader ICs. In the third quarter, supply did finally catch up with demand, but there is no certainty it’ll be able to repeat that in the fourth quarter and onward, based upon orders in its E-family product line.

With supply chain remaining an issue, even with robust demand, any significant interruption would result in underperformance, which when considering its high share price, would bring about a significant correction.

We need to be cautious in how we interpret the company’s communication about supply and demand. An example of that is in relationship to demand exceeding supply by over 50 percent for the sixth quarter in a row. While the company expects that to continue on well into 2023, it’s one thing to have solid demand, it’s another thing to receive the components to be able to meet that demand by shipping products to meet that demand.

Whenever its supply chain issues are resolved, it will be a strong tailwind for the company, but in my opinion, it’s being traded as if they were already resolved, and there weren’t challenges in margin, EPS and the overall bottom line.

My major concern for PI is while it has been growing revenue on a consistent basis from the third quarter of 2020 to the third quarter of 2022, it has failed to consistently improve in gross margins, adjusted EBITDA, and free cash flow.

With gross margins, it’s been up and down from quarter to quarter with no improvement. It has been in a range of 53.3 percent to 58.2 percent during that time, in no specific order.

Adjusted EBITDA has been the same, with the caveat it did break out in the third quarter of 2022, after three straight quarters of decline.

Investor Presentation

As for free cash flow, that has been similar, as it has three straight quarters of decline from the third quarter of 2021 to the first quarter of 2022, before improving from there over the next couple of quarters.

So while revenue has been, overall, consistently growing, a number of other metrics have been all over the place. And some of those metrics are directly related to the bottom line.

Conclusion

There is no doubt there is a lot of demand for its Endpoint IC products, with a significant backlog if it can get the components to meet the demand. I think it’s still going to take a lot of time before that works itself out, so in that regard, the company’s upside is limited, even with its consistent increase in revenue over the last several quarters.

On the earnings side, it is making improvement generally, but it has yet to prove it can sustainably and consistently do so as it boosts sales.

If I saw it start to increase free cash flow to levels that would reflect its current valuation, that would be a large tailwind for the company.

Bringing it all together, I see PI as being on a razor’s edge because, at its current share price level, there is little room for underperformance, as it would, in my opinion, result in a huge correction to the stock.

Nonetheless, even if the company doesn’t underperform in any meaningful way, with the growth trajectory it has been enjoying, I think the share price has gotten way ahead of itself. And if shareholders start taking profits, combined with any meaningful weakness in revenue or earnings, it’s going to take an even bigger hit than is likely to happen in the near future.

I don’t see much upside for investors coming in at this price, but when there is a big pullback, it would be a time to seriously consider taking a position because over the long term, I do think it has a lot of upside left if starting at a lower entry point.

Be the first to comment