alicat/E+ via Getty Images

So if the Fed raises interest rates, how much and how soon will that help inflation? For another project, I went back to Valerie Ramey’s classic review. Here is her replication and update of two classic estimates:

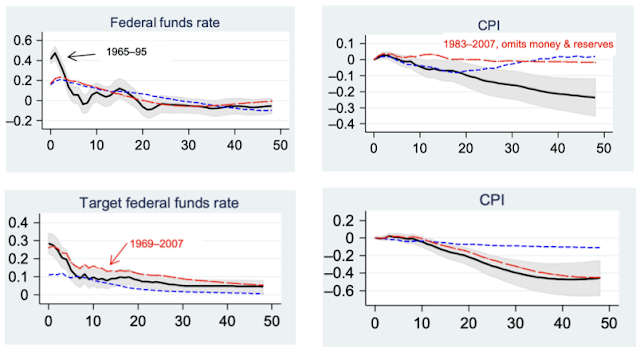

Two estimates of the effect of monetary policy shocks. Top: Christiano et al. (1999) identification. 1965m1-1995m6 full specification: solid black lines; 1983m1-2007m12 full specification: short dashed blue lines; 1983m1-2007m12, omits money and reserves: long-dashed red lines. Light gray bands are 90% confidence bands. Bottom: Romer and Romer monetary shock. Coibion VAR 1969m3-1996m12: solid black lines; 1983m1-2007m12: short dashed blue lines; 1969m3-2007m12: long- dashed red lines (Ramey (2016))

The left side tells us what the federal funds rate typically does after the Fed raises it. The right shows the effect of the rate rise on the level of the CPI. Inflation is the slope of the curve. The horizontal axis is quarters. The top panel uses a vector autoregression. The bottom panel uses the Romer and Romer reading of the Fed minutes to isolate a monetary policy shock.

Top pane (VAR): Multiplying by 10, a 2 percentage point rise in the fund’s rate (blue dash) might lower cumulative inflation by one percentage point in three years (12 quarters) before it runs out of steam. The black line is the most hopeful but it is essentially the 1980 experience. Still, multiplying by 5, a 2 percentage point rise in the fund’s rate only lowers inflation half a percent in those first three years (12 quarters), though after 10 years (40 quarters) you get a full percentage point reduction in the price level.

Bottom panel (Narrative): In the black and red lines that include the 1980 shock, a 3% rise in interest rate produces no noticeable decline in inflation for the first three years. 10 years later, the price level is a decent 4 percent lower, but that is a 0.4% per year reduction in inflation. The blue lines that exclude 1980 show a plausible longer-lasting shock, but a 1% higher interest rate only produces a 1% lower price level in 10 years, 0.1% per year.

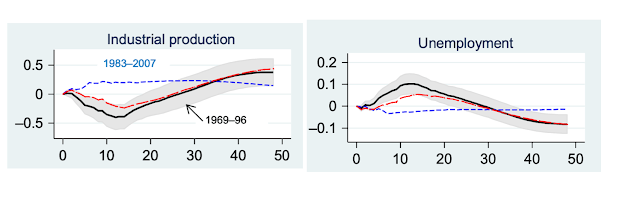

The problem is the ephemeral Phillips curve, which I emphasized in my WSJ oped. In the VARs, the Fed is pretty good at inducing a recession. Here are the Romer-Romer shocks’ effects on output and unemployment:

Author

It’s just that inducing recessions is not particularly effective at lowering inflation.

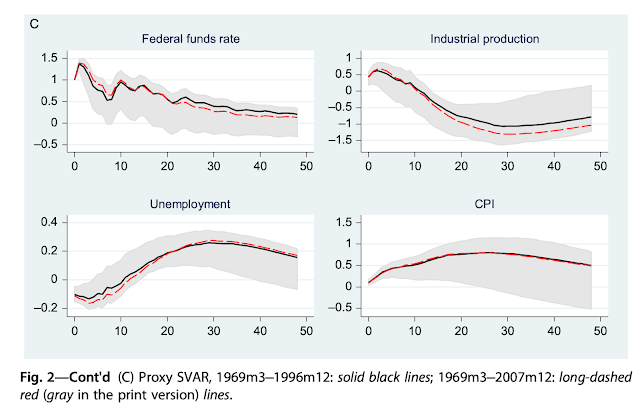

And I cherry-picked good-looking graphs. Many estimates don’t find any effect on inflation or even a positive one:

Author

No theory today, just the facts. This is the empirical basis for the idea that the Fed can swiftly stop inflation by raising interest rates. The underlying machinery does the best that 50 years on the topic have been able to do to separate causation from correlation and to isolate the Fed’s actions from other influences on inflation. Perfect, no, but this is what we have.

Perhaps counting on the Fed to stop inflation all by itself is not such a great idea. And I don’t have in mind more jawboning and WIN buttons.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment