David Taljat

The Context

The past few months have been tough for all of us. Even if the market has treated you well with some winning bets (e.g., tanker stocks), it’s more than likely that your more conventional picks have been in the red.

Unfortunately, the underlying macroeconomic and geopolitical factors that have been stressing the capital markets appear to only be worsening. Thus, in the current market environment, sensible investors might be looking for the following three traits before allocating money to a stock:

- A rock-solid medium-term path of sustainable and growing profits,

- Strong capital returns that increase one’s visibility of a stock’s total return potential,

- and a wide margin of safety against a potential/further valuation multiple compression.

Even the highest-quality companies out there fail to satisfy these conditions in the current market setup. For this reason, we need to turn elsewhere to less conventional options.

I have personally sought shelter amongst containership and container lessors, as they are currently featuring robust cash flow visibility over the medium term and accelerating dividends/buybacks while trading at ridiculously cheap valuations – thus satisfying my three requirements. In my previous two reports, I dived deeper into Danaos (DAC) and Triton International (TRTN), explaining why their risk/reward cases are too good to be missed.

In this one, I want to revisit my take on Global Ship Leases (NYSE:GSL), whose investment case has dramatically improved since I last covered the stock. And even better for current buyers, shares have also become cheaper too. I am also going to suggest how investors can combine the common stock’s robust 9.5% yield along with its 8.7%-yielding preferred shares to form the ultimate high-income combo.

So let’s split this piece into the following parts:

- Why GSL enjoys tremendous earnings growth visibility,

- Why GSL’s capital returns, along with the current valuation, offer a wide margin of safety and massive upside.

- Why combining the common stock with the preferred shares can form the ultimate high-income combo.

Let’s go!

GSL’s Forward Cash Flow Visibility Just Got Even Better

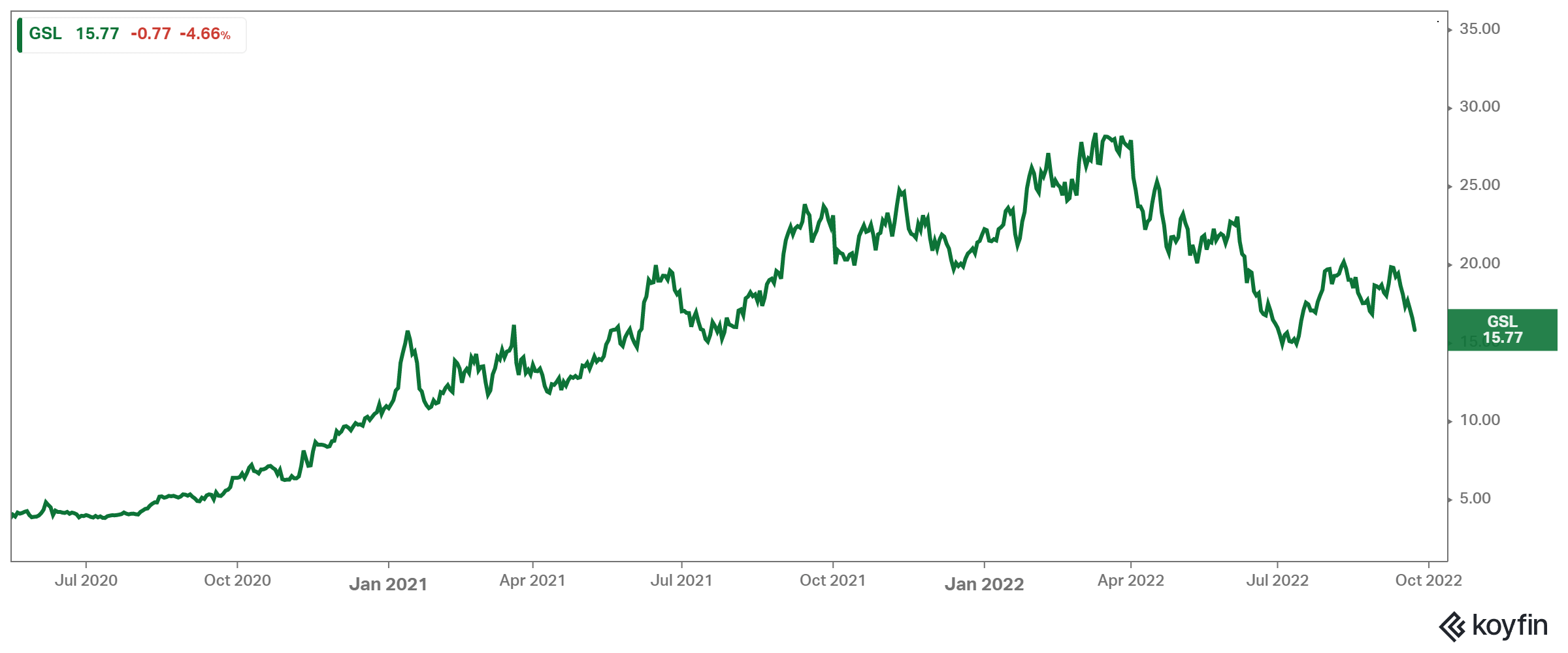

If one unfamiliar with GSL were to see its stock price chart, they would assume that the company’s performance enjoyed tremendous momentum last year but that this momentum has likely started to fade out.

GSL’s stock price (Koyfin)

The truth, however, is that most investors familiar with the stock know that GSL’s earnings are, in fact, set to grow meaningfully in the coming quarters. What the market is, unfortunately, looking at when trading GSL is the cratering rates amongst containerships.

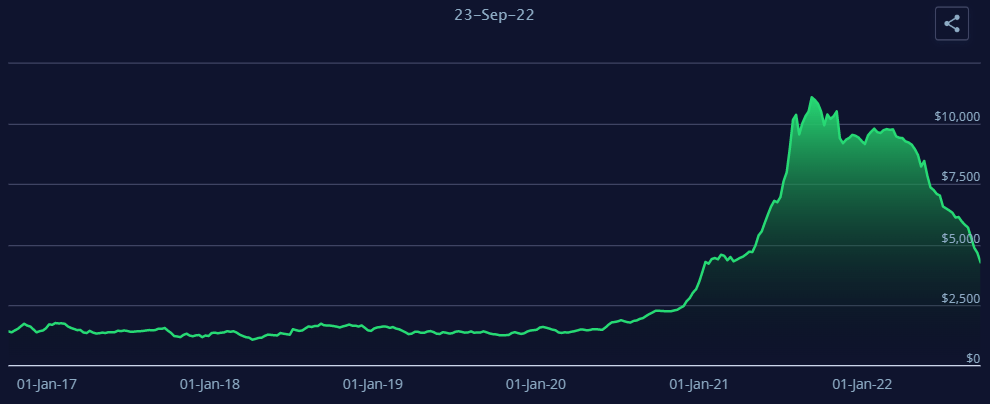

Global Container Freight Index (fbx.freightos.com)

Firstly, yes, containership liners (those who operate the vessels, like ZIM Integrated Shipping Services Ltd. (ZIM)) are indeed experiencing declining rates. However, even at their current levels, these are still very profitable rates for liners, as they are still more than double their historical levels.

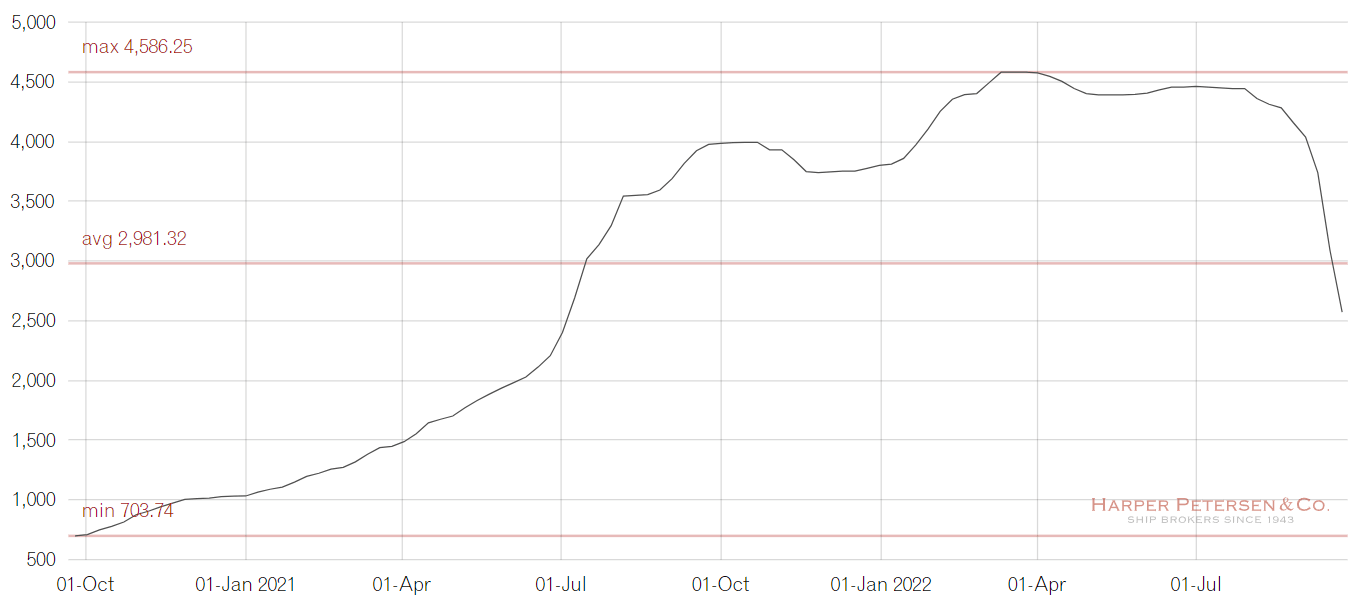

Despite GSL being a containership lessor and not an operator, the stock is being treated by the market alike. But wait, aren’t leasing rates also declining?

HARPER PETERSEN Charter Rates Index (harperpetersen.com/harpex)

Yes, they are. However, i) as The HARPEX index displays, they remain well above their historical levels, ii) GSL has already locked in multi-year contracts, which means that even if rates plummet further, its forthcoming cash flows won’t be affected, iii) the company recently announced even further forward-looking charter extensions that are significantly higher than its already-high ones.

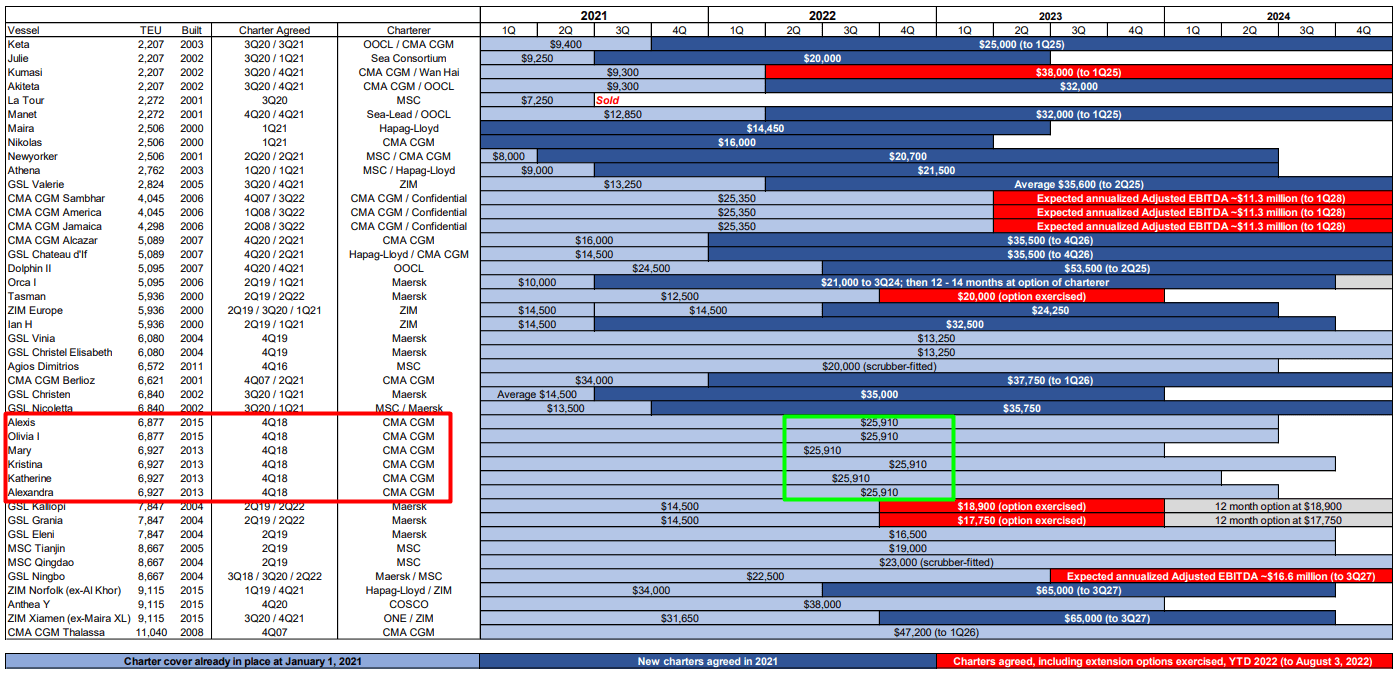

To that last point, late last month, GSL announced a huge extension for six ECO 6,900 TEU modern ships with Hapag-Lloyd. These contracts won’t even start producing cash flows until late 2023 to late 2024, securing predictable revenues for five years through 2029. These are the six vessels I have boxed in red.

GSL’s Core Feet Employment (Q2 Investor Presentation) (www.globalshiplease.com/investors/events-presentations)

But here’s the best part, these new contracts have a time-charter equivalent (“TCE”) rate of about $43K per day. For perspective, the previous rates stand at $25.910/day. That’s a 66% increase that runs through 2029. That’s incredible for GSL to be able to sustain and even further grow its already record earnings.

From another standpoint, just this deal, which concerns just six of GSL’s vessels, added a total Adjusted EBITDA of around $393 on its backlog, which is currently worth as much as 67% of GSL’s market cap (but more on the undervaluation later).

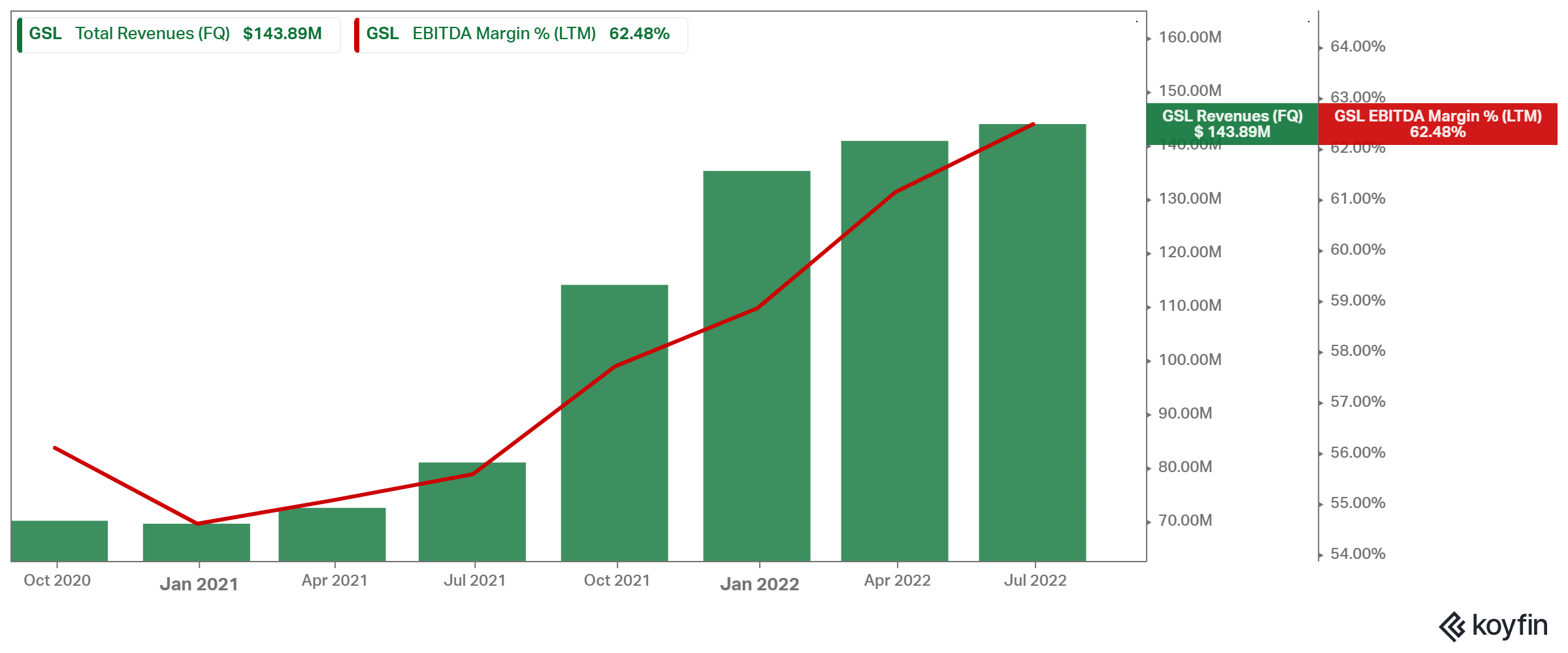

The point is we already know that the company will predictably grow its revenues sequentially over the next several quarters. Accordingly, its net income should grow at an ever faster pace amid expanding EBITDA margins. This is due to relatively stable operating expenses on the corporate level against higher revenues, as well as balance sheet optimization actions such as the recent redemption of its principal senior notes (i.e., reducing expensive debt).

Revenues and EBITDA margin (Koyfin)

On a per-share basis, earnings growth should be even more accretive as the company is expected to ramp up its share repurchase program.

Capital Returns/Valuation/Upside

Speaking of GSL’s stock repurchases, no extra shares have been repurchased since when the company repurchased an additional 184.6k shares at an average price of $26.66/share. However, with all that cash coming in over the next several quarters, this is the company’s best avenue for shareholder value creation, considering the stock’s massive discount to NAV.

To provide some perspective regarding how cheap the stock is, GSL is forecasted to deliver an EPS of $7.48 for the year. This is a rather conservative estimate. GSL has already posted an EPS of $3.75 in H1-2022, and we know that EPS is going to be higher in H2-2022 because several new charter renewals were/are scheduled to kick in between these two periods.

GSL’s Consensus EPS Estimates (Seeking Alpha)

But regardless of whether EPS for the year comes in at $7.50 or, say, $8.00, the company is basically positioned to generate EPS in fiscal 2022 and fiscal 2023 that will exceed the current stock price. This, combined with the excellent (and recently further enhanced) cash flow visibility that the company’s medium-term charters offer, cements that GSL is dramatically underpriced.

If we revise the company’s balance sheet book value for the increased value of vessels in the current trading environment and discount its forward charter backlog, we calculate that the company’s NAV/share should be somewhere between $38 and $45. Accordingly, GSL is currently trading at a 59% discount to NAV at the minimum.

This goes back to our previous point regarding why buybacks would be the most beneficial pathway for shareholders moving forward, as well as why the stock offers a great margin of safety against the risk of further valuation compression. And also it highlights the massive potential upside current shareholders face both from a return towards NAV, especially with such massive predictable cash flows over the medium term, and from the possible buybacks at a steep discount here.

And all this is on top of GSL’s hefty 9.5% dividend yield. How sustainable is the common dividend? Even if we assume an EPS of $7.50 for the year, the payout ratio stands at 20%. Even if the dividend-per-share were to stop growing any further, we know that the payout ratio will only improve in the coming years due to higher leasing rates kicking in over time, as well as a potentially lower share count. It could easily drop to 15% next year.

Thus, I don’t see how the massive dividend is threatened by 2029. The most recent lease renewals on just six ships could alone cover the dividend through 2029, even if the share count were to not decline ($393 million of adjusted EBITDA added over five years against $52 million in annual common stock dividends times 7 years = $364 million.) For this reason, it would not be far-fetched to say that one who buys the stock at its current levels could recoup their investment over the next decade through the underlying dividend alone.

How To Build The Ultimate Income High-Income Setup

Okay, so the common dividend and its 9.5% yield can be relied upon, and the stock itself offers massive upside potential, but how can one set up an even more secure income-oriented investment case (as if the common stock’s case is not good enough already)?

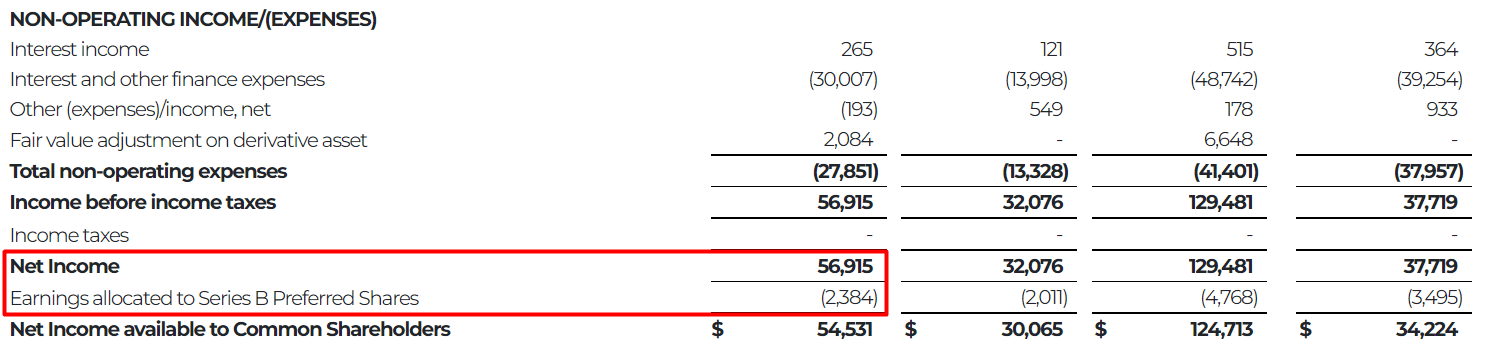

Well, GSL’s preferred shares (NYSE:GSL.PB) are currently yielding 8.7%. If the 20% payout ratio on the common dividend sounds comfortable, then wait till you hear that the preferred dividend is covered by nearly 24 times the company’s net income (i.e., a payout ratio of 3.9%), and remember that we know net income will increase further moving forward.

Preferred Dividend Coverage (GSL’s Q2 earnings report)

This, combined with the cumulative nature of the preferred shares, makes the 8.7% yield entirely insured. It is reckless to talk about “assurance” when it comes to investing, but these are the facts. The preferred dividend should remain very, very well-covered even if the company’s earnings were to crater post-2030.

Could the company redeem its preferred shares? After all, it redeemed its 2024 Senior Notes back in April. Yes, it’s possible. However, it’s nearly impossible to lose money from a redemption here since the preferred shares are not really trading at a premium at their current price of $25.17 (a 0.7% premium), and even then, any accrued dividends by redemption will make up for it.

Further, while I don’t remember which earnings call it was, I distinctly remember GSL’s management mentioning that they like having the preferred stock outstanding as a useful and flexible financing vehicle. This is also confirmed by the occasional preferred stock issuances over time. Thus, the preferred should remain afloat, with its massive yield out there to be grabbed.

Accordingly, besides the common shares alone offering a very compelling investment case, one can build the ultimate high-income combo if combined with the preferred.

Be the first to comment