Frederick M. Brown/Getty Images Entertainment

When DirecTV, still 70% owned by AT&T (T), didn’t want to pay another $1.5 billion for the NFL Sunday Ticket, investors have to wonder why big tech wanted to pay even more. Google (NASDAQ:GOOG, NASDAQ:GOOGL) battled with Apple (AAPL) for the right to overpay for limited out-of-market NFL games. My investment thesis remains very Bullish on Google, but the tech giant needs to avoid over spending on sports rights in a race to the bottom in order to reward shareholders.

Not Exactly A Winning Bid

Google’s YouTube announced winning the NFL Sunday Ticket for the 2023 season. The subscription service will air on YouTube TV and YouTube Primetime channels, though the financial terms of the deal weren’t disclosed.

YouTube has been reported as bidding up to $2.5 billion for the deal to beat out Apple and even Disney (DIS), but some reports have the deal value at only $2.0 billion now since the deal apparently doesn’t include commercial rights. The NFL Sunday Ticket has major limits as follows:

- Sunday night games carried by NBC (CMCSA)

- Monday Night Football on ESPN

- Thursday Night Football games that are streamed via Amazon Prime Video (AMZN)

- Sunday regular season NFL games that are broadcast on local Fox and CBS networks

- Other NFL deals prevent the Sunday Ticket from being offered at lower prices to ensure maximum viewership for broadcast games

Either way, Google is paying a substantial amount for a service with a limited streaming audience. DirecTV had ~2 million subscribers on the service regularly costing over $300 with a prior restriction requiring residential viewers to have a subscription to the satellite service.

The current annual subscriptions don’t come anywhere close to paying for the service. YouTube TV has to hope the NFL Sunday Ticket will attract additional subscribers to the service, but more importantly more subscribers to the $64.99 YouTube TV service.

The biggest concern here is that DirecTV couldn’t make the service work at the $1.5 billion cost despite having a satellite TV service that would lock viewers into 2 year agreements. Also, ESPN backed out of the deal long ago, though the leading sports service clearly knows the ultimate value of sports rights and didn’t see much value in paying more than what DirecTV paid.

Race To The Bottom

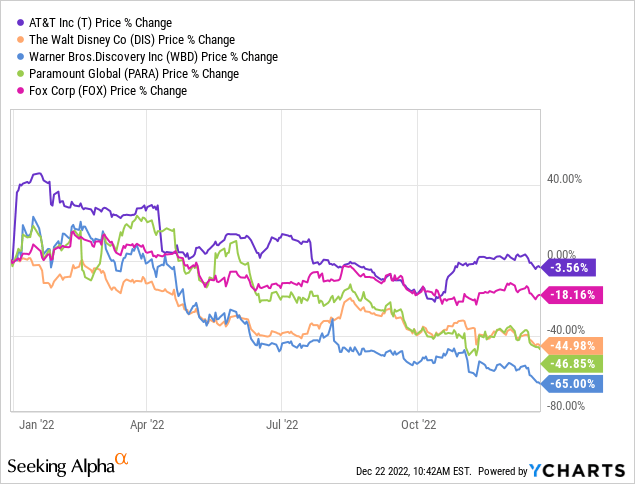

The ironic part about the bidding war for the Sunday Ticket is that AT&T has outperformed the other stocks this year. The company exiting the media space in the last year and not bidding for the expensive ticket has performed by far the best with only a small loss.

The pure media companies have been crushed this year with Disney, Paramount Global (PARA), and Warner Bros. Discovery (WBD) down ~50% on average. These companies have been in a race to the bottom with the excessive content spending and the limited prices of new video streaming services.

For some reason, the big tech companies are following this failed playbook. YouTube won’t even own the content and after years of streaming the Sunday Ticket can easily be replaced by another service such as Apple or Amazon willing to pay even more for the sports rights in the future.

YouTube already has limited profit margins with estimates at ~38%. This deal would only seem to pressure those margins with the service needing to generate $4+ billion in revenues to just produce those margins based on the $2.5 billion rights fee (though the amount might only be $2.0 billion).

YouTube TV probably has even lower margins. The main benefit of such a sports rights deal is to push viewers into other high margin services, but YouTube doesn’t actually have those services and the Sunday Ticket doesn’t have enough subscribers to push the volume of low margin services to drive profits.

Google ended the last quarter with a cash balance of $116 billion, so the company has the cash to pay excessive sports rights fees. The problem is that the deal is highly unlikely to reward shareholders looking for the company to become more productive and boost margins.

Takeaway

The key investors takeaway is that our estimates have Google trading at ~13x non-GAAP EPS targets with the potential to boost the EPS to $10 on hitting efficiency goals. The company paying up for the Sunday Ticket doesn’t appear to help one bit in achieving this goal.

Investors should continue buying Google below $100, but shareholders should pressure the company to move away from bidding wars on media content like expensive sports rights.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment