EzumeImages/iStock via Getty Images

GBT

Does the company have a short-range or long-range outlook in regard to profits? – Phillip Fisher

In biotech investing, it is important that you focus on a stock’s growth cycle. That is to say, a biotech company commences its therapeutic innovation with either in-house development or the in-licensing of a new drug. The medicine typically goes through preclinical and then advances from Phase 1 to 3 clinical investigations. If all goes well, the drug would gain marketing authorization to enter the commercialization phase.

Interestingly, you tend to get the most money by investing in a company before it gains an approved medicine. In the ensuing months after approval, the stock usually gets a haircut. Now, if the medicine can gain market traction, the shares would then embark on a vigorous rally to surpass their former high.

That being said, a stock illustrating the aforesaid phenomenon is Global Blood Therapeutics, Inc. (NASDAQ:GBT). Subsequent to Oxbryta (voxelotor) approval, GBT shares tumbled substantially. However, the stock is rebounding in the past six months as Oxbryta sales are gaining traction. Meanwhile, GBT is brewing a series of catalysts that can galvanize the stock to a new high. In this article, I’ll feature a fundamental analysis of GBT and share with you my expectation of this grower.

StockCharts

About The Company

As usual, I’ll deliver a brief corporate overview for new investors. If you are familiar with the firm, I suggest that you skip to the subsequent section. Headquartered in San Francisco, California, GBT is focused on the development and commercialization of novel medicines to serve the unmet needs in the debilitating blood disorder coined sickle cell disease (“SCD”).

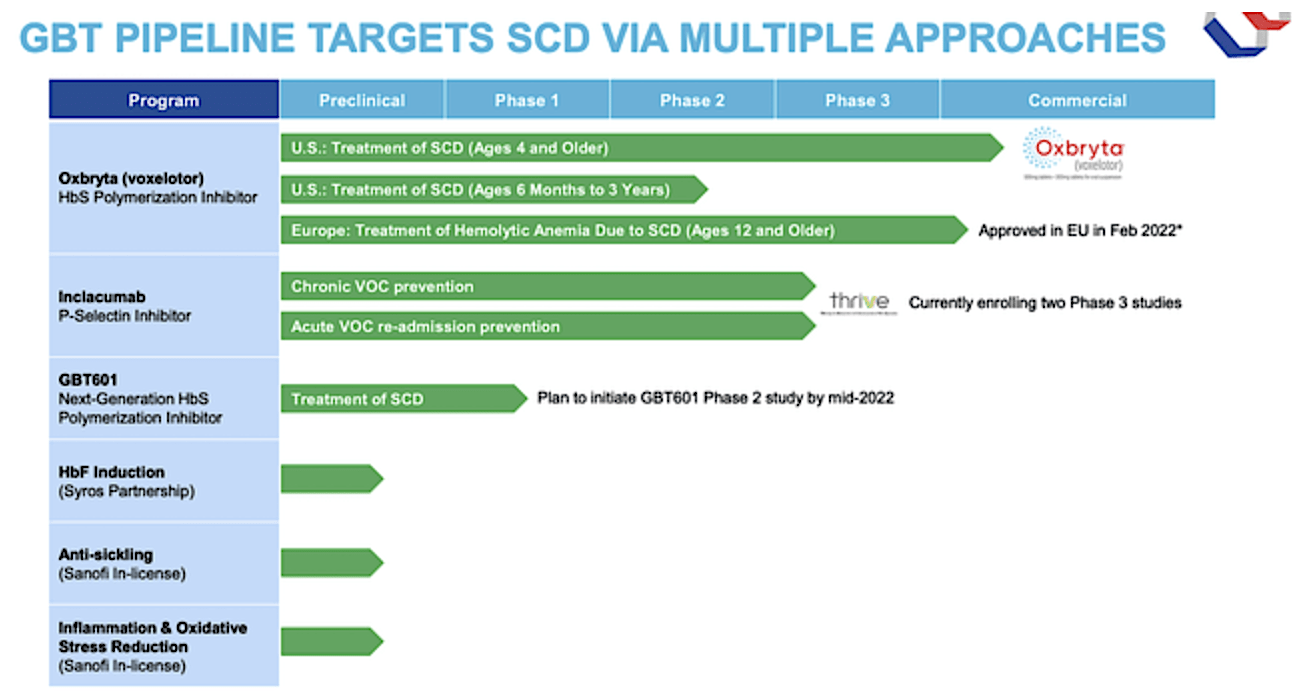

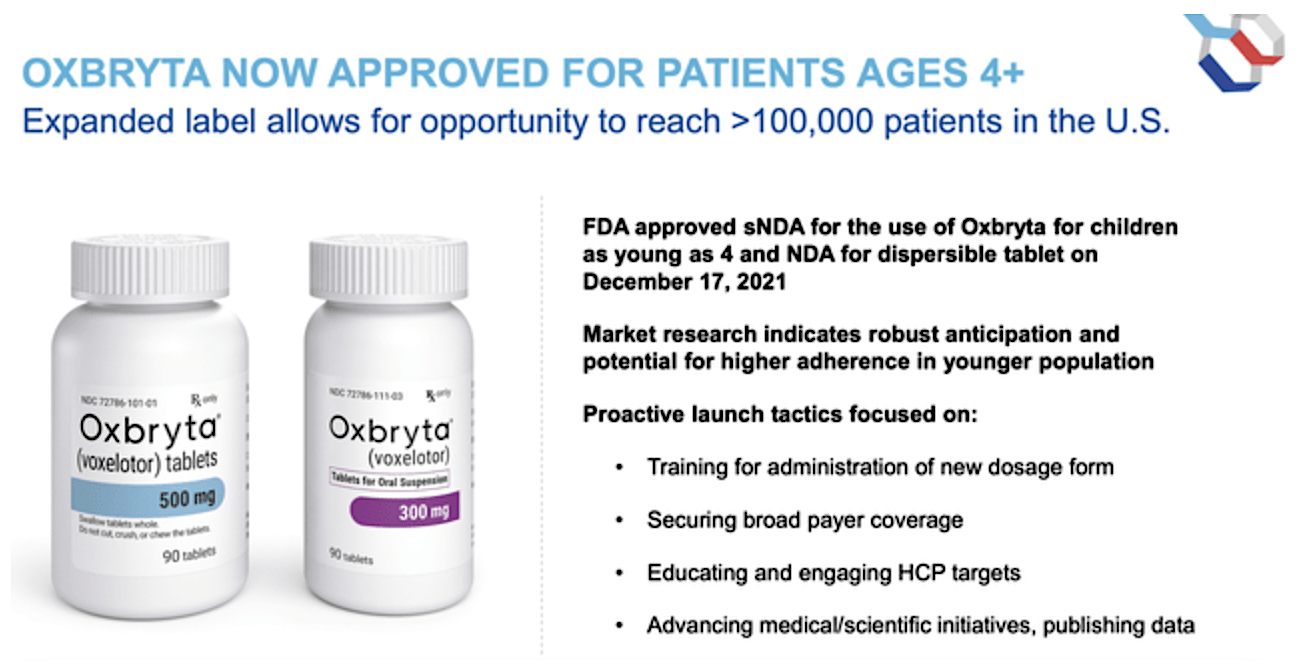

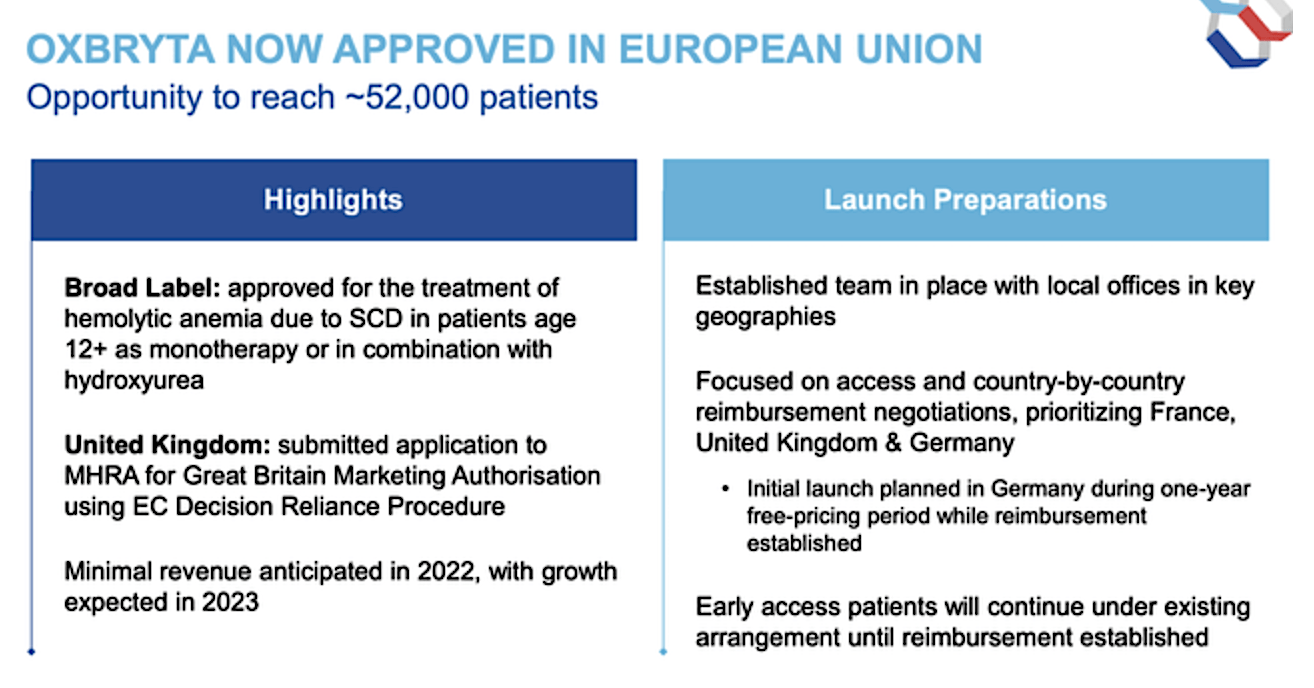

As depicted in the pipeline below, GBT already has launched Oxbryta in the U.S. for adults suffering from SCD. Interestingly, the company gained an expanded Oxbryta label to treat pediatric patients (i.e., kids ages 4-11 years old). In February 2022, GBT also received Oxbryta’s marketing authorization in the European Union (the “EU”).

