Alistair Berg

HP Inc. (NYSE:HPQ) and Dell Technologies, Inc. (NYSE:DELL) are two of the most iconic and successful computer manufacturers in the world. HP started as Hewlett Packard in 1939 in a garage in Palo Alto and Dell was famously begun by a college student, Michael Dell, in 1984 at the University of Texas.

Now they are two of the largest PC manufacturers in the world with combined revenue of over $170 million per year. HP, of course, also manufactures a variety of printers while Dell has expanded into cloud services with its acquisition of EMC in 2015.

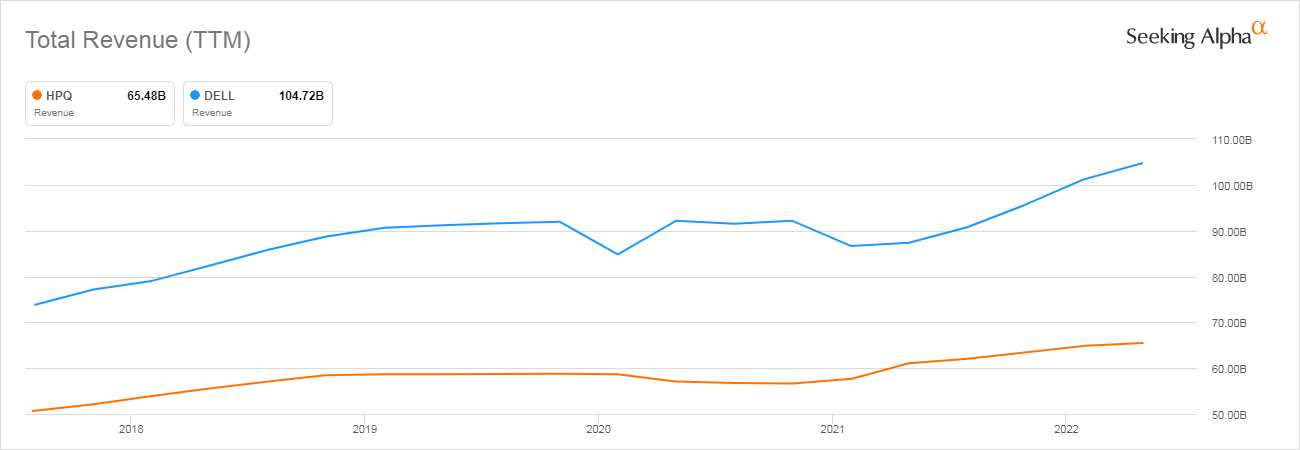

Looking at their 5-year revenue trends, both have increased their revenue but DELL’s increase has been greater at 42% versus HP’s 29%.

Seeking Alpha

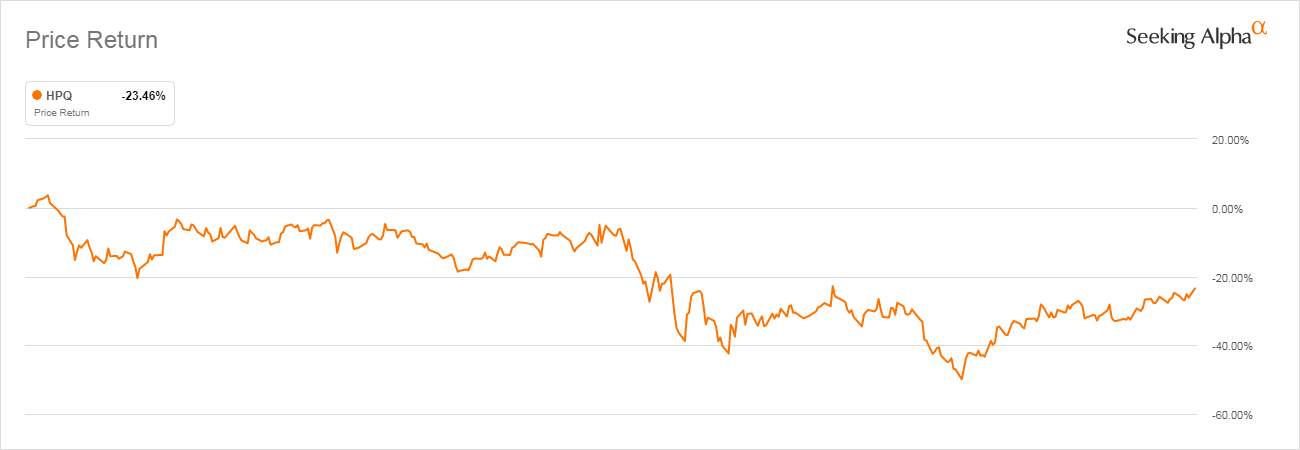

Year to date, both stocks have significantly dropped in price, DELL by 24% and HP by about 15%.

But since Dell went public in 2018, DELL’s price has outpaced HP’s price significantly by 109% to 71%.

Seeking Alpha

In this article, I will compare the current status of both companies and come up with an investment recommendation for both.

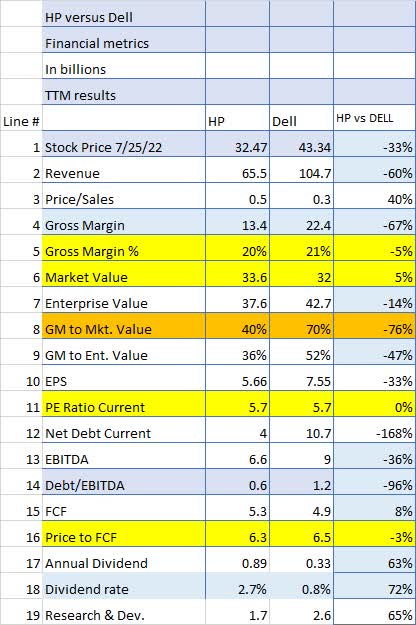

Financial metrics

When looking at the key financial metrics, it is interesting to see how close the two companies are in many of the key metrics.

For example, note the Gross margin (line 5) and Market Value (Line 6) are virtually identical, meaning they both have excellent margins but appear to be underpriced. Other comparables that are very close in value are PE ratio (line 11) and Price to Free Cash Flow (Line 16).

The one item that stands out to me is Gross Margin to Enterprise value (Line 8) where Dell’s is an enormous 70%. That could indicate either DELL is underpriced or HP is overpriced though all other ratios are extremely close.

But both have about the same Gross Margin percentage (Line 5), so no direct advantage there.

Seeking Alpha and author

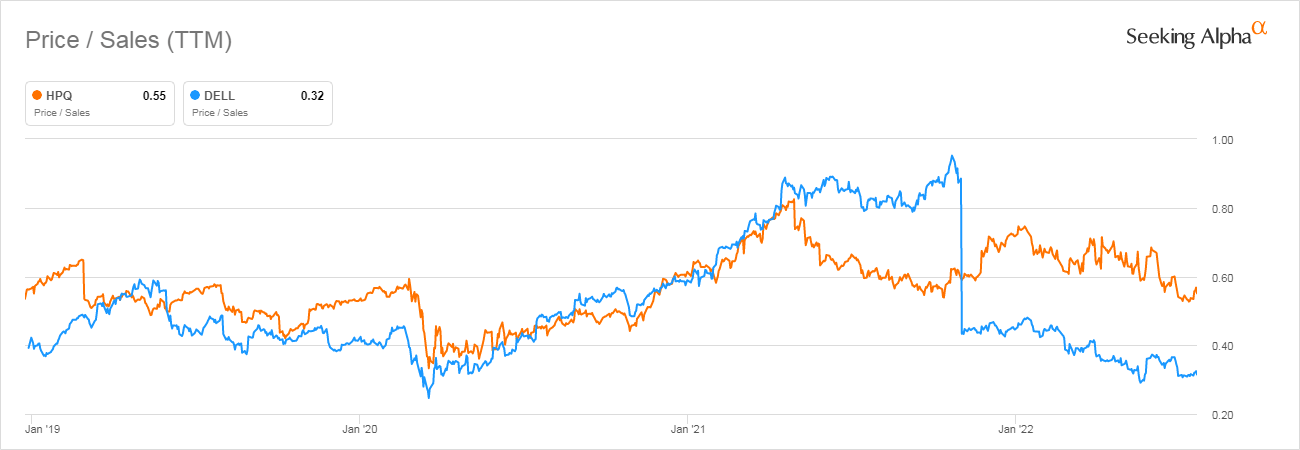

But looking at the Price to Sales ratio historically, we can see that Dell appears to be undervalued currently compared to historical values.

Seeking Alpha

All in all, the metrics are amazingly similar although Dell may be slightly undervalued compared to HP.

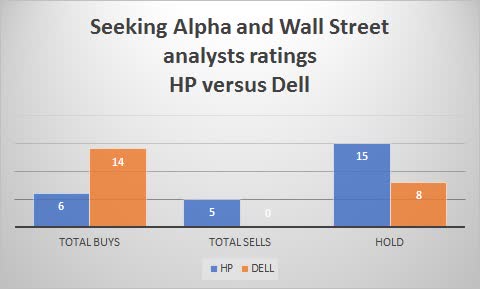

Analysts’ ratings are higher for Dell than HP

If we look at Seeking Alpha plus Wall Street analysts combined, we can see that DELL is more highly recommended than HP with 14 Buys and no Sells versus HP’s almost equal 6 Buys and 5 Sells.

In addition, HP’s 15 Holds show some indecision on the part of analysts.

Seeking Alpha and author

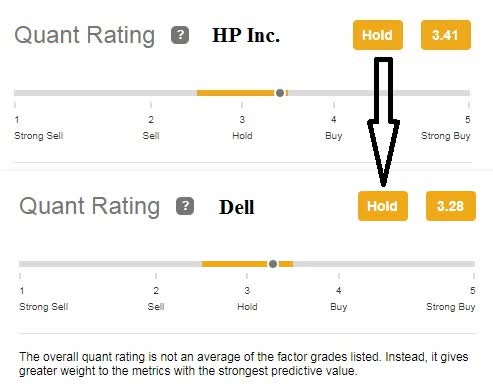

The quants don’t appear to think either one is a Buy at this point with HP rated as a slightly higher Hold than Dell. No enthusiasm from Quants either.

Seeking Alpha and author

HP did not do well in the last recession

If you are concerned, as I am, of a looming recession in the next year or 18 months, knowing how a company did in the last recession can provide some investment insight.

From December 2007 through June of 2009 was the last recognized recession period and HP did poorly down almost 25%. Since Dell went public for the 2nd time in 2018, data for the previous period is unavailable although Dell was public at that time.

Seeking Alpha

However, we do have a recession-like period during COVID-19 that we can use as a comparison. In that particular case, we can see that Dell did much better rising over 130% during that period.

Seeking Alpha

Slowing of business prospects is a concern for both companies

In both companies’ cases, PC sales are the biggest revenue source and right now it does not look good for the next year or so.

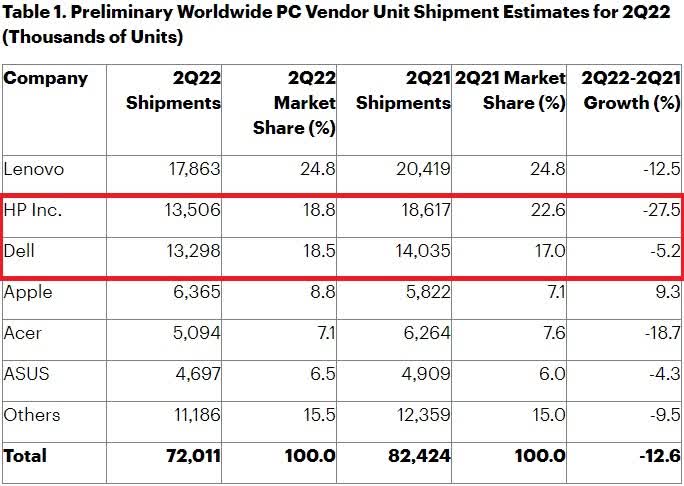

Here are the latest numbers from Gartner and they are not pretty.

Worldwide PC shipments totaled 72 million units in the second quarter of 2022, a 12.6% decline from the second quarter of 2021, according to preliminary results by Gartner, Inc. This is the sharpest decline in nine years for the global PC market, brought on by geopolitical, economic and supply chain challenges impacting all regional markets. Source: Gartner

The downturn is even more evident in this graph from Gartner:

Gartner Group

Note shipments are down across the board except for Apple whose volume went up slightly due to the recent release of the Mac M1.

With the possibility of a recession, inflation, and the huge increase in unit sales during COVID-19 and the Zoom revolution, it is difficult for me to see rising unit sales over at least the next 18 months.

The problem is easily seen in the unit growth numbers from 2020 to 2021 below.

IDC

Those numbers sure look different than the 2021 to 2022 comparisons we saw from Gartner.

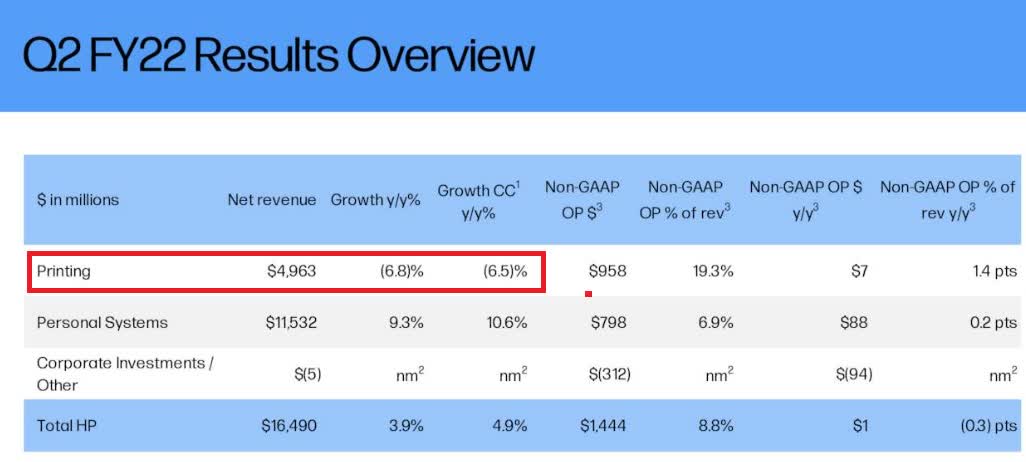

In HP’s case, printer revenues are already trending down from last year.

HP

Conclusion:

Long-term, the future is bright for both companies because their markets will eventually turn around just like they did after COVID. Both companies are profitable, have relatively low debt, and are among the top three PC companies in the world trailing only Lenovo.

But as the negative unit trends shown above indicate the market may be extremely tough over the next year or 18 months and perhaps even further.

The obvious investment question is whether now is the time to buy either of these two companies. Both have shown share price losses over the last 6-8 months in the face of continued logistics and market problems.

But since we are only looking out to 2023, I think we can assume those issues will not be completely resolved by then.

Of course, HP also has the printer business and Dell has expanded aggressively into the cloud market but both areas are very competitive.

As the Financial metrics section above shows, there is not a whole lot of difference between the two companies although Dell may be slightly undervalued compared to HP. But both have to face problems the largest of which may just be negative market sentiment towards hardware vendors in general.

HP has a much more substantial dividend and has raised it every year since 2017.

Until the end of 2023, I see both companies facing headwinds on the revenue side but also from potentially poor stock market performance overall and a large dose of negative sentiment.

Until results improve and market sentiment towards them turns more positive both HP is a Sell and Dell is a Hold.

Be the first to comment