JacobH

There’s no question that 2022 was a good year for Denison Mines Corp. (NYSE:DNN). The company made meaningful progress in testing in-situ recovery (“ISR”) processes in the Athabaskan soil, and, in the process, substantially de-risked its Phoenix Project. Management also recently announced that investors should expect to see the release of Denison’s Feasibility Study (‘FS’) in the first half of 2023.

That event will be key as it will provide much needed cost and timeline updates to Denison’s 2018 PFS targets, some of which management has already indicated will not be met. This may be one of the reasons why, using some measures, Denison shares currently trade at a deeper discount than other developers in the Basin. In this article, we’ll discuss how the FS may impact Denison’s share price.

Company Background

As discussed in a previous article, Denison is currently focused on developing its Wheeler River property. The project is slated to come online in two phases with the first, named Phoenix, utilizing the lower-cost ISR method to be followed by the second phase, named Gryphon, which will use conventional underground mining techniques.

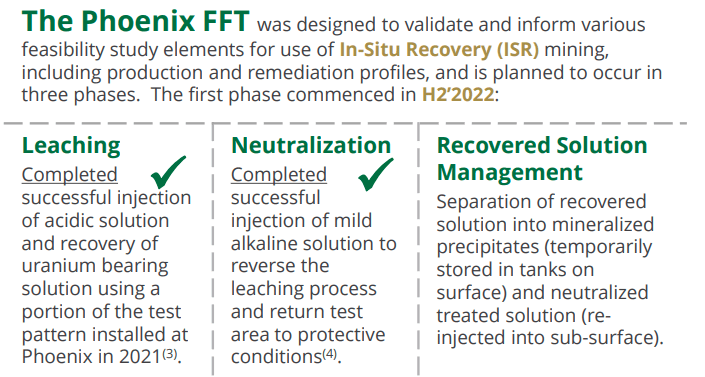

The company intends to be the first uranium miner to use ISR on Canadian soil, and in the Fall of last year announced that it had successfully completed two out of the three steps necessary to do so. It is currently working on the third step, outlined below, which should be completed by mid-year.

Steps in the ISR Process (Investor Presentation)

Valuation

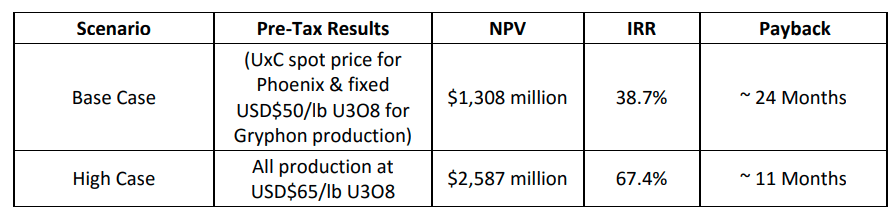

The combined two phases of the project are anticipated to produce 109.4Mlbs of U3O8 over a 14-year mine life, and the 2018 PFS listed the project’s Base Case pre-tax IRR at 38.7% with a CAD$1.3 billion NPV8% (~US$956 million using a 1.36 USDCAD exchange rate). Now granted, that is a fairly modest sum which doesn’t provide much upside when compared to Denison’s current enterprise value of $771 million.

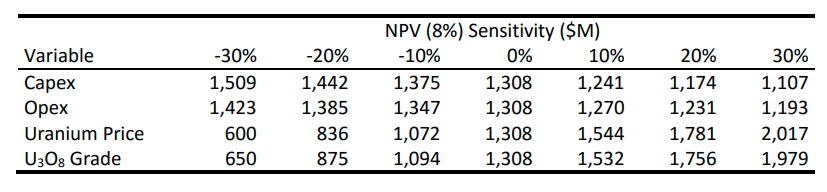

However, it should be noted that the base case uses a $43.92/lb average price for its uranium. And given that U3O8 currently trades in the $50/lb range and yellowcake’s price has not traded below $45/lb for over a year, that price assumption is beginning to look somewhat conservative. The PFS also included the following sensitivity analysis which would lead investors to infer that at current prices Denison’s NPV8% would be just below CAD$1.7 billion, or about US$1.25 billion, improving its valuation to 0.62 NPV.

Prefeasibility Study

But this is where one’s view of current and future uranium prices comes into play. That’s because Denison’s PFS also lists a “High Case” scenario using a $65/lb price in which case the NPV8% comes in at CAD$2.6 billion, or about US$1.9 billion, giving the stock a current valuation of about 0.4 NPV.

Denison Prefeasibility Study

On a relative basis, Denison’s valuation also looks like it may have some upside. Granted, its Enterprise Value per Pound (‘EV/lb’) of $6.15 is priced substantially higher than that of third-tier player Uranium Energy Corp. (UEC), which boasts a very cheap EV/lb of $4.98. Sometimes though, things are cheap for a reason.

But if instead we compare Denison to a top-tier developer such as NexGen Energy Ltd. (NXE), which has an EV/lb of $6.73, then Denison’s stock begins to look like somewhat of a bargain. In order to present a more conservative picture, these numbers use only the Measured and Indicated Resources and, in the case of Denison, use only the Wheeler River numbers, excluding its other small properties.

The difference between the two grows even larger when we consider their Total Acquisition Cost per Pound (‘TAC/lb’). Here, Denison prices substantially lower than NexGen with a TAC/lb of $18.12 relative to NexGen’s much higher $21.89.

But therein lies the risk.

Risk

The Total Acquisition Cost is calculated by adding the Enterprise Value, projected Capex cost, and All-In Sustaining Costs (‘AISC’). That amount is then divided by the Reserve size to get the per pound number. And both Denison’s Capex and AISC numbers are starting to be long in the tooth as those projections were made as part of its 2018 PFS. Needless to say, much has changed in the world during the last 5 years.

It therefore makes sense that the market would be discounting the stock until it gets greater clarity with regards to the project’s costs. Capex and AISC are almost certain to increase when the Feasibility Study is released, but the question is by how much? Given the elevated inflation rates of the last few years, the market may tolerate a 20% or 30% increase in projected costs but may be less forgiving of numbers substantially above that.

However, there is no way of really knowing, and this uncertainty is likely to overhang the stock until the FS is released.

Takeaway

I continue to believe that Denison’s stock has strong potential, but I cut my rating from Strong Buy to Buy as I wait for greater cost and timeline clarity from the Feasibility Study. And while I don’t think it very likely that uranium prices will surge to $100/lb anytime soon, I can definitely see prices rising to the $65/lb range by the middle part of this decade, and for those reasons I continue to hold the stock.

Be the first to comment