Spencer Platt/Getty Images News

Thesis

The Goldman Sachs Group, Inc. (NYSE:GS), is one of the largest investment banking companies in the world. The problem is that it is just one of the largest investment banking companies in the world. Goldman’s lack of diversification in revenue streams continues to plague the company. As rates rose at a historically fast pace, Goldman’s reliance on cyclical revenues was exposed and their 2022 earnings reflected that. To make matters worse, their long-term attempt at diversification hit roadblocks as Marcus, their consumer business, announced a shift in strategy and was also reportedly under investigation by the Fed. In my view, Goldman’s recent large layoffs shows the firm’s lack of confidence in its near-term prospects as interest rates continue to rise. I believe Goldman’s valuation is elevated given the abundance of bad news. Therefore, I initiate Goldman Sachs at Sell.

Q4 & FY 2022 Earnings

Overview

Goldman’s most recent earnings were simply terrible and the stock plunged as a result. Their full year net earnings were basically halved as they plunged from $21.64 billion in 2021 to only $11.26 billion for FY22. For Q4, it was even worse. Earnings for Q4’22 were only $1.33 billion compared to $3.94 billion in Q4’21. It was the same story for their ROTE as it dropped from 24.3% to 11.0% for the FY and from 16.4% to 4.8% quarterly YOY. Revenues also showed declines as both their Asset & Wealth Management and Global Banking & Markets showed revenue weakness. In addition, provisions for credit losses also soared. For the FY, provisions were $2.72 billion up from last year’s $357 million, reflecting a conservative stance. Its efficiency ratio worsened from 53.8% to 65.8%. In my view, the stock’s plunge post-earnings was justified as it was truly difficult to find positives from this earnings report. I also believe these earnings reflects why Goldman is chronically valued lower than many of its big-bank counterparts as it is showing high earnings volatility.

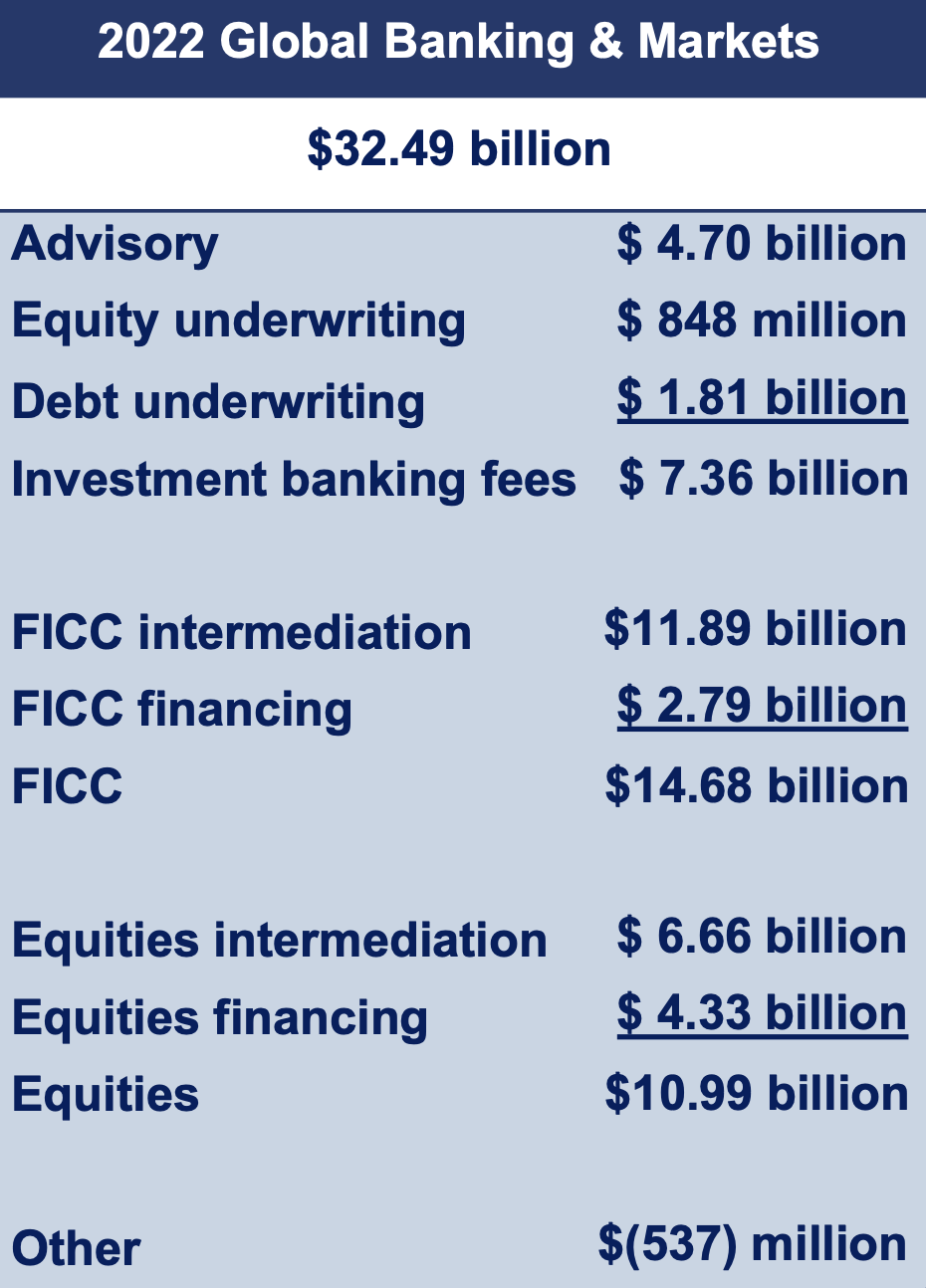

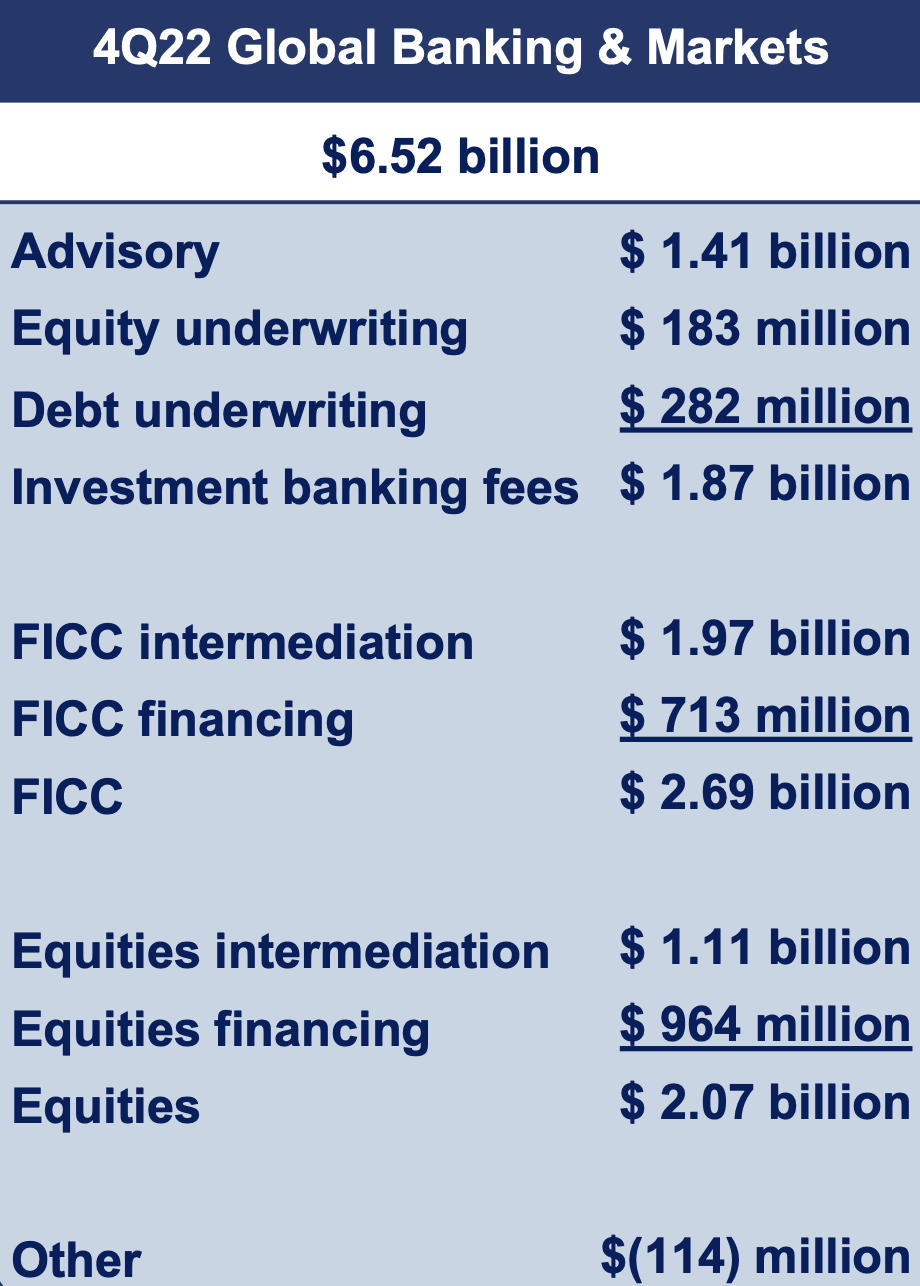

Global Banking & Markets

Goldman Sachs Q4 & FY22 Earnings

For this department as a whole, net revenues were down 12% in FY terms and down 14% quarterly YOY and from Q3’22. Within this department, it is no surprise that the worst performing was Investment Banking fees. Revenues from Investment Banking were down 48% both for the FY and Q4 YOY. Debt and equity underwriting revenues were down due to low issuance volumes and advisory revenues were also lower as M&A activity suffered throughout 2022. Even though it is expected that investment banking suffers as rates rise, this shows that Goldman’s weakness is its large reliance on this segment’s earnings. In my view, Goldman’s flagship segment is directly at the mercy of the Fed. With the Fed continuing to be hawkish, I expect the underperformance in investment banking to continue.

Goldman Sachs Q4 & FY22 Earnings

For their FICC segment, revenues showed a respectable 38% increase in FY terms and was up 44% quarterly YOY. They had higher revenue in FICC intermediation as they had higher revenues in interest rate products, currencies, and commodities for the FY. However for Q4, currencies and mortgages dragged on revenues but FICC intermediation still managed to show Q4 YOY gains. FICC financing revenues were also higher for the FY and Q4 YOY, driven by secured lending. In my view, this segment was perhaps the sole bright point for Goldman as high interest rates likely drove this segment’s respectable results.

Lastly, for their Equities segment, revenues were down 6% for the FY and down 5% for the quarter YOY. This decline was a result of lower revenues in equities intermediation as there was a decrease in revenues in cash products and derivatives. However, equities financing offset some of the lost revenue as it reported higher client activity. With higher trading revenues usually accompanying higher market volatility, I was slightly disappointed from this segment’s overall revenue decline as it failed to offset the loss revenue in its investment banking operations.

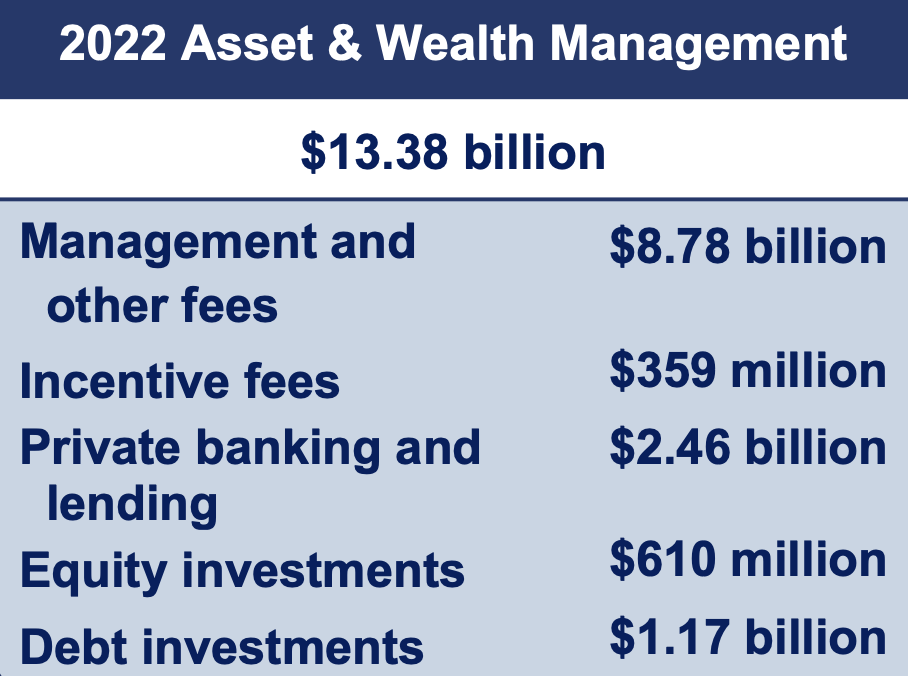

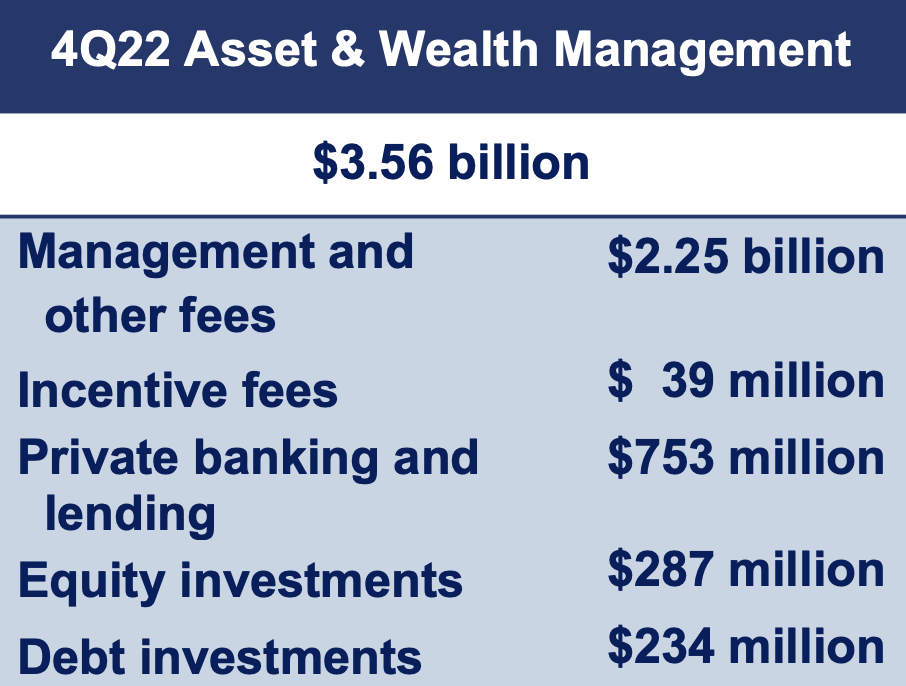

Asset & Wealth Management

Goldman Sachs Q4 & FY22 Earnings

In my view, Asset & Wealth Management results were terrible. For the FY, revenues were down 39% and for the quarter, revenues were down 27% YOY and 12% from Q3’22. This department failed to offset the decreases in investment banking revenues as it showed high correlation. While Asset & Wealth Management departments generally attempt to decrease earnings volatility, Goldman’s Asset & Wealth Management department failed to deliver and instead added to the revenue plunge. They had lower revenue from both debt and equity investments. For equity investments they had lower net gains from private equity investments for both the FY and Q4. For the FY in general they also had mark to market losses in public equity investments.

Goldman Sachs Q4 & FY22 Earnings

Their decrease in debt investment revenues comes from net markdowns and lower net interest income. Their incentive fees also plunged as a result of harvesting in the prior year. The bright spots were Private Banking & Lending and Management & Other fees. The inclusion of NN Investment Partners drove net gains in revenue in Management & Other fees while higher deposit spreads with higher loan and deposit balances created gains in revenue in Private Banking & Lending. From my analysis, this department was a huge disappointment as revenues collapsed with interest rate hikes showing a lack of resilience in its business. Goldman does not have a department to fall back on when its investment banking is suffering.

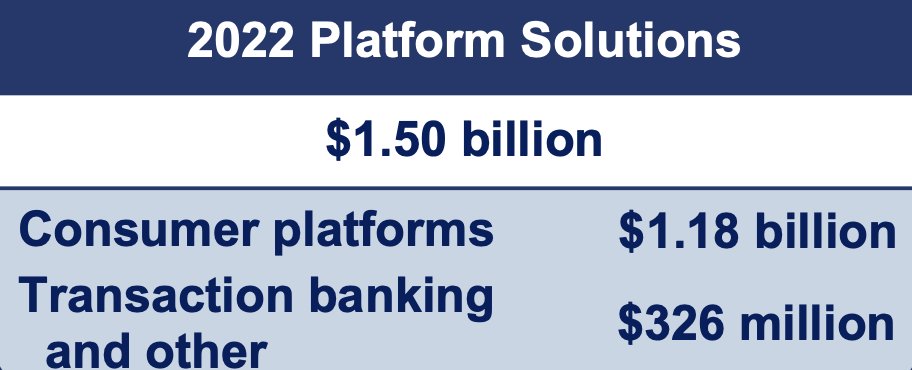

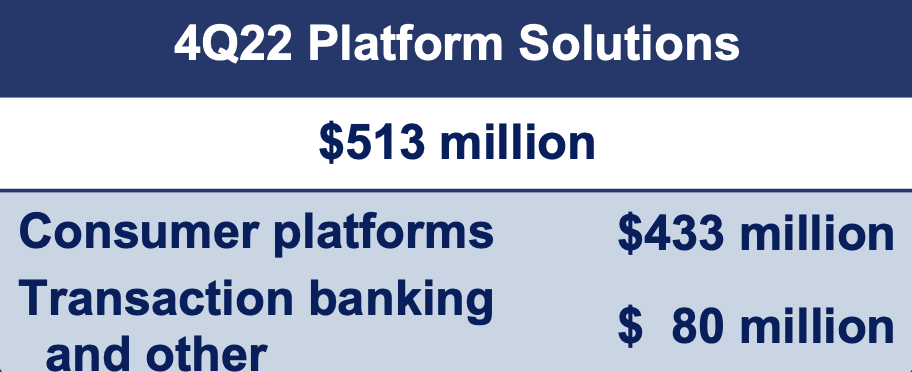

Platform Solutions

Goldman Sachs Q4 & FY22 Earnings

At a first glance, Platform Solutions’ results were good and maybe even great. They reported that revenues were up 135% for the FY and for the quarter up 171% YOY and 36% from Q3’22. However, a closer look reveals a different picture. This department only managed to bring in $1.50 billion of revenue in contrast to Goldman’s total revenue of $47.37 billion. This department is minuscule and is largely irrelevant. In addition, part of these large gains is from higher consumer platform revenues driven by higher credit card balances.

Goldman Sachs Q4 & FY22 Earnings

In my view, high credit card balances can become a double edged sword in the long run and therefore not a sustainable source of revenue gains. The other component, ‘transaction banking & other,’ also showed gains due to higher deposit balance, likely as a result of higher rates. Overall, from my analysis, while results seemed to be decent, results from this department are mostly irrelevant given the size of this department and major issues with Marcus that will be discussed later.

Marcus

In October of last year, it was reported that Goldman was shifting its strategy in its consumer banking business. They admitted missteps as they shifted their goal away from building a full-scale digital bank. Instead of mass acquiring customers, they are shifting to attracting customers using workplace and wealth management channels and also just focusing on existing clients of Marcus. As reported by CNBC, this comes after many internal issues such as executive turnover, branding confusion, and product delays. It was also reported that even their Apple Card partnership was not as profitable as Goldman hoped it would be. Simply put, Marcus has become a nightmare for Goldman. In my view, they attempted to diversify their revenue streams in an effort to decrease earnings volatility but they failed spectacularly.

To make matters even worse, it was reported in January that the Fed was investigating Marcus. The Fed is investigating if proper safe-guards were used to protect consumers as it increased lending in the consumer division and the stock dropped as a result. I believe these issues have both short-term and long-term implications. In the short-term, Goldman’s earnings and reputation will continue to be weighed on by its failing consumer business. In the long-term, questions will be raised on how Goldman plans to diversify after this failed attempt. Nonetheless, in my view, nothing is going right for Goldman’s consumer business right now and that will continue to weigh on Goldman’s earnings and valuation.

Macro Headwinds

Earlier this month, the Fed raised rates by another 25bps and hinted at more hikes to come. The overall tone of the Fed is that they believe inflation has come down somewhat but is still elevated. They are looking for more evidence to confirm that inflation is truly cooling. The Fed and Jerome Powell’s wording does not signal an end to rate hikes and also does not hint that rate cuts are coming later this year. In addition, the most recent job report shows highly unexpected strength giving the Fed even more room to raise rates. Therefore, I believe Goldman is facing another tough year in terms of the macro environment. With most of their businesses negatively affected by interest rate increases, I believe their earnings will continued to be weighed on and their lack of diversification will be exposed once again this year.

Goldman also shows a lack of confidence in its near term prospects as they announced major layoffs in January. They are cutting up to 3,200 employees equaling 6.5% of their 49,100 employees. Even though these cuts are less than originally feared, it signals that Goldman expects continued weakness. Needless to say, more storm clouds are looming on the horizon for Goldman this year and its valuation will be compressed as a result.

Valuation

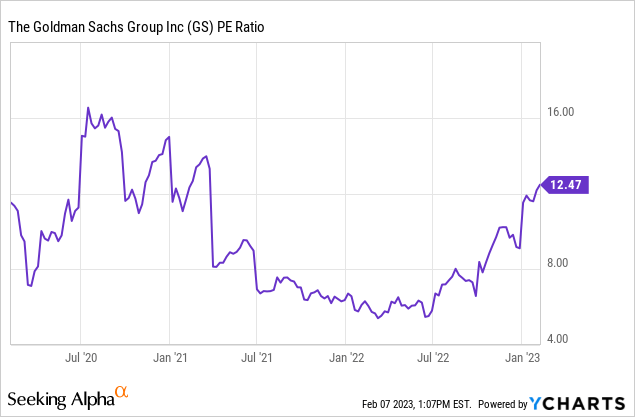

Currently, Goldman trades with a P/E of around 12.5. As you can see, it is highly elevated relative to levels seen in the past three years. The last time its P/E was this high was in early 2021 when rates were basically at zero and the macro environment heavily in Goldman’s favour. It is currently the exact opposite and Goldman is still trading at those P/E levels. Therefore I believe this valuation is highly unsustainable. In my view, Goldman would be correctly valued in the mid-single digits, near the 2022 P/E lows given the amount of difficulty Goldman is facing both internally and externally.

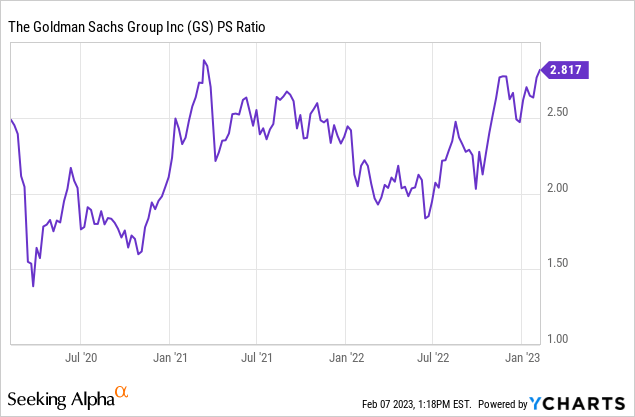

The P/S ratio of Goldman is approximately 2.8, close to a three year high. Like the P/E ratio, the P/S has not been this high since early 2021. Likewise, Goldman is also overvalued in terms of P/S given current conditions. Therefore, I believe Goldman would be much more fairly valued near the 2022 P/S lows of approximately 1.75.

If Goldman’s valuation corrects to a P/E in the mid-single digits and a P/S of around 1.75, with earnings and revenues unlikely to significantly rebound in 2023, Goldman’s stock price will be under extreme pressure in the coming months. Therefore, I believe Goldman’s stock has significant downside.

Risks

A risk to my bear thesis is the direction of rates. If rate hikes were to end more quickly than the Fed anticipates and if rate cuts do indeed occur later this year then Goldman may be a beneficiary. In fact, after Jerome Powell’s remarks during Feb 1st rate hike, markets rallied despite a hawkish stance. The market seemed to have ignored his hawkish statements and seemed to insist that the Fed is wrong about the direction of rates. The market expects one more hike of 25bps in March and then rate cuts starting in September. If the market’s view turns out be correct, then Goldman’s cyclical businesses could potentially make a large comeback later this year. In my view, this could boost Goldman’s earnings and could help it avoid a valuation contraction as discussed above. However, markets have had many failed bear market rallies in the past months and this time may be no different. Therefore, I believe this risk is not likely to occur.

A second risk would be a comeback from Goldman’s consumer business. Even though the business is currently in crisis, their shift in strategy may be beneficial in the longer run. By concentrating on existing customers and using wealth management channels to market its business, Goldman may be able to cuts costs and boost the profitability of this department. Having a slower growing consumer business that is more profitable is better than a faster growing but money-losing consumer business. Therefore, in the long run, Goldman could be rewarded if this shift in strategy proves to be better than sticking with a money-losing strategy. Nonetheless, Marcus is facing many external and internal issues and in my view it will be very difficult for Goldman to turn it around. Therefore, I believe this is a minor risk.

Conclusion

I believe Goldman is a very tough sell in this environment. Its most recent earnings were very bleak. Its traditional investment banking revenues collapsed while Asset & Wealth Management failed to come through as a revenue stabilizer. Meanwhile, Platform Solutions showed growth but is mostly irrelevant due to its insignificant size. In addition to poor earnings, Marcus is facing regulatory scrutiny and is lacking a clear direction as a result of a shift in strategy. The hostile macro environment also does not help Goldman’s cause as the Fed expects more hikes and no cuts in the coming months. Despite all of these negative factors, Goldman’s valuation is still near 2021 highs in terms of the P/E and P/S ratios. Thus, I believe Goldman is currently highly overvalued and is at high risk of a major correction. All things considered, I initiate Goldman Sachs at a Sell rating.

Be the first to comment