It’s time to talk about one of my favorite stocks on the market. A company that continues to fly under the radar as it’s a niche industrial company. The Virginia-based aerospace & defense company Huntington Ingalls (NYSE:HII) has been a tremendous source of stability and gains this year. However, the company has frequently been prone to significant selloffs and bad earnings. Both were caused by supply chain headwinds that continue to pressure the company. It’s the reason why the stock hasn’t gone anywhere since the start of the pandemic and why Bank of America downgraded the stock again. In this article, I will elaborate on all of this and explain why the company remains one of my favorite dividend stocks. The yield isn’t high, but the company is about to report accelerating free cash flow, resulting in an almost double-digit free cash flow yield. That makes the valuation attractive, and it helps to provide for a juicier dividend (growth) investment case.

So, let’s dive into it!

No Commercial Weakness, But Supply Chain Issues

With a market cap of $9.0 billion, Huntington Ingalls is certainly not a small player in the aerospace & defense industry. In the case of HII, the company has nothing to do with aerospace except for the fact that its products are used as mobile airfields.

Huntington Ingalls is the only stock-listed company solely focused on building the Navy’s largest ships and submarines. Its largest competitor is General Dynamics (GD), which owns Electric Boat and NASSCO.

Prior to 2011, the company was a subsidiary of Northrop Grumman (NOC).

[…] we design and construct non-nuclear ships for the U.S. Navy and U.S. Coast Guard, including amphibious assault ships, expeditionary warfare ships, surface combatants, and national security cutters (“NSC”). We are the sole builder of amphibious assault ships and one of two builders of surface combatants for the U.S. Navy. We are the sole builder of large multi-mission NSCs for the U.S.

The core business of our Newport News segment is designing and constructing nuclear-powered aircraft carriers and submarines, and the refueling and overhaul, and inactivation of nuclear-powered aircraft carriers.

This segment evolved when HII bought Alion in 3Q21. This deal added asset-light high-tech capabilities to the company, allowing it to participate in multi-domain warfare developments instead of being mainly hardware-focused.

What this means is that the company has no commercial exposure. Unlike a company like Raytheon Technologies (RTX), which is currently 50/50 defense/commercial.

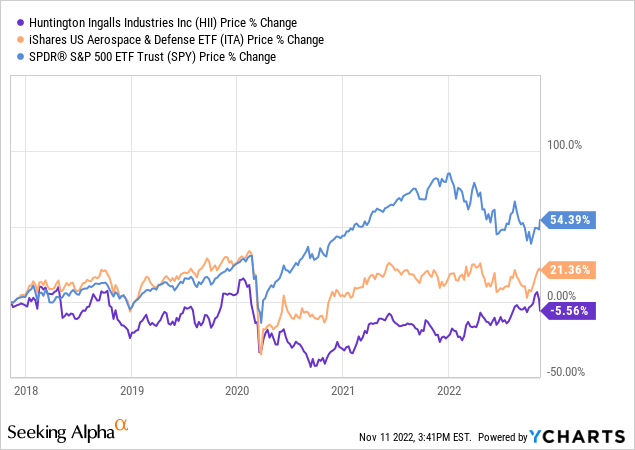

I’m bringing this up because HII hasn’t gone anywhere since 2018. Excluding dividends, HII shares are down 5.6% over the past five years.

In 2019, the stock made a new attempt to break out, which was quickly ended by the pandemic. The pandemic is still putting pressure on HII. However, it’s not for obvious reasons. After all, the company does not deal with commercial aviation.

This is all about supply chain issues.

While I am writing this, I have roughly 24% aerospace & defense exposure. I deliberately made that choice as I like the dividend growth characteristics these stocks bring to the table. However, I would not have bought so much if it weren’t for the sell-off opportunities I got over the past 2 years.

See, every single major A&D player is dealing with supply chain issues. Material shortages, long lead times for electronics like semiconductors, labor shortages, and labor inflation all hurt the industry.

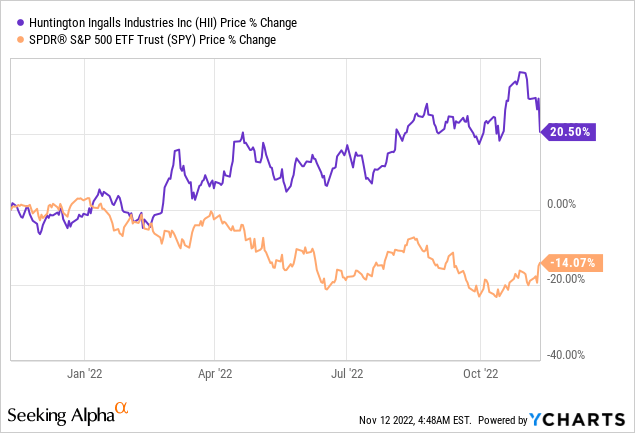

Nonetheless, defense companies are doing a tremendous job generating wealth when it matters most. Over the past 12 months, HII shares are up 21%, outperforming the S&P 500 by 35 points.

Yet, it’s a volatile uptrend with relatively steep drawdowns. The most recent occurred on Friday, November 11, when Bank of America downgraded multiple defense stocks as a result of persisting supply chain issues.

[…] Bank of America downgraded both stocks given persistent supply chain challenges that have shown little sign of fading.

[…] Epstein also cut Huntington Ingalls to Underperform with a $230 PT, saying the company’s anticipated 3% annual shipbuilding growth is “underwhelming given the enormity of funding funneling into the U.S. Navy and fleet modernization,” after the business grew at a 5.6% compound annual growth rate during 2017-21.

With that said, it feels like one of those days where my entire portfolio gets dragged down by defense. However, when looking at the bigger picture, I welcome it as I continue to believe in the importance of owning quality A&D in a dividend growth portfolio. I would not have had so much exposure if it wasn’t for opportunities like the one we just discussed.

Moreover, there is plenty of good news that makes me believe that HII will continue long-term outperformance, leading to very juicy dividends and total returns.

Tailwinds (Orders) vs. Headwinds (Supply Chains)

I’m not writing this to publicly disagree with Bank of America. Most of these banks have more short to mid-term views on companies. I rarely care if banks disagree with me. Especially because I’m in this for the long term. While I did have my doubts about the company because of its slow growth, I remained invested for one major reason. I believe that HII shares are trading well below their fair value.

The just-released third-quarter earnings confirmed that, although it’s not because of its outlook. The company now expects to generate between $8.2 to $8.3 billion in shipbuilding revenue. The prior range had an $8.5 billion upper bound.

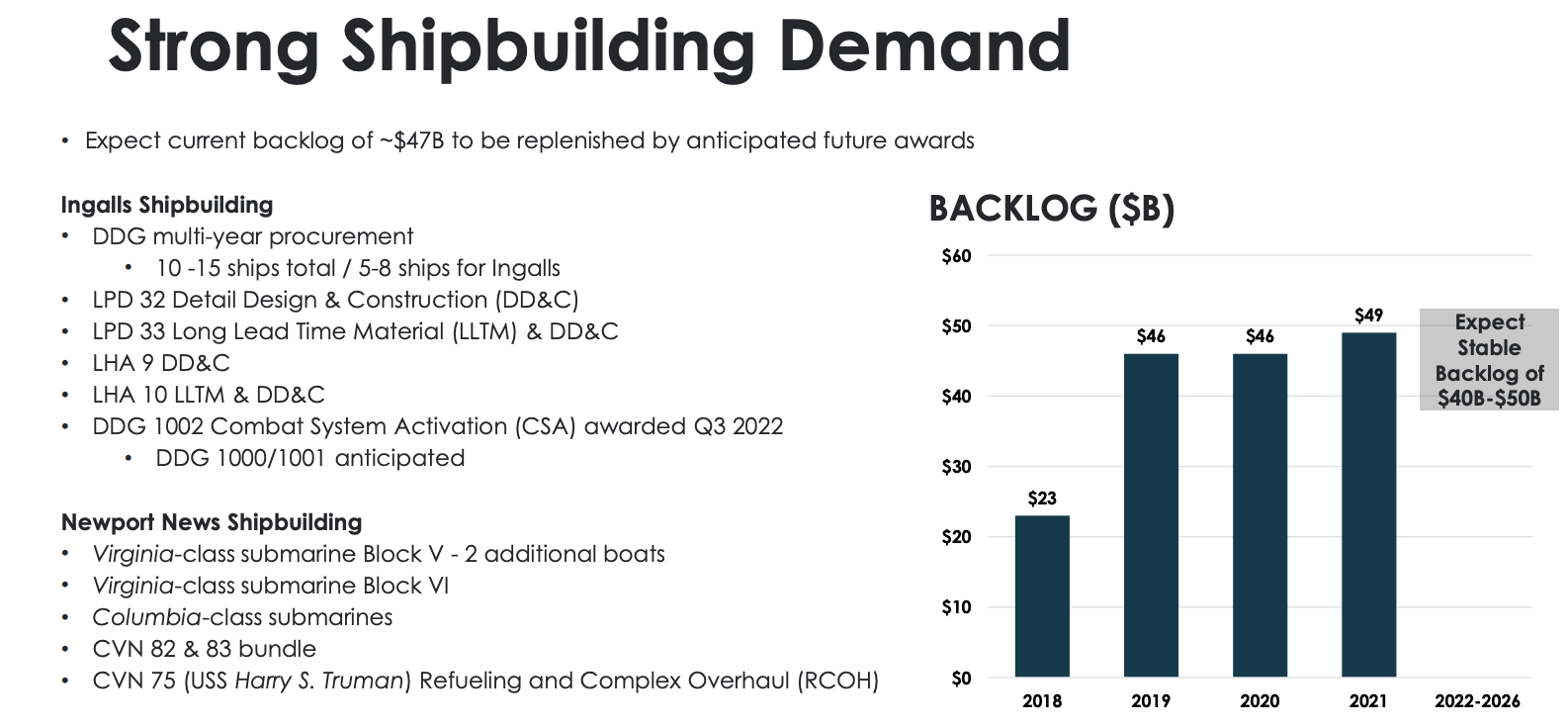

What matters is how HII is evolving. The company won new awards valued at $2.1 billion, which is now resulting in a backlog of $46.7 billion. $23.2 billion of this is fully funded.

Huntington Ingalls

In the third quarter, the book-to-bill ratio came in at 2.2, which implies that orders came in more than twice as fast as the company can turn orders into finished products. It caused the backlog to rise. On a year-to-date basis, the book-to-bill ratio is 1.1, which is a healthy number as well.

One major risk to its backlog is the defense budget. The current budget is still a continuing resolution, which funds the government operations through December.

In a recent article, I highlighted the good news regarding the defense budget:

There’s also good news with regard to the US government fiscal year (“GFY”) 2023 Department of Defense (“DoD”) budget.

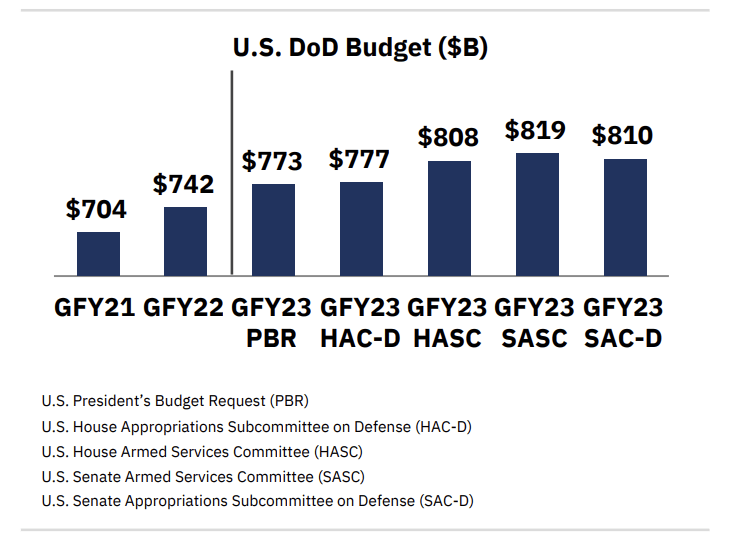

The Senate Appropriations Subcommittee on Defense supports a $37 billion increase to the President’s budget request of $773 billion. This represents a 9% increase year-on-year.

L3Harris Technologies

As the chart above shows, the budget is now likely to end between $773 and $819 billion, indicating a 4-10% growth range versus GFY22.

While Huntington Ingalls remains cautious (as they should until facts are revealed), the company sees strong demand for its products:

[…] we are pleased to see defense oversight committees provide strong support to shipbuilding to include recommendations for new DDG 51 multiyear procurement authority, additional funding for amphibious ships, and requirements for not less than 31 amphibious warfare ships.

The company expects that defense needs cause significant contract award opportunities in the future, boosted by demand for destroyers, amphibious ships, submarines, and aircraft carriers. This includes new construction and maintenance.

However, the company is not out of the woods yet, which is one of the reasons why the stock was downgraded. According to the company:

[…] the operating environment remains challenging and we were not able to overcome the slow start to the services contracting pace which has resulted in revenue guidance moving to the low end of our prior ranges.

The broader macroeconomic environment continues to challenge the company. Mainly a tight labor market with no material improvement in general conditions – so far. So far, the company has hired 3,600 craftsmen and women this year. Its full-year target is 5,000, which could be tricky to achieve.

Moreover:

[…] supply chain challenges continue across our supplier ecosystem, resulting in longer material lead times and inflation pressure. As we’ve discussed previously on inflation, we do have some contractual mitigation and we continue to actively manage the supply chain and our production schedules to minimize impacts.

I believe that these challenges will ease in 2023. Slower economic growth will NOT slow Huntington’s orders. Yet, it will make the labor market a lot less tight. That’s why I believe that the economic slowdown is actually a good thing for A&D companies that can finally smoothen operations. Keep an eye on that as we head into 2023.

The Longer-Term Dividend Bull Case

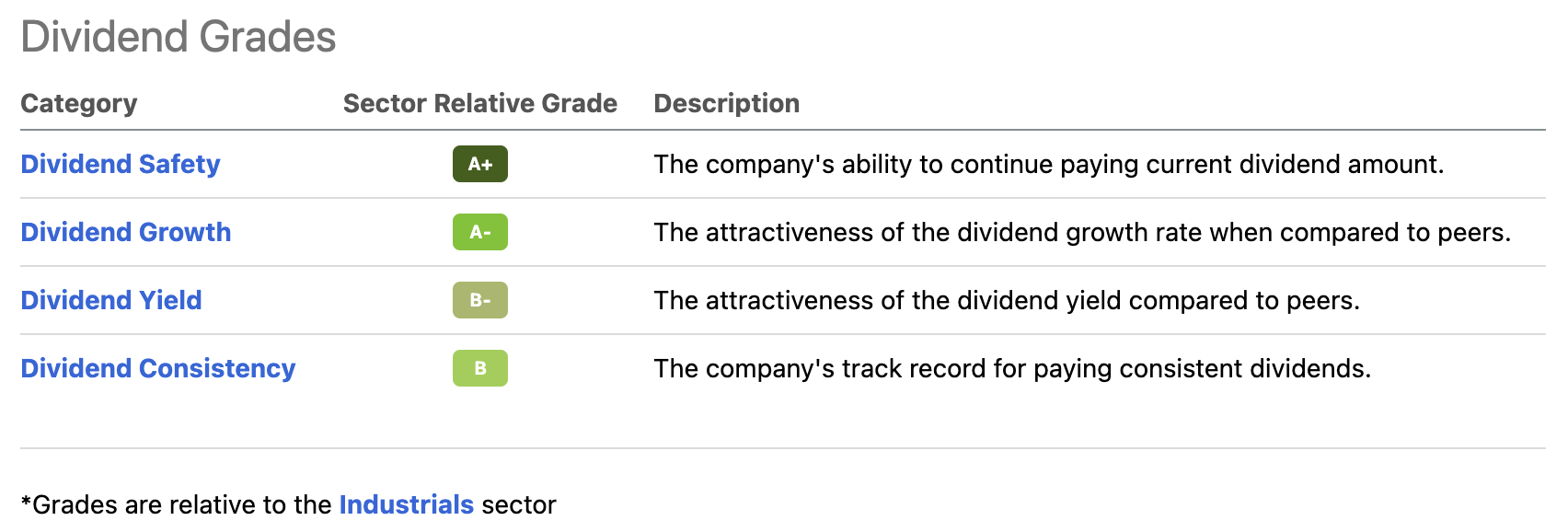

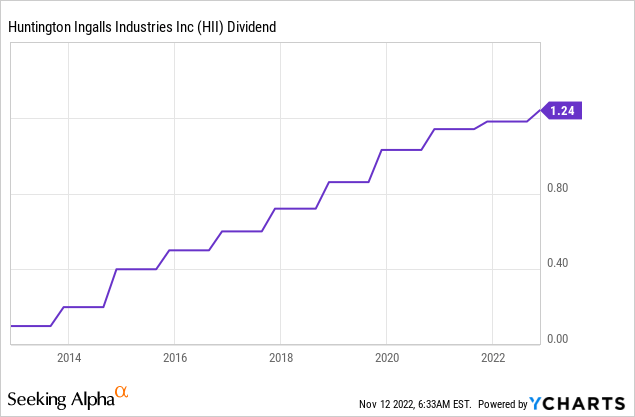

The current HII dividend is $1.24 per share per quarter. That’s $4.96 per year or 2.2% of the current stock price.

A 2.2% yield isn’t something to write home about. However, it’s backed by strong (expected) dividend growth and a fantastic dividend scorecard. The company scores high on dividend safety, growth, yield, and consistency.

Seeking Alpha

The 5-year average annual dividend growth rate is 14.5%. However, that’s mostly because of aggressive hikes after the spin-off from Northrop Grumman.

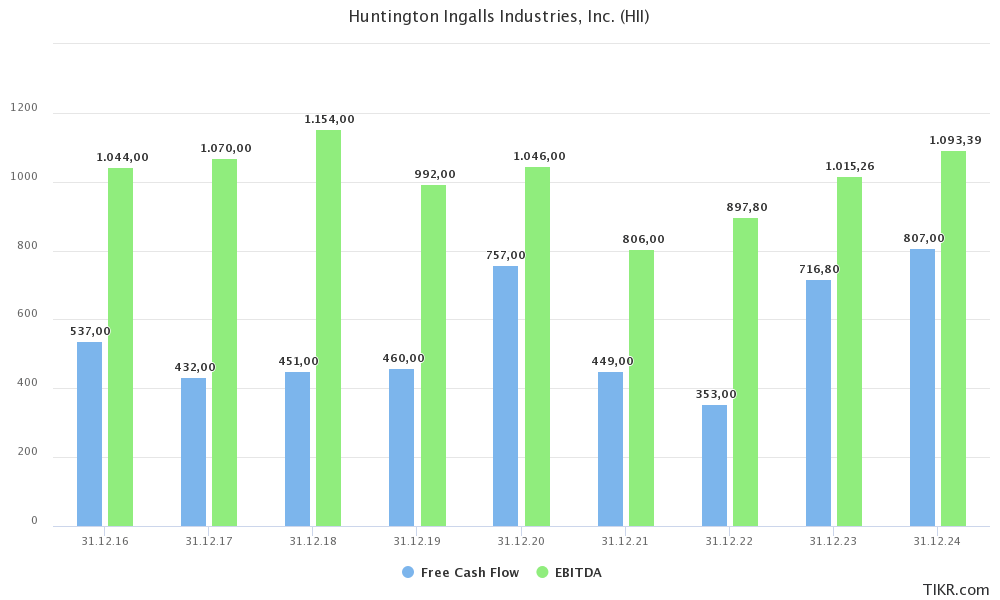

The major reason why dividend growth has declined is lower free cash flow. This is due to working capital requirements and related issues.

Now, the company expects free cash flow to rapidly improve, while long-term shipbuilding revenue growth is expected to remain at 3% per year.

TIKR.com

With that said, while EBITDA is expected to remain rangebound, free cash flow is about to accelerate to a new all-time high in 2024. The company’s guidance sees between $730 million to $830 million in free cash flow. Analyst estimates are at $808, which is somewhere in the middle.

This would imply a 9.0% free cash flow yield in 2024, which is truly impressive. Equally important is that HII is committed to returning substantially all of its free cash flow between 2022 and 2024 to shareholders after planned debt repayment.

The company’s debt target is net debt to EBITDA of less than 2.0x by the end of 2024.

At that point, we’re looking at accelerating dividends again, and buybacks to distribute any free cash flow left after that. That’s a great deal, especially because the company is likely to reach its targets and it trades at an equity value of just $9.0 billion (high free cash flow yield).

This brings me to the valuation.

Valuation

The implied free cash flow yield of 9% is obviously a big part of the valuation. A lot of peers trade at a free cash flow yield below 7%. Most of them are growing faster, which justifies it, but when it comes to finding long-term dividend growth opportunities, I believe that investors are not giving HII enough credit.

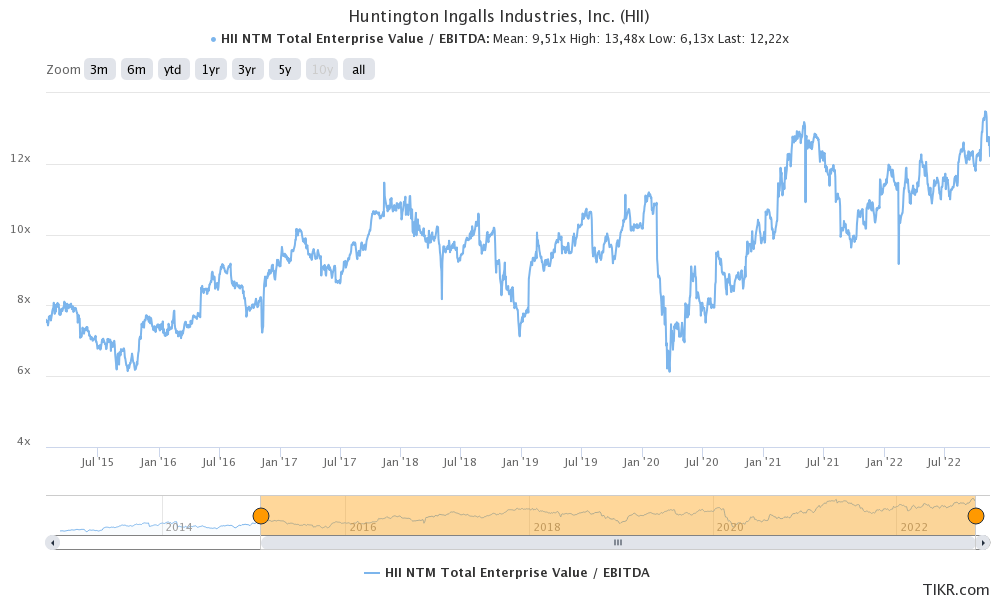

With that said, HII trades at 11.8x 2023E EBITDA of $1.0 billion. This is based on a $12.1 billion enterprise value, consisting of its $9.0 billion market cap, $2.3 billion in 2023E net debt (2.3x EBITDA), and $750 million in pension-related liabilities.

This valuation is fair as we need to incorporate that EBITDA estimates have come down due to supply chain issues. The market has now priced that in. Also, with an unchanged free cash flow forecast, I doubt the stock will get much cheaper.

TIKR.com

Hence, I stick to what I wrote in my last article:

Over the next 2-3 years, I expect at least 30%-40% in capital returns. 50% over the next four years.

Takeaway

My love/”hate” relationship with HII continues. The “hate” part consists of regular sell-offs triggered either by bad earnings or analyst downgrades – both resulting from supply chain headwinds.

The good news is that these headwinds are set to fade in 2023. HII didn’t comment too much on that, yet it’s something I expect given the state of the economy and supply chain improvements.

The “love” part is getting stronger. Not only do I expect supply chain headwinds to linger, but I also expect funding to accelerate. The company is sticking to its long-term free cash flow guidance, which will allow management to accelerate shareholder distributions in the years ahead.

Add to this that HII is attractively valued, and I have little reason to believe that HII won’t continue to outperform the market.

Moreover, its dividend yield isn’t half bad. Add its terrific dividend scorecard, and I truly believe that HII is an undervalued dividend gem worth buying.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment