Robert Way/iStock Editorial via Getty Images

A Quick Take On Golden Heaven Group Holdings

Golden Heaven Group Holdings (GDHG) has filed to raise an undisclosed amount in an IPO of its ordinary shares, according to an F-1 registration statement.

The firm operates amusement and water parks in southern China.

GDHG’s revenue growth has stalled in the most recent operating period.

I’ll provide an update when we learn more IPO details.

Golden Heaven Overview

Nanping City, China-based Golden Heaven was founded to operate amusement, water parks and related recreational facilities at various locations in the south of China.

Management is headed by Chairman and CEO Ms. Qiong Jin, who has been with the firm since January 2020 and was previously Chairman at Nanping Jinsheng Amusement Management Ltd.

As of March 31, 2022, Golden Heaven has booked fair market value investment of $3 million from investors including Jinzheng Investment Co (Chairman Jin), Qingyu Investment, Hong Kong Greater Power Ventures and others.

Customer Acquisition

The firm advertises in local media, online and through word of mouth in the cities in which it operates.

The company’s parks are located within close distance of a total of 21 million persons in cities in southern China.

Selling expenses as a percentage of total revenue have trended lower as revenues have plateaued, as the figures below indicate:

|

Selling |

Expenses vs. Revenue |

|

Period |

Percentage |

|

Six Mos. Ended March 31, 2022 |

13.9% |

|

FYE September 30, 2021 |

14.5% |

|

FYE September 30, 2020 |

18.4% |

(Source – SEC)

The Selling efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of Selling spend, fell to 0.0x in the most recent reporting period, as shown in the table below:

|

Selling |

Efficiency Rate |

|

Period |

Multiple |

|

Six Mos. Ended March 31, 2022 |

0.0 |

|

FYE September 30, 2021 |

1.9 |

(Source – SEC)

Market & Competition

According to a 2022 market research report by McKinsey & Co, the Chinese market for amusement parks was an estimated $5.6 billion in 2019 and is forecast to reach $12.6 billion by the end of 2025.

This represents a forecast CAGR of 14.4% from 2019 to 2025.

The main drivers for this expected growth are a rise in new entrants from high-quality international businesses that have brought increased visibility to the industry and an increase in urban populations seeking improved recreational opportunities.

However, the ‘zero-COVID’ policies by Chinese regulators have served to reduce industry growth and serve as a source of unpredictability going forward.

Park operators are now beginning to incorporate augmented and virtual reality experiences into park operations, to enhance visitor enjoyment of relevant attractions.

Major competitive or other industry participants include:

-

Walt Disney Co.

-

Universal Studios

-

Haichang Ocean Park

-

Chimelong

-

Fantawild Holdings

-

Overseas Chinese Town Group

-

Shanghai Shendi

-

Sunac China Holdings

-

Others

Financial Performance

The company’s recent financial results can be summarized as follows:

-

Flattening topline revenue growth

-

Dropping gross profit but rising gross margin

-

Increasing operating profit

-

Variable cash flow from operations

Below are relevant financial results derived from the firm’s registration statement:

|

Total Revenue |

||

|

Period |

Total Revenue |

% Variance vs. Prior |

|

Six Mos. Ended March 31, 2022 |

$ 20,756,934 |

0.4% |

|

FYE September 30, 2021 |

$ 38,517,742 |

38.4% |

|

FYE September 30, 2020 |

$ 27,823,960 |

|

|

Gross Profit (Loss) |

||

|

Period |

Gross Profit (Loss) |

% Variance vs. Prior |

|

Six Mos. Ended March 31, 2022 |

$ 14,760,969 |

-1.5% |

|

FYE September 30, 2021 |

$ 26,830,586 |

52.1% |

|

FYE September 30, 2020 |

$ 17,638,625 |

|

|

Gross Margin |

||

|

Period |

Gross Margin |

|

|

Six Mos. Ended March 31, 2022 |

71.11% |

|

|

FYE September 30, 2021 |

69.66% |

|

|

FYE September 30, 2020 |

63.39% |

|

|

Operating Profit (Loss) |

||

|

Period |

Operating Profit (Loss) |

Operating Margin |

|

Six Mos. Ended March 31, 2022 |

$ 10,302,324 |

49.6% |

|

FYE September 30, 2021 |

$ 18,720,222 |

48.6% |

|

FYE September 30, 2020 |

$ 11,101,381 |

39.9% |

|

Comprehensive Income (Loss) |

||

|

Period |

Comprehensive Income (Loss) |

Net Margin |

|

Six Mos. Ended March 31, 2022 |

$ 8,003,413 |

38.6% |

|

FYE September 30, 2021 |

$ 14,868,424 |

71.6% |

|

FYE September 30, 2020 |

$ 8,410,476 |

40.5% |

|

Cash Flow From Operations |

||

|

Period |

Cash Flow From Operations |

|

|

Six Mos. Ended March 31, 2022 |

$ 5,522,508 |

|

|

FYE September 30, 2021 |

$ (4,961,897) |

|

|

FYE September 30, 2020 |

$ 13,702,670 |

|

(Source – SEC)

As of March 31, 2022, Golden Heaven had $10.7 million in cash and $23.4 million in total liabilities.

Free cash flow during the twelve months ended March 31, 2022, was negative ($4.8 million).

IPO Details

Golden Heaven intends to raise an undisclosed amount in gross proceeds from an IPO of its ordinary shares.

No existing shareholders have indicated an interest to purchase shares at the IPO price.

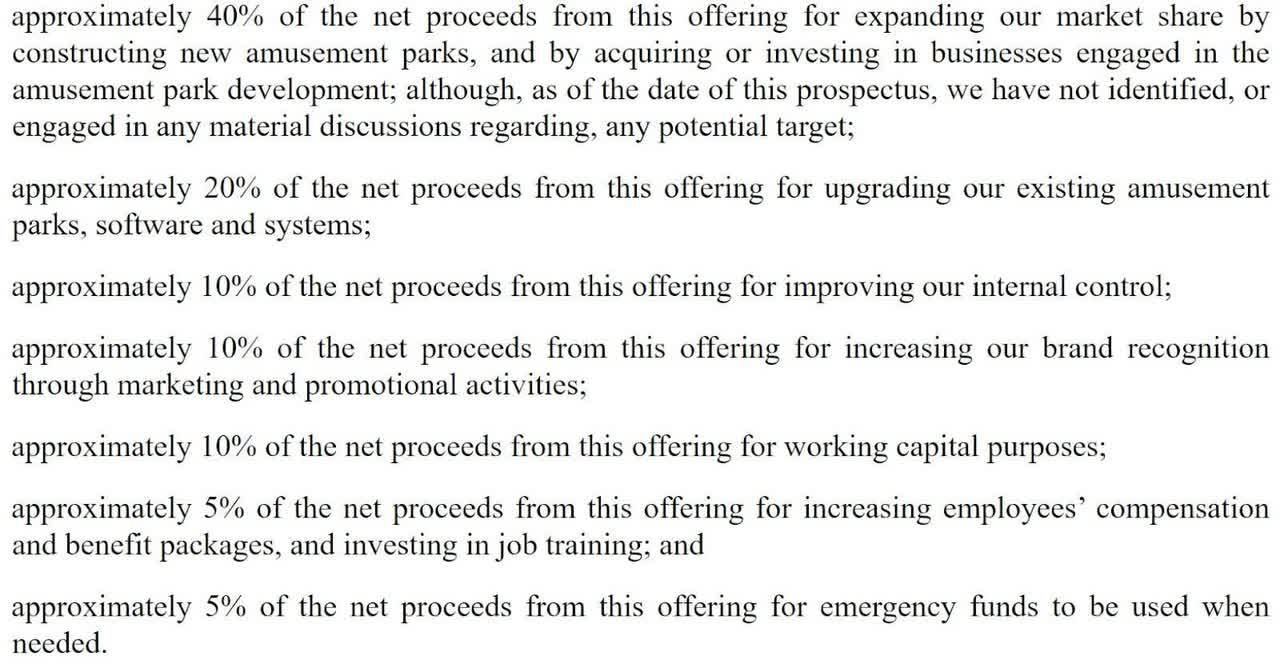

Management says it will use the net proceeds from the IPO as follows:

Company Proposed Use Of Proceeds (SEC)

(Source – SEC)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, the firm is subject to a number of legal proceedings but management says the ‘outstanding payment liabilities do not materially adversely affect the business of the operating entities, or our financial condition and results of operations.’

The sole listed bookrunner of the IPO is Revere Securities.

Commentary About IPO

GDHG is seeking U.S. public capital market investment to fund its expansion plans, including acquisition of additional amusement park assets.

The company’s financials have shown topline revenue has stopped growing, gross profit falling but gross margin rising, operating profit increasing but cash flow from operations fluctuating.

Free cash flow for the twelve months ended March 31, 2022, was negative ($4.8 million).

Selling expenses as a percentage of total revenue have dropped as revenues have flatlined; its selling efficiency multiple fell to 0.0x in the most recent reporting period.

The firm currently plans to pay no dividends and to retain future earnings for reinvestment back into the firm’s growth plans.

The market opportunity for amusement parks in China is substantial and expected to grow at a moderate rate of growth in the coming years, but the firm faces major entity competition.

Like other firms with Chinese operations seeking to tap U.S. markets, the firm operates within a WFOE structure or Wholly Foreign Owned Entity. U.S. investors would only have an interest in an offshore firm with interests in operating subsidiaries, some of which may be located in the PRC. Additionally, restrictions on the transfer of funds between subsidiaries within China may exist.

The recent Chinese government crackdown on IPO company candidates combined with added reporting and disclosure requirements from the U.S. has put a serious damper on Chinese or related IPOs resulting in generally poor post-IPO performance.

Also, a potential significant risk to the company’s outlook is the uncertain future status of Chinese company stocks in relation to the U.S. HFCA act, which requires delisting if the firm’s auditors do not make their working papers available for audit by the PCAOB.

Prospective investors would be well advised to consider the potential implications of specific laws regarding earnings repatriation and changing or unpredictable Chinese regulatory rulings that may affect such companies and U.S. stock listings.

Additionally, post-IPO communications from management of smaller Chinese companies that have become public in the U.S. has been spotty and perfunctory, indicating a lack of interest in shareholder communication, only providing the bare minimum required by the SEC and a generally inadequate approach to keeping shareholders up-to-date about management’s priorities.

Revere Securities is the sole underwriter and there is no data on its IPO involvement over the last 12-month period.

The primary risk to the company’s outlook as a public company is the zero-COVID policy by Chinese authorities that can shut down its park operations with essentially no advance notice.

When we learn more information about the IPO, I’ll provide a final opinion.

Expected IPO Pricing Date: To be announced.

Be the first to comment