pawopa3336

Investment Thesis

I have covered Fresnillio (OTCPK:FNLPF) in the past, which is the largest silver producer in the world, that also produces gold, and smaller amounts of base metals. The company is listed in Mexico, the UK, and available OTC in the U.S. It is one of very few silver producers that has consistently delivered profits over the years, even when the market has been less accommodative, and other silver producers have stumbled.

Figure 1 – Source: Koyfin

The company has recently been having delays getting the Juanicipio mine connected to the national electricity grid, which has held back the production volume some, and likely the share price as well. Given that the plant has now been connected to the grid and the commissioning is ongoing, and is expected to reach full nameplate capacity in Q3 2023, it has the potential to be a positive catalyst for the company during 2023.

Production & Guidance

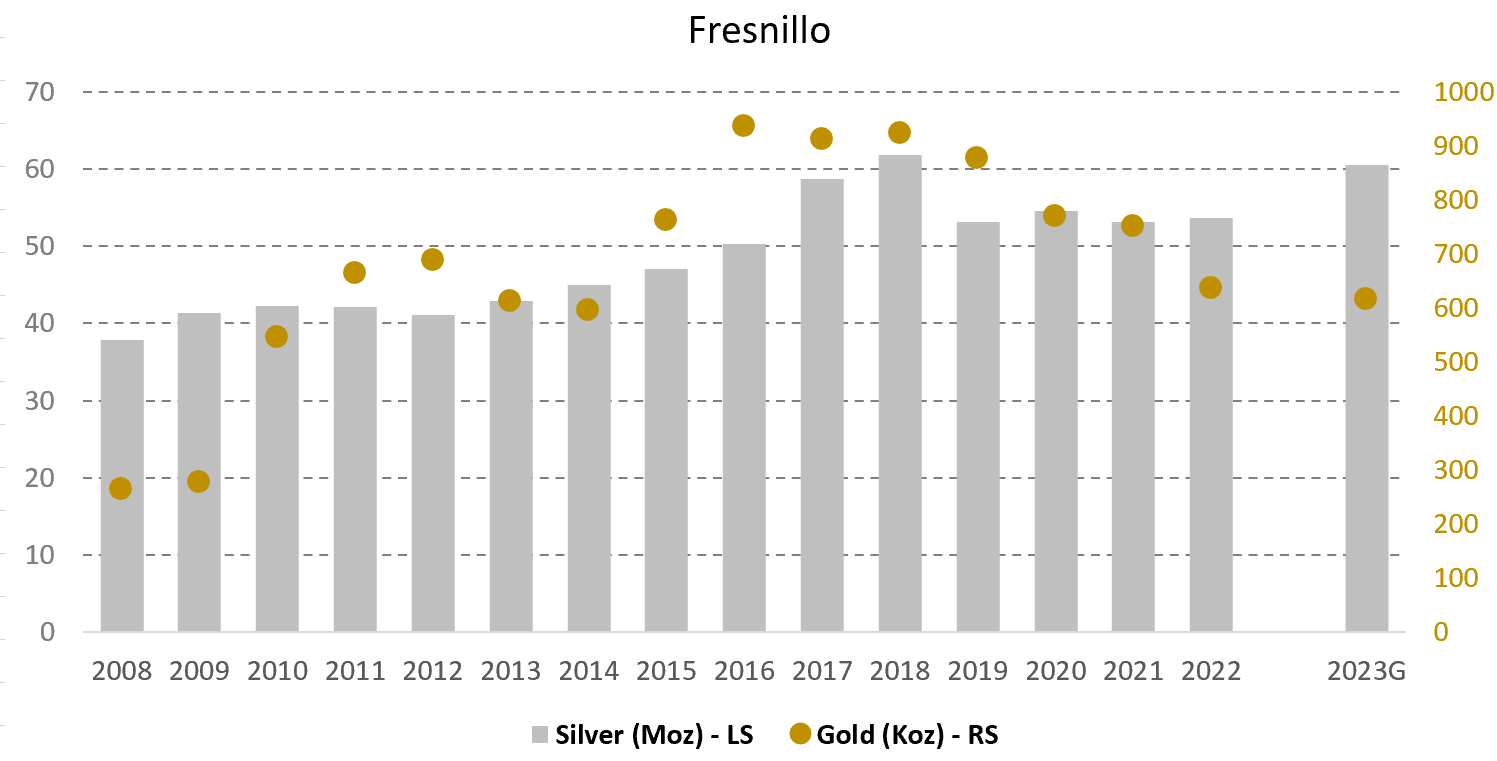

Fresnillio did on the 25th of January release the Q4-22 and 2022 production report for the company, which indicated a slight 1.2% production increase in total silver production in 2022 compared to 2021. Gold production declined year-over-year by 15.3% and base metal production also declined marginally. The numbers were in line with guidance.

Figure 2 – Source: Q4-22 Production Report

The company did also provide production guidance for 2023, where the mid-point of guidance looks to deliver a 13% increase in silver production during 2023 and gold production is only expected to decline by 3%. So, 2023 is the first year in a while that the company is expected to see a year-over-year increase in silver equivalent production. This is, no doubt, a welcome change for the company.

Figure 3 – Source: Data from Annual Reports & Production Updates

Valuation

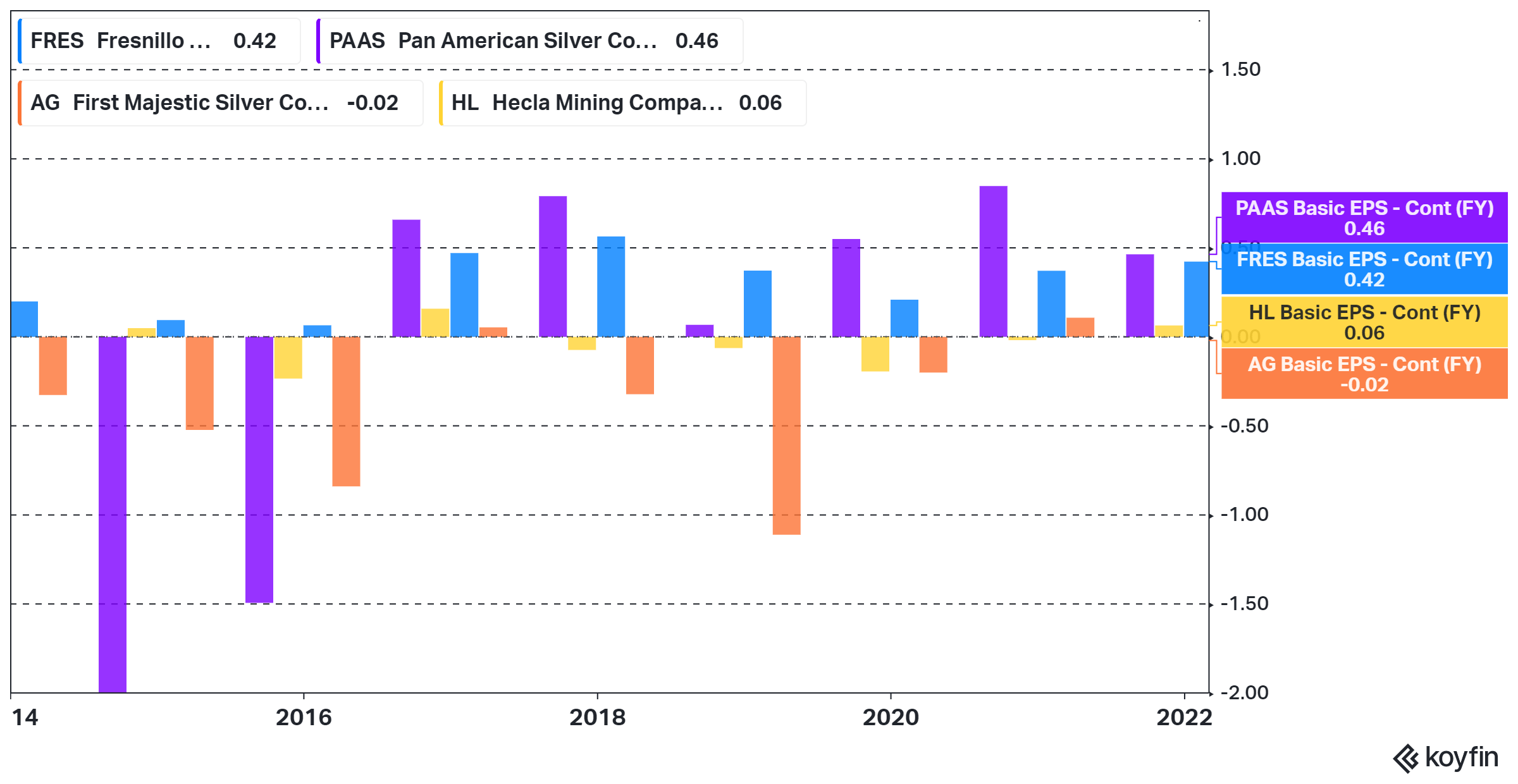

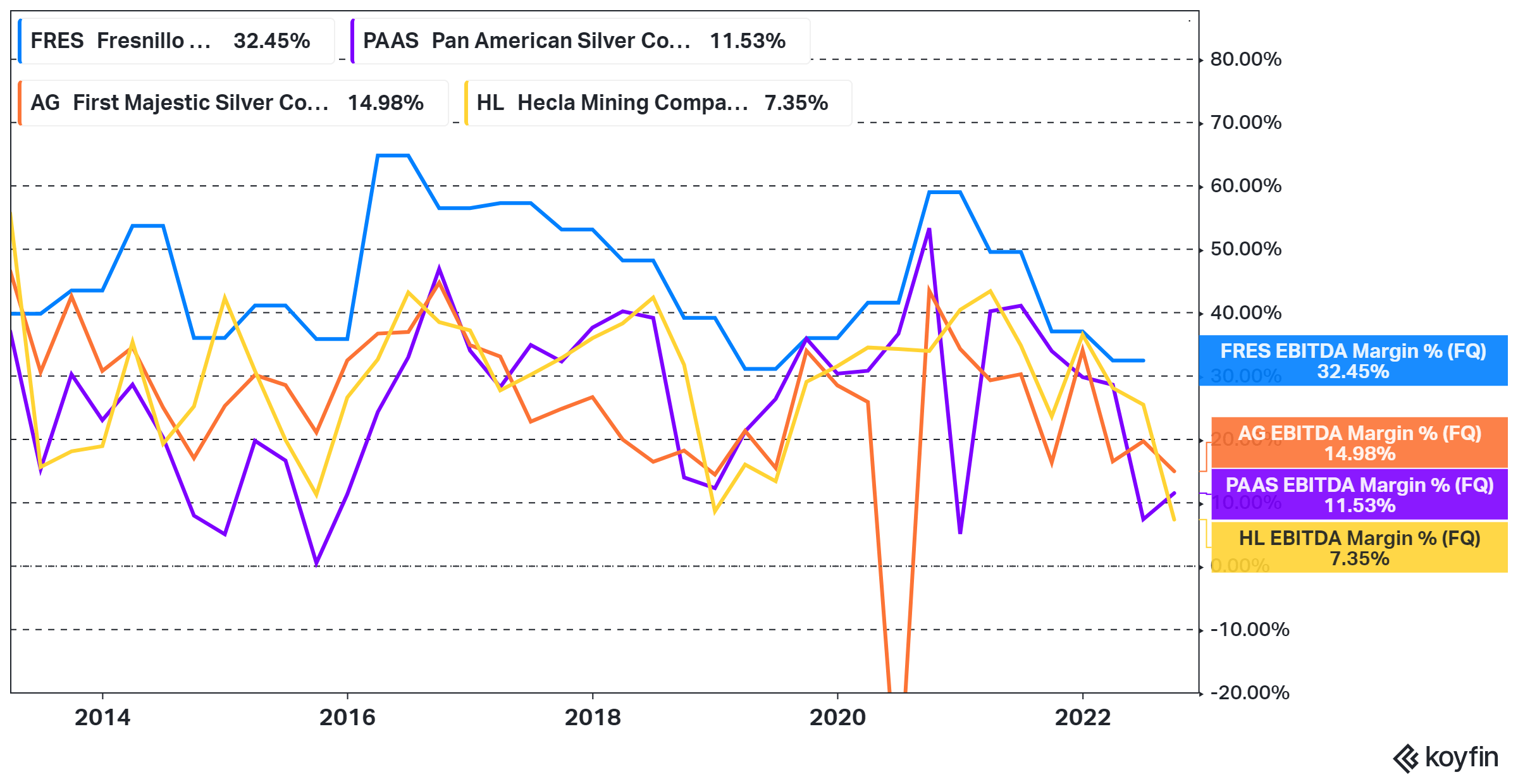

Fresnillio does offer several attractive characteristics among the silver miners. The company has higher margin assets, which is the reason for the consistent profitability over the last decade.

Figure 4 – Source: Koyfin Figure 5 – Source: Koyfin

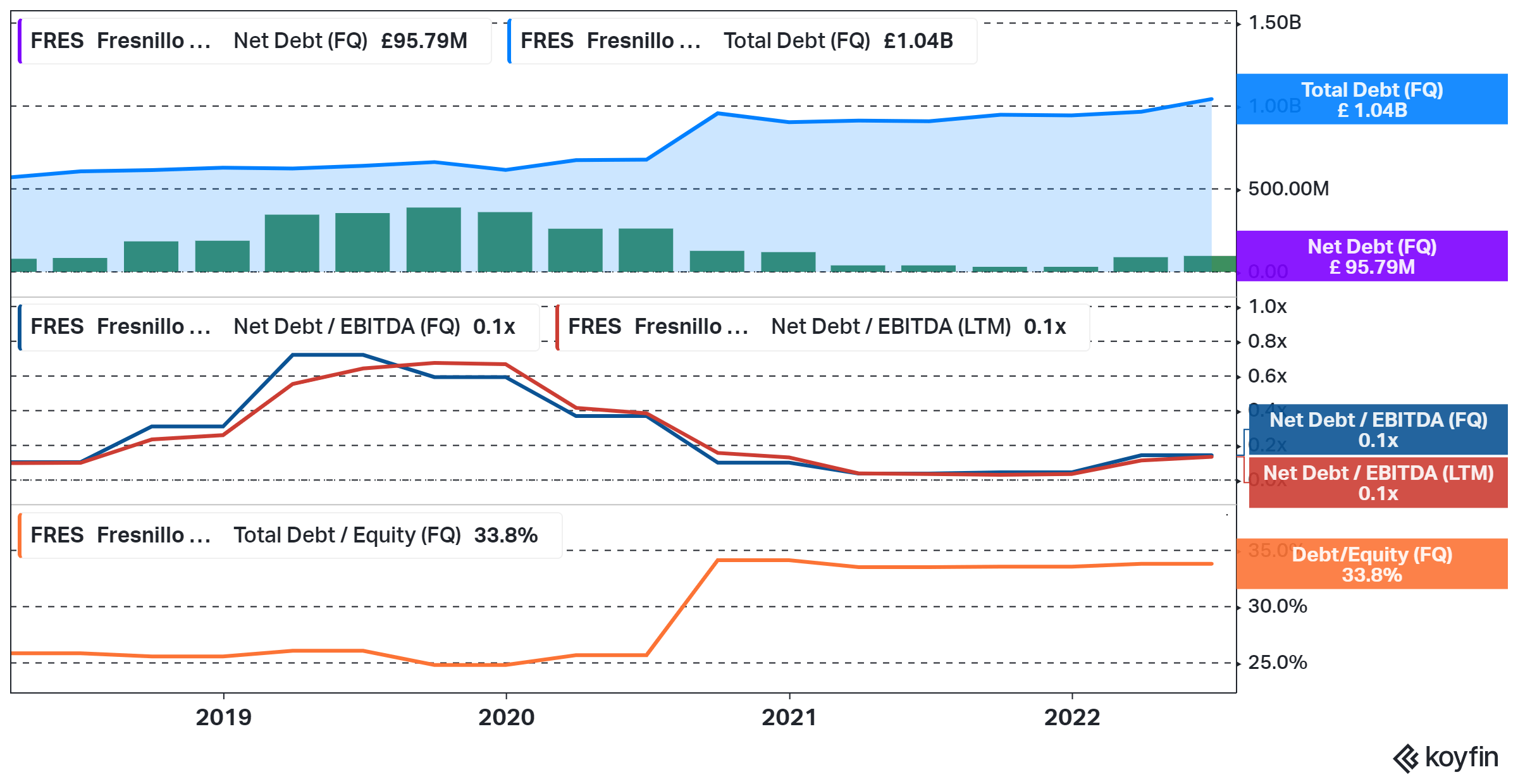

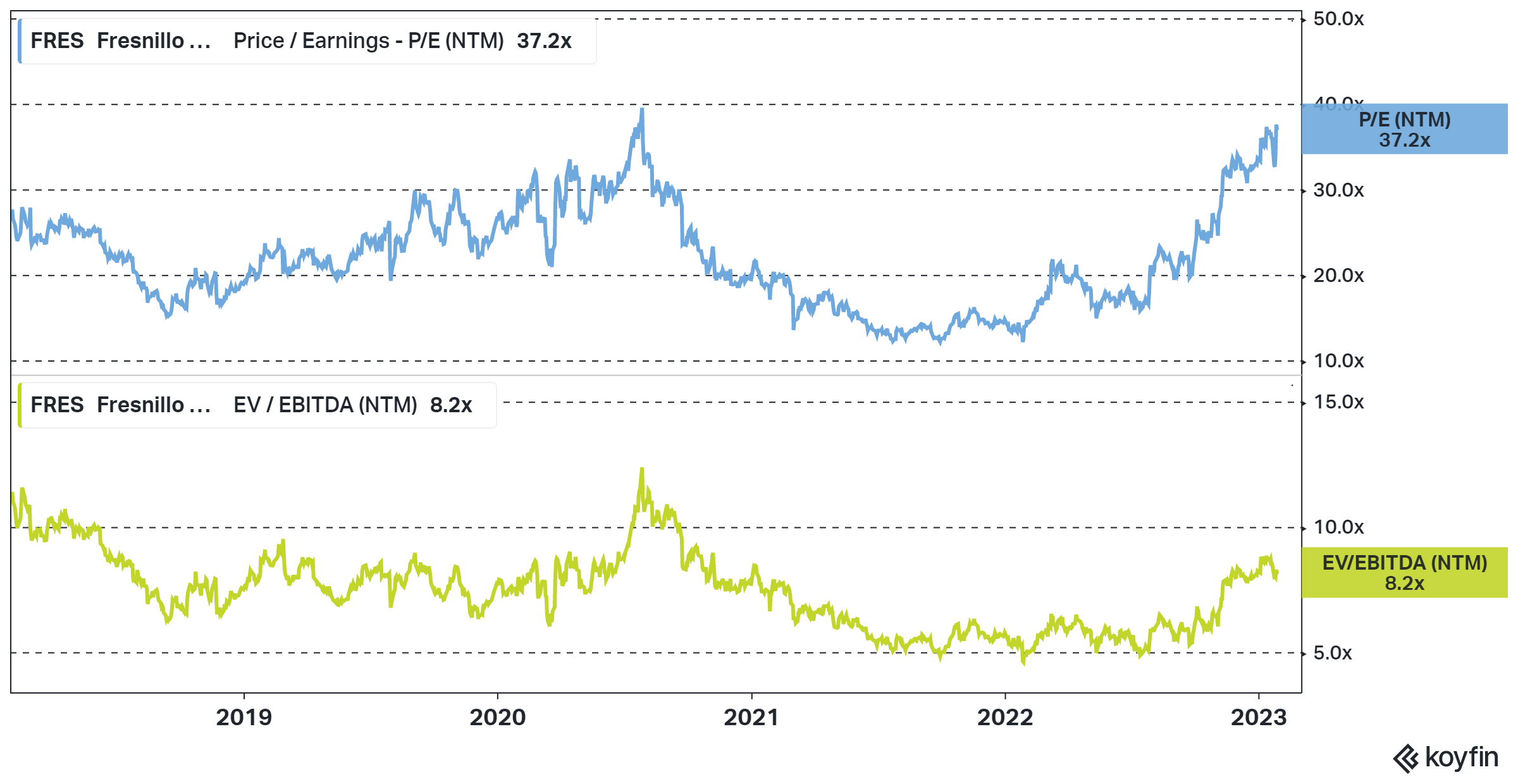

It is a company with a solid balance sheet, where the net debt is close to zero, which means the net debt to EBITDA is very low. So, given the quality characteristics, one could certainly make an argument for a premium valuation. However, the stock has recently traded in the upper end of the 5-year range for EV/EBITDA and Price/Earnings. So, it does feel far from a bargain at this level.

Figure 6 – Source: Koyfin

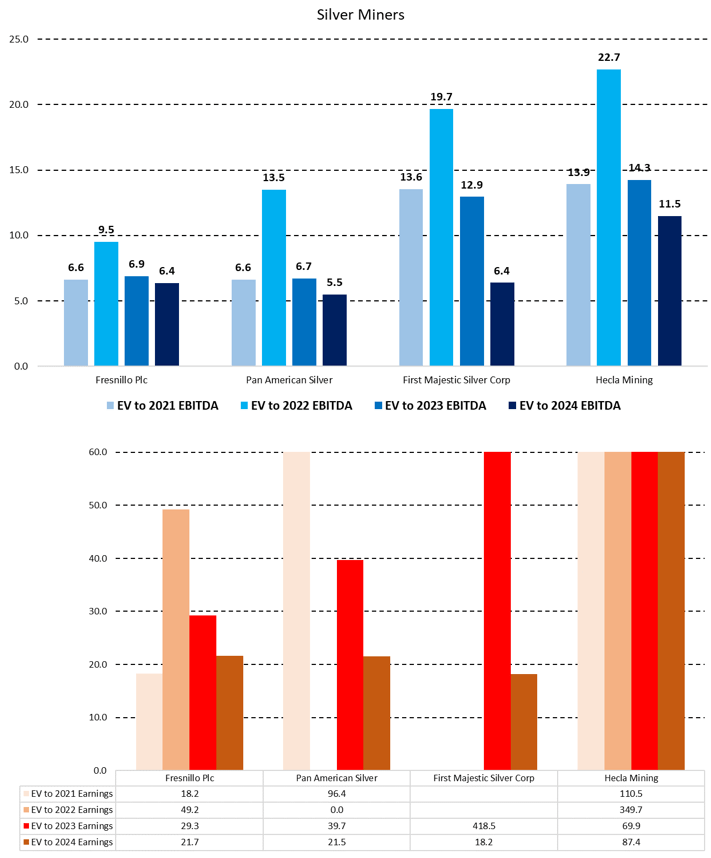

Now, if we compare the valuation of Fresnillo to some selected silver peers, the valuation is far from extreme, as the below charts indicate. However, at least to me, the absolute valuation is far more important than the relative valuation. It is also worth pointing out that the other larger silver producers have recently struggled with profitability. So, it might not be a massive achievement either to look more attractive than them on a valuation basis.

Figure 7 – Source: Estimates from Koyfin & Other Data from Quarterly Reports

Conclusion

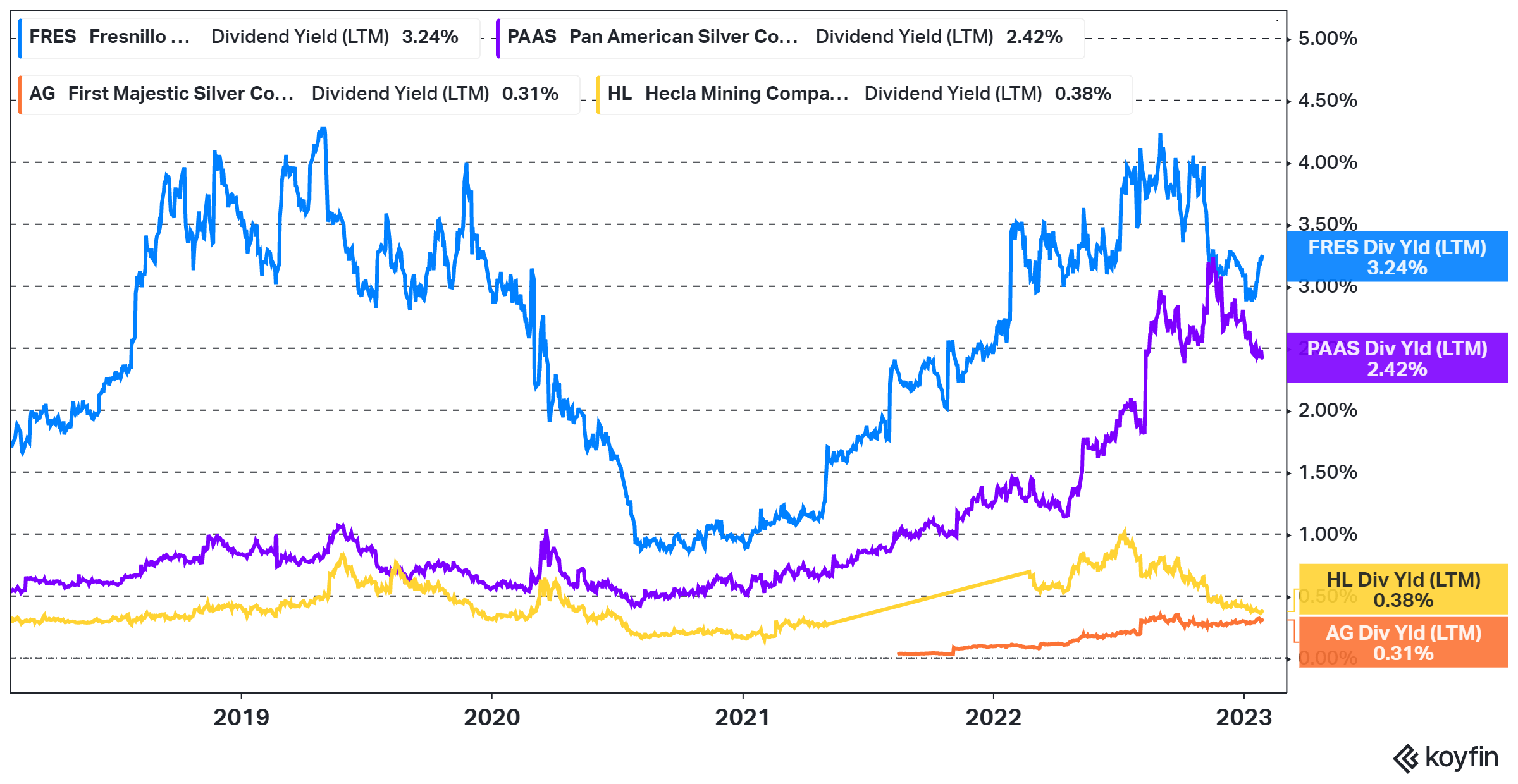

The good balance sheet and dependable profitability are quality characteristics for Fresnillo, which are not easy to found in the industry. The company has also been paying a relatively attractive dividend yield, well above its peers most of the time.

Figure 8 – Source: Koyfin

The valuation is, however, too steep for me at this level. Especially when there are more junior quality silver developers still trading at very depressed levels.

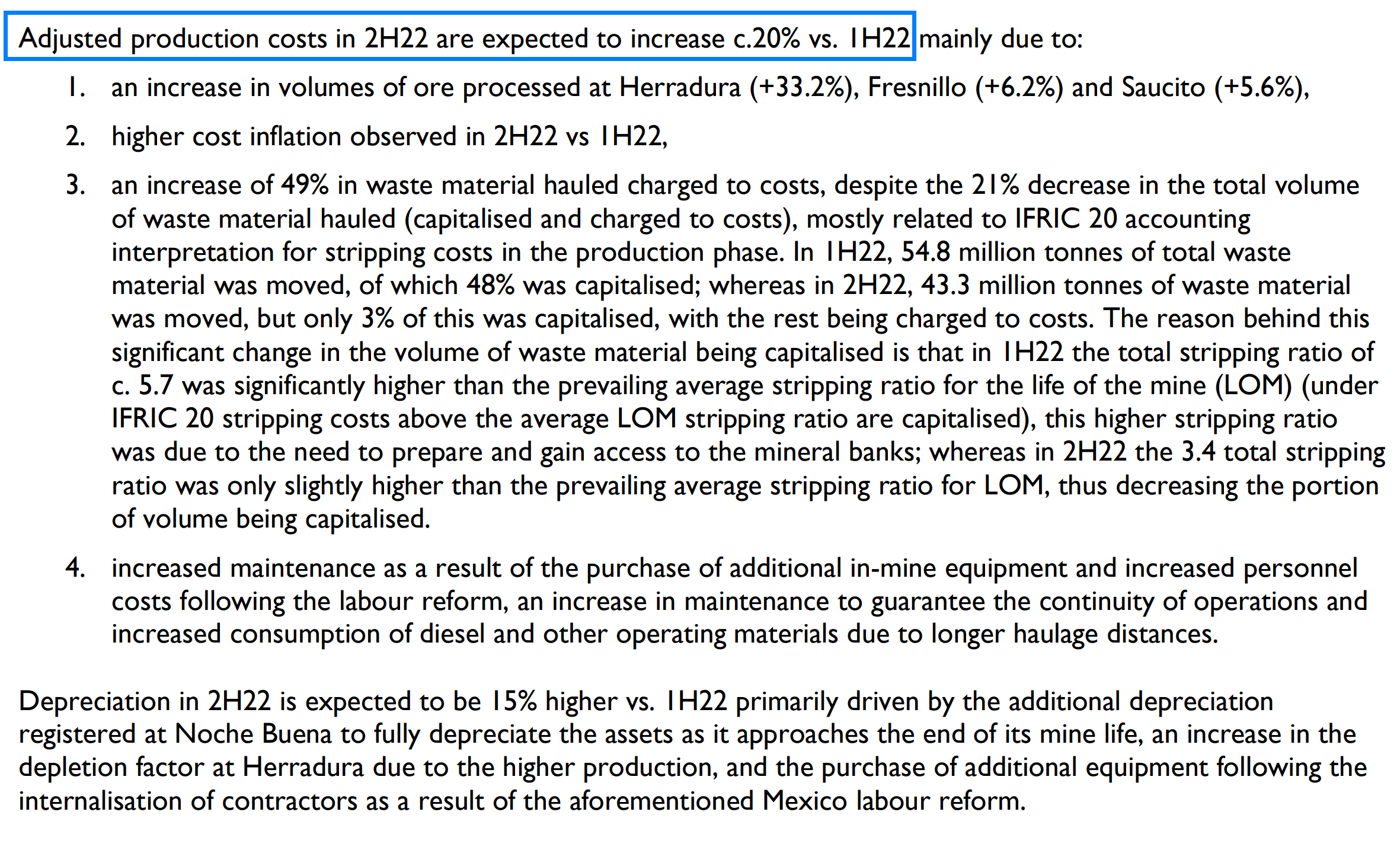

Another concern is inflation. It could be argued that this has impacted all miners and Fresnillo has managed costs reasonably well judging by the profitability of the company. However, it was in the production update communicated that production costs for H2-22 are expected to increase by 20% compared to H1-22, which is no small amount. A cost increase of this size has the potential to offset any positive momentum in the share price might get from the Juanicipio commissioning.

Figure 9 – Source: Q4-22 Production Report

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment