Urupong/iStock via Getty Images

For much of this past year, CrowdStrike (NASDAQ:CRWD) escaped the wrath of the tech crash. The leading cybersecurity firm is widely seen as a consolidator in the space as customers seek a one-stop shop for their cybersecurity needs. This is evidenced by the aggressive growth rates that the company has posted year after year. Yet the company is showing signs of impact from the weak macro backdrop, and its rich valuation was hit as a result of that. The company is still generating positive free cash flow and has a strong balance sheet. CRWD is as buyable as ever after the partial valuation reset.

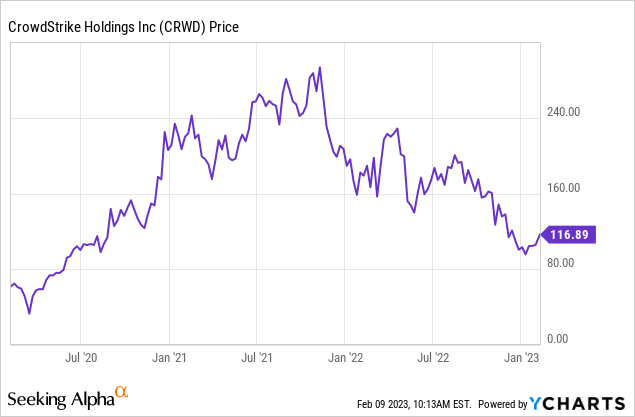

CRWD Stock Price

It was not until the second half of this year that CRWD really began to tumble. The stock saw its most recent plunge come after reporting earnings that were just not quite good enough. With great valuations comes great expectations.

I last covered CRWD in November where I rated it a buy on account of the high quality of management and underlying business. After the valuation reset, the stock has narrowly creeped into my “strong buy” rating range.

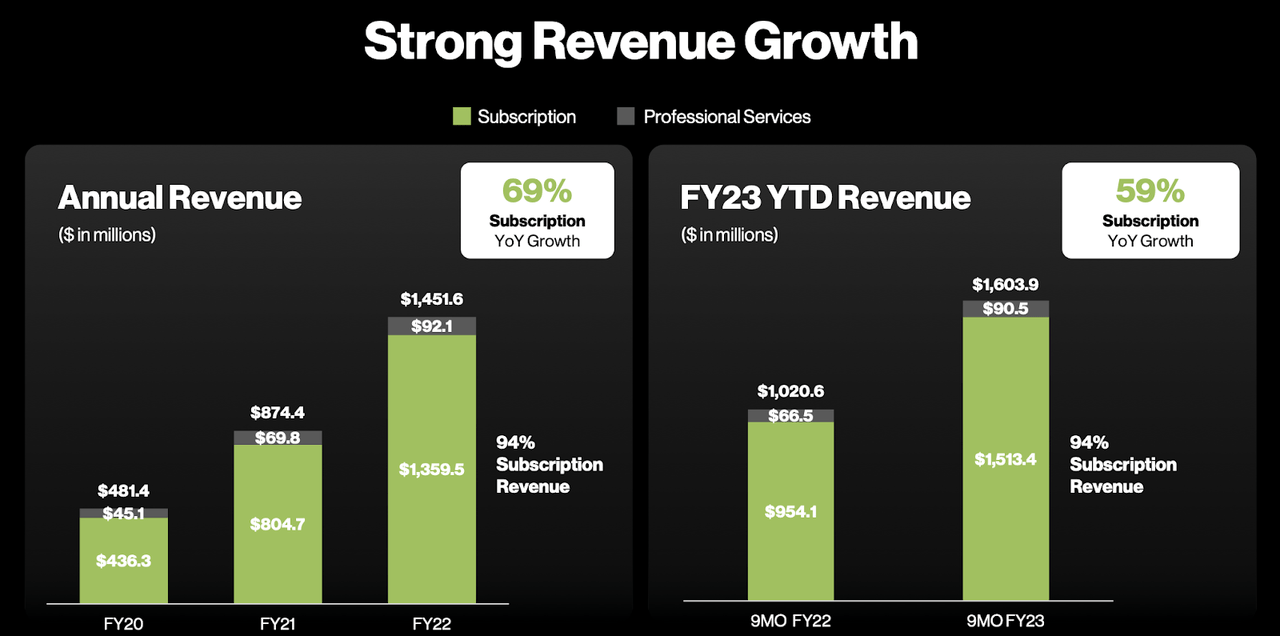

CRWD Stock Key Metrics

In its most recent quarter, CRWD delivered 52.8% YOY revenue growth. That came on top of 66% growth in the last full fiscal year. These strong results show that cybersecurity was not a pandemic fad and remains in high demand even after accelerated transformation that happened during the pandemic.

FY23 Q3 Presentation

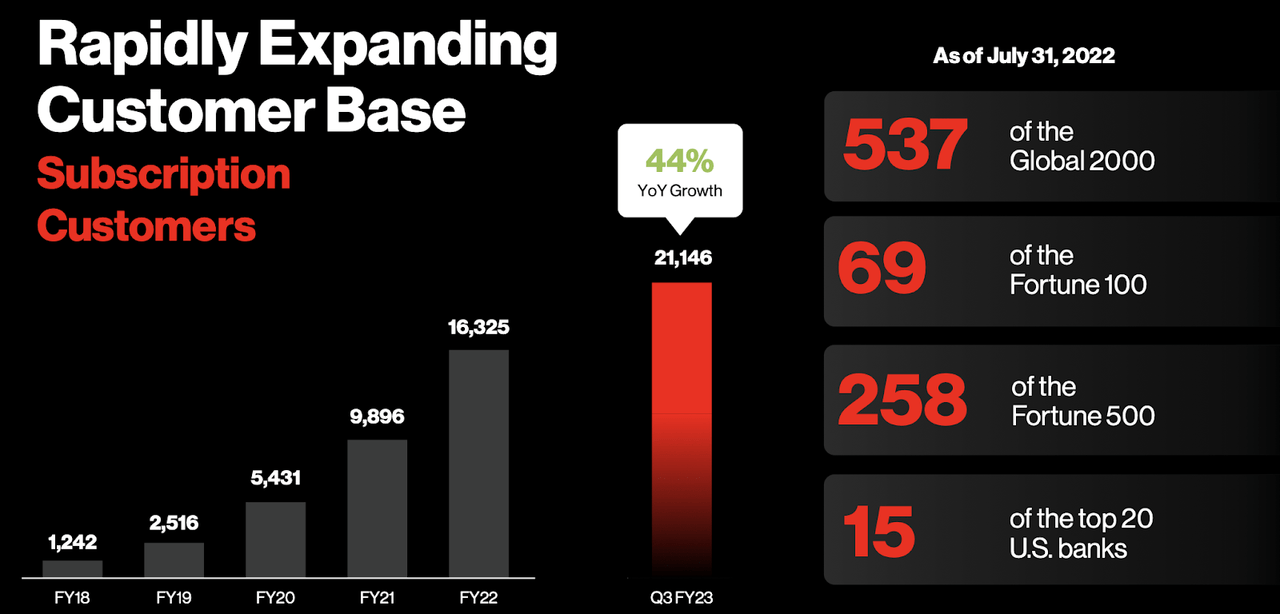

CRWD continued to grow its customer base at a 44% YOY clip. CRWD is considered a clear leader in cybersecurity, led by its endpoint product, as evidenced by its large customer count among the largest global companies.

FY23 Q3 Presentation

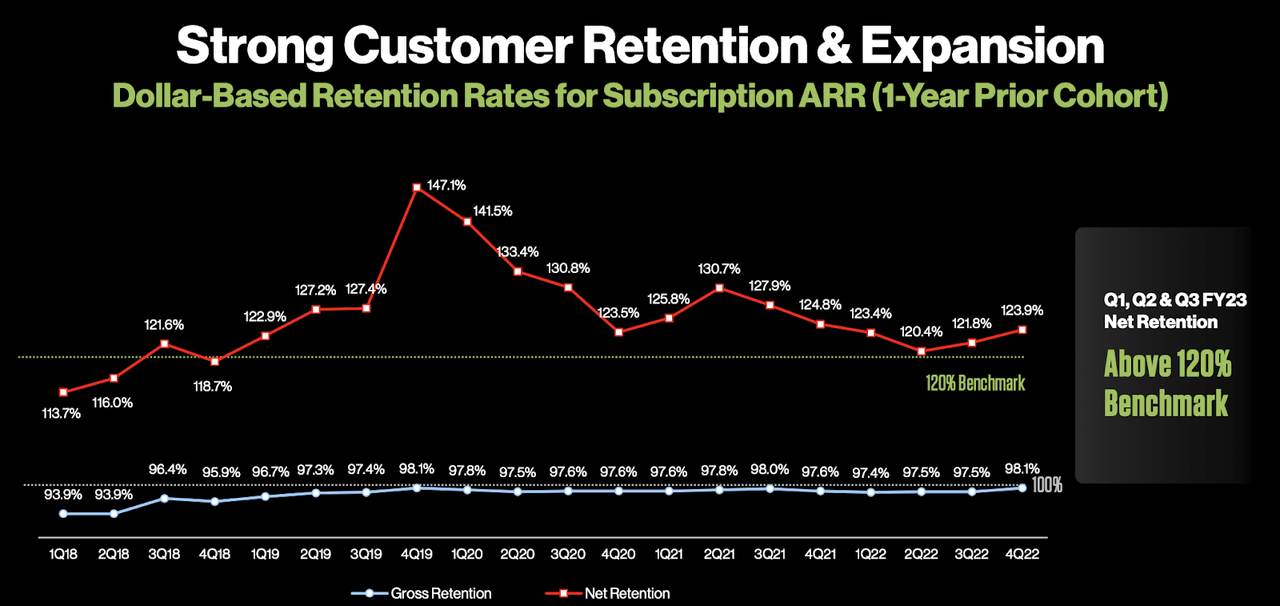

CRWD maintains a high dollar-based retention rate in excess of 120%, courtesy of the company’s large product portfolio. Tech investors may wish to prefer companies like CRWD which have the ability to cross-sell new products to existing customers as that may be a crucial source of growth during economic slowdowns.

FY23 Q3 Presentation

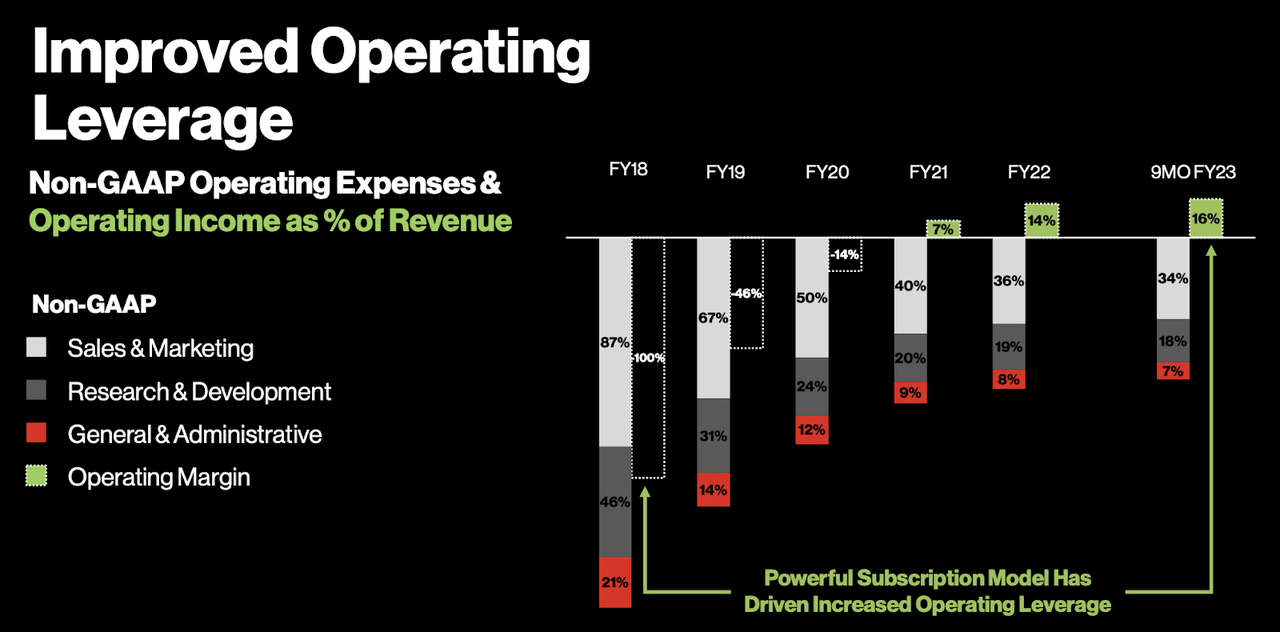

CRWD also delivered some operating leverage, with non-GAAP operating margins creeping up to 16%.

FY23 Q3 Presentation

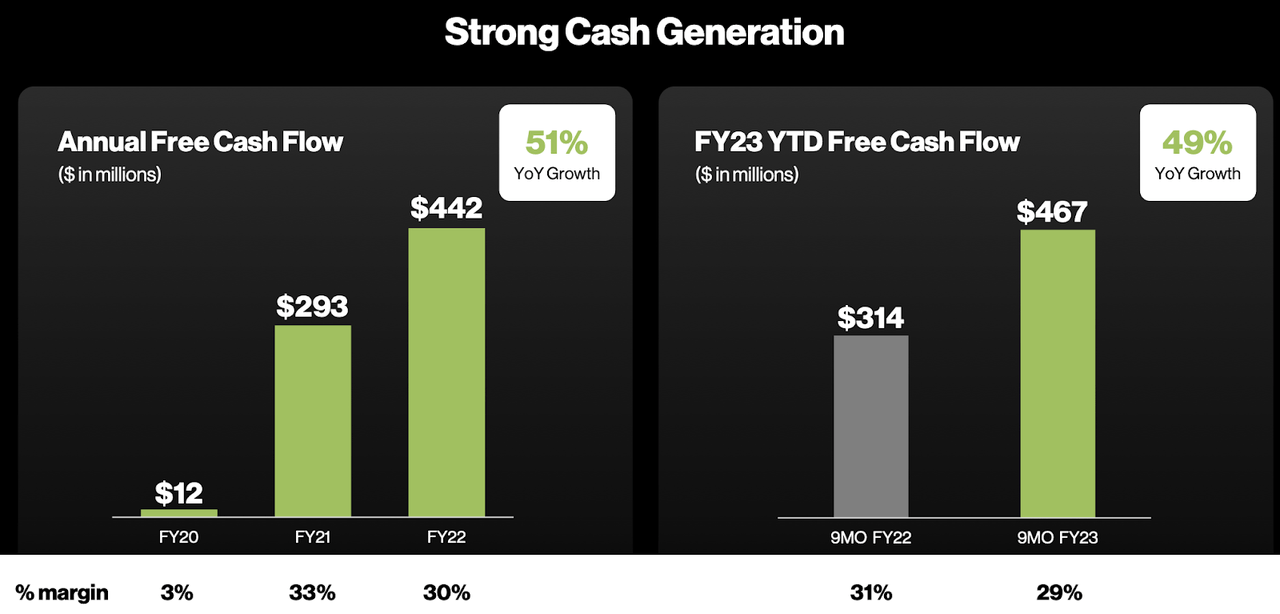

CRWD has historically been highly free cash flow generative as its customers often pre-pay their subscription plans. After generating $442 million in free cash flow in the last fiscal year, CRWD has already generated $467 million in free cash flow year to date.

FY23 Q3 Presentation

These strong results come even as the company faces the same tough macro backdrop that every other company is experiencing. On the conference call, management acknowledged that it was beginning to see some macro impact. Specifically, its smaller non-enterprise accounts saw increased sales cycles as average days to close lengthened by approximately 11%. Management believes that these deals are delayed, not lost. Management has given conservative guidance for the fiscal 2024 year (the latest quarter was FY23 Q3), expecting revenue growth in the “low to mid-30s.” Management also expects 30% free cash flow margins in that fiscal year as well as some operating leverage in non-GAAP operating margins.

With $1.7 billion in net cash, management believes that it may be able to take advantage of the weak operating environment to take market share from financially weaker competitors. Finally, management continues to target $5 billion in annual revenues by the end of fiscal year 2026 and to reach their target operating model by fiscal year 2025.

Is CRWD Stock A Buy, Sell, or Hold?

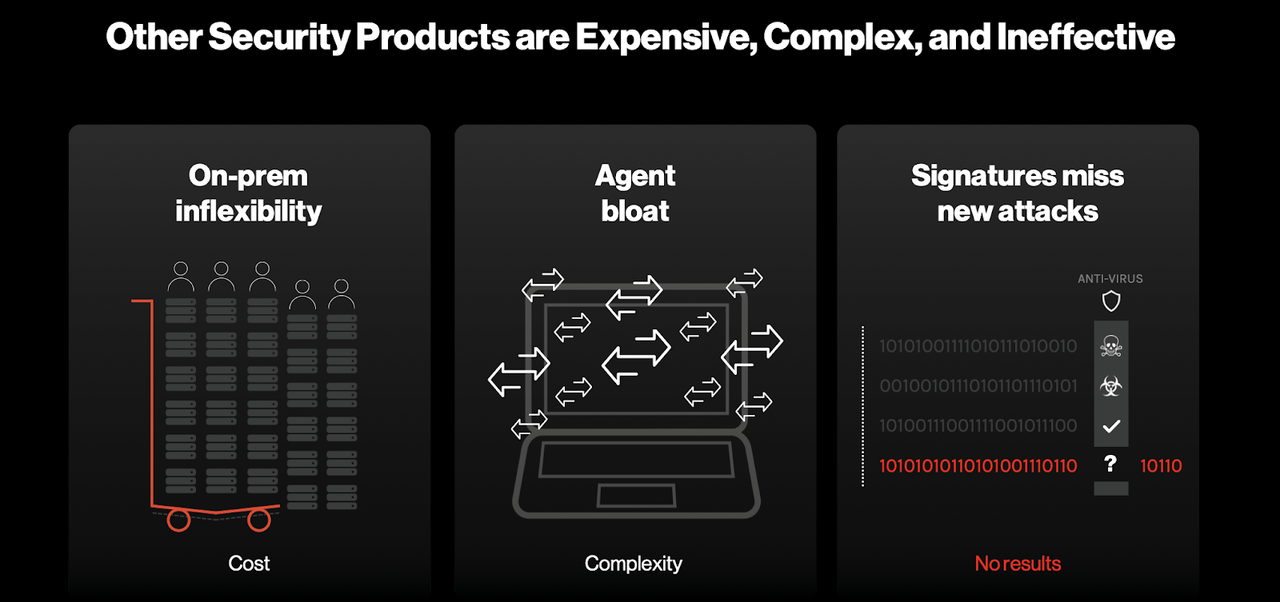

Based on management’s commentary above, it seems that while CRWD is experiencing some macro impact, any impact is near term in nature and do not impact the long-term growth thesis. That does seem to make sense, as CRWD is addressing a large and mission-critical target market. Legacy cybersecurity systems are losing relevance in a rapidly evolving digital world.

FY23 Q3 Presentation

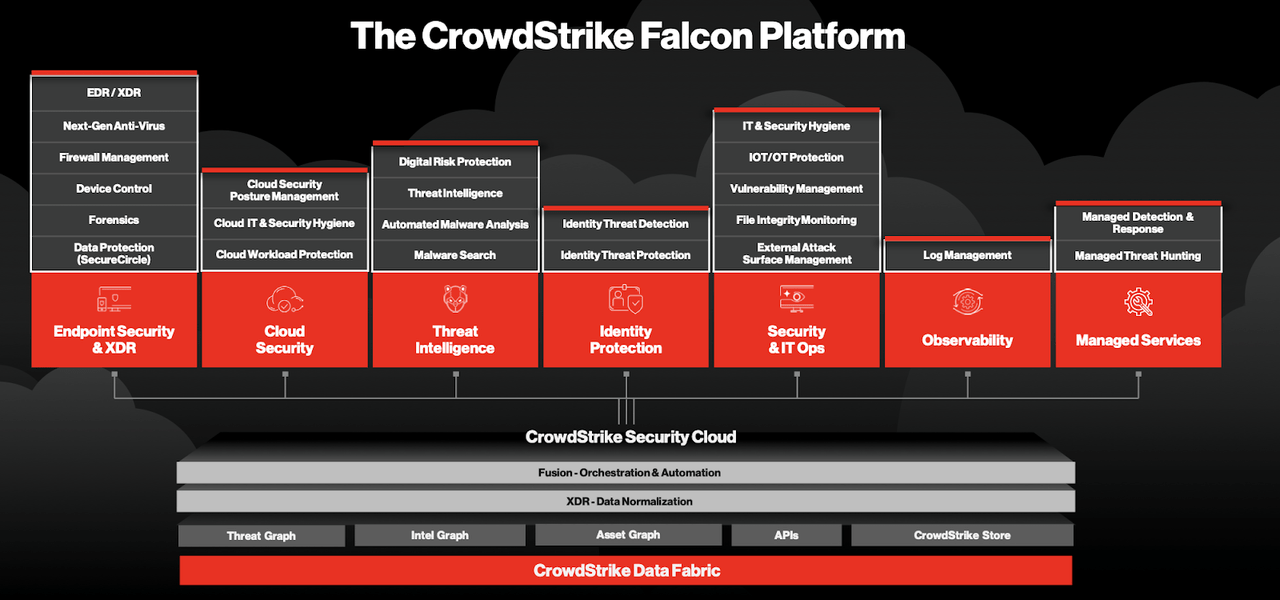

CRWD offers an impressive cybersecurity portfolio which ranks highly in both the breadth and depth of its offering.

FY23 Q3 Presentation

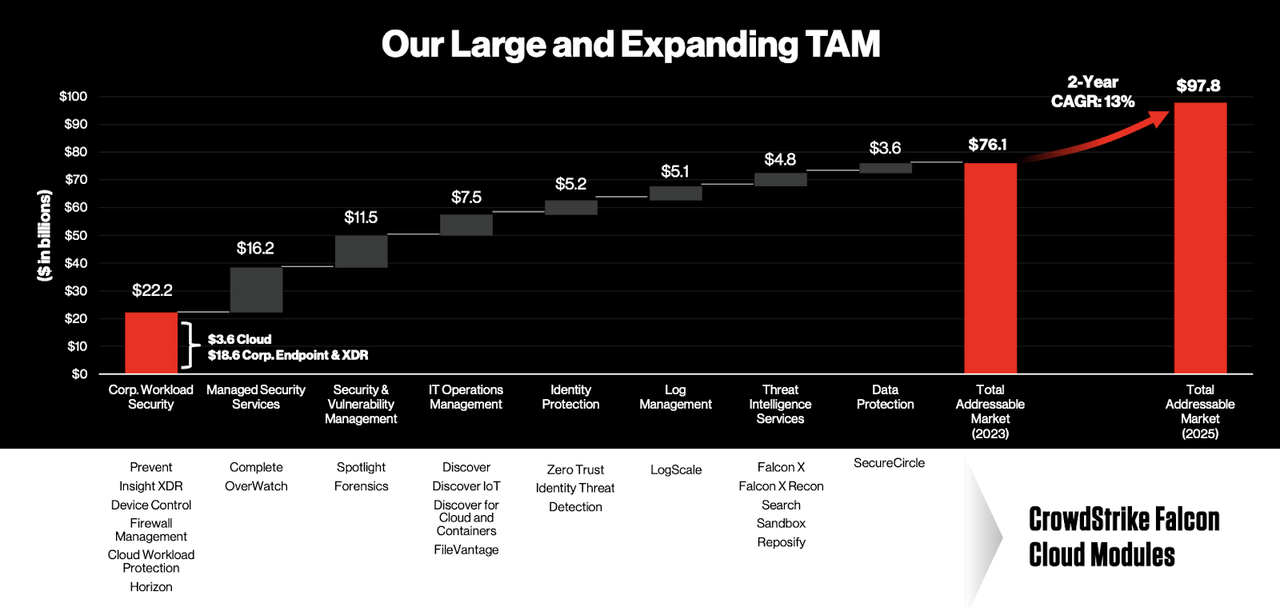

As CRWD adds new products to its product offerings, it believes it can continue to increase its total addressable market, as well as sustain its history of rapid growth rates.

FY23 Q3 Presentation

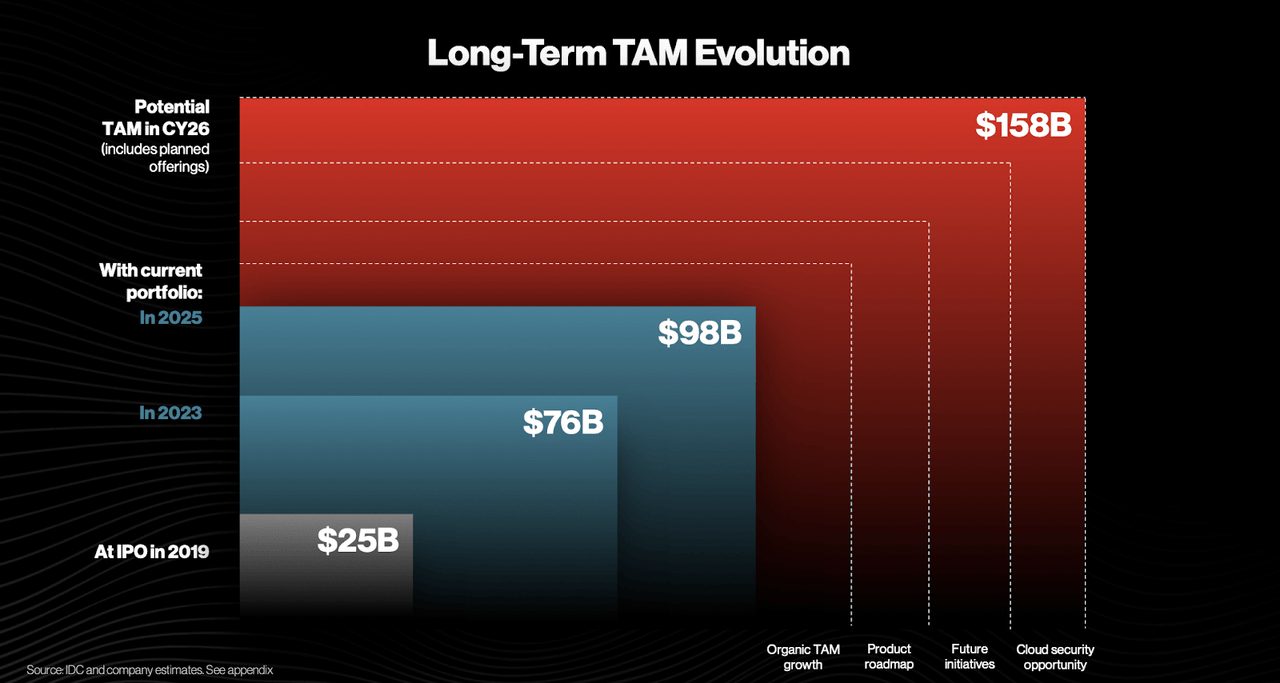

CRWD sees its TAM growing to as much as $158 billion over time as it fully captures the cloud security opportunity.

FY23 Q3 Presentation

As a top operator in the highly attractive cybersecurity sector, CRWD has earned a rich multiple. CRWD stock recently traded at just around 12x sales.

Seeking Alpha

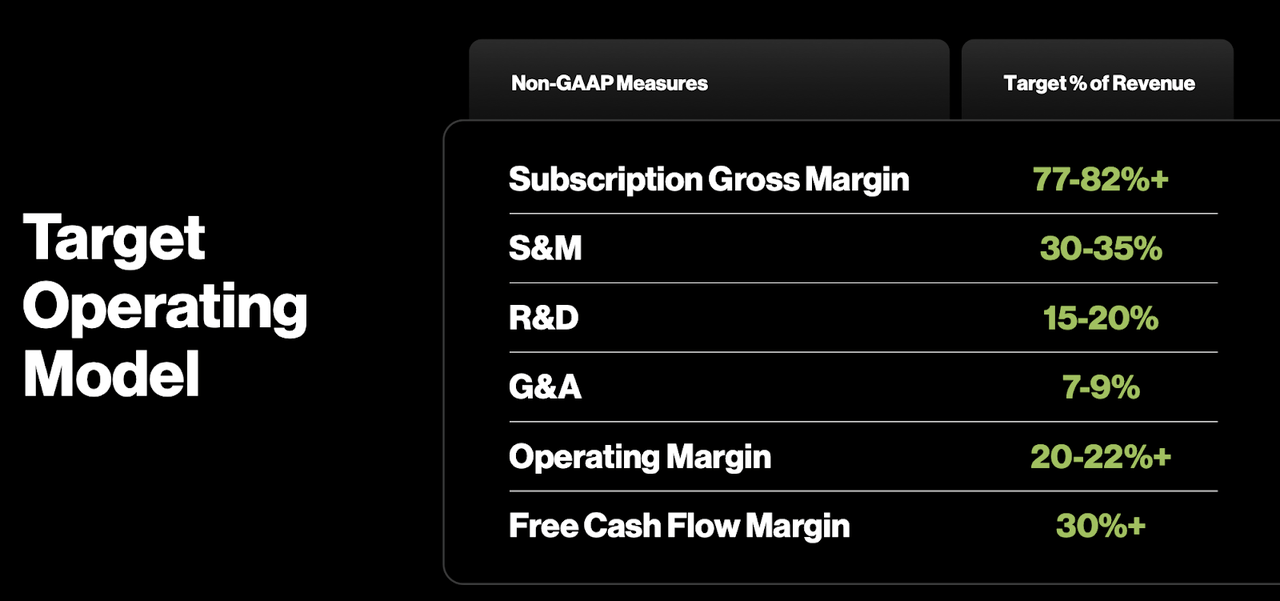

As discussed earlier, CRWD expects to hit its “target operating model” by fiscal year 2025. That target operating model called for 22% non-GAAP operating margins and 30% free cash flow margins.

FY23 Q3 Presentation

Assuming that the company can achieve 25% net margins over the long term and that the stock trades at a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see CRWD trading at 7.5x sales by the end of 2025, implying a stock price of $169 per share. That implies 13% compounded annual returns over the next 3 years which should be enough to beat the broader market. I note that the assumptions may prove too conservative as I assumed only 20% growth exiting 2025 and CRWD may command a PEG ratio in excess of 1.5x due to the attractive growth story and strong operating position. Assuming 25% growth and a 2x PEG ratio, CRWD might trade at 12.5x sales, implying a stock price of $282 per share or 34% compounded annual returns over the next 3 years.

What are the key risks? CRWD trades as one of the more richly valued stocks in my tech coverage universe, even on a growth-adjusted basis. If investor sentiment sours on the name, I could see the stock dropping as much as 40% to trade in line with cheaper peers. I wouldn’t be surprised if the stock encountered great volatility. It is possible that macro has a greater impact on sales cycles in the near term and that the market fails to take a long-term view on the stock – that may lead to substantial multiple compression. Another risk is that of competition – Microsoft (MSFT) remains a formidable competitor in the endpoint security space though for now, CRWD appears to have a stronger product offering. I am of the view that cybersecurity is a product in which companies will be willing to pay more for the best product instead of accepting MSFT’s discounted cybersecurity offering as part of a bigger bundle, but perhaps in tough economic conditions that view may be proven wrong. As discussed with subscribers to Best of Breed Growth Stocks, a diversified portfolio of undervalued tech stocks may be the best way to take advantage of the tech stock crash. CRWD fits in such a portfolio as a higher quality allocation, though my preference remains with cheaper peers. In particular, SentinelOne (S) looks more attractive here and is a top position in our portfolio. Nonetheless, CRWD remains highly buyable here and I own a small position.

Be the first to comment