akinbostanci/iStock via Getty Images

Introduction

I have close to 50% industrial exposure in my portfolio. Hence, I’m constantly looking at how peers are doing. Not just because I want industry insights, but also because I want to make sure I’m still betting on the right horses. The Dover Corporation (NYSE:DOV) is an industrial company operating in the specialty industrial machinery industry. In this article, I will discuss what I think of this company from a dividend investor’s point of view, incorporating ongoing economic trends. On the one hand, I like the company. Dover has a fascinating business with a strong focus on acquired growth. Its balance sheet is healthy, free cash flow generation is tremendous, and its valuation is good. However, dividend growth is very slow, and its yield is everything but satisfying. While I don’t have the feeling that Dover is missing from my portfolio, the company does offer long-term returns for investors.

Author Portfolio

So, let’s look at the details!

What Dover Is All About

Dover was incorporated in 1947 and is headquartered in Downers Grove, Illinois. With a market cap of $17.5 billion, it’s a top 15 company in the specialty industrial machinery industry. That’s the same industry companies like Honeywell (HON), 3M (MMM), or General Electric (GE) operate in.

All of these companies have one thing in common: they operate in a lot of sub-industries and niches.

It’s hard to summarize these businesses in one sentence. This also applies to Dover.

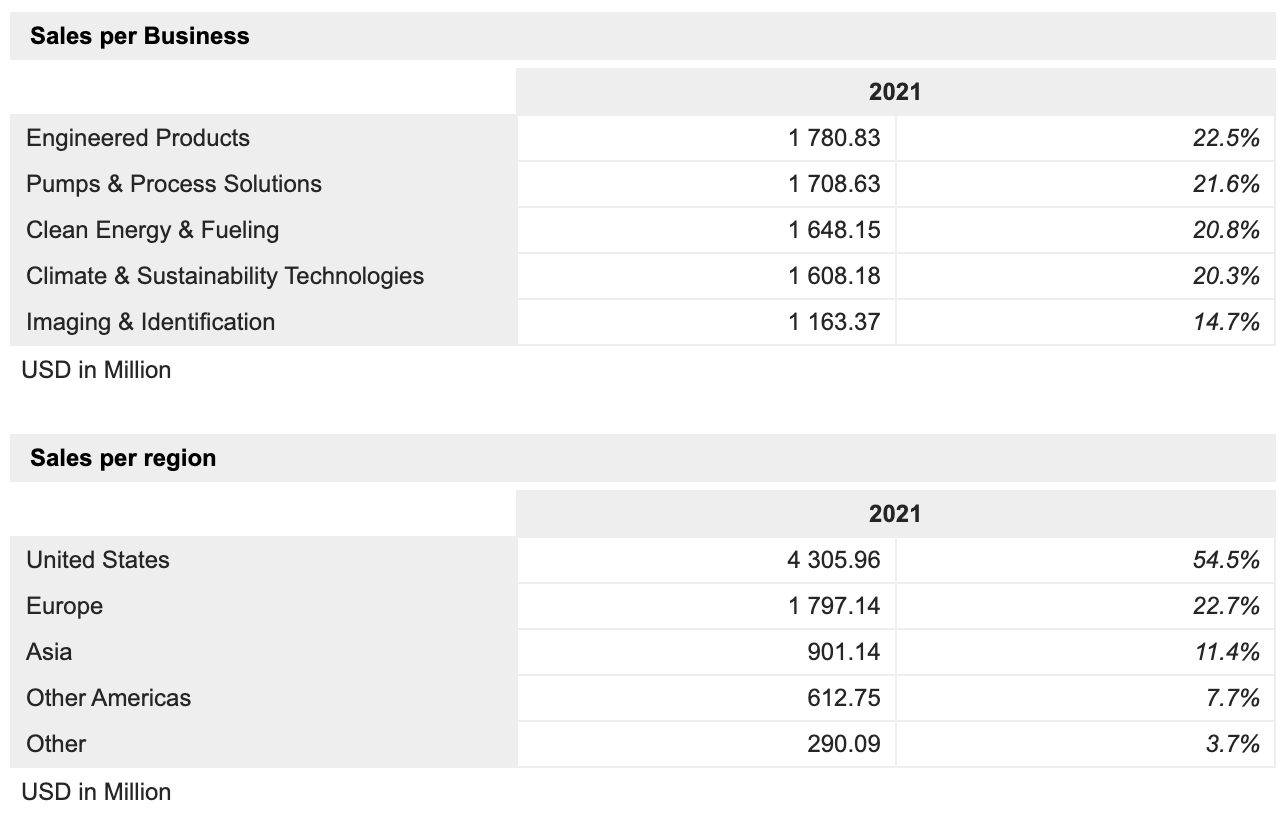

The overview below accomplishes two things. It shows the company’s five segments and it shows backlog strength.

Dover Corp.

The “D”s in front of the abbreviations stand for Dover. The full name of the segments is listed below – just like the company’s geographic sales breakdown showing that roughly half of the total sales are generated internationally.

MarketScreener

Basically, the company’s business segments achieve one thing, they make Dover an industrial leader engaged in more or less all industrial aspects imaginable – to a certain degree.

In its engineered products segment, the company provides a wide range of equipment, components, software, solutions, and services that serve customers in waste handling, aftermarket vehicle services, industrial automation, aerospace, industrial winch/hoist, as well as fluid dispensing.

The pumps and processes segment sells to customers engaging in plastics and polymers processing, chemical production, food/sanitary, biopharma, medial, petroleum refinery, and related.

Clean energy & fueling is one of my favorite segments – if I had to pick one – as it has high exposure to LNG and hydrogen applications. Two “technologies” that I’m a huge fan of. According to the company:

Clean Energy & Fueling segment provides components, equipment and software, and service solutions enabling safe storage, transport. handling and dispensing of clean and traditional fuels, cryogenic gases and other hazardous fluids, as well as safe and efficient operation of retail fueling and vehicle wash establishments across the globe. Among solutions supplied by the segment are dispensing equipment and components for gasoline, compressed natural gas (“CNG”), liquified natural gas (“LNG”) and hydrogen (H2) fueling sites, payment systems, hardware and underground containment systems, vehicle wash systems, as well as asset tracking, monitoring and operational optimization software.

The climate and sustainability segment offers commercial refrigeration, heating, and cooling, as well as container and beverage packaging equipment solutions.

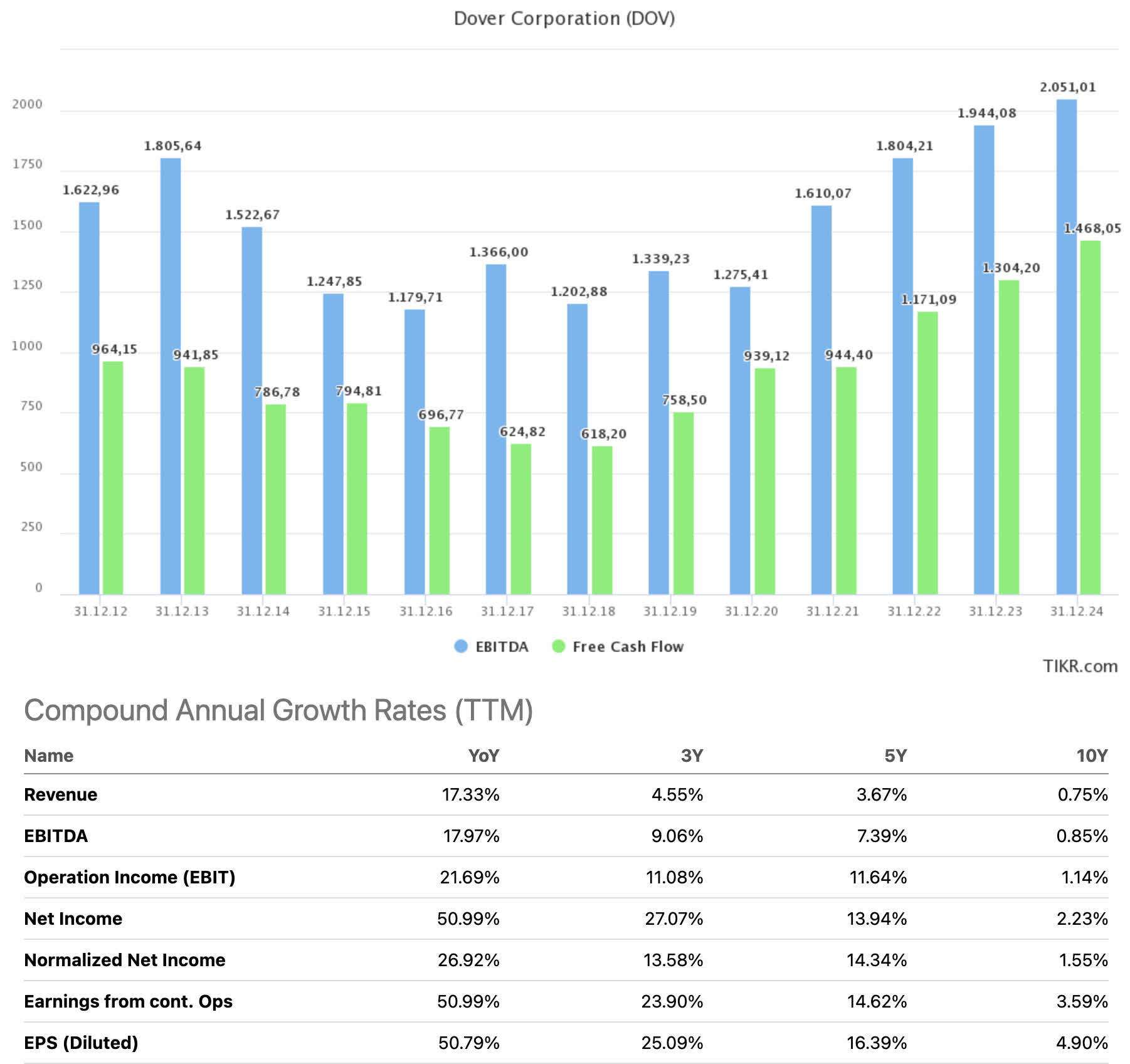

Generally speaking, DOV isn’t known for its high growth rates. Over the past 10 years, revenue has grown by a mere 0.75% per year. This has accelerated over the past five years to 3.7%, boosting net income by roughly 14.0%. Growth is expected to remain above average in the 2 years beyond 2022 – as far as analyst estimates go, for now.

TIKR.com/Seeking Alpha

The best news regarding this uptrend in growth is the fact that organic growth is a major driver. In both 2018 and 2019, organic revenue growth was 4%. In 2020, it was negative 7%. In 2021, it was +15%, followed by an expected surge of 7% to 9% in 2022.

On a long-term basis, Dover aims to grow its revenue by 3-5% per year, and at least above US GDP growth.

One necessary tool to achieve this is acquisitions. The company aims to consistently buy companies that complement its existing products and services. Dover also looks for large M&A opportunities that can fuel long-term growth.

Between 2019 and 2021, the company spent $1.7 billion on acquisitions buying 18 businesses. Between 2018 and 2022 (so far), spending on acquired growth was $2.0 billion consisting of the following businesses:

Dover Corp.

With that said, its slow-growth business is supporting dividends and total shareholder returns.

The Dover Dividend

The relative dividend grades of Dover compared to its industry peers aren’t bad at all. The company scores high on everything except for its yield.

Seeking Alpha

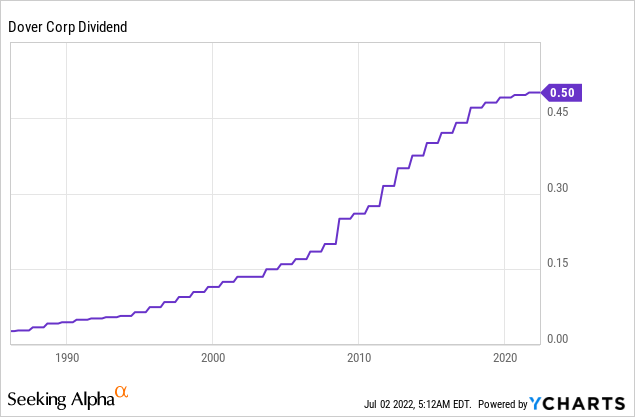

Dover pays a $0.50 quarterly dividend per share. That’s $2.00 per year or 1.7% of the company’s current stock price. That’s roughly 10 basis points above the S&P 500 yield of 1.6%. That’s not a huge difference and far from levels that income-oriented investors consider to be acceptable.

With that said, there’s an issue: dividend growth.

As the dividend scorecard shows, longer-term dividend growth is fine. Over the past 10 years, dividend growth has averaged 9.0% per year. That’s more than decent.

However, dividend growth has slowed down significantly. The 3-year average dividend growth rate is now a mere 1.4%.

These are the most “recent” hikes:

- August 2021: 1.0%

- August 2020: 1.0%

- August 2019: 2.1%

- August 2019: 2.1%

On the one hand, Dover has raised its dividend for 66 consecutive years, making the company a dividend king. Yet, that title doesn’t mean anything for new investors who get a 1.7% yield and a very low dividend growth rate.

There are much better alternatives on the market with both higher yields and higher growth.

Moreover, stock buybacks aren’t that impressive. Between 2017 and 2021, the company reduced the number of shares outstanding from 155.7 million to 143.9 million. That’s a decline of 7.6%, which is okay, but not something that gets me very excited.

With that said, there’s good news. Higher organic growth and a strong backlog of orders are expected to result in accelerating free cash flow. Free cash flow is basically operating cash flow minus capital expenditures. It’s cash a company can distribute to shareholders or use to reduce debt.

Just like its other financials, free cash flow growth between 2012 and 2020 was flat. However, next year, free cash flow could reach $1.3 billion.

TIKR.com

To put things into perspective, $1.3 billion is 7.4% of the company’s market cap. In other words, the company has a lot of room to pay a dividend and repurchase shares. After all, net debt was just 1.7x EBITDA at the end of 2021. Now analysts are pricing in a decline to less than $600 million in net debt by 2024 – just 0.3x EBITDA. Please bear in mind that analysts often do not take buybacks into account. If DOV accelerates buybacks, net debt will end up higher in the years ahead.

Either way, if the company is indeed able to boost free cash flow to almost $1.5 billion in 2024 (8.4% of the current market cap), the company has tremendous opportunities to return cash or engage in much larger acquisitions, if it finds the right targets. I hope that this keeps the company’s young growth streak alive.

Valuation & Current Events

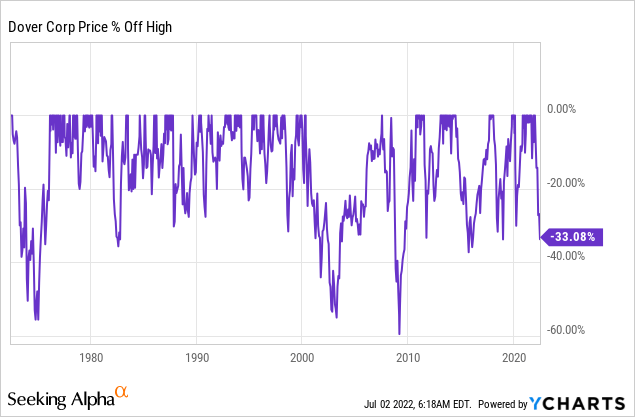

Dover isn’t having a great year. The stock is down 33% year-to-date, which is roughly 13 points below the S&P 500’s 20% drawdown.

FINVIZ

If history is any indication, the stock is offering a good risk/reward. The 2014/2015 manufacturing recession, 2018 sell-off, and pandemic were all similar when it comes to the max drawdown (using monthly closes).

Moreover, when incorporating manufacturing surveys, we see that the stock is now pricing in a (manufacturing) recession.

Author

The high correlation with manufacturing indices isn’t a coincidence. As we briefly discussed, the company is engaged in a lot of manufacturing processes.

Right now, this is hurting new orders.

While organic revenue was up 9.3% in 1Q22, organic new orders were down 4.3%. The pumps segment saw a 14% decline. Climate saw a 9.4% decline. Clean energy orders were down 2.7%.

Basically, the company is being hit by supply chain and demand problems. In its 1Q22 earnings call, the company commented:

Going into the quarter, we had appropriately forecasted the supply chain and input inflation headwinds, but we did not forecast significant geopolitical destabilization nor the return of pandemic challenges in China, which negatively impacted some businesses in our portfolio from a demand and supply chain perspective. We were able to largely offset these unexpected headwinds through robust production performance, particularly late in the quarter on the back of our backlog strength.

While I don’t know what China is up to, the situation remains extremely tense. Especially for companies like Dover, who require smooth supply chains and high orders to maintain a strong backlog. In 1Q22, the company did not comment on potential new orders headwinds related to economic growth weakness. I expect that to change in its 2Q22 call.

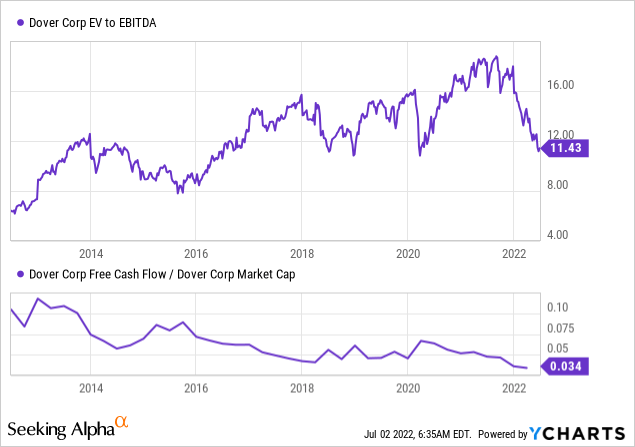

With that said, the company is trading at 9.9x expected 2023 EBITDA. This is based on its $17.5 billion market cap, $1.5 billion in expected net debt, $140 million in pensions, and $1.94 billion in expected EBITDA.

That’s a very fair multiple, which is pretty much the lower bound of the valuation range since 2017. The same goes for the implied 2023 free cash flow yield of 7.4%, which I calculated in this article. It implies the highest rate since 2015.

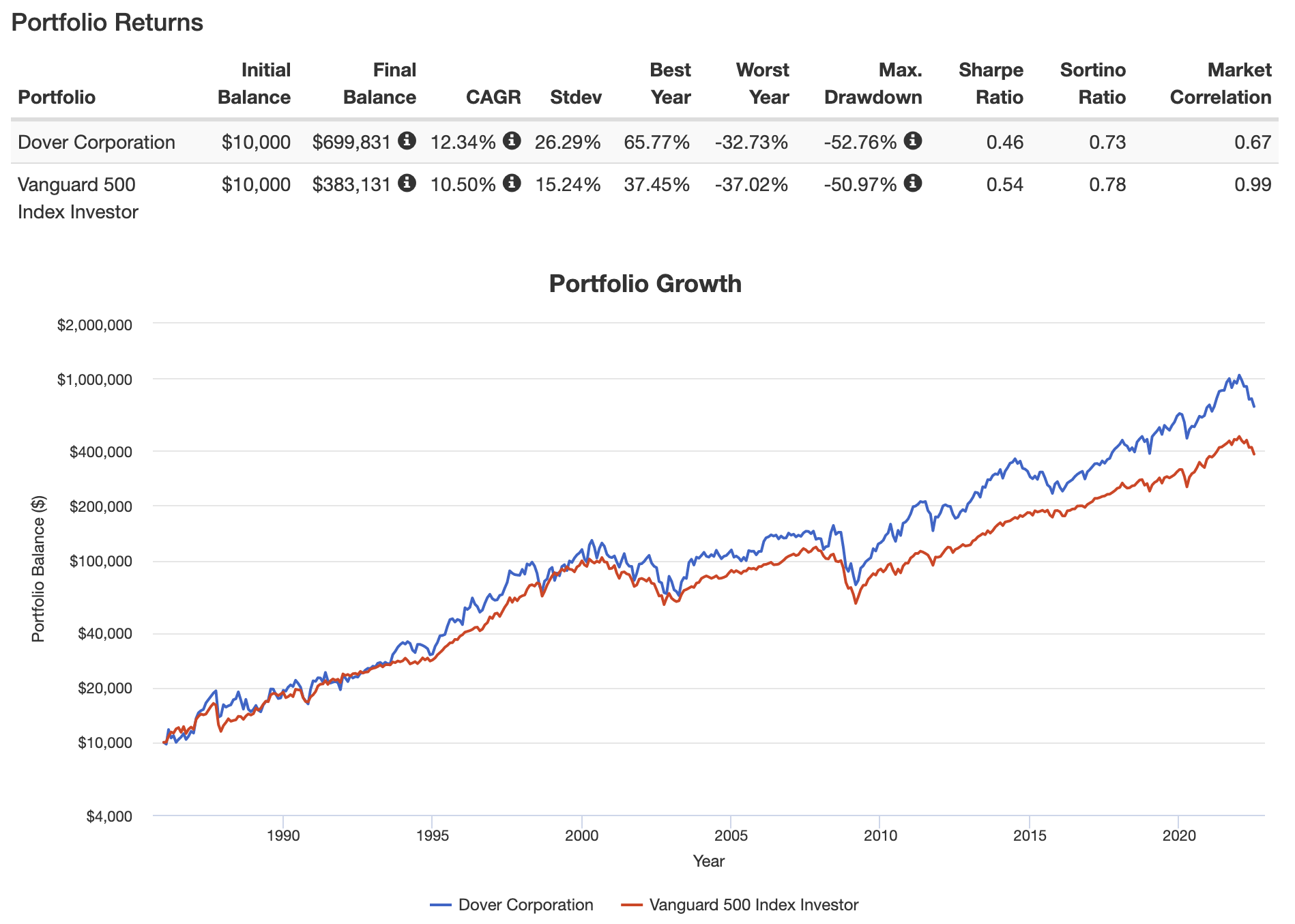

Despite regular sell-offs, Dover is an outperformer. Since 1985, the stock has returned 12.3% per year. This beats the S&P 500 by a couple of points.

Portfolio Visualizer

On a 10- and 5-year basis, we’re still dealing with outperformance. Over the past 5 years, the stock returned 15.4% per year (11.1% S&P 500). Over the past 10 years, DOV returned 15.2% (12.8% S&P 500).

These returns are good, and it does help that DOV follows economic growth indicators so well. It makes timing investments much easier.

Takeaway

Dover is an interesting company. It is a source of income for 25,000 employees and a place where shareholders have gone for steady returns for decades. This dividend king is a part of countless industrial processes thanks to its diverse business model that currently benefits from strong organic growth and acquired growth to remain competitive.

Despite somewhat aggressive M&A, the company has a very healthy balance sheet and impressive free cash flow generation. The implied 7.4% free cash flow yield for 2023 will almost certainly provide Dover with the opportunity to boost dividend growth, buybacks, and balance sheet health.

The company is at a point where it doesn’t make a lot of sense to hold onto free cash flow unless the goal is to become net cash positive (no positive net debt).

In other words, either shareholder returns need to be boosted or the company will have to engage in a major M&A deal. Both are bullish.

It also helps that the market has priced in a lot of economic weakness, which makes the risk/reward rather attractive.

Investors who want exposure should start buying gradually. The market is nervous and it’s hard to tell where the bottom is. For example, buying 25% now and adding over time allows investors to average down if the market keeps falling. If the stock suddenly takes off, investors have a foot in the door.

With that said, I won’t be a buyer. Not because I don’t trust the company, but purely because I have close to 50% industrial exposure already. The 1.70% dividend yield just doesn’t cut it. Moreover, dividend growth has fallen off a cliff. While I do expect dividend growth to pick up, I prefer to buy companies that are hiking more aggressively already. But that’s just a personal opinion based on my own strategy.

The bottom line is that I am giving this stock a buy rating. Not because I expect the stock to take off suddenly, but because the risk/reward has become quite good on a long-term basis.

(Dis)agree? Let me know in the comments!

Be the first to comment