deepblue4you/iStock via Getty Images

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note’s date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

The Future’s So Bright, You Gotta Wear Shades

This was the theme of the Tesla (NASDAQ:TSLA) earnings call yesterday following the print. And like all growth stocks, if you are to buy and indeed hold TSLA, you have to be looking to the future and not the past. Value stocks are priced on dividend yield, balance sheet strength, rate of buybacks and so forth; growth stocks valued based on a belief that tomorrow will be better than today. This is why, when they disappoint, they hit the deck so hard and so fast. And it’s also why, when on the deck, the best of them pick themselves up, dust themselves down, and get back to work making the future a better place.

None more so than Tesla.

Today And Yesterday

This is what today and yesterday looks like at Tesla.

It was a weak quarter with growth declining and margins down. The company has a part-time CEO – he must be part time since he’s also CEO of Twitter which one would think is a full time job by itself (not that this ever bothered the prior Twitter CEO, who also treated it as a side hustle whilst being CEO of Block (SQ)). Tesla also has senior staff who spend part of their time at another business part-owned by the Tesla CEO. Competition is hot on the heels of this sector leader. The model range is aging and the new models – Cybertruck, Semi – are yet to hit the street in anything like production form. The sidelines – solar and battery packs – remain sidelines. And the stock trades at c.60x cash flow.

That’s a recipe for a continued down move. If you’re looking backwards.

If you are looking forward into the light, into the landscape as painted during the earnings call? Then your focus would be on the clear statement that order intake rates are exceeding the rate of production. That price cuts would work in Tesla’s favor because in the end volume wins in this sector. And that the development of Full Self Driving continues apace.

This comes down to, do you believe. Do you believe that Tesla can keep ahead of the competition? Do you believe that volume at lower automotive gross margins can in the end drive either bigger cash flows or a bigger multiple of lower cash flows. And do you believe that the behemoths headed Tesla’s way – VW, Daimler-Benz first amongst them – can be held at bay. (Or – whisper it lest you annoy the Teslarati – will someone buy Tesla to secure leadership in the EV sector, delivering you a fat premium on the stock price from here?)

Well, we’re fundamentalists here at Cestrian. We bought into Tesla stock personally not based on a dream in 2012 or 2016 but based on convincing fundamentals in 2018 and, more, in 2019. Tesla bears may not care to admit it but if you put your thumb over the name of the company and just looked at the fundamentals, only an idiot wouldn’t say, well, that’s one beautiful set of numbers. And that remains the case post Q4. Growth down, margins down, still a great business looking backwards.

The price that the market is asking you to pay – 60x TTM unlevered pre-tax FCF or a little under 6x TTM revenue – is based on looking forward. Only you can decide whether that’s a buy, a sell, or a hold. For us? We believe that the company, imbued with the Musk quasi-founder DNA still even at this scale, will fight its way out of the current problems. We anticipate Musk’s role at Twitter and at Tesla resolving such that management structures can be normalized enough, we believe the Twitter distraction will level off once it is refinanced and demonstrates pro-forma profitability having cut a reported 75% of its staff, and we believe that a back-to-the-wall Tesla will surprise to the upside. Maybe not tomorrow. Might take a while. But this is a retirement-account hold for us, and we can wait.

