Igor Kutyaev/iStock via Getty Images

With global markets close to post-Ukraine war highs, we remain neutral on global equities. There seems limited scope for further upward gains in the short term in an environment of increasingly hawkish rhetoric from the US Federal Reserve and ECB, while valuations for US equities which account for approximately 50% of global market capitalisation remain well above long-run average levels.

This hawkish turn in central bank policy is something of a surprise to us, given the resolutely dovish bias of both institutions over the past decade. However, with at least one US rate increase now expected at each FOMC meeting for the rest of the year, the US Fed is serious about tightening financial conditions to squeeze out inflation.

In the UK, the Bank of England is the outlier for now, raising interest rates by a further 0.25% but alluding to the possibility of an easier trajectory of rate increases as growth slows due to the economic impact of the war in Ukraine.

Both the US Fed and ECB are now in something of a self-imposed catch-up mode, having spent much of the prior 12 months asserting that the surge in inflation was transitory. Yet the “transitory” inflation argument has been cast aside during Q122. In his most recent press comments, Fed Chair Powell highlighted his determination act “expeditiously” to tighten policy to avoid embedding higher inflation expectations within the economy. The recent war-induced rise in energy and food prices is clearly unhelpful for the Fed’s objective. Headline inflation will be higher and above central bank targets for longer, compared to expectations at the start of 2022.

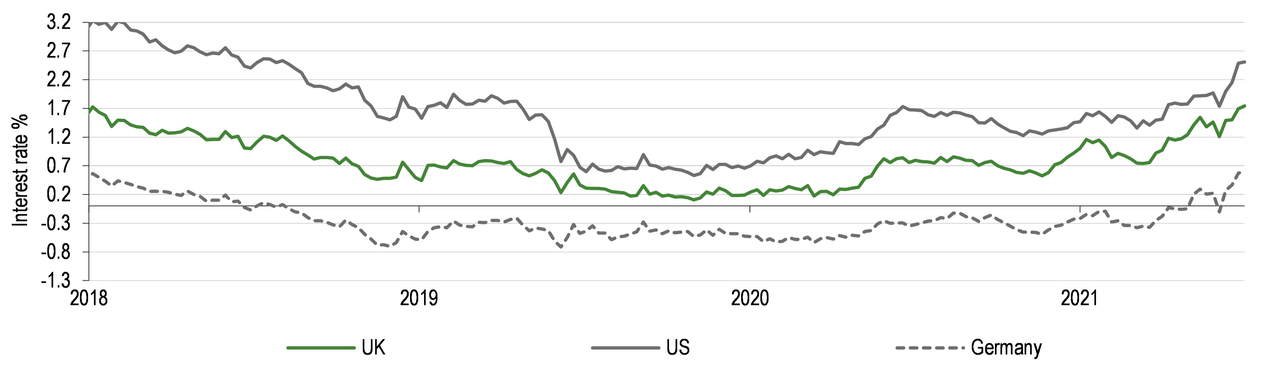

Following this turn in central bank policy, long-term government bond yields have been rising rapidly, Exhibit 1. Despite the outbreak of war in Ukraine, which would normally be expected to be positive for government bonds as investors seek safe havens, the pace of increases in global bond yields has only accelerated. We note the US 10y yield is now above levels prevailing in the pre-COVID era.

Exhibit 1: Global government bond yields rising as US Fed and ECB switch to hawkish track

Refinitiv

Yet the implicit forward guidance in the dot-plots contained within the US Fed’s Summary of Economic Projections (SEP) that US rates will rise monotonically from current rates for the remainder of the year is only part of the story, in our view. Judging from the yield curve, Exhibit 2, investors do not expect the US Fed to be able to raise rates as quickly as policymakers currently indicate and we would concur with this assessment.

The recent increase in food and energy costs worldwide is likely to act as a significant drag on consumer-driven economies. Developed market GDP growth was in any case set to decline during H222 as COVID-19 base effects fell out of the data. We note the spread between US 2-year and 10-year rates is already close to zero, leaving the yield curve perilously close to inversion, which often signals a recession ahead. The combination of rapidly rising interest rates and a slowing economy at a time of surging energy and food prices is hardly an ideal environment for equities, in our view.

Exhibit 2: US 2y-10y yield spread close to zero with Fed tightening cycle only just underway

Refinitiv

For now, global earnings estimates are still rising. Led by the energy and resources sectors which have seen the largest forecast earnings upgrades following the implementation of sanctions on Russia, this is likely to be a one-off benefit concentrated in these few sectors. It also represents input cost pressure for the remainder of the market and strains consumer budgets.

Exhibit 3: Global earnings estimates remain on rising track, led by energy

Refinitiv

Russia appears set to remain isolated

At present, almost all scenarios for the outcome of the war in Ukraine appear to leave Russia largely isolated from the world economy over the medium-term and possibly until there has been change of regime. As a result, for many investors, Russia will remain off-limits and the substantial discount for Russian assets is likely to persist. Given the entrenched nature of Putin’s administration, any handover of power may take some time as the only legitimate mechanism for change is internal pressure within Russia. Past experience suggests a relatively long period of lowered living standards may be required to convince Russian voters of the need to end sanctions and reintegrate into the global economy. There is also the possibility is that the popular opinion instead switches to a siege mentality, centred on the current leadership.

Before the war, Putin’s regime was an irritant with an expansive hybrid foreign policy spanning military operations, influence campaigns and assassinations of opponents on foreign soil. Nevertheless, Germany appeared reluctant to take the European lead on the kind of sanctions which would have had a material effect on the Russian economy.

As the Russian regime has now revealed its willingness to engage in such a war, economic sanctions are likely to be long-lived, regardless of a supposed ‘win’, loss, or stalemate on the ground in Ukraine. In some respects, the only remaining uncertainty is to what extent China or India chooses to exploit the situation for its own economic and political advantage.

We, therefore, expect oil and food prices are likely to remain elevated for the duration of 2022 which will maintain upward pressure on headline measures of inflation. We are however reminded of the oil market’s aphorism that the cure for high oil prices is high oil prices, which similarly applies to agricultural commodities.

Both oil and wheat prices are strongly in backwardation, meaning that prices for delivery in the short term are much higher than prices for deliveries further into the future. Brent crude oil for delivery in 2029 was moving higher prior to the outbreak of war but is little changed at only US$70 since mid-February. There is a similar story in wheat futures where European prices for 2024 are up only 10% compared to spot prices which have risen by over 40% during the same period.

We expect governments to move swiftly to reconfigure supply chains to avoid major disruption to either energy or food supplies as Russian volumes are reduced or eliminated entirely. We note the recent agreement between the US and EU for LNG supplies and early signs of a more favourable oil and gas investment climate around the UK. As hydrocarbon-based energy becomes more expensive, we also expect further investment in renewable energy, which will permanently displace fossil-based fuel.

We also note the EU has proposed relaxing environmental requirements for farmers to set aside land, increasing the acreage available for combinable crops to compensate for both the loss of acreage and likely difficulties exporting grain from Russia and Ukraine. Supply chain, energy and agricultural themes are likely to benefit from positive earnings momentum in the short term. Nevertheless, investors should be careful not overestimate the duration of the uplift from an essentially transient phenomenon which is likely to become played out within the next 12 months.

Still neutral on global equities

We maintain a neutral outlook on global equities with some significant caveats following a hawkish turn in monetary policy in the US and eurozone. Rising US interest rates and tighter than expected monetary policy in the eurozone is likely to prolong the period of underperformance for the most highly valued segments of the equity market whether on a regional and sector basis. These sectors currently account for an unusually large percentage of headline market indices.

Instead, we continue to prefer traditional sectors such as banks, insurers, defence, energy and telecoms over still highly valued technology at this time. We highlight the defence sector as commitments to increased defence spending are likely to outlast any ceasefire in Ukraine. 10-year government bond yields are likely to continue to move higher in the short run with increases in interest rates, but the flattening of the yield curve suggests that the point where long-term rates stop rising in anticipation of growth slowdown is approaching rapidly.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment