Nikada/iStock Unreleased via Getty Images

The recent action we’ve seen in the stock market has been enormously telling, in my view. I said a couple of weeks ago I think the bottom is in, and as such, I’ve been trading growth stocks pretty heavily. After all, when the market makes a tradable bottom, you want exposure to growth, not value, as the former will outperform in such a scenario.

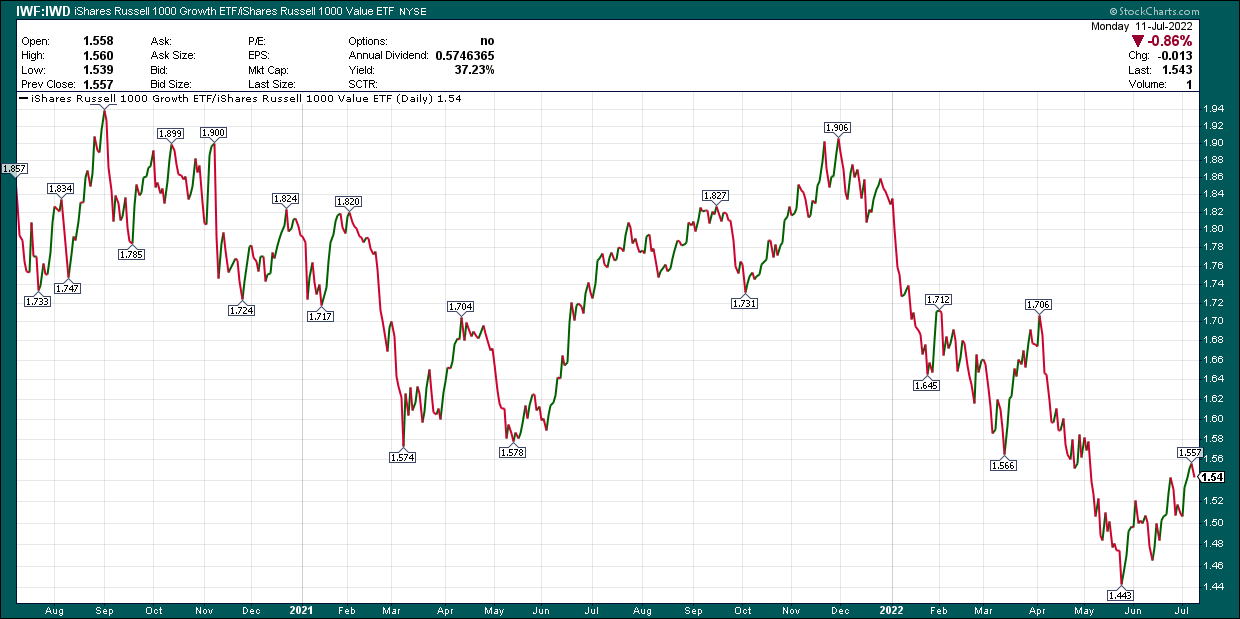

So far this year, value has trounced growth, as we can see below with the growth-to-value relationship in stocks.

StockCharts

This breakdown in growth versus value is why the Nasdaq has greatly underperformed the S&P 500, why consumer staples have outperformed consumer discretionary, etc. However, since the middle of May, growth is beating value, which is one of the reasons why I think we’ve bottomed.

Given this view, and the significance of Apple (NASDAQ:AAPL) to both tech and the S&P 500 due to its enormous weighting, it makes sense to understand whether we can play this bounce via buying the tech giant, or if there are better ways to take advantage.

In this article, we’ll take a look at the technical outlook for Apple, as well as some reasons why I think you should avoid it if you’re looking for market-beating returns in the coming months.

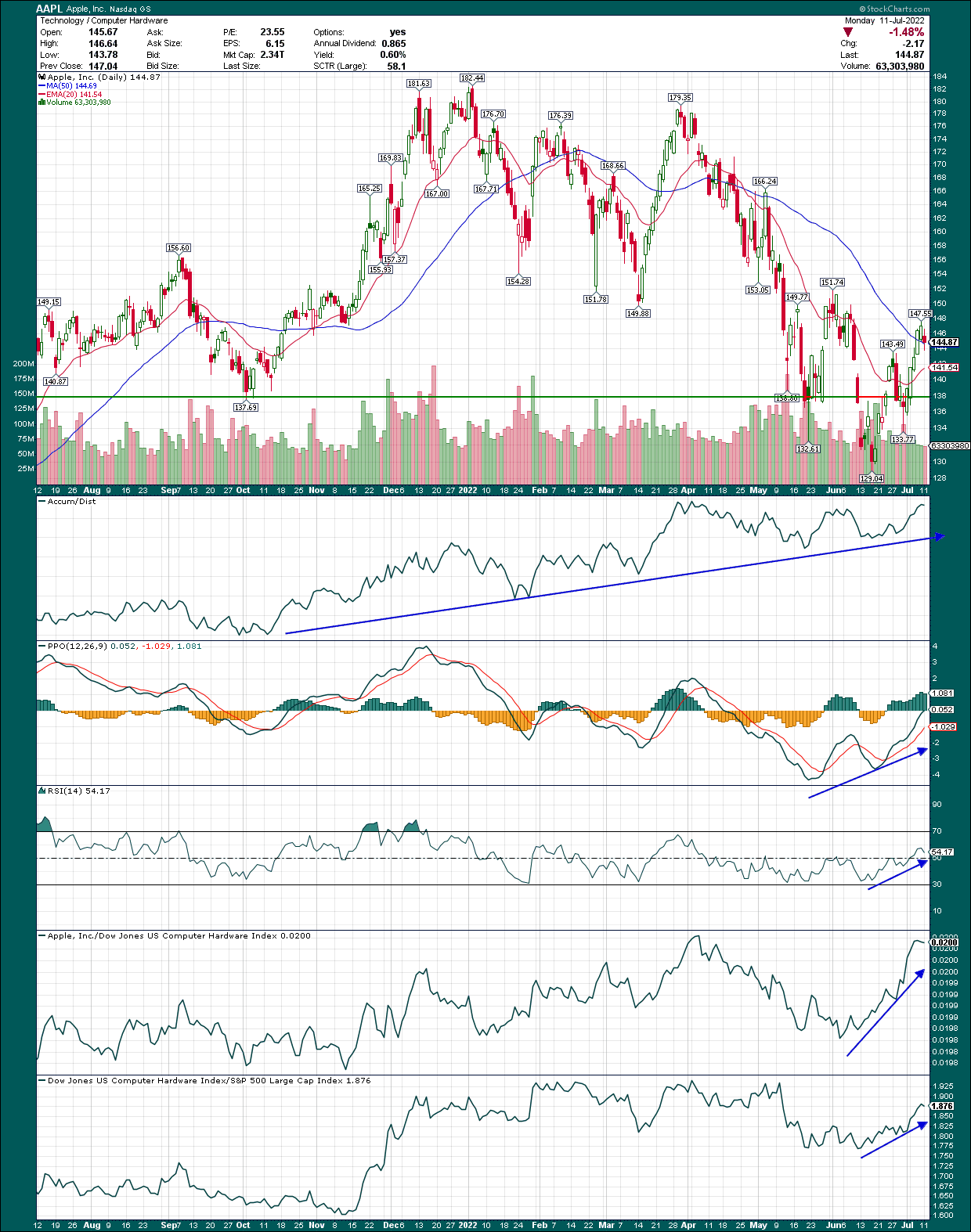

Let’s start with the chart, which has given bears plenty to cheer about this year.

StockCharts

The bottom that was made was fairly messy and looks a bit like an inverse head-and-shoulders pattern, which would be bullish if it came to fruition. I don’t like H&S patterns because they’re unreliable, but it’s worth mentioning. What I do like is price support and resistance, moving averages, and momentum indicators, so let’s see what we have.

There’s strong support at $137/$138 if this pullback gets that far, so if we break that level, we are almost certain to retest the recent low at $133, and potentially $129. I do not think that will happen, but it’s something to watch if you’re long.

Now, the reason I don’t think we’ll get that far is because of all of the other evidence we have. The 20-day EMA is now sloping sharply upward, which is a great sign. Barring a large pullback, we should see the 20-day EMA make a bullish crossover with the 50-day SMA in the coming days.

Next, the accumulation/distribution line is actually making new highs, which is pretty incredible given the weakness we’ve seen in the share price. Wall Street is buying this one on dips, rips, and everything in between.

The momentum indicators look great, as both the PPO and the 14-day RSI have moved sharply higher in recent weeks. While there’s still work left to do, the bulls have done a lot to wrest control from the bears.

Finally, the company’s peer group is flying against the broader market, and Apple is outperforming the peer group. That’s an ideal scenario and another feather in the quill of the bulls.

Overall, I think Apple has bottomed, which is great for the overall health of the market. Given Apple’s weighting, it would be almost impossible for the market to bottom without Apple having done so first. That box has been checked, according to what I’m seeing.

So why am I suggesting you don’t want Apple if it’s bottomed? In short, Apple is no longer a growth stock, so the upside potential is much less than that of actual growth stocks as we come out of the bear market, and into the next phase of this secular bull market. So while I think Apple is going higher on an absolute basis, on a relative basis, it looks unattractive. Permit me to explain.

This is what maturity looks like

Growth stocks, in general, tend to be early-stage, meaning they have lots of runway to add new customers, sell more products, generate more margin leverage, etc. Apple, being one of the world’s largest companies by several different measurements, is about as far from early-stage as one can imagine. That means the runway for improvement in things like revenue and margins is muted, and that’s a problem for relative strength when we’re entering a new bullish phase in the market.

Seeking Alpha

Revenue estimates show ever-declining rates of growth in the coming years, with 2024 looking at a utility-like 3.7% growth rate. That’s just not going to cut it, but it’s understandable. This company is the most successful in the global smartphone market, so there simply isn’t room to take meaningful share as long as Android is around. The other product lines the company has aren’t going to fuel meaningful growth either because, in comparison to iPhone, they just don’t matter that much. I know Apple has other great businesses, including services, which support extremely high-margin growth. But Apple is about the iPhone, primarily.

It also seems like every other day there’s some bearish note from an analyst, which poses a real risk if we have a recession this year (or are already in one now), as expensive tech purchases aren’t exactly at the top of the list for marginal consumers during a recession.

Cowen thinks iPhone shipments will decline 3% next year. Monness, Crespi, Hardt says economic headwinds will curtail growth this year, and potentially into next year. Goldman Sachs says there’s “huge” downside risk in a recession for Apple, and it’s difficult to disagree. The company had demand pulled forward during the pandemic, as did many other companies, so there’s going to be some give-back there. And as mentioned, if we do get that recession, a $1,200 phone is an easy big ticket purchase for consumers to delay or cut entirely.

I’m not saying you have to agree with what these analysts are saying, but I think ignoring it is done at your own peril. We’ve reached a period in the economic cycle where it is certainly possible Apple could need estimates trimmed, so that’s something to keep in mind. The company’s estimates for growth aren’t that great in the first place, and sentiment seems fairly weak at this point, so I’m not seeing a lot of reason to want to own it from a revenue perspective.

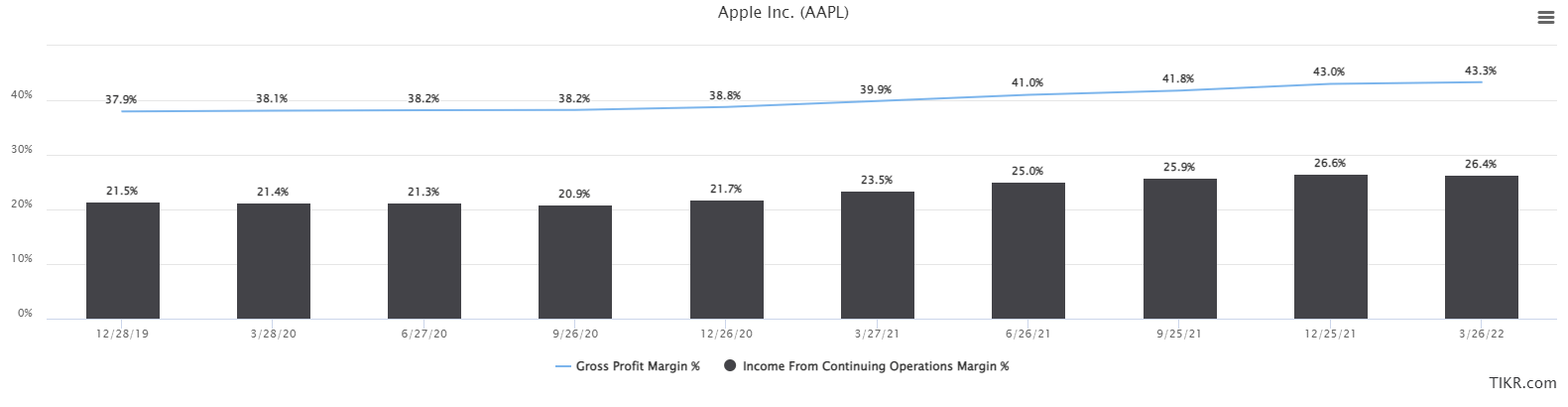

There are other ways to grow EPS besides revenue, however, with margins being the second one. Below we have trailing-twelve-months gross margins and operating margins for some historical context.

TIKR, margins

Gross margins can rise through lower input costs, higher pricing, and other factors, but those things can drag margins down as well. Heading into the pandemic, gross margins were steady at ~38%, while operating margins were around 21%. Today, those numbers are 43% and 26%, respectively. The spread has remained the same, with about 17% between gross and operating margins pre- and post-pandemic. That means that all of the margin expansion we’ve seen in recent quarters has been attributable to gross margins. In other words, there’s been no change in the other costs of operating, so it makes sense to focus on gross margin potential.

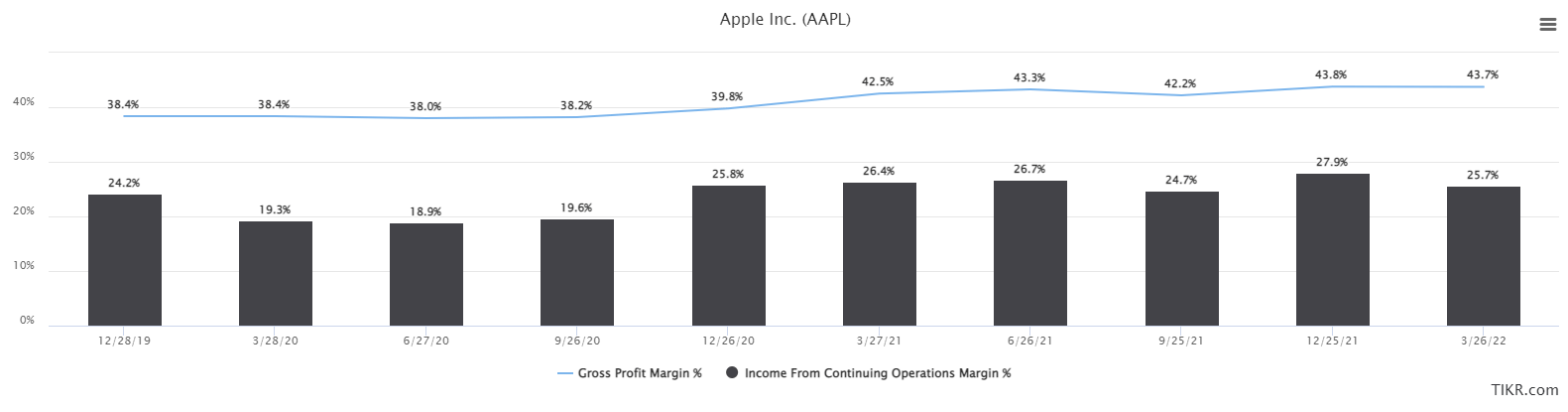

Here’s the same set of numbers but on a quarterly basis, rather than TTM.

TIKR, margins

Gross margins topped out at 27.9% in the Christmas quarter of 2021, which you’d expect given the company sells a lot of products as gifts each year. But if we look at the March 2022 quarter against the year-ago period, we can see gross margins not only plateaued recently but fell 70bps. Now, one quarter is not a trend but in the face of shutdowns in China, immense supply chain issues, rising freight costs, rising labor costs, etc., it stands to reason we’ve seen the top in gross margins for the foreseeable future. We’ll know more with the next quarterly report, but I’d wager we’re going to see weaker margins.

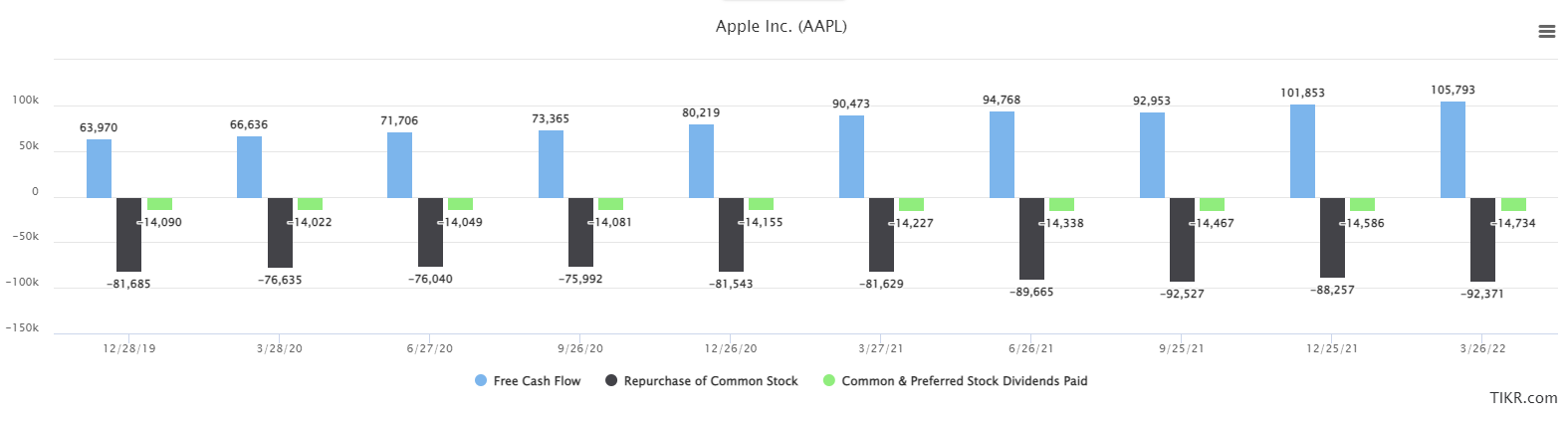

The third way a company can grow EPS is via reducing the “S” portion of EPS, which is to buy back shares. Simply put, the same amount of earnings on a lower number of shares produces higher EPS. We know Apple is a cash generation machine, which we can see below with TTM FCF, share repurchases, and dividends.

TIKR, cash flow and usage

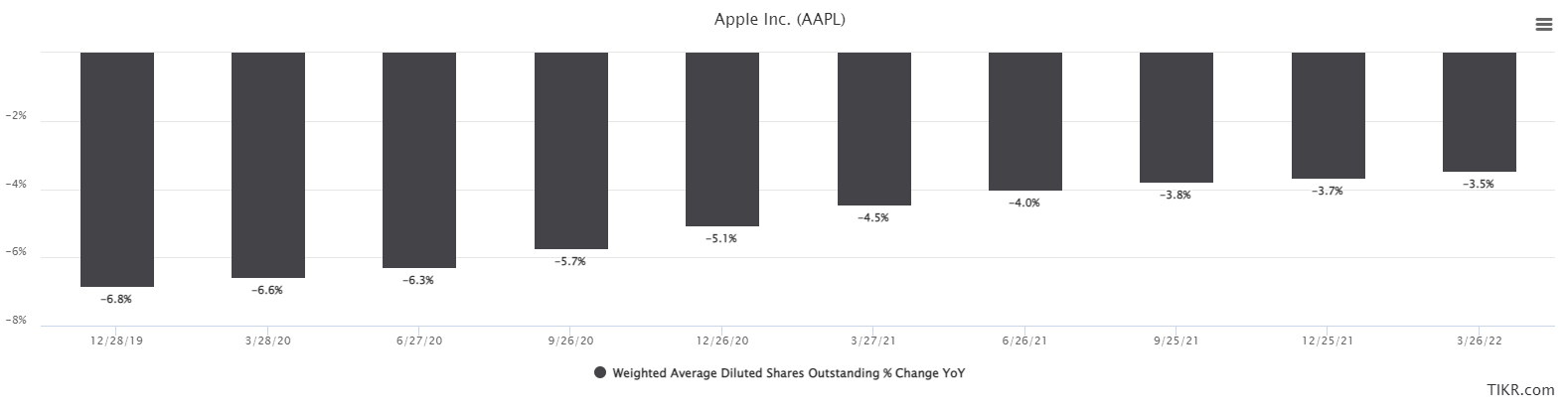

Apple produces in excess of $100 billion in FCF every year, making it one of the best in the world on this measure. It is also spending substantially all of it, with ~$90 billion in repurchases, and ~$15 billion in dividends. That’s been going on for some time, and there’s no reason to believe that won’t continue. But what is that really buying Apple? Below we have TTM net change in diluted shares outstanding, which directly measures the actual impact of buyback spending.

