alexsl/iStock Unreleased via Getty Images

Company Description

eBay (NASDAQ:EBAY) is one of the original multinational e-commerce companies, allowing consumers and businesses to sell to the buying public.

The initial premise was an auction-style website where the public could sell stuff from around their house. It later developed into the website it is now, allowing businesses to trade and for people to buy from around the world.

eBay monetizes these sales through listing, transaction and promotion related fees.

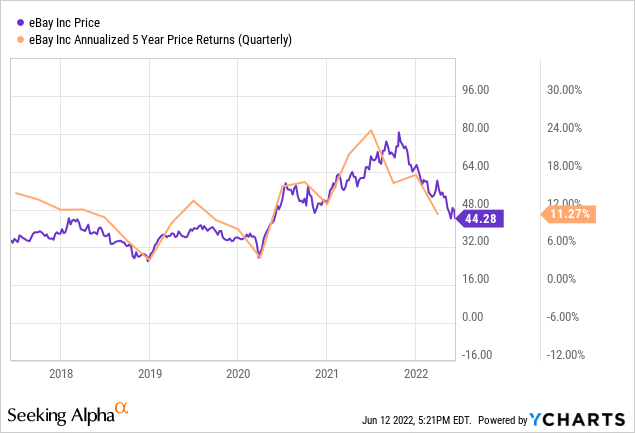

eBay’s share price has been victim of the recent negative sentiment in the market, with the shares down from a recent high of $81.19.

Investment Thesis

eBay is a veteran software business which is no longer in the limelight.

eBay has made many moves in recent years to respond to specialized marketplaces threatening eBay’s hold on various pre-owned markets. We believe this response to be smart for the brand, although it is very early to judge the outcome.

Macro conditions are tough, especially so for a business in retail. Our belief is that eBay could struggle. The shining light is that eBay’s profitability is extremely good, but the growth is not enough to make this worth it.

Our objective is to assess the investability of eBay in the current market conditions. With the market risks we see and the valuation being marginal, it is difficult to suggest investing in eBay at its current price.

Recent Updates

eBay has been branching out the services its marketplace offers. They have recently announced the following:

- eBay vault – This is a secure location where trading cards can be kept. Sellers can use this as both storage but a location within which they can trade. Thus eBay’s vault acts as both a custodian of assets and a marketplace.

- eBay sneaker authentication – eBay has also branched out into sneaker authentication. The benefit for the buy is that it reduces the risk of them buying a fake, which is a major risk and worth paying a premium for.

- eBay watch authentication – Similar to the sneaker authentication offering, eBay will confirm the legitimacy of a watch as protection for buyers.

The one thing these 3 services have in common is hype. Several years ago, you could walk into a Rolex boutique and buy most of their watch models, now you need to spend tens of thousands just for the chance. Sneakers have blown up to the extent that it’s difficult to get your hands on a pair of New Balances (NB 550). Finally, during lockdown, Pokemon cards especially saw an exceptional rise in popularity, culminating in Logan Paul paying $5.2M for 1 card.

This is an interesting strategy from eBay and we believe it is routed in the stagnating brand of eBay. According to Interbrand, eBay was the 36th most valuable global brand in 2011, 10 years later it has fallen to 56th. We would not be surprised if the proportion of young people and those on social media has fallen further. This has the potential to bring eBay back to the forefront of society.

From a financial perspective, it is growth inducing. The biggest risk with buying hype trainers or watches is the item being fake. Removing this risk removes the only barrier for using eBay. In the case of Sneaker, Nike (NKE) is currently suing StockX for selling fakes and so this is a great time for eBay to steal market share. eBay is estimating that the vault will store $3BN in assets within a few years, this will generate substantial revenue annually.

Finally, decades too late arguably, eBay is launching its first digital wallet as a way of replacing the relationship it had with PayPal (PYPL). This will allow customers and sellers to accumulate and hold money on their account, increasing the likelihood of using those funds on the platform. Further, it allows eBay to process the transactions themselves, thus increasing their take-rate.

Macro analysis

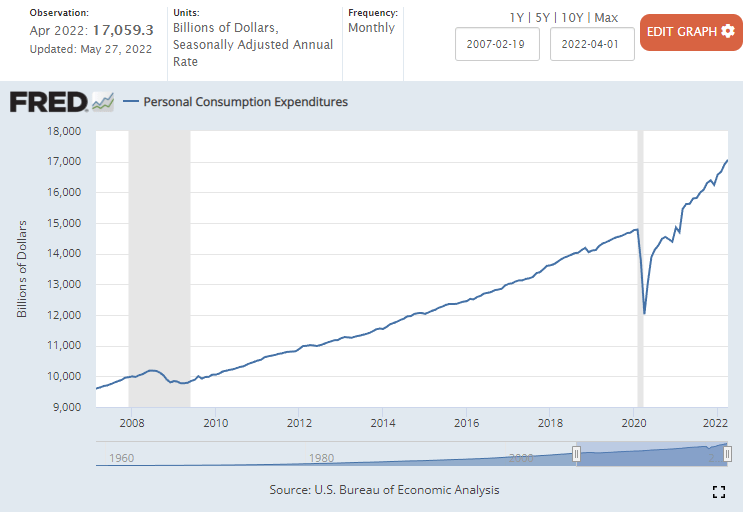

eBay is a consumer-spending-driven business. It makes most of its money when a transaction completes. Therefore, demand in the economy is a key indicator as to how eBay will perform.

When we look at consumer spending, we note strong levels of spending. This is interesting as consumers went on a binge post-COVID, this does not seem to have subsided.

Consumer spending (FRED)

This suggests eBay should experience healthy growth into 2022, with a substantial increase from 2021. The issue with this however is that GDP is made up of more than just consumer spending. As 2009 and 2020 shows, this is not a leading indicator of a recession (grey lines). Consumer spending can easily drop off a cliff soon after.

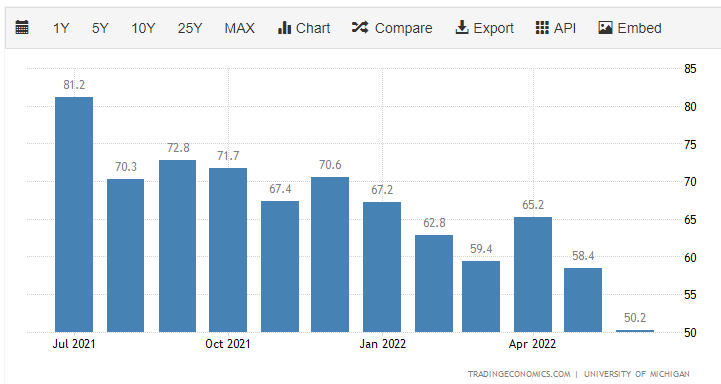

Consumer sentiment is a better indicator for future spending habits and it does not look good. Sentiment has fallen substantially in the last few months.

Consumer Sentiment (University of Michigan)

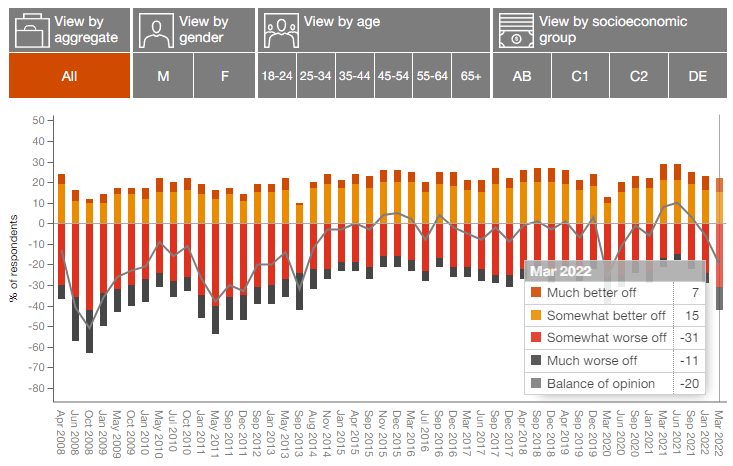

PwC believes this is due to the cost of living crisis we are experiencing as a result of heightened inflation. With more income allocated to necessities, less is available for discretionary spending. The proportion of people who are worse off is staggering. PwC has put together a more detailed graph than the above.

Consumer Sentiment (PwC)

This will inevitably harm eBay’s near-term growth, until economic conditions improve. With the threat of stagflation, this could be a prolonged suffering. A counter argument would be that with wallet’s tightened, people will look for pre-owned goods rather than buying new ones. eBay grew 11.3% in 2007, 2.2% in 2009 and 4.9% in 2010 (Source: TIKR Terminal) and so this argument is not preposterous.

Financials

Gross Merchandise Value (GMV) is a key metric for eBay, it represents the value of goods transacted on the platform. Compared to 2019, eBay has grown 7%-12%. We have purposely excluded 2020, due to the impact of COVID-19. This is mediocre, only being slightly greater than GDP growth in 2019 annualized. eBay has been able to respond by improving its take-rate, the net impact was a 5% decrease of revenue in Q1 2022. Given the economic stimulus and lack of social spending at the time, a 5% fall is fairly impressive.

Management is guiding $9.9-9.6BN of revenue in 2022, which is in line with analyst consensus numbers. This equates to $2.4BN in quarterly revenue. Given the fall in consumer sentiment, our belief is that eBay may come in slightly below this.

eBay is a profit machine. It has a ROCI of 37.5% (When excluding G/L on investments, which is a non-cash, non-trading expense), with an FCF margin of 28% (Source: TIKR Terminal). This is one of the reasons we are not too concerned about growth chugging along at a mediocre rate, the cash-flow conversion is insane. The reason for this is eBay’s position in the market, eBay is still the go to for pre-owned goods.

There is no liquidity risk with eBay. It currently has a net debt position of $3.4BN and an interest coverage ratio of 12.5x.

Advertising

Another area of growth for eBay is its advertising strategy. Historically, eBay allowed solely 3rd parties to advertise on its platform, thus trading potential sales for ad revenue. Now, they are allowing first parties to also advertise. This has the benefit of driving sales on the platform, thus earning eBay income on the ad and sale.

Hidden Assets

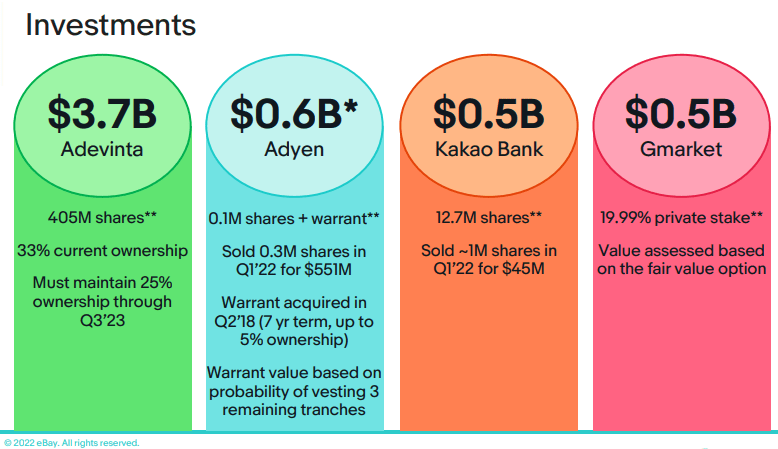

eBay is true to its Silicon Valley roots and is an investor in several tech businesses.

In recent years, eBay disposed of its investment in StubHub for $4BN, its classified business for $2.5BN and 80% of its South Korean operations for $3BN.

The following are the largest remaining investments.

eBay’s investments (eBay)

All of these investments have the scope to turn out like the above, with Ayden (OTCPK:ADYEY) being the crown jewel. eBay has the option to acquire 5% ownership through warrants, which at Ayden’s peak share price of EUR 2,745 represents c. $4.25BN. This represents 18% of the current equity value. eBay has also looked to incorporate Ayden into its marketplace as a payment option, creating the option to share growth.

Much of this cash has been used for buybacks, eBay has repurchased an astounding 20% of its outstanding share count, with c.7BN in shares repurchased last year.

These investments have the potential to create genuine “bonus” value for shareholders and the track record of deal making suggests eBay is competent in this space. The reason we consider this a bonus is due to the value we attribute to eBay’s current operations.

Valuation

We are comfortable with the current operations of eBay, with various areas to get excited about. The valuation must line up however. In order to assess eBay, we have conducted a discounted cash flow assessment.

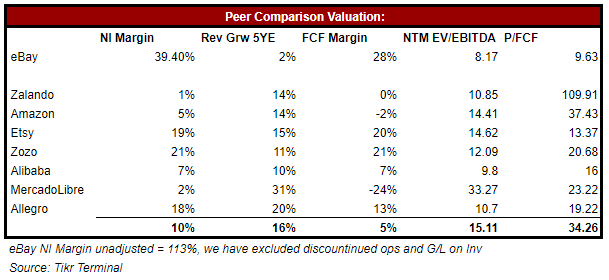

When looking at eBay’s peers, we noted one characteristic which created difficulty in assessing an EBITDA multiple.

eBay’s comp set comparison (Tikr Terminal)

As noted in the table above, eBay outperforms the market in all key KPIs. The issue is that eBay’s forecast growth is extremely poor. As a result of this, markets are assigning a sharp discount. Judgement is required when assessing where eBay’s fair value sits.

Our belief is that an 8x multiple would be fair. Since 2005, eBay has grown revenue at an average rate of 5%, with markets attributing an average NTM EBITDA multiple of 10x (Source: TIKR Terminal). During this same period the average FCF yield was 6.9%, compared to 10.47% today. The growth rate in this case is more valuable, as within 12 years the 2%/10% combination would become inferior and so we must discount this 10x.

Clearly, with eBay trading at 8.10x, an 8x multiple would suggest eBay is fairly valued, but the DCF is worth looking at.

DCF valuation for eBay (Author’s own calculation)

eBay’s cash flows are nothing to be scoffed at. If we assume a perpetual growth rate of 2% and a growth of FCF in the coming years of 2%-3%, we get a valuation of $65.

In normal market conditions, we would assign more weight to the DCF as it factors in both valuation methodologies but here, it is difficult to invest on the cash flows alone.

Final Thoughts

We only want to invest when all of our boxes are ticked but especially when markets are as they are. Sentiment is so poor that the market is regularly falling and so all investments made during this time must be with the downside considered also. In the case of eBay, we believe it is trading around its fair value, on a market-based valuation. Therefore, as much as we like the business, there is certainly further downside potential. With many businesses being oversold, the opportunity cost here is too high. We currently rate eBay a hold.

We will not leave this on a negative note however. eBay is true to its Silicon Valley roots, innovating in many ways to remain relevant. The cash flow conversions and revenue combination is very good, and we see no reason why this cannot continue into the future.

Be the first to comment