Central Bank Watch Overview:

- As 2021 comes to a close, rates markets are less aggressive in their expectations on Fed policy in 2022 and 2023.

- The Fed’s accelerated rate of tapering will see QE end by March 2022, where Fed funds futures are currently discounting the first 25-bps rate hike.

- Fed rate hike odds are still discounting five rate hikes through the end of 2023, with a 63% chance for six 25-bps rate hikes in total.

Dovish or Hawkish Tightening Ahead?

In this edition of Central Bank Watch, we’ll review comments and speeches made by various Federal Reserve policymakers in the two weeks after the communications blackout window around the December Fed meeting ended. To no surprise, all is quiet on the Fed front, insofar as the Christmas and New Year holidays have seen policymakers go on vacation.

For more information on central banks, please visit the DailyFX Central Bank Release Calendar.

Mostly Quiet Since December Fed Meeting

Considering the momentous shift in Fed policy at the December Fed meeting, one may find it surprising that there have been nearly zero communications by Fed officials in the immediate aftermath. But perhaps this is due to market pricing: after all, markets were already pricing in the change to the pace of tapering, and had for several months discounted five-plus rate hikes through the end of 2023. With the holidays upon us, Fed policy officials may have simply opted to take their time off as opposed to inadvertently upsetting the proverbial apple cart; US equity markets are closing out the year at or near all-time highs.

December 15 – The December Fed meeting sees the FOMC increase the rate of QE tapering to $30 billion per month in January and February 2022, which will zero out asset purchases by March 2022. With Powell (Fed Chair) noting that “the economy has been making rapid progress toward maximum employment,” it was determined that “economic developments and changes in the outlook warrant this evolution of monetary policy.”

December 17 – Waller (Fed Governor) suggested that the acceleration in QE tapering positions the Fed to raise rates early in 2022, further commenting that “actually raising interest rates would be a sign of a positive development in terms of where we are in the economic cycle.”

More Hawkish…and Less Hawkish?

Rates markets are starting to twist and turn in a manner that suggests that Fed may be both more hawkish and less hawkish. More hawkish in the sense that rate hikes could arrive sooner than previously anticipated, but less hawkish in the sense that fewer rate hikes may ultimately transpire by the end of 2023 if the Fed acts aggressively in 2022.

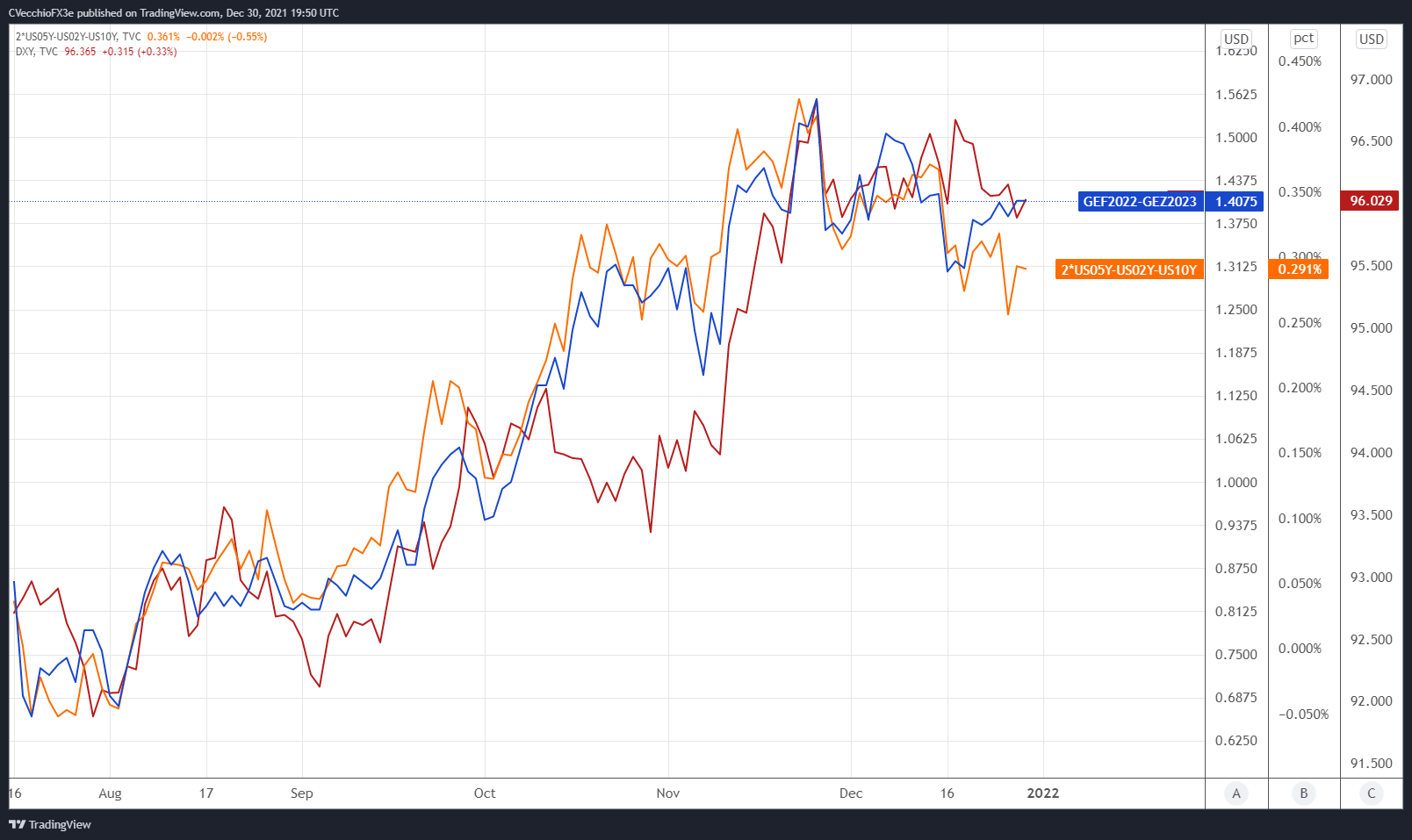

We can measure whether a Fed rate hike is being priced-in using Eurodollar contracts by examining the difference in borrowing costs for commercial banks over a specific time horizon in the future. Chart 1 below showcases the difference in borrowing costs – the spread – for the January 2022 and December 2023 contracts, in order to gauge where interest rates are headed by December 2023.

Eurodollar Futures Contract Spread (January 2022-December 2023) [BLUE], US 2s5s10s Butterfly [ORANGE], DXY Index [RED]: Daily Timeframe (July 2021 to December 2021) (Chart1)

{kind=link}

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly, we can gauge whether or not the bond market is acting in a manner consistent with what occurred in 2013/2014 when the Fed signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

There are 140.75-bps of rate hikes (that’s five 25-bps rate hikes plus a 63% chance of a sixth hike) discounted through the end of 2023 while the 2s5s10s butterfly recently is at its narrowest spread since early-November. It’s worth noting that Eurodollar spreads are less aggressive than they were at their December peak, when there was a 100% chance of six 25-bps rate hikes through the end of 2023.

Federal Reserve Interest Rate Expectations: Fed Funds Futures (December 30, 2021) (Table 1)

Fed fund futures, on the other hand, have become more aggressive over the course of the month. Ahead of the December Fed meeting, Fed funds futures were discounting an 81% chance of a 25-bps rate hike in June 2022 – which would be the first rate hike of 2022. Now, at the end of December, Fed funds futures are pricing in March 2022 for the first 25-bps rate hike with a 63% chance.

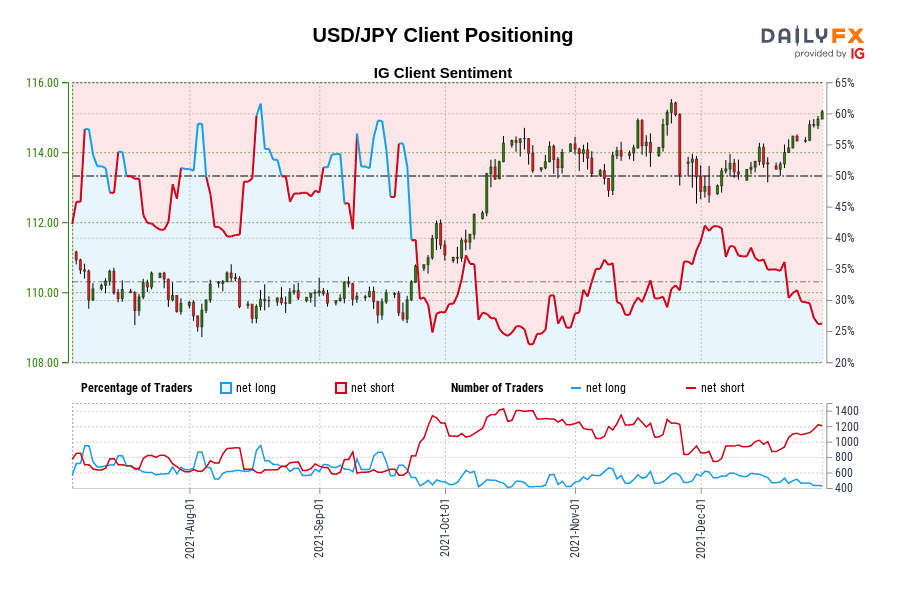

IG Client Sentiment Index: USD/JPY Rate Forecast (December 30, 2021) (Chart 2)

USD/JPY: Retail trader data shows 26.88% of traders are net-long with the ratio of traders short to long at 2.72 to 1. The number of traders net-long is 6.60% lower than yesterday and 17.17% lower from last week, while the number of traders net-short is 3.11% higher than yesterday and 10.25% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests USD/JPY prices may continue to rise.

Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger USD/JPY-bullish contrarian trading bias.

— Written by Christopher Vecchio, CFA, Senior Strategist

Be the first to comment