sankai

I covered Diodes Inc. (NASDAQ:DIOD) at length in the article Diodes Inc.: The Growth Story Is (Still) Intact. In this article, I provide an update using the Q2 2022 earnings.

I examine the validity of the growth thesis behind DIOD, explain DIOD’s three-prong strategy to drive growth, and how its rock-solid balance sheet enables it to spur further growth through acquisitions.

Part 1: Growth Thesis Stays Intact

In my earlier article on DIOD, I wrote:

DIOD is a well-managed company that is financially strong and has been growing its top and bottom line over the years, despite operating in a cyclical industry. DIOD is a profitable growth stock that is anticipated by analysts to keeping growing earnings between 15% to 40% for the next few years, which could potentially provide investors with a nice return in 12-18 months.

At the closing price of $73.76 on 20 May 2022, I believe DIOD offers investors an opportunity to invest in a growing company at a price that is below its fair value.

Over the past few months, we have been hearing CEOs and CFOs across the board lamenting declining revenues and earnings, attributing these to a host of well-publicized issues such as supply chain constraints, the tensions between the United States and China, the war in Ukraine, inflation woes softening demands, etc. Therefore, it is very refreshing to hear a slightly more upbeat take from DIOD’s earnings call.

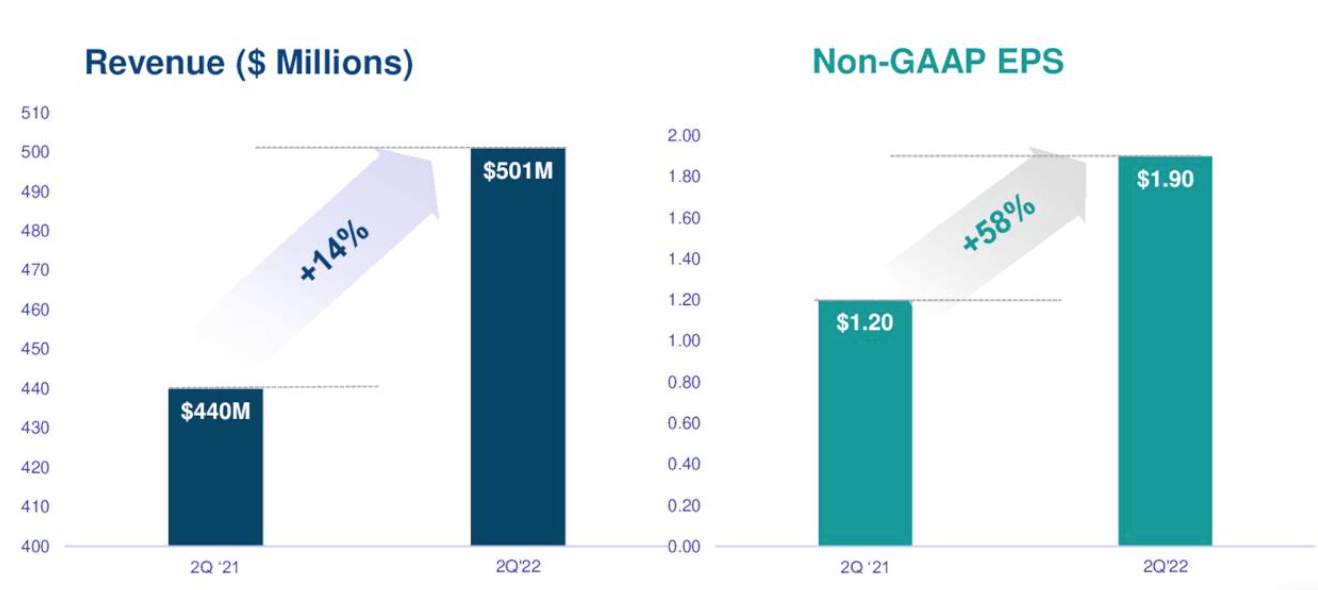

DIOD did well in the latest quarter. In fact, according to management, DIOD’s revenue, gross profit, and earnings have been increasing for 6 consecutive quarters.

Q2 2022 Investor presentation (DIOD)

Year-on-year growth in revenue and earnings per share (non-GAAP) was also at a respectable 14% and 58% respectively.

Q2 2022 Investor presentation (DIOD)

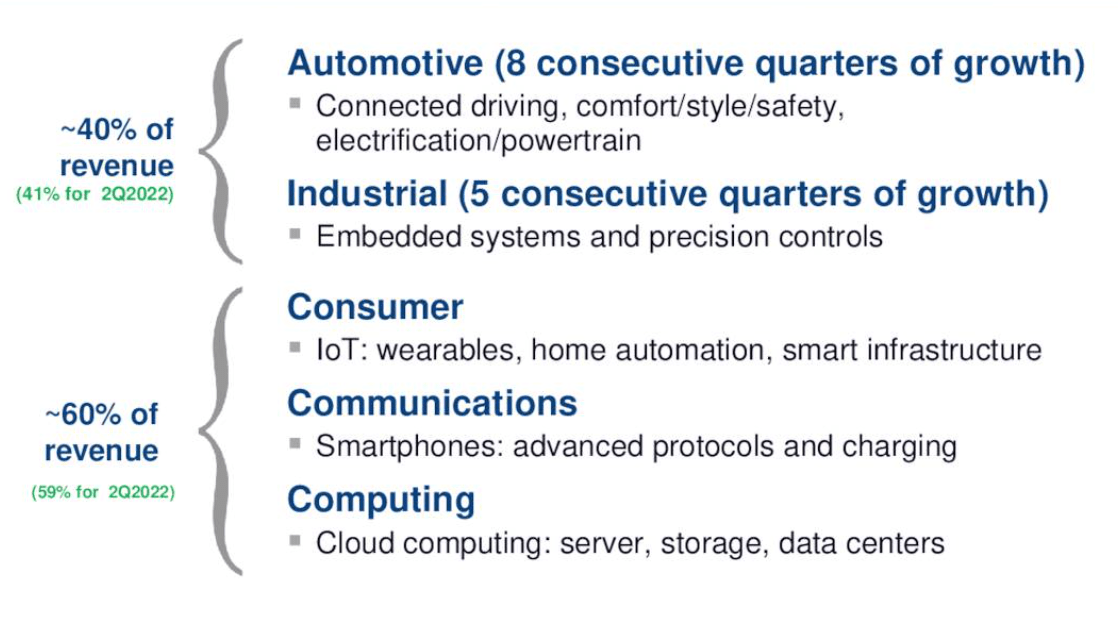

In two out of the five high-growth areas that DIOD focuses on, the Automotive and Industrial segments have been growing revenue consecutively for 8 quarters and 5 quarters respectively. In fact, these two segments are responsible for 41% of the recorded revenue in Q2 2022, up from 39% in Q1 2022.

Q2 2022 Investor presentation (DIOD)

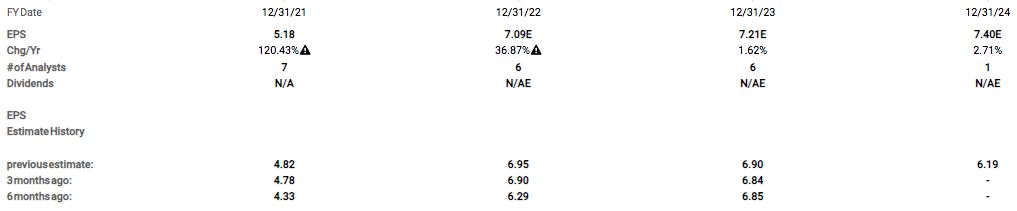

Analysts have also been increasingly bullish about DIOD. Over the past 6 months, analysts have been increasing their adjusted operating earnings per share forecast for DIOD for FY 2022 ($6.29 to $7.09), FY 2023 ($6.85 to $7.21), and FY 2024 ($6.19 to $7.40)

FAST Graphs (DIOD)

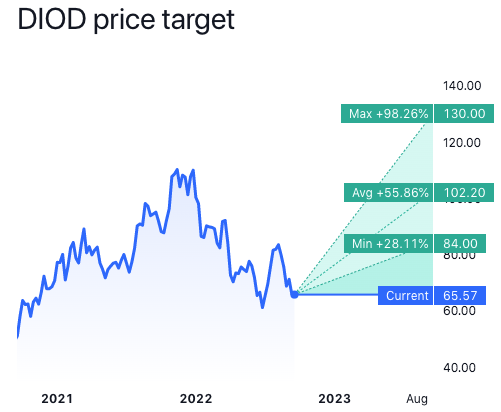

Analysts’ one-year price targets for DIOD continue to look robust suggesting lots of room for upside.

