Thomas Lohnes/Getty Images News

Investment Thesis

Year-to-date Commerzbank (OTCPK:CRZBF) is up about 8% while Deutsche Bank (NYSE:DB) shares are down some 20%. The smaller German lender is even trading at a small premium to tangible book relative to DB. From the current vantage point, Commerzbank still looks like the better pick largely due to a stronger capital position which should allow it to do an extra buyback next year, all else equal.

I think a key risk for Commerzbank is its still large Russia exposure at 1B EUR, while DB will take a hit to tangible book if the dollar rally reverses.

While rates are still rising, current expectations are that they will peak sometime in 2023, which would be a boost to Deutsche bank’s less interest rate sensitive Investment banking and Asset management segments.

In this article I will go over the Q2 results of the two banks and compare them at the end.

DB Company Overview

Deutsche Bank operates in four key segments, namely the Investment Bank at around 40% of Q2 2022 revenues, Asset Management at 10% of Q2 2022 revenues, the Private Bank at 32% of Q2 2022 revenues, and the Corporate Bank at circa 23% of Q2 2022 revenues.

DB Q2 Overview

Deutsche Bank reported a RoTE of 7.9% in Q2 2022, with tangible book growing 2% Q/Q to 25.68 EUR/share, driven by organic earnings and 0.95B EUR gain in other comprehensive income, mainly the result of currency gains.

CET 1 capital improved by 14 basis points to 13% with no substantial release of risk-weighted assets (RWA) from the capital release unit (CRU). As a reminder, the CRU continues to hold a disproportionately large amount of operation risk RWA (32%) relative to the rest of the bank (just 6.7% of total RWA):

| DB Total RWA | Of which in the CRU | |

| Operational Risk RWA | 59 | 19 |

| Market Risk RWA | 28 | 1.8 |

| Credit Valuation Adjustments | 5 | 0.6 |

| Credit Risk RWA | 278 | 3.6 |

| Total | 370 | 25 |

Source: DB Q2 2022 Results presentation and Earnings report.

CET 1 capital included a provision for dividends of 450M EUR and was 253 basis points above the maximum distributable amount (MDA) requirement. With a 2.1B EUR profit attributable to shareholders for the six months ended June 30 2022, we see that the current payout ratio is around 20%.

Turning to the 2022 outlook, Deutsche Bank confirmed its revenue guidance of 26-27B EUR (2021 25.4B EUR), its 8% RoTE target, as well as its cost of risk guidance of 25 basis points. The cost/income ratio guidance deteriorated however, with the previous target of 70% now seen as mid to low seventies.

Despite some near-term difficulties, the bank confirmed its 2025 targets:

For 2025, the bank targets compound annual revenue growth of 3.5-4.5%; post-tax RoTE of greater than 10%, and a cost/income ratio of below 62.5%. The bank also reaffirms its aim for cumulative capital distributions of around € 8 billion in respect of the years 2021 – 2025.

Source: Deutsche Bank Q2 2022 Interim Report

DWS

DWS, in which Deutsche Bank holds a 79.5% stake, is the most impacted segment of the bank given the current market and economic environment. The asset manager saw its assets under management drop 7.7% quarter-over-quarter to 833B EUR, driven by market developments and a 25B net outflow, mainly in cash products. Still adjusted profit before tax came in at 273M EUR, down 2% Q/Q but up 11% year-over-year.

DWS is trading at a 0.74 price to book when taking into account its intangible assets, or 1.5 times its tangible book value, very health compared to Deutsche bank’s 0.34 price-to-tangible book value.

Commerzbank Company Overview

Commerzbank operates in two main divisions – Private and Small Business Customers (PSBC) at 65.8% of underlying Q2 2022 revenues, of which Polish majority-owned (69.3% Commerzbank stake) subsidiary mBank accounted for 17.4% of underlying Q2 2022 revenues, and Corporate Clients (CC) at about 38.9% of underlying Q2 2022 revenues.

Commerzbank Q2 Overview

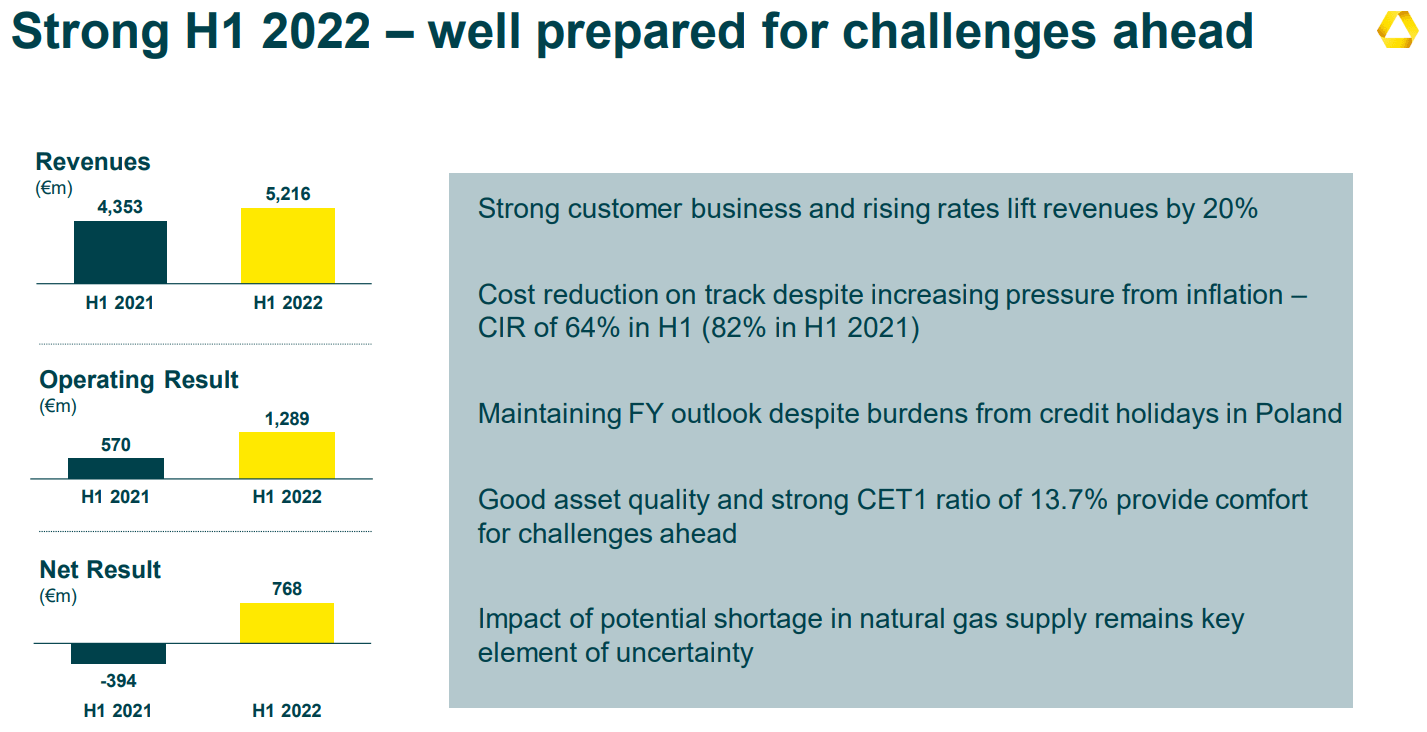

Commerzbank reported a 6.7% net RoTE helped by 111M EUR (4.5% of Q2 2022 revenue) of exceptional revenue items. Tangible equity grew by 2.85% Q/Q to 20.12 EUR/share driven by operating earnings:

H1 2022 Highlights (Commerzbank Q2 2022 Results Presentation)

CET1 capital improved by 20 bps to 13.7% which is a very comfortable buffer to MDA of around 430 bps. The CET1 ratio includes a 30% provision of H1 profits for dividends.

Looking ahead, Q3 will be burdened by a 210-290M EUR negative impact from the Polish mortgage holiday. Commerzbank’s mBank stake is currently worth around 1.3B EUR, with mBank stock down 50% year-to-date. However despite the crash, mBank is still trading at a P/B of around 0.69 or almost twice as high as Commerzbank’s 0.36 price-to-tangible book.

The headwinds in Poland aside, Commerzbank confirmed its target of a net result of above 1B EUR, absent further deterioration in the economic environment or incremental Swiss franc provisions.

Comparing the two banks

Now that we have seen how the two banks are doing, let’s compare their key performance indicators:

| Commerzbank | Deutsche Bank | Commerzbank/DB Comparison | |

| RoTE | 6.7% | 7.9% | -1.2% |

| Tax Rate | 31.3% | 21.8% | +9.5% |

| Cost/Income Ratio | 64.3% | 73.2% | -8.9% |

| P/Tangible book | 0.36 | 0.34 | 0.02 |

| CET1 Capital | 13.7% | 13% | 0.7% |

| MDA Requirement | 9.42% | 10.47% | -1.05% |

| MDA Buffer | 4.3% | 2.53% | 1.77% |

Source: Author’s calculations based on Q2 2022 company disclosures

The first thing that stands out is that despite a lower Cost/Income ratio Commerzbank delivers an inferior RoTE thanks to a higher tax rate. As the geographic mix of revenues should stay fairly constant in the coming years this should prove to be a boost for Deutsche Bank over the long term.

The second thing to note is that Commerzbank has a much higher buffer to its MDA, which implies two things. Firstly, it may absorb more losses before it has to raise capital. Secondly, it should be the first of the two banks to do an extra buyback all things equal.

One thing to point out is that DB is gradually winding down its capital release unit which holds some 25B of RWA and no contribution to earnings, meaning as it is gradually wound down (which would also RoTE by about 1%) it could boost CET1 capital to 13.94%, a level even higher than Commerzbank.

However as things stand, Commerzbank comes out ahead on CET1 capital. In fact, it is sitting on a 1.22B EUR capital buffer which it could use for buybacks and still get to a CET1 of 13%, on par with DB. With a market cap of around 9B EUR, the buyback would be enough to retire some 13.4% of the shares, in effect boosting the tangible book by 10% to about 22.11 EUR/share.

It is important to note is that Commerzbank is still sitting on a larger Russia exposure of about 1B EUR net which will delay any plans for a buyback, especially against the gas situation background.

Investor Takeaway

Both banks are attractively valued. Commerzbank should outperform over the next year if it manages to do an extra buyback. Looking further ahead, perhaps Deutsche Bank will come out on top thanks to a wind-down of its Capital release unit, a stronger underlying profitability and a more favorable geographic revenue mix from a tax perspective.

Personally I like both banks and will continue to hold a diversified position in the two lenders.

Thank you for reading.

Be the first to comment