JHVEPhoto

Both Alphabet (NASDAQ:GOOG) and Meta Platforms (META) have seen huge draw-downs in their valuations this year, chiefly because advertisers adopted a more cautious outlook in 2022 and cut back on spending. Inflation is weighing on sentiment in the digital advertising industry which has resulted in moderating top line growth and declining free cash flow for both companies. While both companies generate enormous amounts of revenues and free cash flow, I consider one stock to be the clear winner for 2023 and beyond!

Google Vs. Meta: strength and weaknesses

Google and Meta have both been affected by the down-turn in the advertising industry this year which has resulted in slowing top line growth, lower operating margins and pressure on free cash flow. Meta Platforms especially was hit hard by the advertiser pullback which is related to advertisers adjusting their ad budgets in a market defined by economic uncertainties and to Apple’s iOS 14.5 changes in 2021. The iOS change profoundly impacts marketers to this day as Apple requires users to specifically consent to advertisers tracking their online activities. For advertisers this is a big problem and has led to less effective marketing campaigns and a lower return on ad-spend.

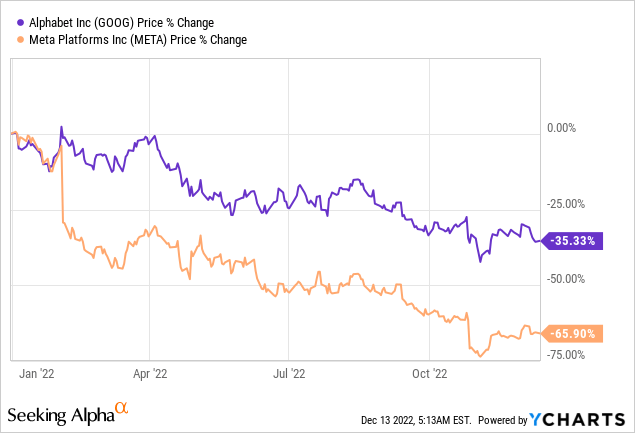

As a result, both Google and Meta have lost large amounts of value this year. Year to date, Google’s stock price has declined 35% while Meta lost almost about twice as much, 66%.

The near term outlook, I believe, favors Google more than it does Meta since the social media company is totally dependent on advertising: the ad business accounted for 98.3% of Meta’s revenues in the third-quarter and Meta projected only $30.0B and $32.5B in revenues for Q4’22, implying a top line contraction of 11% year over year decline. Google’s advertising platforms, for comparison, had a 78.9% revenue share in Q3’22, so they still dominate Google’s revenue mix. However, the online search giant is much less exposed to the digital advertising down-turn than Meta due to the presence of the Cloud business. Cloud is Google’s growth engine and the segment is not only growing revenues rapidly but also gaining market share.

Free cash flow

Both Google and Meta generate an enormous amount of free cash flow, which is the result of their quasi-monopolies. Google has a market share in Search of approximately 92%, according to Statcounter, while Meta’s apps have close to 2.0B daily active users. Both companies give advertisers unrivaled reach in their respective domains which is key to the generation of material free cash flow.

Google generated $62.5B in free cash flow in the last twelve months compared to Meta’s $25.7B. While the advertising down-turn affected both companies’ businesses negatively in FY 2022, Meta was additionally hurt by its aggressive investments in the metaverse which led to a collapse in free cash flow (margins) in the third-quarter. Google’s free cash flow margins also declined, but remained above 20

Meta’s free cash flow dropped 98% in Q3’22 due to ramped up capital spending which may or may not result in a metaverse-related revenue stream going forward. In any case, not only is Google’s free cash flow less dependent on the digital advertising industry than Meta’s, but Google’s free cash flow in the last twelve months was larger by a factor of 2.4 X. For those reasons, Google has a lot more firepower to execute on stock buybacks during a recession than Meta. I continue to believe that Google could announce a $100B stock buyback next year.

|

$millions |

Q3’21 |

Q4’21 |

Q1’22 |

Q2’22 |

Q3’22 |

Y/Y Growth |

|

|

||||||

|

Revenues |

$65,118 |

$75,325 |

$68,011 |

$69,685 |

$69,092 |

6.1% |

|

Free cash flow |

$18,720 |

$18,551 |

$15,320 |

$12,594 |

$16,077 |

-14.1% |

|

Free cash flow margin |

28.7% |

24.6% |

22.5% |

18.1% |

23.3% |

-19.1% |

|

Meta |

||||||

|

Revenues |

$29,010 |

$33,671 |

$27,908 |

$28,822 |

$27,714 |

-4.5% |

|

Free Cash Flow |

$9,547 |

$12,562 |

$8,528 |

$4,450 |

$173 |

-98.2% |

|

Free Cash Flow Margin |

32.9% |

37.3% |

30.6% |

15.4% |

0.6% |

-98.1% |

(Source: Author)

Downward pressure on ARPU and free cash flow

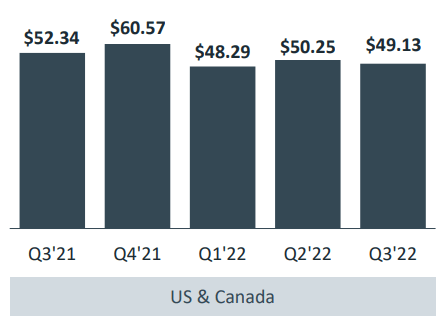

Because of Meta’s reliance on advertising, the firm’s revenue stream is significantly more exposed to volatility than Google’s, which I believe serves to make Google a more compelling investment for investors. A downturn in advertising could disproportionally impact Meta’s average revenue per user/ARPU which is already seeing material downward pressure. Meta’s average revenue per user in North America (the firm’s most important advertising market) declined 19% since the end of FY 2021 to $49.13 in Q3’22 and I can see Meta’s ARPU continue to fall in FY 2023, especially if advertisers move ad dollars over to rival social media platforms like TikTok. Due to Meta’s reliance on digital advertising and the aging profile of its social media network, I believe the company could see a 10-15% decline in ARPU/free cash flow in FY 2023 if monetization, as measured by ARPU, continues to suffer.

Source: Meta Platforms ARPU

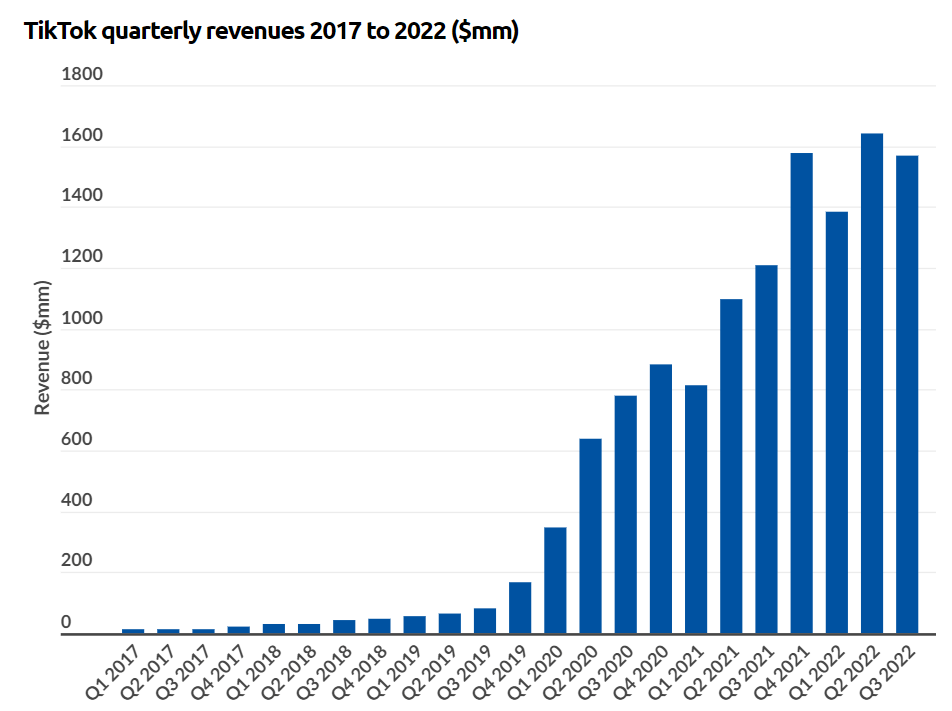

What could add to Meta’s challenges is the rising popularity of TikTok which is appealing to a younger demographic. Social media networks gain and lose in popularity over time and TikTok is clearly ascending. TikTok’s revenues are soaring:

Source: Business Of Apps

A decline in Meta’s user base, partially because rivals like TikTok pull users way from mature social media platforms, could result in a weaker appeal of Meta as an advertising platform. Google, as a search-based company, doesn’t have this problem which is why I see Google’s free cash flows as fundamentally more secure than Meta’s.

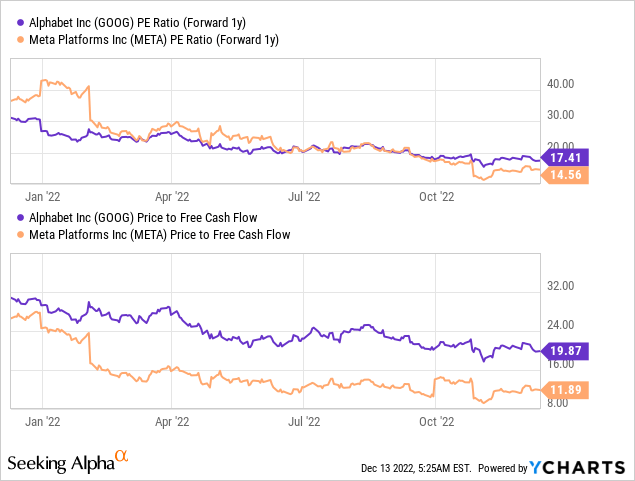

Valuation comparison: Google Vs. Meta

Because Google has its Cloud operations to fall back on if the state of the digital advertising industry continues to deteriorate, the market generally has more positive growth expectations for Google than for Meta. Google’s Cloud segment generated 37.6% year over year top line growth in Q3’22. On the other hand, Meta’s revenues declined 4.5% in Q3’22 and expectations indicate that the social media has a lot more revenue and free cash flow risk than Google.

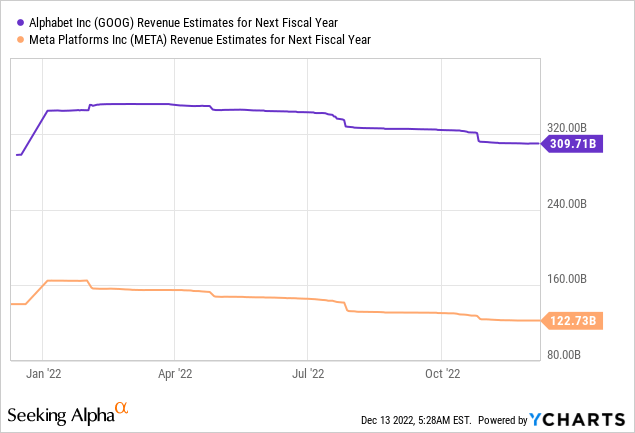

Google is expected to generate $309.7B in revenues next year while Meta is expected to see a total top line of $122.7B, implying growth rates of 9% and 6%. Both companies are seeing slowing top line growth, but, as I pointed out above, Google has a materially stronger revenue and free cash flow position than Meta.

Due to Meta’s full and unmitigated exposure to the advertising market, the stock sells at lower earnings and free cash flow multiples than Google, so Meta’s higher risks are reflected in the valuation. Considering that Google generates much more free cash flow (with less risk) than Meta, I believe Google still offers the better value here, despite a higher FCF multiplier factor (19.9 X for Google vs. 11.9 X for Meta).

Meta has higher earnings risk than GOOG

A 10-15% downturn in Meta’s ARPU/free cash flow could further weigh on Meta’s valuation which is why I recently made the case for buying Meta aggressively at prices of $66-73. For Google, I expect single digit free cash flow growth in FY 2023 as the search giant’s diversification stabilizes its free cash flow profile.

The expected earnings trend for Meta is highly negative with analysts projecting two years of EPS declines, but only one year of declining EPS for Google. The percentage declines for FY 2022 are also much more moderate for Google, too. Google is expected to see an EPS drop of only 15% in FY 2022 compared to Meta’s 34% EPS decline in FY 2022.

Risks with Google and Meta

Both companies have sizable advertising segments, but Google presents investors, at least to some extent, with an offset provided by its Cloud business. Meta’s revenues are overwhelmingly dependent on the advertising market, so the social media company, I believe, has a lot more short-term revenue and free cash flow unpredictability than Google. Meta’s revenues are also subject to potentially steep short-term drawdowns as advertisers can, at the button of a mouse click, suspend advertising spending until they have a clearer view of economic conditions.

Final thoughts

Meta’s business has more exposure to the advertising market than Google which means Meta’s revenues and free cash flow are likely going to be more volatile and unpredictable in 2023 than Google’s revenues and free cash flow. Google offers better diversification due to the presence of its fast-expanding Cloud business and the search giant generates materially higher free cash flow relative to Meta (meaning Google has less down-side risk).

Considering the downward trajectory of the economy, high inflation and growing macro uncertainty, I am heading into 2023 with a desire to prioritize safety and stability… which I believe Google provides. In a direct comparison to Meta, I believe Google wins regarding revenue growth prospects, FCF stability, FCF margins, stock buyback potential and risk.

Be the first to comment