Numbers

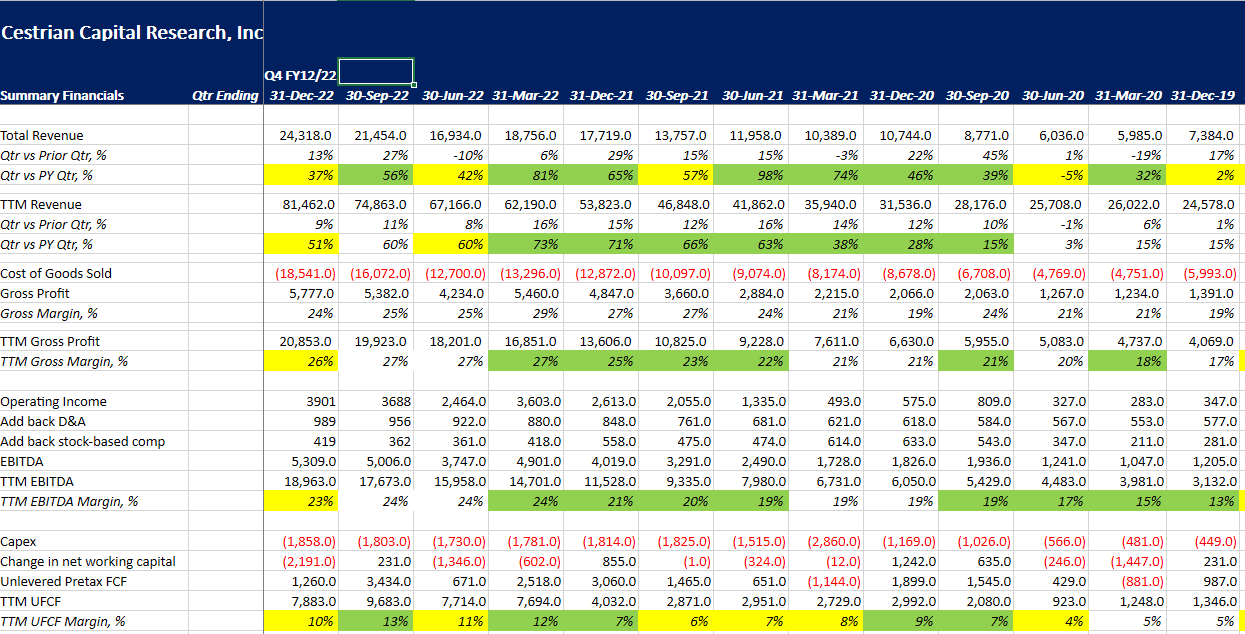

- Revenue growth fell to +37% for the quarter vs. Q4 FY12/21, +51% on a TTM basis vs. the period to end Q4 FY21.

- Gross margins down to 24% in quarter from a peak 29% in Q1 this year – this will remain under pressure from the price cuts and is a key bet by Musk that volume will counteract the margin pressure.

- Unlevered pre-tax FCF margins down to 10% on a TTM basis – that looks bad vs. the last three quarters but it remains high vs most of Tesla’s history and indeed high for the auto sector at large.

TSLA Fundamentals I (Company SEC Filings, YCharts.com, Cestrian Analysis)

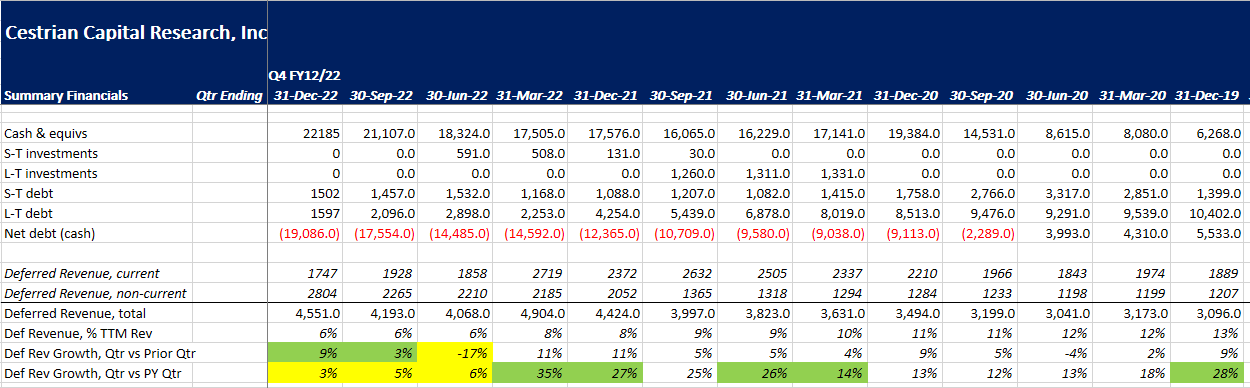

- The balance sheet remains strong – $19bn of net cash on hand.

TSLA Fundamentals II (Company SEC Filings, YCharts.com, Cestrian Analysis)

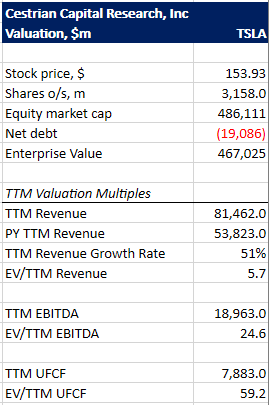

Valuation is, as we raised above, based on looking forward, not backwards. 59x TTM unlevered pre-tax FCF / 5.7x TTM revenue is a big number in the light of the slowing growth and margin compression.

TSLA Valuation (Company SEC filings, YCharts.com, Cestrian Analysis)

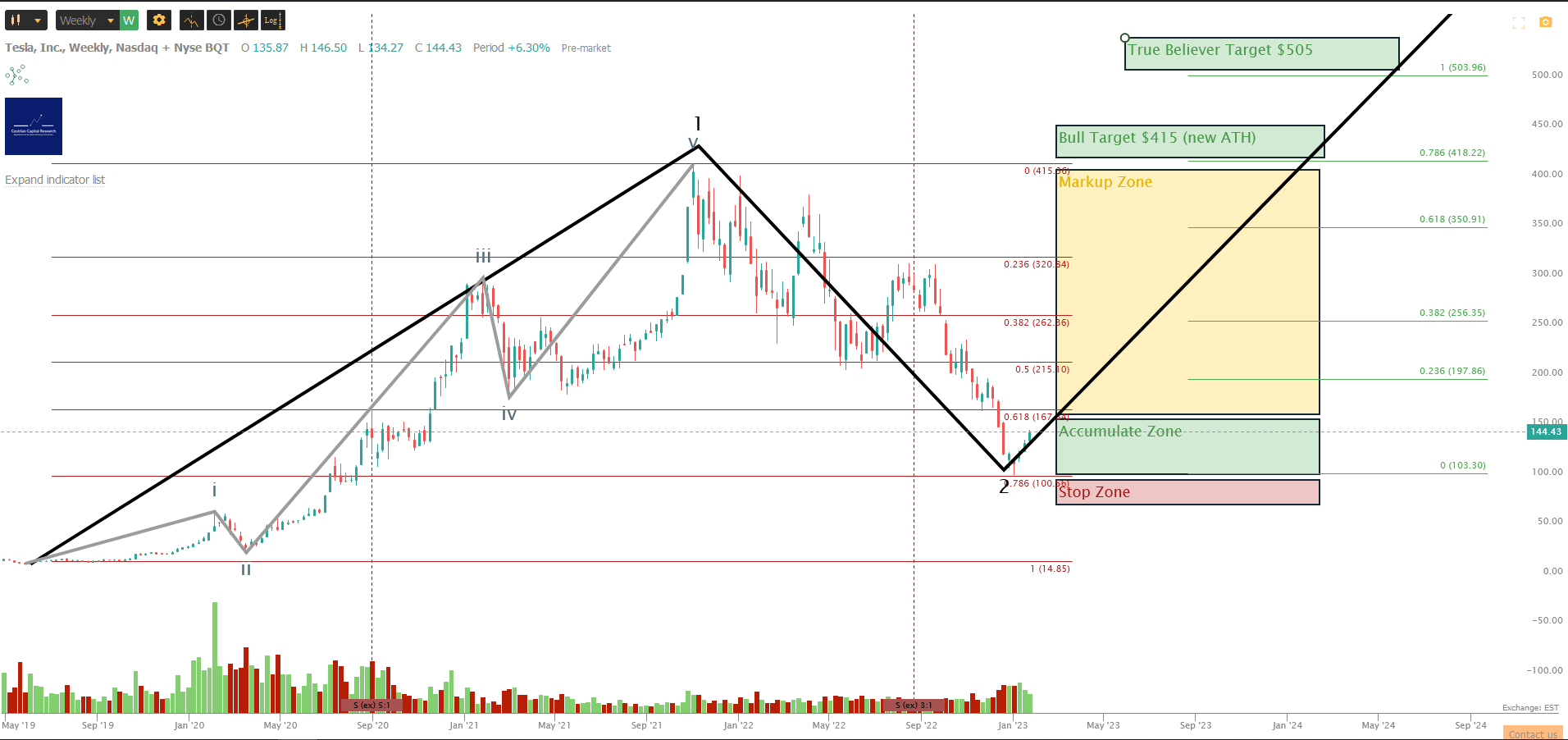

Chart Outlook

Here’s the chart as we see it.

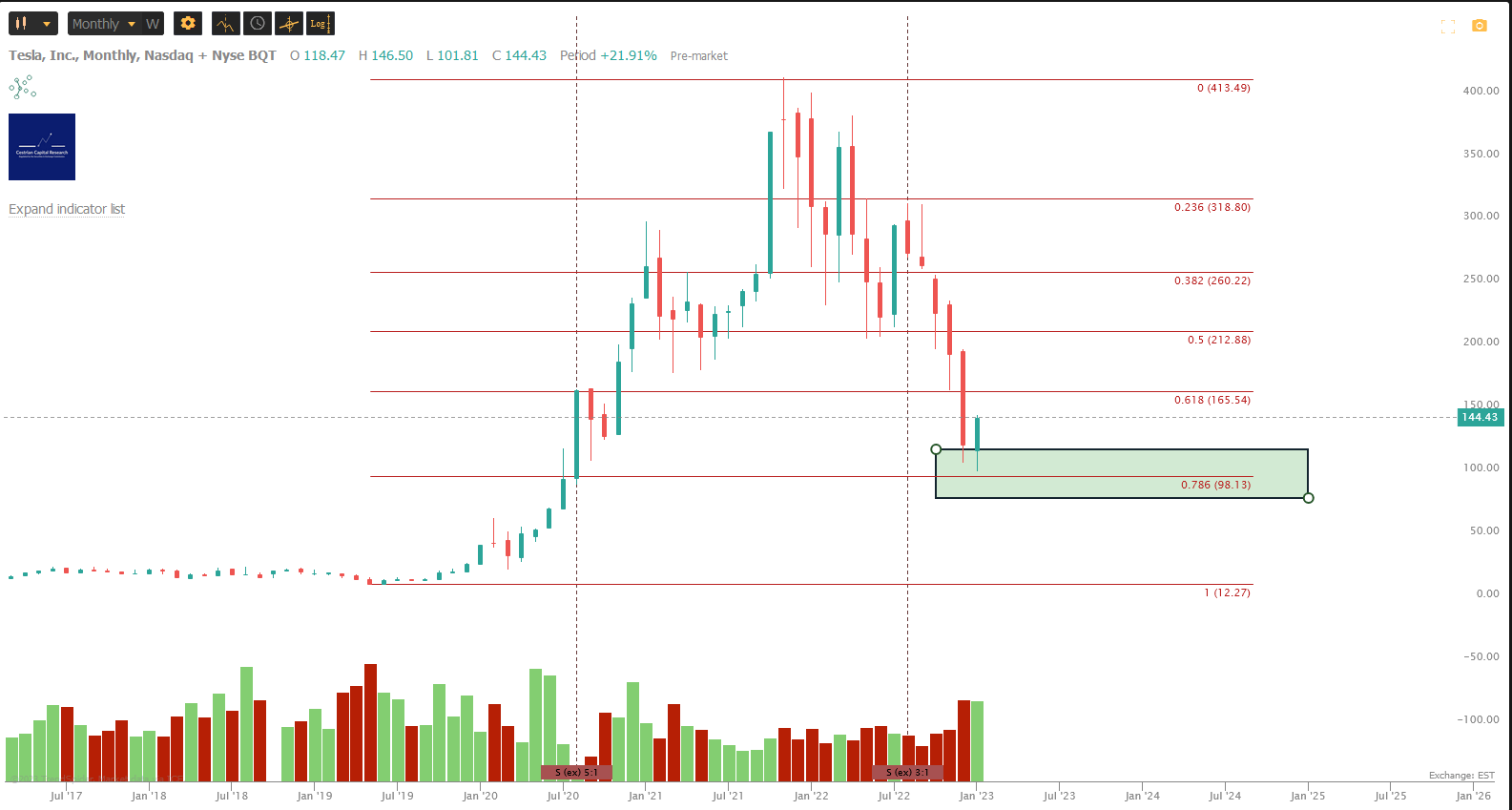

First, note that the stock found support and reversed hard at the 78.6% Fibonacci retracement of the move from the 2019 lows to the 2021 highs.

TSLA Long Run Chart (TrendSpider, Cestrian Analysis)

That suggests the end of a large and brutal wave two down and the start of a wave three upwards. If true, TSLA stock may surprise everyone – to the upside. We make no judgment here. Stocks can keep moving down from that Fib level – just ask Ark Invest – but when you see a reversal there it can be meaningful. You can find a similar pattern at Meta (META) and Nvidia (NVDA). Also the Bitcoin chart by the way looks exactly like that – support and reversal at the .786 retrace of the huge up-move peaking at the end of 2021. It means you have a logical place for a stop which can prevent major losses while still allowing the stock the volatility it possesses.

Here’s our outlook. You can open a full page version, here.

TSLA Chart (TrendSpider, Cestrian Analysis)

So – looking back and looking forward? We rate at Accumulate. In staff personal accounts we are long TSLA stock, long TSLA calls, and hold protective TSLA put positions too. Overall, net long.

Cestrian Capital Research, Inc – 26 Jan 2023.

Be the first to comment