razihusin

Shares of General Dynamic (NYSE:GD) have been a rare bright spot during a difficult year in the equity market, about 12% in the past twelve months. While Russia’s invasion of Ukraine has caused terrible human suffering and contributed to the market carnage, it has been a tailwind for defense contractors on the expectation of larger defense budgets. In addition to the secular tailwinds aiding the sector, GD’s product mix and adept management of supply chain challenges make it an attractive investment.

Seeking Alpha

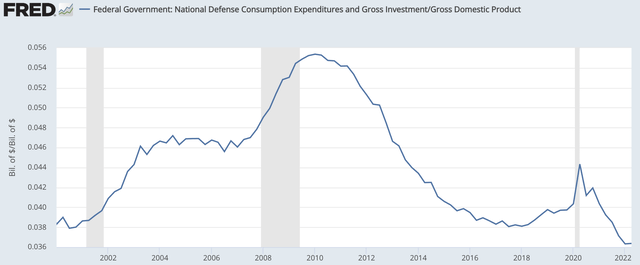

There is broad-based agreement that we need to increase defense spending. The threat posed by China and Russia certainly appears to have risen, yet as a share of GDP, defense spending sits at a 20-year low as last decade’s budget sequestration and recent years’ inflation has sapped the Pentagon of its purchasing power. There is $90 billion in potential new defense spending to just return our footing to the pre-COVID levels, and some may want to do more.

St. Louis Federal Reserve

Indeed, the Pentagon is requesting an additional $31 billion next year for a $773 billion budget, which seems like a lot, but Congress has even greater ambitions. The House is pushing an $840 billion proposal while the Senate is backing an $857 billion proposal. Regardless of which chamber wins out, there will be a lot more dollars flowing to the Pentagon, and that means a significant increase in orders for defense contractors. Even at the current spending level, General Dynamics has been able to grow its backlog, so the upside potential of more spending is significant.

That may not be first apparent when looking at the second quarter results because revenue fell 0.3%. As with many manufacturers, supply chain issues have lengthened delivery times for General Dynamics. They hit defense contractors particularly hard because making some components requires security clearances meaning that shifting supply routes is simply not feasible in a very short time period. It is important to note that GD was not alone in seeing revenue decline due to supply chain issues, but it has actually handled them better than peers. Northrop Grumman (NOC) reported a 4% decline in revenue; L3Harris (LHX) 6%, Lockheed Martin (LMT) 9% and Raytheon’s (RTX) defense units posted an 11% drop. Relative to its major competitors, General Dynamics had the best revenue results.

A further testament to management’s navigations of these disruptions is that operating earnings rose 2% to $978 million as margins increased by 20bp to 10.6%. In general, supply chain disruptions add costs and reduce production, so there was very effective cost management. As a consequence, EPS was up 5.4% to $2.75. A reason EPS growth outpaced income growth is that the company’s share count is down about 1.5% over the past year. GD’s strong free cash flow generation enables it to steadily buy back stock and compounds over time to accelerate per share earnings growth.

While the vast majority of GD’s business is defense, it does have a non-defense component to its aerospace unit with its ownership of Gulfstream, the leading maker of business jets. Post-COVID, I was fearful that lessened business travel would hit this business. However, that does not seem to be the case. Perhaps even with somewhat less travel, companies are more willing to go private rather than commercial to reduce time and complexity.

Indeed, aerospace revenue rose 15%, and even more impressively, Gulfstream registered twice as many orders as deliveries. Whatever my fears were, this unit is a source of growth. In fact, its backlog has risen from $12 billion to start 2021 to $18.8 billion today. That is about 2.5 years’ worth of revenue without a single net new order. Given a growing order book, its Gulfstream unit will likely be a steady generator of cash flow for years to come.

On the defense side of the business, marine systems saw a 4.5% increase in revenue as the Columbia-class submarines continue to progress on schedule, and it has a $41 billion backlog. Despite a 10% drop in combat systems revenues, operating margins rose 70bp to 14.7% with the backlog steady at $13.4 billion. The technologies unit also expanded margins by 40bp. Across the board operating performance was strong.

In aggregate, the business had a book to bill ratio of 1.1x for the quarter, pushing the backlog to $87.6 billion. Unfunded and unexercised options create another $39 billion in revenue opportunities. First half free cash flow was nearly $2.3 billion, but this was aided by $800 million of favorable working capital movement. For the year, the company should be able to generate $3 billion in free cash flow, assuming flat working capital.

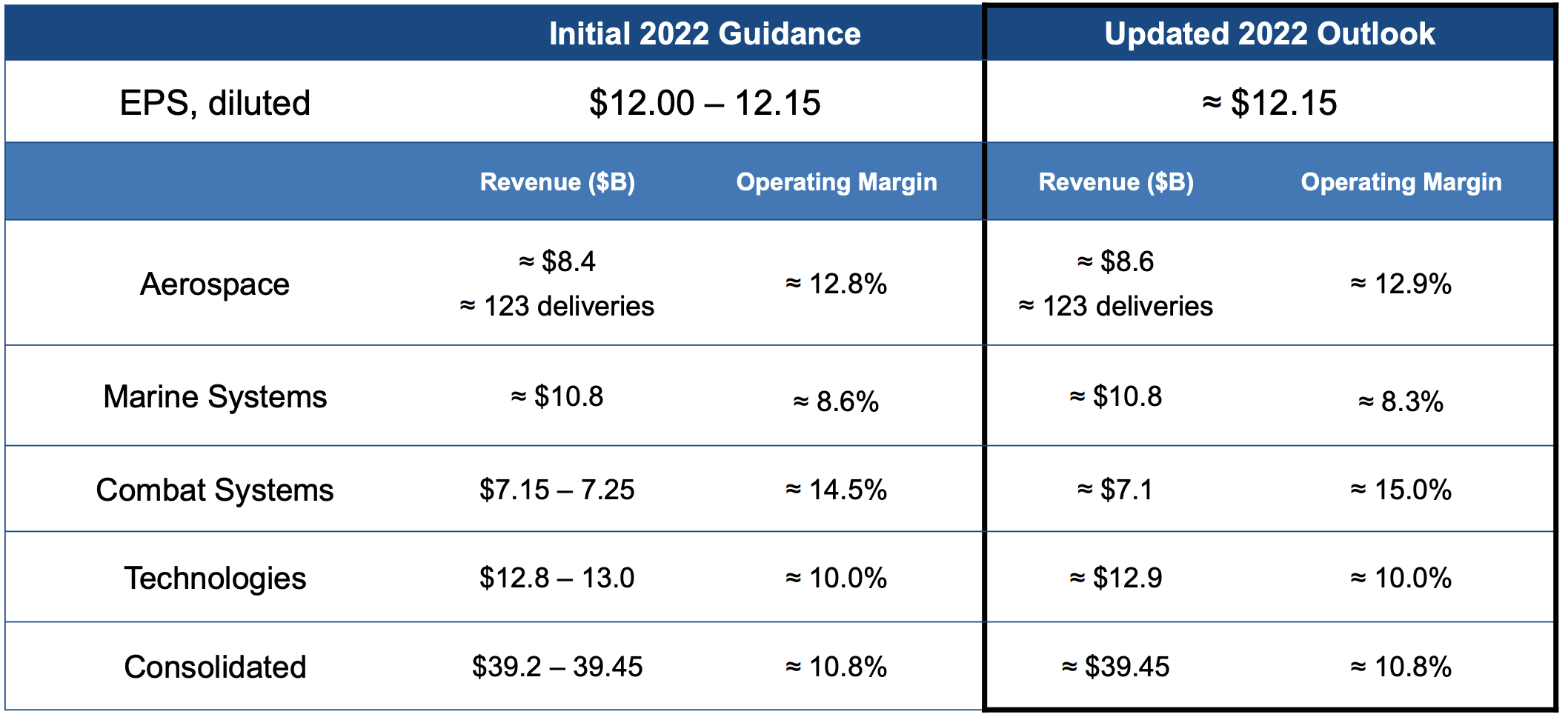

Even as Q2 revenue fell slightly, management affirmed that revenue will come in at the high-end of its forecast. This should translate to at least $11.10 in earnings per share this year.

General Dynamics

Beyond the strong management of supply chain challenges and a rising defense budget, there is one program that makes me particularly optimistic about General Dynamics’ potential earnings growth: the Columbia-class submarine.

The Columbia-class submarine is “the Pentagon’s top acquisition priority.” In fact, the Navy has listed it as its top procurement item since 2013. The lead ship is currently being built with the Navy hoping to build at least twelve and likely sixteen. At twelve ships, this is estimated to be a $113 billion program, and we are still in the beginning stages.

A successful roll out is critical to replace the Ohio-class as the submarine arm of the strategic nuclear force’s triad (ground, sea, and air launch capabilities of nuclear weapons). With China aggressively expanding its naval and submarine presence, General Dynamics is critical to ensure the US navy can sustain and grow its submarine fleet. Fortunately, everything continues to run on schedule.

Just as the F-35 system has helped generate significant growth and cash flow for Lockheed Martin over the past decade, Columbia-class submarines can power significant growth for General Dynamics over the next decade. So while the overall Pentagon budget is poised for several years of mid-single digit growth, I expect GD to get a bigger share of that spending with the potential for several years of 10% growth as the Gulfstream delivers on its backlog and the production of Columbia-class submarines ramps up.

With about $12.20 in 2023 earnings power, GD has a multiple of about 18.3x. Given the noncyclical nature of its industry, the secular growth of its product position, and strong cash flow generation, I think GD will be able to earn a 20x multiple as investors appreciate what Lockheed is to the Air Force, General Dynamics is to the Navy. I am looking for shares to trade to the low $240s, pointing to about 10% upside from here.

Be the first to comment