TIKR, share count change

We’re down to 3.5% in the past twelve months, which is fine, but is hardly enough to make up for fairly weak revenue growth, and the very real prospect of declining profitability.

Now that we’ve had a look at the three components of EPS growth – revenue, margins, share count – let’s see what analysts think.

Seeking Alpha, EPS revisions

This chart is still fairly bullish, in that the lines are moving up and to the right, for the most part. We do see some significant downward revisions in the out years, but this year and 2023/2024 look okay. My issue is that we may see some downgrades in the coming weeks/months on gross margin concerns, and if we get further iPhone shipment reductions, this chart could get much less bullish in a hurry.

To be very clear, I’m not suggesting Apple is a sell, or that you need to start shorting it. But what I am suggesting is that in the scenario where growth is likely to outperform value, Apple just doesn’t cut it. It’s not a growth stock, and I don’t see any scenario where it would be considered as such.

So is Apple a value stock?

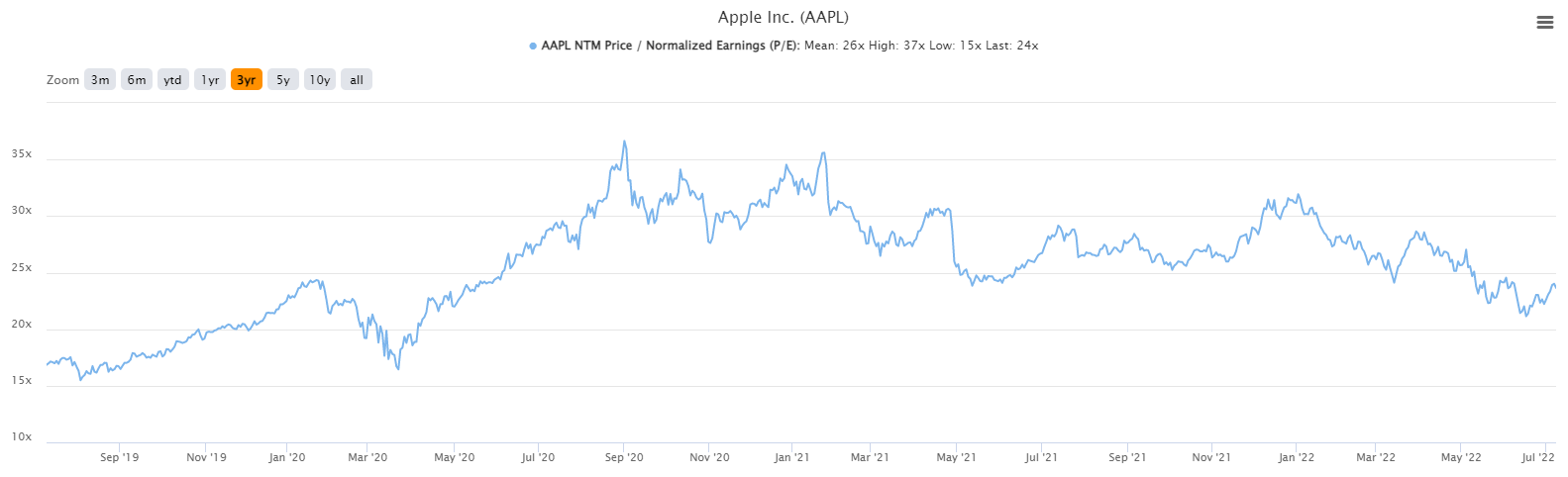

Not really. Apple stock is cheaper than it has been, but at 24X forward earnings, and a company with significant potential headwinds in front of it, I wouldn’t say it’s cheap by any means.

TIKR, forward P/E

The average multiple for the past three years has been 26X forward earnings, as Apple has been assigned a much higher multiple recently due to its burgeoning services business producing high-margin recurring revenue. That’s fine and I don’t have a problem with that sort of multiple re-rating when revenue mix changes. However, at 24X forward earnings for a company with high-single-digit growth potential at best, and low-single digits at worst, it’s not a value stock, either.

Given all of this, I have no idea how someone would make the case that this is a growth stock, but it’s not cheap enough to be a value stock either. I think Apple is going higher later this year, but I also think on a relative basis compared to tech growth stocks, it will underperform. In short, your investing capital deserves better, and I would suggest you use it elsewhere.

Be the first to comment