GBT

Sickle Cell Disease Opportunity

As a devastating condition that shortened the patient’s life by nearly three decades, SCD is a major health concern, imposing a significant economic burden. Afflicting millions of people worldwide, SCD usually hits African and Hispanic descendants. In an oxygen-deprivation state (such as being sick), SCD causes a deformation of the oxygen-carrying protein in the blood coined hemoglobin (i.e., Hb). As the deformation builds up, it causes the red blood cells (“RBC”) to clump up, which lead to a blockage of blood vessels and consequently a painful vaso-occlusive crisis (“VOC”).

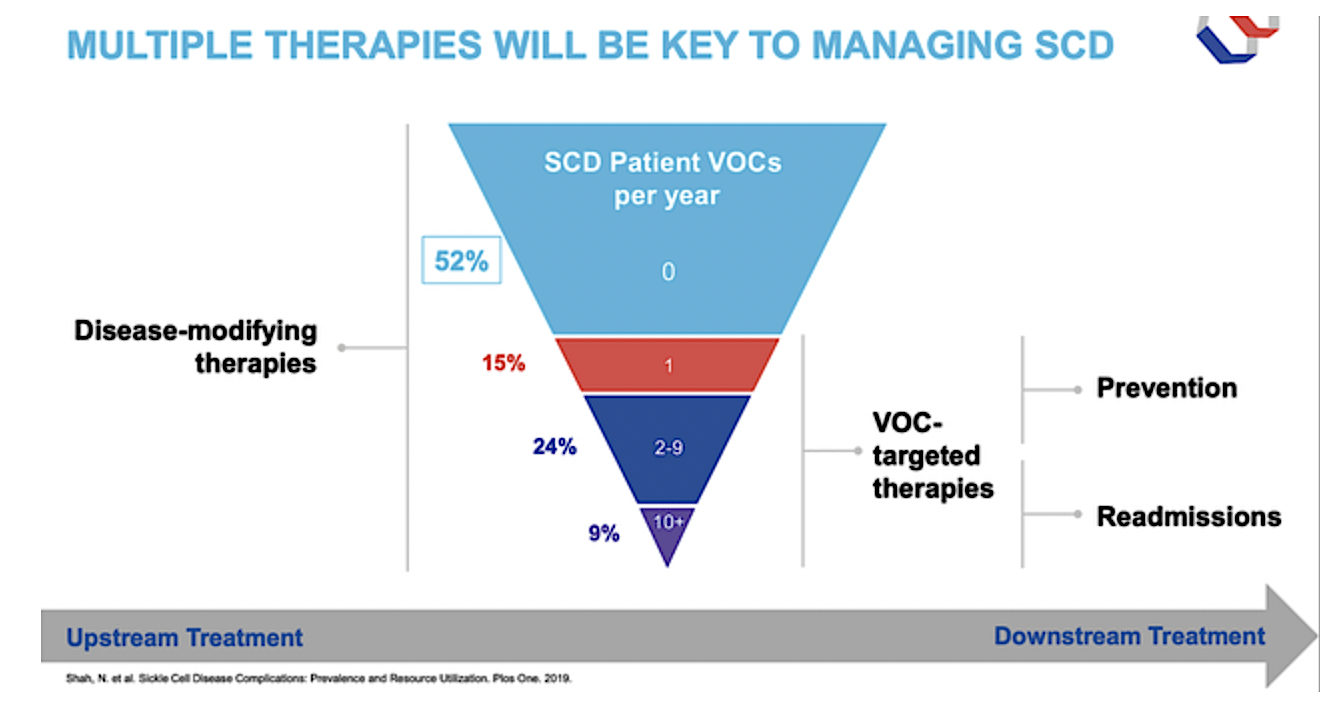

Viewing the figure below, you can see that the upstream treatment is to change the disease course through disease-modifying therapies (i.e., hydroxyurea or Oxbryta). Specifically, Oxbryta increases the Hb level and reduces the sickling/breaking down of RBCs (i.e., the underlying culprit of VOCs and other long-term SCD complications). That aside, you have drugs to prevent VOCs from occurring. Thus far, there isn’t much innovation in this space, which heightened the demand for novel treatments like Oxbryta and others of GBT’s medicines (i.e., inclacumab, GBT601, etc.).

GBT

Oxbryta Commercialization Progress

As you can see, launch progress is an extremely important measure of your investment success. After all, it determines whether your stock would continue to appreciate in the long term. That being said, you should check up on Oxbryta’s commercialization status.

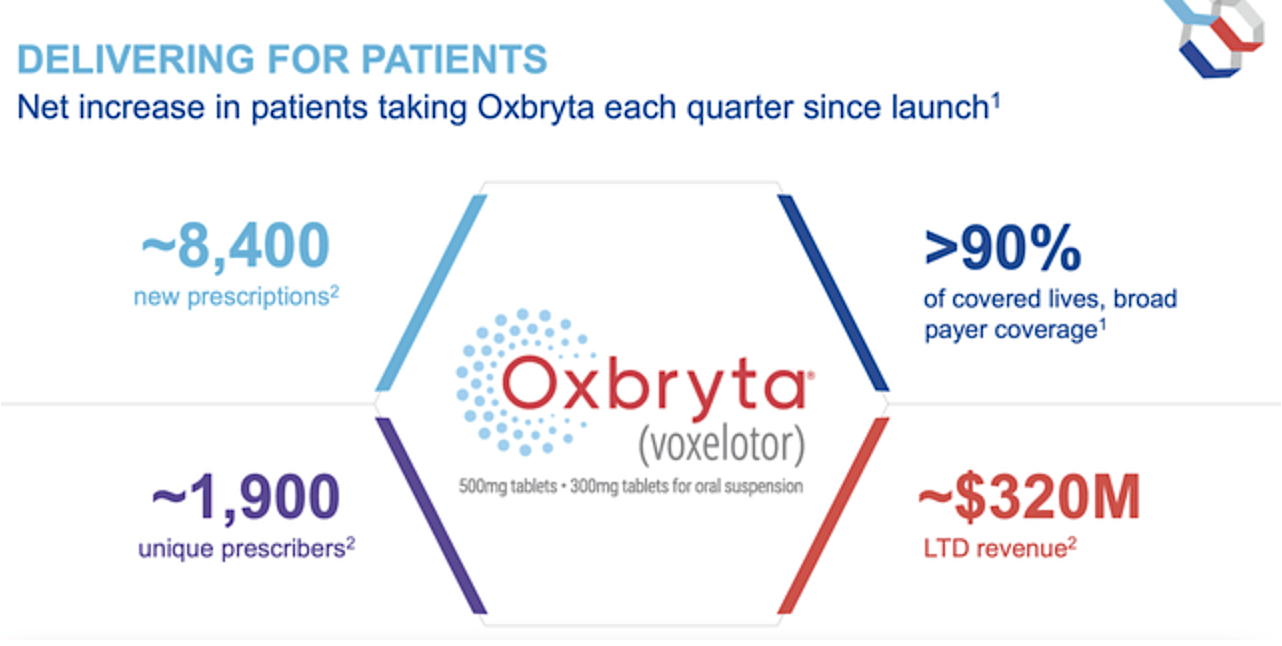

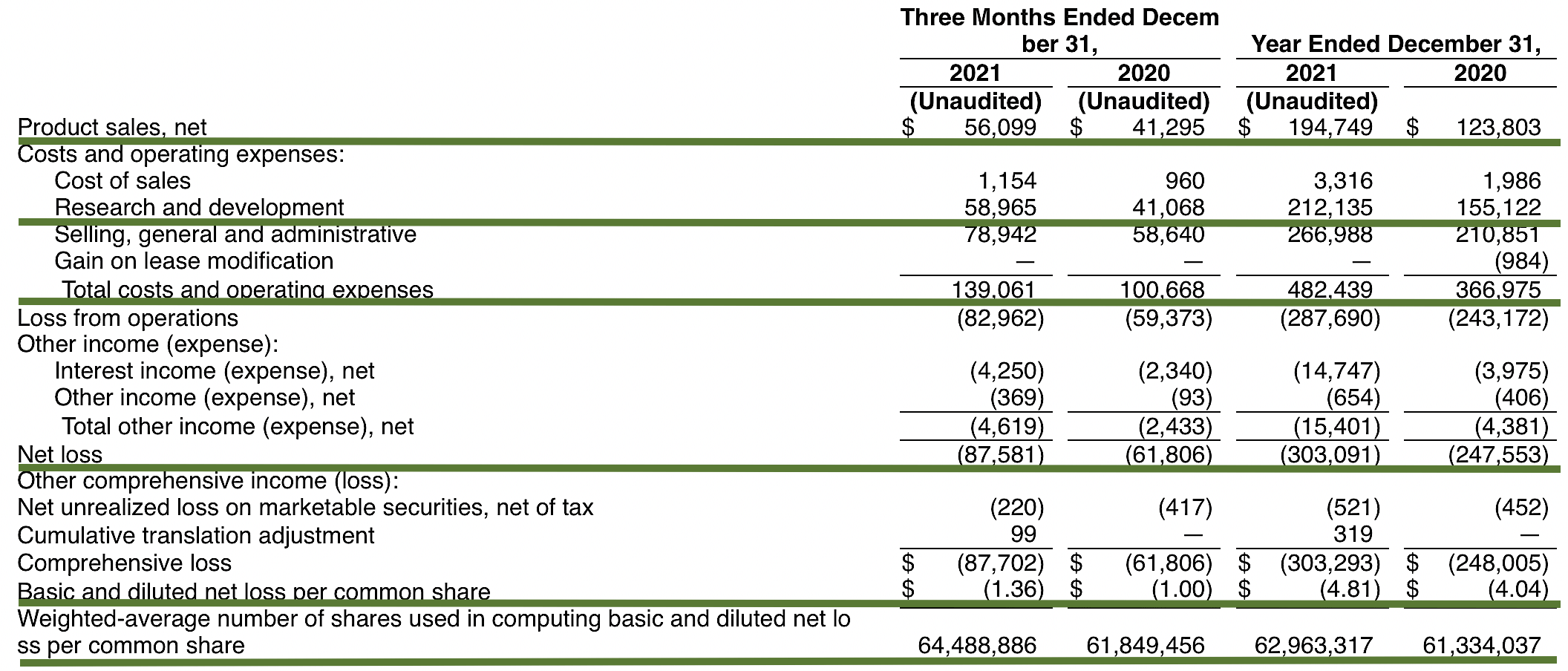

As you may know, Oxbryta has been FDA-approved since November 2019. In the past two-plus years, sales have steadily increased. In 4Q2022, Oxbryta procured $56.1M in sales and thereby represents a 36% year-over-year (YOY) increase. On a sequential basis, sales growth logged in at 8% due to high patient demand. Now Fiscal 2021 generated $194.7M in sales, which is a 57% YOY improvement.

Since its launch to date (LTD), Oxbryta has garnered roughly $320M while reaching 1.9K unique prescribers. Amid the pandemic, the drug still enjoyed 8.4K new prescription growth this quarter. As you can imagine, sales could be picking up robustly in the next few quarters as COVID is abating.

GBT

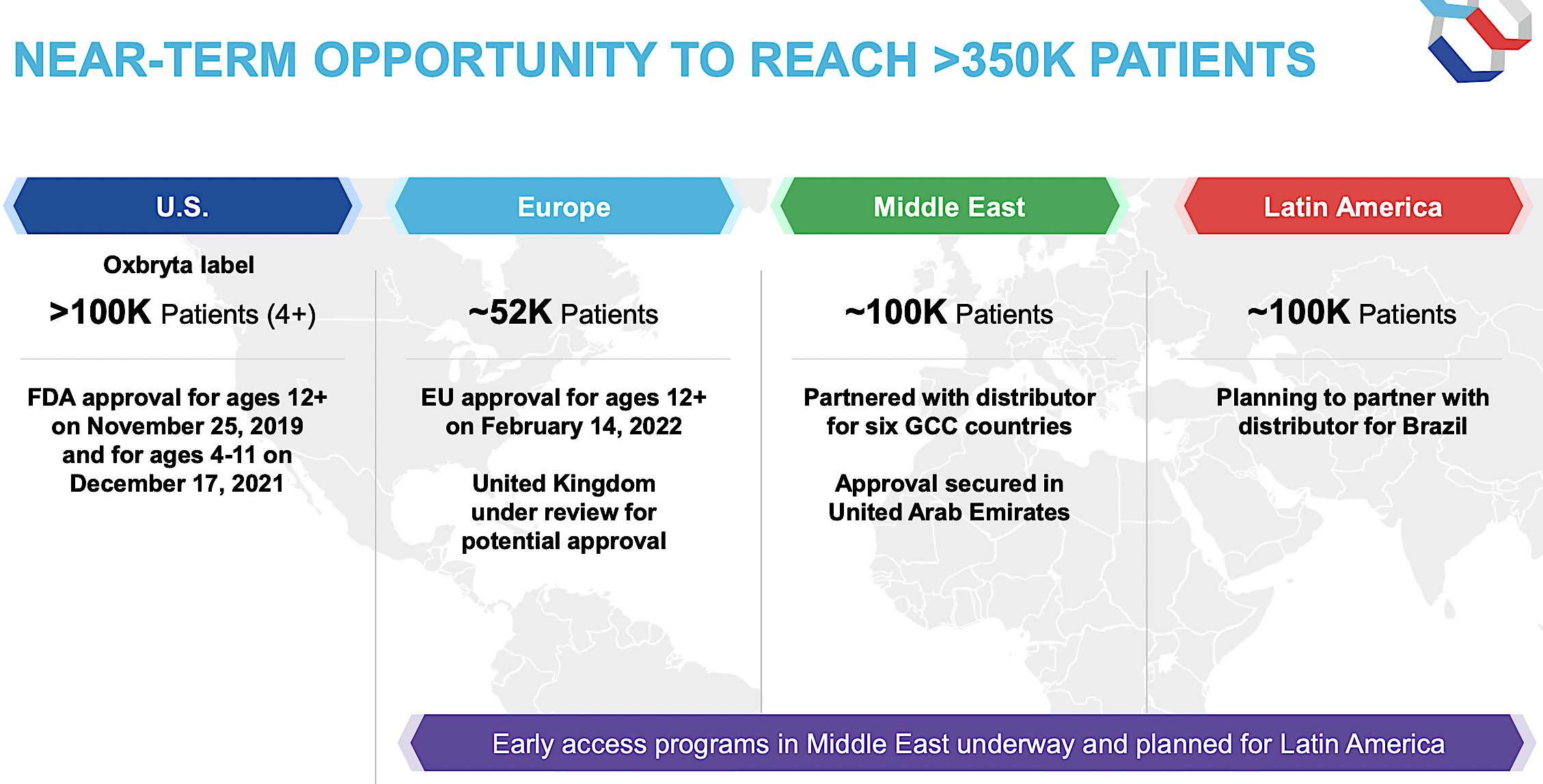

Asides from COVID, there are other crucial catalysts powering further growth. As you know, the first is the recent U.S. FDA approval of Oxbryta for kids. Second is the Oxbryta approval in the EU for patients 12 years and older. You can also expect good results from the marketing review in the UK. Beyond that, launch activities in the Middle East and Latin America are brewing. Taken all together, you can anticipate stronger sales growth going forward.

Pediatric Approval Galvanize Sales Growth

Shifting gears, let us take a closer look at the pertinent growth catalysts to get a clearer picture of where Oxbryta sales are heading. Of the various factors mentioned, you can project that the U.S. pediatric approval will deliver the most bang for the bucks later this year and beyond.

That is to say, this label expansion would enable Oxbryta to reach an additional 100K pediatric patients in the U.S. suffering from SCD. With higher compliance in kids, I believe that Oxbryta sales should be more than double that of the adult population.

GBT

Like an army poised for conquest, GBT already set up the sales/marketing infrastructure to power its aggressive expansion to serve kids. The company leverages traditional sales/marketing along with the digital revolution. As to market potential, you’re looking at 17 key states having 85% of all adults and kids (4 years or older) with SCD. It’s likely that those states have the highest population of Blacks and Hispanics. Now that figure is interesting, because GBT already has a sales/marketing presence in those 17 areas. With approval, the company only has to expand its footprint into the pediatric population.

Leaning on 10 medical science liaisons (“MSLs”) and 55 sickle cell drug specialists, GBT focuses its marketing efforts on 4.7K docs. While that is a significant number of reps and sales specialists, I believe that GBT needs to boost its sales professionals. The more reps the company has, the more aggressive the launch. Nevertheless, the existing statistics are encouraging.

GBT

Upcoming Launch In the European Market

In February, Oxbryta gained marketing authorization in the EU as the first sickle hemoglobin polymerization inhibitor here. The company also received a positive opinion from Great Britain that foretells upcoming approvals. If you are unaware, Britain is not a member of the EU post-BREXIT. Of note, you should not expect any significant revenues in that market this year. After all, GBT has only set up initial launch initiatives.

GBT

Long-Term Growth Strategy

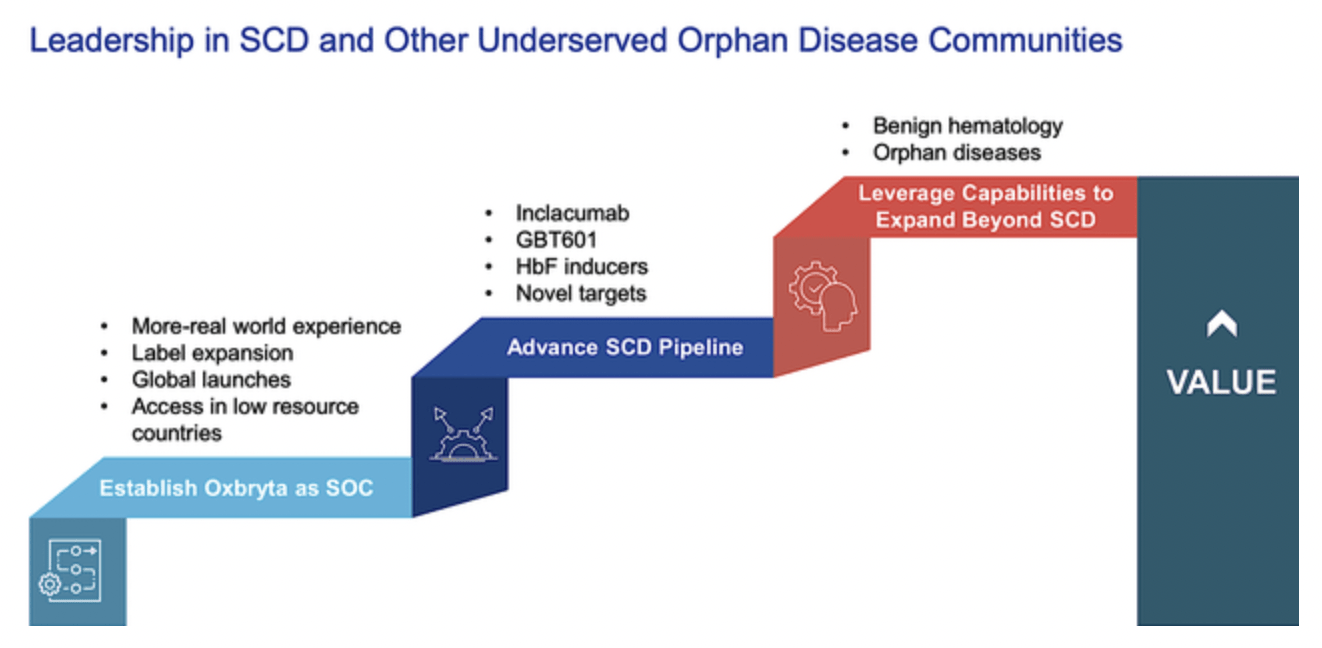

In the long view, GBT is building its pipeline and expanding its innovation infrastructure to power growth. Looking at the figure below, you can see that the company is unlocking value in the next generation of drugs such as GBT601 and other novel SCD treatments like inclacumab.

With more success from SCD, the firm is poised to expand into other orphan disease markets. As you can imagine, orphan disease represents a profitable investment segment. Despite the small number of cases, orphan diseases warrant a premium reimbursement to ensure that innovation efforts are rewarded.

GBT

Competitor Landscape

Regarding competition, Oxbryta faces traditional medicines such as hydroxyureas (i.e., Droxia, Hydrea, Siklos) and supportive care. Though effective, hydroxyurea increases the patient’s risk of infection. The FDA also recently approved L-glutamine oral powder (Endari) which reduces the number of VOCs. There is also crizanlizumab (Adakveo) to lower complications. That aside, there are novel treatment modalities like gene therapies in development. Despite the competition, Oxbryta is a novel and highly efficacious drug. As such, it should trump competition to take the most dominant shares over time.

Financial Assessment

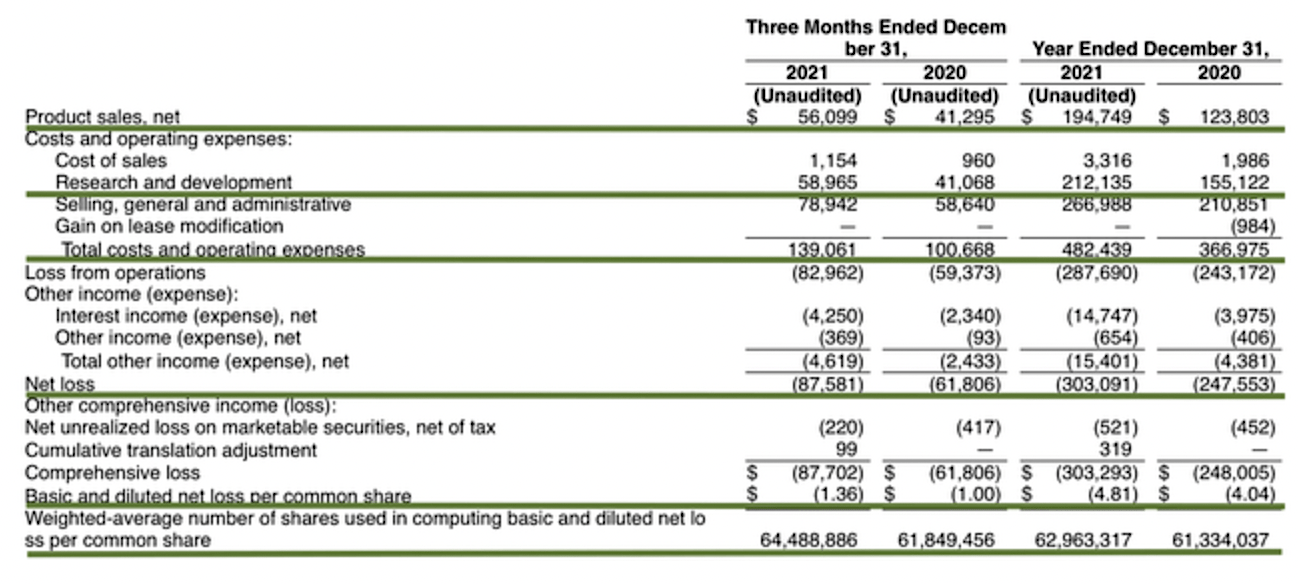

Just as you would get an annual physical for your well-being, it’s important to check up on the financial health of your stock. For instance, your health is affected by “blood flow” as your stock’s viability is dependent on the “cash flow.” With that in mind, I’ll analyze the 4Q2021 earnings report for the period that concluded on December 31.

As follows, GBT procured $56.0M in revenues compared to $41.0M for the same period a year prior. The 36.5% increase is quite significant. On an annual basis, the company enjoyed the $194.7M in revenue which entail a 57% increase from $123.8M. Both the quarterly and annual numbers suggest a healthy business that is growing aggressively.

That aside, the research and development (R&D) for the respective quarters registered at $58.8M and $41.0M. The additional investment goes into funding GBT601, inclacumab, and other developments. I view the 43.4% R&D increase positively because the money invested today can turn into blockbuster profits tomorrow. After all, you have to plant a tree to enjoy its fruits.

Additionally, there was an $87.5M ($1.36 per share) net loss compared to a $61.8M ($1.00 per share) net decline for the same period. On a per-share basis, the bottom line depreciated by 36%. Don’t be alarmed by this, because GBT is simply putting more money earned into developing additional medicines. While the company takes a hit right now, that should pay off in the long haul.

{kind=link}

{kind=link}

On the balance sheet, there were $734.8M in cash, equivalents, and investments. Against the $139.0M quarterly OpEx, there should be adequate capital to fund operations into 1Q2023. Simply put, the cash position is robust yet the burn rate is a bit high.

While on the balance sheet, you should check to see if GBT is a “serial diluter.” After all, a company that is serially diluted eventually will render your investment essentially worthless. Given that the shares outstanding increased from 61.8M to 64.4M, my math reveals a 4.2% annual dilution. At this rate, GBT easily cleared my 30% cut-off for a profitable investment.

Valuation Analysis

It’s important that you appraise Guardant to determine how much your shares are truly worth. Before running our figure, I liked to share with you the following:

Wall Street analysts typically employ a valuation method coined Discount Cash Flows (i.e., DCF). This valuation model follows a simple plug-and-chug approach. That aside, there are other valuation techniques such as price/sales and price/earnings. Now, there is no such thing as a right or wrong approach. The most important thing is to make sure you use the right technique for the appropriate type of stocks.

Given that developmental-stage biotech has yet to generate any revenues, I steer away from using DCF because it is most applicable for blue-chip equities. For developmental biotech, I leverage a combination of both qualitative and quantitative variables. That is to say, I take into account the quality of the drug, comparative market analysis, chances of clinical trial success, and potential market penetration. Qualitatively, I rely heavily on my intuition and forecasting experience over the years.

|

Molecules and franchises |

Market potential and penetration |

Net earnings based on a 25% margin |

PT based on 64.4M shares outstanding and 10 P/E |

“PT of the part” after appropriate discount |

|

Oxbryta for SCD |

$1.5B (estimated based on the $5.5B SCD market, growing at a 14.3% CAGR) |

$375M | $58.22 | $52.39 (only 10% discount because it’s gaining strong sales traction) |

| GBT601 for SCD | $1B (estimated based on the $5.5B SCD market, growing at 14.3% CAGR) | $250M | $38.81 | $19.40 (50% discount because it’s still in early stage). |

|

Inclacumab for SCD |

$1B (estimated based on the $5.5B SCD market, growing at 14.3% CAGR) | $250M | $38.81 | $19.40 (50% discount because it’s still in early stage). |

| Younger pipeline assets | Will appraise with more development in the future | NA | NA | NA |

|

The Sum of The Parts |

$91.19 |

Valuation analysis (Source: Dr. Tran BioSci)

Potential Risks

Since investment research is an imperfect science, there are always risks associated with your stock regardless of its fundamental strengths. More importantly, the risks are “growth-cycle dependent.” At this point in its life cycle, the main concern for GBT is whether the company can continue to ramp up Oxbryta revenues.

Though Oxbryta is showing highly promising sales results, it’s still difficult for a small company going at it alone in commercialization to unlock full value. Moreover, there are risks that other pipeline molecules (like inclacumab and GBT601) won’t generate positive clinical outcomes. Furthermore, GBT might grow too aggressively and thereby run into a potential cash flow constraint.

Conclusion

In all, I maintain my buy recommendation on Global Blood Therapeutics with the 4.8 out of 5 stars rating. Global Blood Therapeutics is showing signs of a successful transition from a developmental to commercialized stage biotech. Subsequent to Oxbryta approval, sales ramp-up has been steady. Nevertheless, the latest quarterly results indicate that the company is hitting an “inflection point in its growth.” Epitomizing an aggressive growth phase, this growth inflection is powered by strategy, sales/marketing efforts to capture the traditional approach as well as digital innovation. More importantly, the recent pediatric and European approvals would boost sales even more robustly.

In the longer view, you have next-generation Oxbryta (i.e., GBT601), inclacumab as well as other SCD drugs. That aside, the company is poised to expand into the lucrative land of orphan disease to serve the unmet needs of patients and to reward shareholders.

As usual, I’d like to remind investors that the choice to buy, sell, or hold is always yours to make. In my view, you should either hold GBT or accumulate more shares on any pullback.

Be the first to comment