TradingView (DIOD)

The question is of course: How did DIOD accomplish all these especially when headline inflation news suggests a worsening economic outlook?

Part 2: DIOD’s Three-Pronged Strategy Works

DIOD has three strategies to keep growing.

Strategy 1: DIOD’s products are used across multiple end-user product categories

Strategy 2: Each of these categories promises a huge total addressable market.

By (1) having products that can be used in different end-user product categories (2) being sold in 5 different high-growth segments, this affords the company the flexibility to shift the production in a segment experiencing slower growth to one benefiting from higher growth. These 5 high-growth segments are found in:

- Automotive: connected driving, comfort/style/safety, and electrification/powertrain

- Industrial: embedded systems, precision controls, and IIoT

- Consumer: IoT, wearables, home automation, and smart infrastructure

- Communications: smartphones, 5G networks, advanced protocols, and charging solutions

- Computing: cloud computing, including server, storage, and data center applications

This was how the CEO Keh-Shew Lu put it during the Q2 2022 conference call:

When we designed the product, we designed it such that they go to multiple in market, okay? So for example, if you design a product for this play in the PC, that product can be used in automotive.

Emily Yang, the Senior Vice President of Worldwide Sales and Marketing, elaborated on this strategy with the following explanation:

Within the same end market, there are still different areas that with strong demand and definitely some softness. So what we’ve been doing in order to achieve the record is actually shifting our capacities to really support the good focus areas that will continue…

With communication, I think everybody knows that we have slowed down, especially China smartphone area. But within communication, again, we have a record, right? So how do we do that? We’re still seeing a lot of strength related to 5G enterprise-related networking optical area. So again, that’s how we achieve the record. So basically utilize the capacity…

Computing, even within computing, low MPCs, motherboards, definitely, we’ve seen softness. But anything related to enterprise, cloud computing server storage, we’re still seeing strength in that area.

Management demonstrated keen insights in the sub-segments within each of the 5 major high-growth areas and showed nimbleness in adjusting to the varying demands, so in spite of declining growth in certain sub-segments, the company is more than able to make up for the slack in higher growth sub-segments.

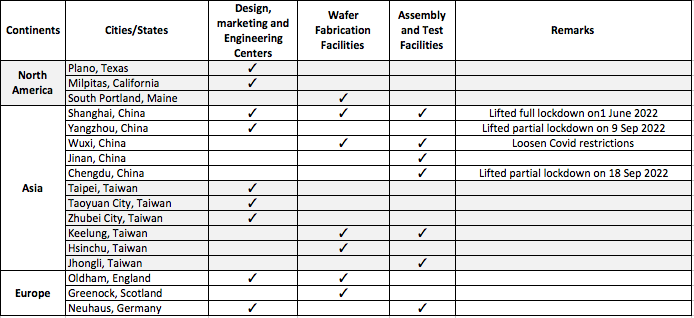

Strategy 3: DIOD established multiple production facilities across three continents to manage supply-chain shocks

DIOD has numerous facilities located across 17 cities over 3 continents. There were definitely concerns that in the face of China’s zero-covid policy and the resulting city-wide lockdowns production will slow.

Author

DIOD’s decision to locate its facilities across the world helped to mitigate these issues as well as other supply-chain disruptions.

Part 3: Driving Future Growth With Acquisitions

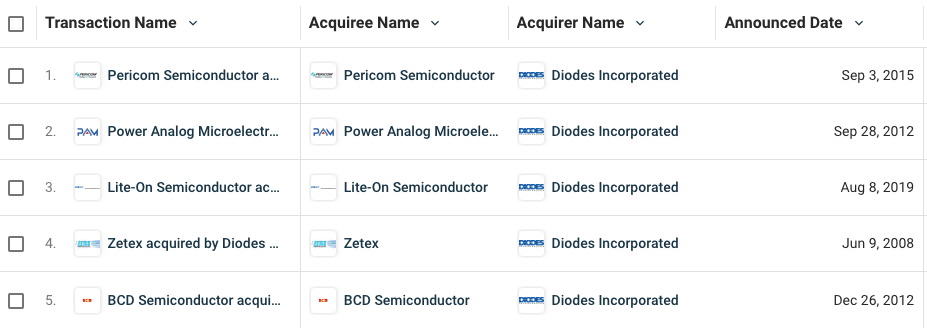

To understand DIOD’s growth story, one needs to understand DIOD’s modus operandi. DIOD has grown through numerous acquisitions over the years. Acquiring a business is not a guaranteed approach to doing well. There are many botched acquisitions that one can think of (e.g. Sprint and Nextel Communications, for starters). However, the management at DIOD has a knack for acquiring businesses that complement well with its existing portfolio. In the past ten years alone, DIOD has acquired five other semiconductors as well as analog and power integrated circuits companies that produce products that align well with its growth strategy in the five high-growth areas.

Crunchbase (DIOD)

Take the 2015 acquisition of Pericom Semiconductor for instance. Pericom products are now responsible for supporting the company’s growth ambitions in the Computing and Consumer end-markets, setting a record seven consecutive quarters of growth in the most recent quarter. The 2019 acquisition of Lite-On Semiconductor (LSC) was another good example. After the acquisition, CEO Dr. Keh-Shew Lu, said,

We are very pleased to complete the acquisition of LSC, which will be immediately accretive to Diodes’ earnings per share and represents the next significant step in executing our strategic growth plan. This acquisition broadens our discrete product offerings, including providing us with a leadership position in glass-passivated bridges and rectifiers that will allow us to further extend our position in the Automotive and Industrial market spaces consistent with Diodes’ overall growth strategy.

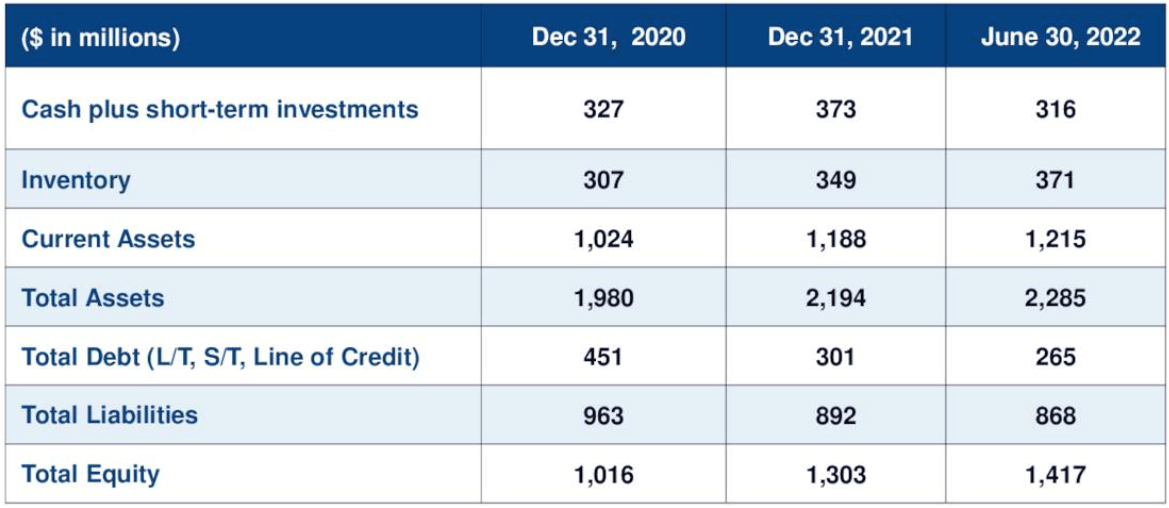

DIOD has $1.21 billion in current assets, $316 million in cash and cash equivalents, and just $265 million in total debt, meaning management can simply pay off all the debt and still has $51 million left. In my opinion, DIOD’s rock-solid balance sheet is well-positioned to make future acquisitions with ease.

Q2 2022 Presentation (DIOD)

Risks To The Growth Story to Consider

I am no fanboy of any company, especially those that I have a Buy/Strong Buy rating because I do invest my hard-earned monies in these companies, so I try to be as clear-eye as I possibly can by playing devil’s advocate.

Is The Growth Story Really Intact?

Naysayer 1 May Say:

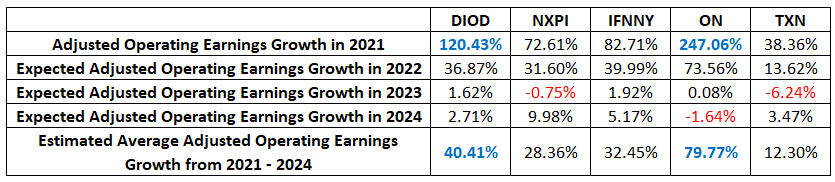

Yes, DIOD’s recent growth has been impressive. From 2020 to 2021, DIOD boasts growth of 120% in adjusted operating earnings, 105% in operating earnings, 67% sales growth, and 41% in free cash flow. To put it mildly, DIOD has done well.

However, analysts also do not think that these growth rates can be sustained. They have already projected an expected adjusted earnings growth rate of 36.87% in 2022 which is a significant decline from 2021’s 120%. They are also projecting a more anemic 1.62% growth in 2023, and 2.71% growth in 2024. In fact, the consensus growth estimates across the board for companies in DIOD’s peer group (see table below) is a huge decline from the high double-digits in 2020 and 2021 to low to mid-single digit earnings growth rates in the next two years.

Adjusted Operating Earnings Growth Rate (Peers)

This sudden surge in growth experienced by all these companies has been largely attributed to the chip shortages in 2020-21 and therefore not to be repeated.

James, wouldn’t that kill the “growth story” straightaway? Duh.

My Response Would Be:

Hold your horses. Yes, I agree with the fact that chip shortages contributed to the growth spurt in 2021. However, one should not sell DIOD short, nor any of these companies, just because of that. One fact does not make a story complete.

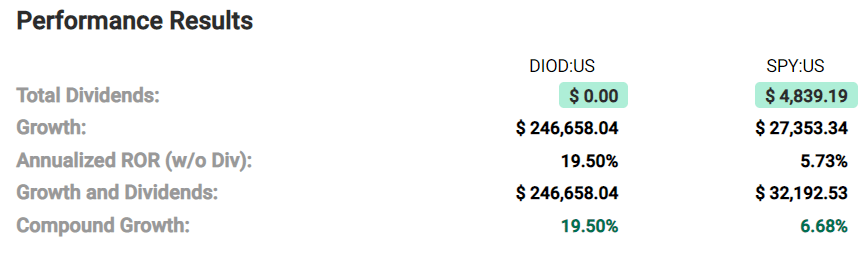

Here is a fact for us to chew on. Even before the pandemic, in the period from January 2002 to January 2020, DIOD performed admirably with a compound annual growth rate of 19.5%, easily besting S&P 500’s 5.73%.

Performance (DIOD)

That meant that $10000 invested in DIOD in 2002 would have turned into a sweet quarter of a million dollars 18 years later, versus the $32k one would have gotten from investing in the S&P 500. And to put things in further context, the 2002-2020 period was a wild roller-coaster ride that included The Great Recession in 2008-2009, three periods of negative growth in the semiconductor industry (2011-2012, 2015-2016, 2019-2020), and the start of the trade war with China in 2019.

That should be a testament to DIOD’s ability to grow under both normal and stressful circumstances.

Naysayer 2 May Say:

Isn’t DIOD a tiny company compared to the peers you showed earlier? How can you expect DIOD, a $3 billion market cap company, to compete against the big boys like the $29 billion market cap ON Semiconductor (NASDAQ: ON) and $42 billion market cap NXP Semiconductors (NASDAQ: NXPI) and outperform them?

My Response Would Be:

To be clear, I am certainly not claiming that DIOD is the best company among this peer group. DIOD is practically a minnow in this group of much larger companies. For instance, all the peers above have operating earnings exceeding several billion dollars in the last twelve months while DIOD only made $338.82 million (TTM) in operating earnings.

However, I like DIOD for two reasons. It is cheap and good.

Let me elaborate.

Cheap

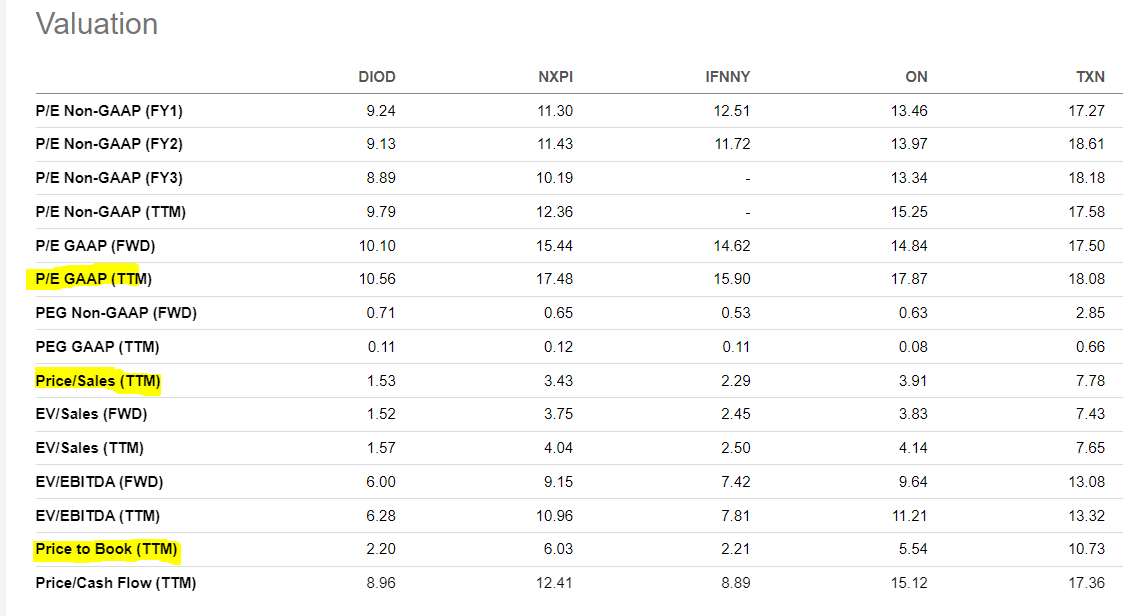

For a stock that typically trades at a blended PE of 22.15 to be trading at a PE GAAP (TTM) of 10.56 now indicates a very strong value proposition, and with DIOD continuing to post quarter after quarter of growth, this company is no value trap.

When compared across varying metrics such as PE, PS, and PB, DIOD is also much cheaper compared to its peers.

Seeking Alpha Valuation (Peer)

Good

DIOD is no slouch. It’s explosive sales growth in 2021 was more than twice its nearest rival in this peer group, and if the forecasted sales growth from 2022-2024 comes to fruition, DIOD will also experience the highest 4-year average sales growth at 21.14% among this peer group.

Likewise for the adjusted operating earnings growth rate of these five companies.

Adjusted Operating Earnings Growth Rate (Peers)

Although ON Semiconductor topped this group in terms of adjusted operating earnings growth in 2021, as well as the estimated average adjusted operating earnings growth rate from 2021 to 2024, DIOD came in a strong second ahead of the remaining competitors.

When I compared DIOD to its larger peers over different time periods, I observed that DIOD performed well in the pre-pandemic years too and not just during the pandemic period (I chose 2019-2022 for that comparison). DIOD even outperformed the peer group over an 18-year period from 2002 to 2020 as well as a 5-year period from 2015 to 2020.

Annualized ROR over different time periods (Peers)

Note: By the way, these timeframes were not cherry-picked to make DIOD shine or for me to make a point. The FactSet data I gleaned through FAST Graphs could only go back 20 years to 2002 so that I the earliest I could set the start year. The 2009/10 to 2020 period is selected to factor in the effects of The Great Recession, together with the rise of the age of smartphones. The 2015/16 period was chosen to study how these companies did when the semiconductor industry went into a downward cycle in 2015 and 2019.

Conclusion: The Bull Case for DIOD

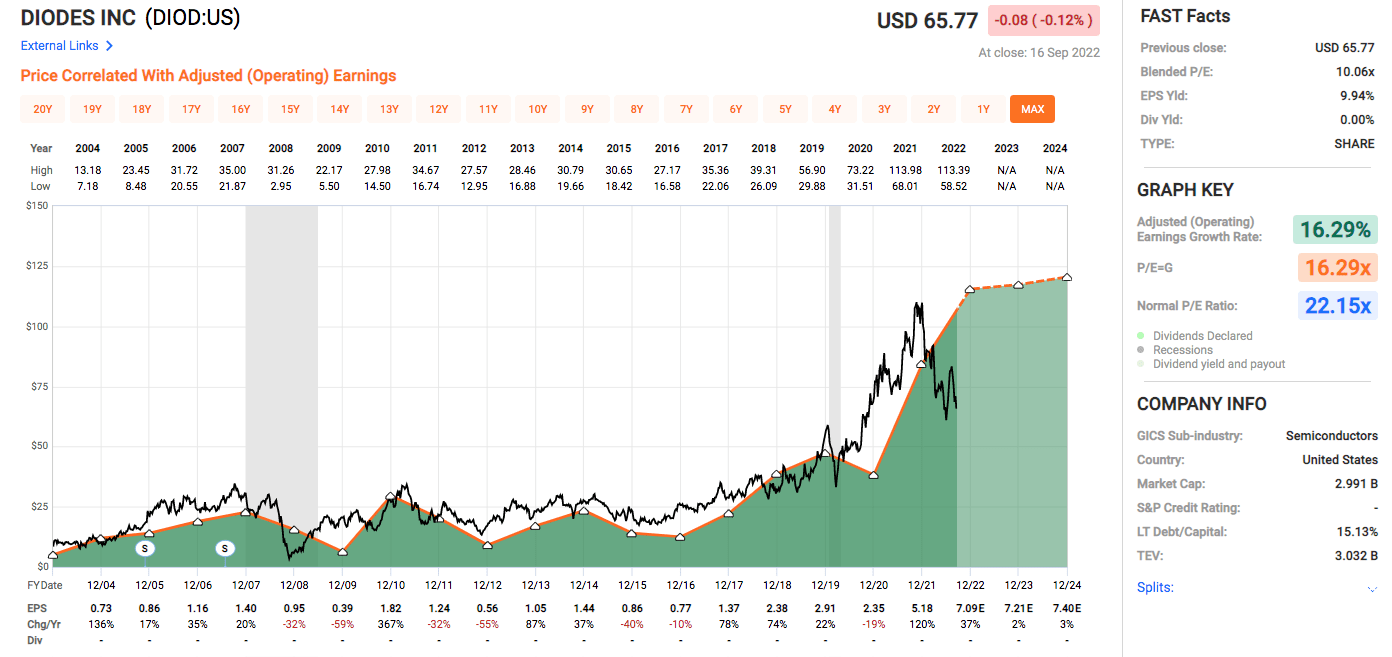

There is certainly no risk-free investment, and most certainly not in the cyclical semiconductor industry. When I wrote my first article on DIOD in May, the stock price was $72.13. It went up 16% to $84.17 on 3 August before falling 21% to $66 at the time of writing this second piece on DIOD. The volatile stock price is just how Mr. Market works and is not reflective of the fundamentals of the company. As seen below, over the long term, the stock price generally moves in tandem with the earnings. As earnings grow, the stock price grows with it.

FAST Graphs (DIOD)

DIOD’s three-prong strategy keeps it nimble and adaptable in challenging macroeconomic conditions to keep growing revenue and earnings. With its solid balance sheet, low valuation, and successful long-term history of outperformance against its larger peers, DIOD is one to consider owning. By being the cheapest among the selected peer group, and for the growth in earnings and revenue that DIOD has achieved in 2021 and is expected to achieve in the next 2 years, I would say DIOD provides a favorable risk-reward opportunity for investors interested in this industry. With the stock price becoming further depressed due to the continued market selloff in the broader markets in 2022, the current attractive entry price for DIOD is a gift for long-term investors.

Be the first to comment