FX Week Ahead Overview:

- Price pressures are in focus for market participants with inflation data from Mexico (Tuesday), China (Wednesday), and US (Wednesday).

- Focus returns back to the US Dollar in the coming days, with the US fiscal stimulus talks ongoing and Fed Chair Jerome Powell set to deliver a speech

- Changes in retail trader positioning suggest that most USD-pairs are on mixed footing.

Starts in:

Live now:

Feb 15

( 11:02 GMT )

Recommended by Christopher Vecchio, CFA

FX Week Ahead: Strategy for Major Event Risk

For the full week ahead, please visit the DailyFX Economic Calendar.

02/09 TUESDAY | 12:00 GMT | MXN Inflation Rate (JAN)

On Tuesday, the January Mexican inflation rate (CPI) is expected to show an uptick from +3.15% to +3.46% (y/y). Higher inflation may help cool some of the dovish talk at the margins around Banxico in recent months, which in turn could help the Peso continue last week’s run of strength. Recall that at the end of 2020, Mexican President Andres Manual Lopez Obrador nominated Galia Borja Gomez, the Treasurer of the Mexican Finance Ministry, to join Banxico has deputy governor. Historically, Banxico has had a hawkish tilt, but Mexican Treasurer Gomez has dovish leanings.

02/10 WEDNESDAY | 01:30 GMT | CNY Inflation Rate (JAN)

As ground zero for the outbreak, the Chinese economy was hit by the coronavirus pandemic earlier and harder than its developed counterparts in Asia, Europe, or North America. To this end, the big drop off in economic activity is leading to a base effect in some data, inflation included (this base effect is due to arrive in the rest of Asia, Europe, and North America over the coming months). The People’s Bank of China may thus look through any spike in the inflation figures that would, in an otherwise normal environment, suggest that a reduction in monetary support might be considered.

02/10 WEDNESDAY | 13:30 GMT | USD Inflation Rate (JAN)

The January US inflation (CPI) report will be released on Wednesday, February 10 at 13:30 GMT. According to a Bloomberg News survey, further stabilization in price pressures is anticipated with the headline inflation rate due in at +1.5% from +1.6% (y/y) in December, while core inflation is due in at +1.5% from +1.4%. Marginally weaker price pressures may not do much to move the needle on Federal Reserve monetary policy, as FOMC officials have tamped down any preliminary taper talk. But we’ll soon learn how resilient of a position the Fed has staked out, as the likely impact of a base effect could drive headline inflation higher to and through +2% over the coming months.

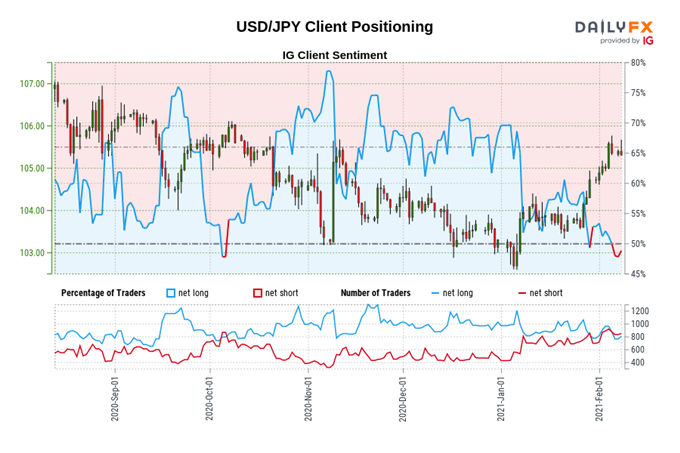

IG Client Sentiment Index: USD/JPY Rate Forecast (February 8, 2021) (Chart 1)

USD/JPY: Retail trader data shows 47.19% of traders are net-long with the ratio of traders short to long at 1.12 to 1. The number of traders net-long is 11.71% higher than yesterday and 9.58% lower from last week, while the number of traders net-short is 14.32% higher than yesterday and 15.71% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests USD/JPY prices may continue to rise.

Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger USD/JPY-bullish contrarian trading bias.

02/10 WEDNESDAY | 19:00 GMT | USD Federal Reserve Chair Jerome Powell Speech

The Federal Reserve has firmly pushed back against nascent taper tantrum fears, with Fed Chair Jerome Powell making clear that the FOMC was in no hurry to shift course. As long as Fed Chair Powell is at the helm, the FOMC will stay the course, with the intent of keeping interest rates low through 2023. Fed funds futures are pricing in a 93% chance of no change in Fed rates in 2021. Fed Chair Powell’s speech on Wednesday, February 10 has a chance to stir volatility, perhaps more than usual, given the fact that there is no FOMC meeting this month.

02/12 FRIDAY | 07:00 GMT | GBP Growth Rate (DEC & 4Q’20)

The end of 2020 was difficult for the UK. Uncertainty over Brexit collided with the widespread emergence of the B1.1.7 mutation of COVID-19, leading to significant hurdles for the UK economy. But data in recent weeks has been encouraging. The UK leads the developed Western world in vaccination rates, while the post-Brexit transition has thus far gone smoothly (outside of some public issues around shellfish). Any issues seen in the December 2020 or 4Q’20 UK GDP data may be overlooked as more near-term information paints a brighter future.

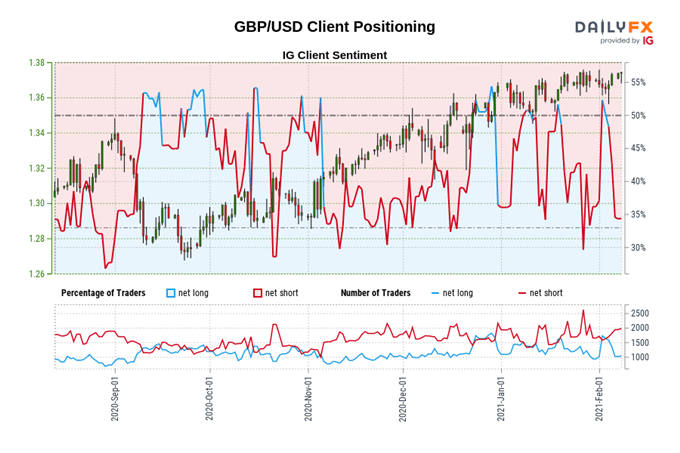

IG Client Sentiment Index: GBP/USD Rate Forecast (February 8, 2021) (Chart 2)

GBP/USD: Retail trader data shows 38.94% of traders are net-long with the ratio of traders short to long at 1.57 to 1. The number of traders net-long is 25.91% higher than yesterday and 6.88% lower from last week, while the number of traders net-short is 3.05% higher than yesterday and 12.01% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests GBP/USD prices may continue to rise.

Positioning is less net-short than yesterday but more net-short from last week. The combination of current sentiment and recent changes gives us a further mixed GBP/USD trading bias.

— Written by Christopher Vecchio, CFA, Senior Currency Strategist

Be the first to comment