Foryou13

In the early days of the COVID-19 pandemic, the Federal Open Market Committee (FOMC) announced primary and secondary market corporate bond purchase programs as part of its response to the severe market and economic dislocations. These initiatives were aimed at supporting corporations’ access to credit and improving liquidity in the primary and secondary corporate bond markets.

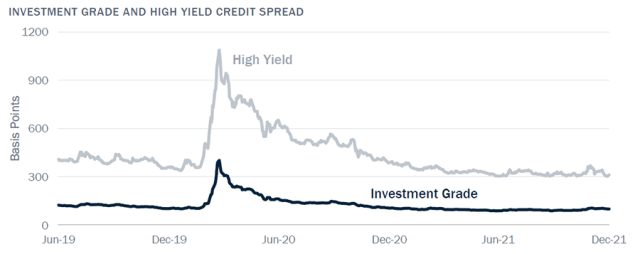

The programs had an almost immediate impact on liquidity and valuations in the investment grade market, where the purchases were concentrated. And even though the US Federal Reserve bought only token amounts of fallen angels and high-yield exchange-traded funds (ETFs), these actions also helped stabilize the high-yield market.

Over the course of the program, investment grade (IG) and high-yield (HY) companies could access primary markets, doing so in record amounts to refinance their debt at historically low interest rates.

The Fed backstop also boosted investor confidence in the corporate bond market, leading spreads on IG and HY indices to quickly retrace to pre-pandemic levels. The programs were so successful in restoring investor confidence that ultimately, out of a secondary market purchase commitment of up to $250 billion, the Fed only bought $13.7 billion of corporate bonds and ETFs.

While these and other Fed responses to the pandemic prevented much worse market and economic outcomes, the corporate bond purchase program has generated criticism.

Some believe corporate bond market interventions have permanently altered price discovery as investors may now assume corporations are ring-fenced from future economic shocks.

Having crossed a longstanding red line and purchased credit instruments, the Fed will most certainly do so again during future recessions or financial crises. Or so the logic goes.

Even if this turns out not to be the case, the expectation of future intervention can still affect corporate credit valuations, at least until that expectation has disappointed. The lower cost of credit for corporations could thus encourage excessive leverage, which could very well sow the seeds of a future crisis.

Fed Intervention Stabilizes Financial Markets

Other investors may believe there is a higher hurdle to Fed intervention in credit markets; that is, it would take a tail event, such as a major financial crisis, for the central bank to bring back the corporate purchase facilities.

Even so, this expectation could impact compensation for bearing long-term credit risk even during normal times, resulting in a new, lower equilibrium for credit risk compensation.

In addition to financial stability concerns, the perception of a Fed backstop for corporate credit may have implications for investment strategy. And these implications are of immediate import, given that recessions in both the United States and Eurozone are likely over the next year.

For example, investors who typically underweight corporate credit markets late in the economic cycle on expectations of spread widening may instead discover that the activation of a corporate purchase program prevents spreads from widening as much as they otherwise would as the economy weakens.

Alternatively, such investors stand to benefit if market assumptions of a “Fed put” in credit markets turn out to be incorrect. Thus, understanding the extent to which market valuations currently reflect expectations of future central bank interventions, and the conditions under which the Fed might indeed intervene during future shocks, will remain important to credit investors.

In this series, we first review corporate bond purchase activity under the Fed’s credit programs during the pandemic. In the second installment, we will discuss corporate bond purchases in the euro area, where the European Central Bank’s (ECB’s) authority to purchase corporate bonds is clearer and more independent of the political process.

Comparisons with bond purchases in the euro area are also useful in our analysis of spreads, model-based valuations, and options pricing. For example, if investors now assume a permanent Fed backstop of corporate credit, US credit might be permanently repriced relative to euro-area credit, where a corporate backstop has been in place for longer.

We will also provide a legal framework for corporate credit purchases by the Fed, as well as the political context of purchases, because these considerations will influence the potential for future interventions in credit markets. By way of contrast, our analysis will also include some discussion of the legal framework for ECB corporate bond purchases.

Following our review of corporate bond purchase activity in the United States and the euro area, we will move on to the heart of our analysis: the search for evidence that credit market interventions have left an enduring “footprint” on corporate debt valuations.

Our focus is on spread levels, pricing of credit indices relative to model valuations, and options pricing. Comparison of current spreads to valuation models, as well as options skew, can help us understand whether Fed and ECB purchases of credit instruments continue to influence pricing.

Finally, we will summarize our findings and determine whether there is clear evidence that the Fed’s and ECB’s purchases of corporate bonds have permanently altered the pricing of corporate credit risk.

A Review of the Corporate Purchases: The Fed

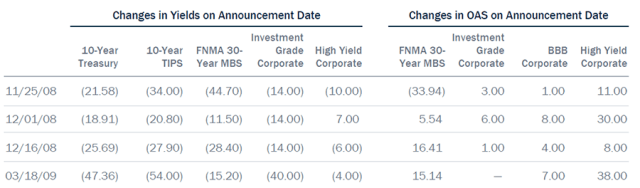

Asset purchase programs as we know them became a staple of US monetary policy in 2008, in response to the housing and resulting financial crisis. On 25 November 2008, the Fed announced that it would purchase up to $600 billion in agency mortgage-backed securities (MBS) and agency debt.

On 1 December 2008, then-Fed chair Ben Bernanke provided the public with details on the program, which was formally launched later that month on 16 December 2008. On 18 March 2009, the FOMC announced it would expand purchases of MBS and agency debt by an additional $850 billion and purchase $300 billion of US Treasury debt.

These announcements resulted in a substantial decline in the yields of various assets, as the table below demonstrates, including those not on the Fed’s buy list. Option-adjusted spreads (OAS), however, generally widened on the news. This was likely due to expectations of an economic downturn and probable increase in default risk, or at a minimum, impaired liquidity conditions at the time.

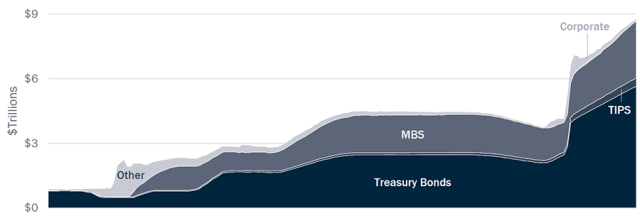

The Fed followed up this first foray into quantitative easing (QE) with two more purchase programs during the recovery from the global financial crisis (GFC). During the pandemic, the Fed returned to asset purchases, at significant scale, only scaling back in November 2021.

The Fed’s balance sheet continued to grow until the first quarter of 2022, albeit at a declining pace, and has since begun to shrink for only the second time since the GFC, in an attempt to tighten financial conditions to combat inflation.

Fed Announcements Alone Can Influence the Market

The purchase of long-term corporate debt is new in the United States, and like past announcements, there was an immediate market response. When the Fed announced a program to purchase investment grade corporate debt and ETFs on 23 March 2020, financial markets responded immediately.

Indeed, the Fed didn’t even start buying bonds until June, but the announcement alone was enough to begin to restore calm to an otherwise fragile market.

The Secondary Market Corporate Credit Facility (SMCCF) was authorized to purchase up to $250 billion of corporate bonds and ETFs, a paltry sum against the $10 trillion corporate bond market.

Still, as has been the case with all other facilities, the market likely assumed the Fed would do whatever it took to restore liquidity to credit markets and expand the programs if it ever became necessary.

Fed Balance Sheet: Securities Held Outright

The expansion of the SMCCF to newly fallen angels and high yield ETFs on 9 April 2020 contributed to the market’s “whatever it takes” interpretation of the policy response.

In the end, the Fed purchased just under $14 billion of bonds and ETFs, but its mere presence restored order to markets in short order. However, this episode alone is insufficient to claim the presence of a Fed put on a go-forward basis.

We need evidence of a more durable impact. If the Fed opened up a Pandora’s box, we would expect more muted volatility, tighter spreads, and lower downside risk than what market participants have experienced in the past.

In future installments of this series, we will look for evidence of this in the ECB’s experience with corporate bond purchases as well as in US markets.

Disclaimer: Please note that the content of this site should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment