RAND ANALYSIS

- SARB raises rates by 25bps to 4%.

- Initial reaction: marginal rand weakness

MPC PROVIDES NO SURPRISES LEAVING RAND FAINTLY LOWER

The SARB announced on Thursday that the repo rate will be increased to 4% from 3.75%. Four members of the MPC voted for a rate hike while one member voted against. There was no discussion about a 50bps hike but rather a 0 – 25bps choice. Markets largely priced this result into the rand leading up to the announcement which has led to a marginal weakening in the ZAR against the USD. Any surprise on the hawkish side would have given further impetus to rand strength however, nothing significant resulted from the announcement nor the post-announcement conference.

SARB Summary:

- EM growth to lag due to slower vaccination rates echoing IMF forecast.

- Uncertainty on normalization timing remains.

- Economy estimate to grow faster than potential.

- Yield curve steep.

- Inflationary pressure filtering through to SA reflective in inflation pushing above midpoint of target range. Headline inflation forecast: 4.9% for 2022.

ZAR FUNDAMENTAL BACKDROP

FED HAWKISHNESS

Yesterday’s hawkish FOMC press conference prompted dollar strength across the board particularly against low yielding currencies. The South African rand(high yielding currency) held its own despite the stronger greenback closing only 0.44% lower from the opening price. The carry trade appeal (borrow low yielding currency, purchase high yielding currency) of the rand remains steady while commodity prices look upwards – via Russia/Ukraine tensions on the oil and gas sector.

COMMODITIES

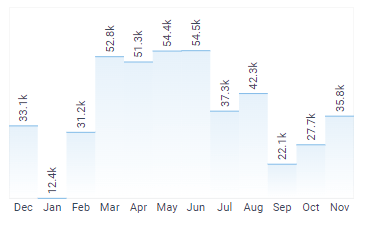

Noteworthy rand-linked commodities including coal, iron ore and platinum have all been appreciating of recent laying a supportive environment for local currency and looks to remain elevated as financial markets largely dismiss COVID-19 fears. An uptick in commodity prices have allowed for the recent rise (surplus) in the South African balance of trade figures shown below:

South Africa Balance of Trade:

{kind=link}

Source: DailyFX

HIGH BETA

With ZAR being a high beta currency with exposure to China (major trading partner) and overall global risk sentiment, there seems to be a tug-of-war between the two opposing forces.

GROWTH

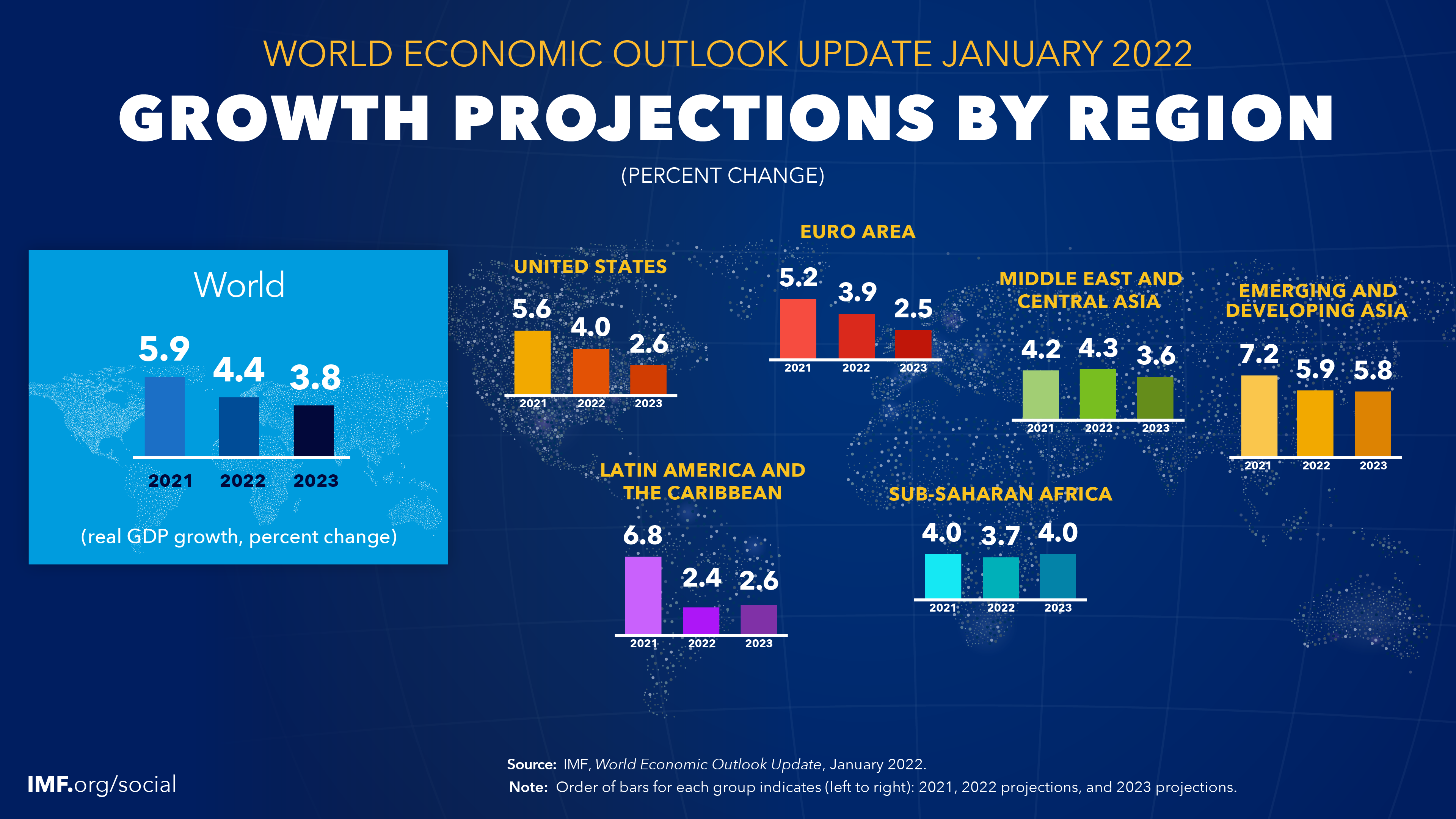

On the growth front, the IMF released it’s 2022 GDP growth forecasts yesterday with an overall revision lower across the globe. South Africa has been projected to grow by 1.9% in 2022 (previously 2.2%) followed by a further decline in 2023 at 1.3% (far lower than the regional average in Sub-Saharan Africa).

IMF Regional Forecast:

Source: IMF

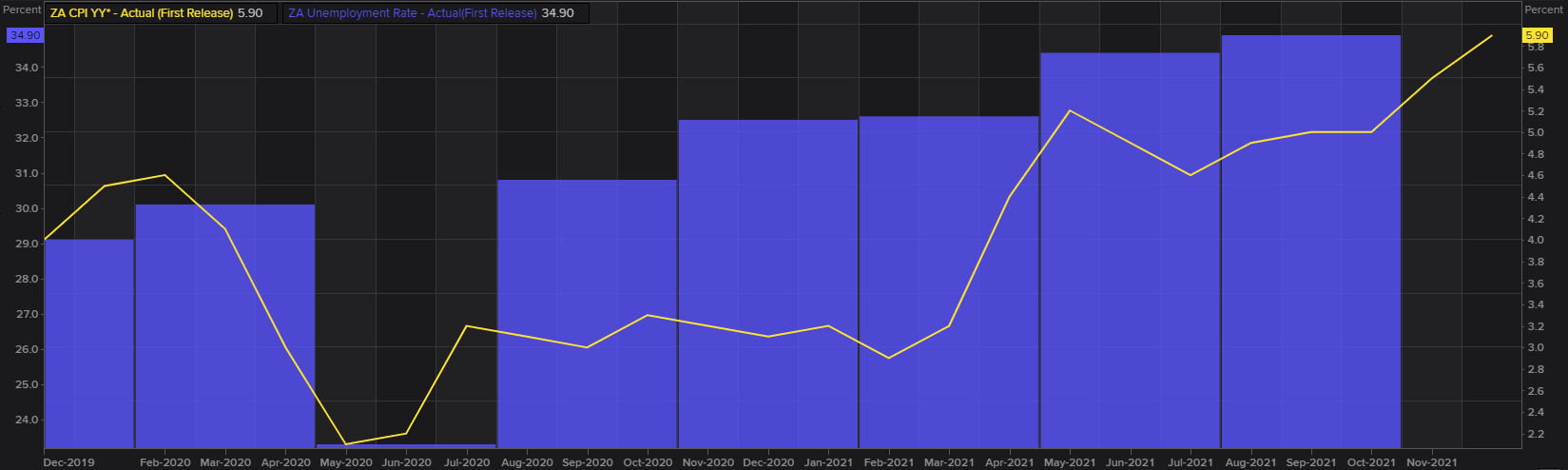

INFLATION AND UNEMPLOYMENT

The challenge facing the SARB and central banks globally is the inflation discussion and whether or not we are seeing peaks or is there more room to run? South Africa is unique in that other Emerging Market (EM) nations have begun the rate hike process in 2021 while the SARB has adopted a more patient approach. Current inflation is increasing but remains within the allotted target and between 3% – 6%. A hasty approach particularly after a Fed focused on rate hikes may unnecessarily hamper an already stifled economy with unemployment figures reaching record highs.

South Africa Inflation (yellow) and Unemployment Rate (purple):

Source: Refinitiv

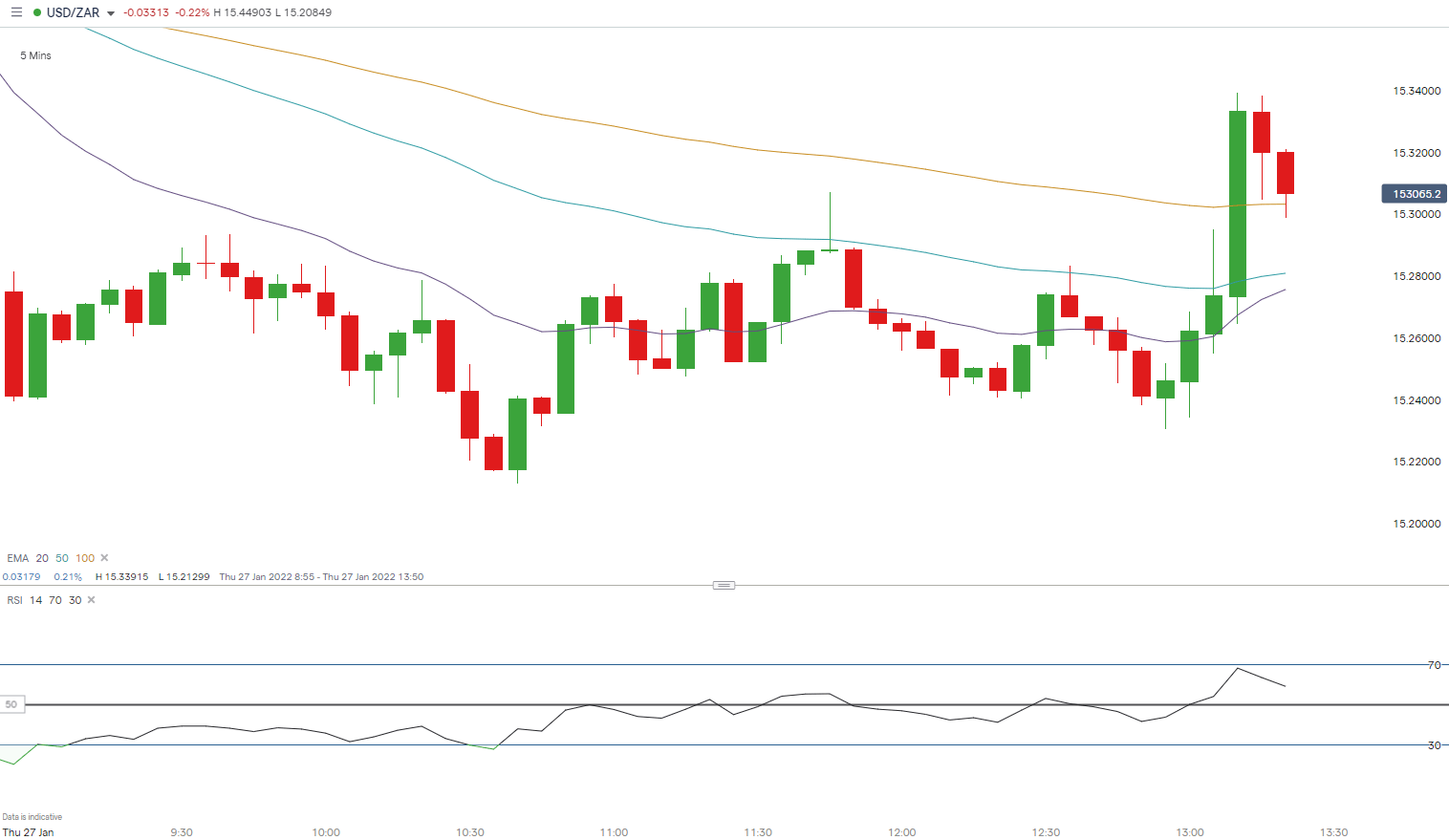

TECHNICAL ANALYSIS

USD/ZAR DAILY CHART

Chart prepared by Warren Venketas, IG

Early response by market participants were supportive of dollar strength but overall relatively muted due to a predictable MPC outcome. We now look forward to U.S. centric data to drive price action.

Contact and follow Warren on Twitter: @WVenketas

Be the first to comment