Last week, I started to “update” my analysis of companies, which I already covered in the past, but with a special focus on the business model with regard to COVID-19 and the upcoming recession. One of the companies covered so far, is the fast-food chain McDonald’s (MCD), which will be affected in a negative way by COVID-19 as well as the upcoming recession.

Starbucks’ (SBUX) business model is in some ways similar to McDonald’s business model and the company will also be affected by store closures and social distancing, but Starbucks has also a well-established take away business, which will soften the negative impact. And compared to McDonald’s we have one big advantage: our analysis can in parts rest upon the already released preliminary numbers for the last quarter.

(Source: Pixabay)

All these articles will follow the same structure and focus on four different aspects that seem to be very important right now:

- Impacts from COVID-19: I am trying to analyze how COVID-19 as well as the measure and political decisions (lockdowns, social distancing, closures, etc.) will affect the business model.

- Impacts from a potential recession: As a global recession seems to be inevitable, I will also analyze how a recession will impact the business model.

- Solvency and Liquidity: In turbulent times, debt levels, solvency and liquidity are especially important and we are therefore taking a closer look at the balance sheet.

- Intrinsic Value Calculation: Although I included a potential recession in the near future in almost all calculations and considered a declining free cash flow, COVID-19 might call for an update of the intrinsic value.

(Source: Author’s own work)

And similar to several other companies covered so far in this series, we also take a peek at the company’s dividend.

Impact from COVID-19

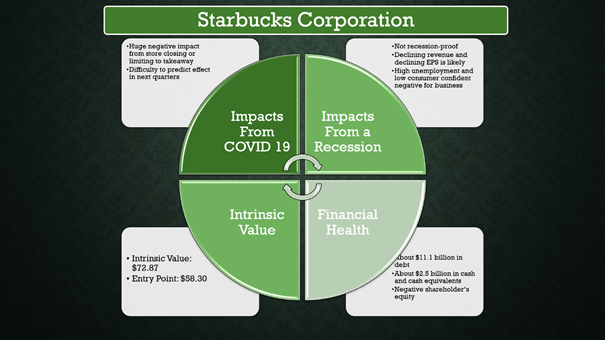

By the nature of its business model, Starbucks is affected quite heavily by COVID-19 and the resulting consequences of the lockdown in China, stores closures and social distancing. Already in January 2020, Starbucks had to close stores in China, in February 2020, the comparable store sales in China were off 78% YoY and in March 2020, Europe and the United States were also hit by social distancing, stores closing or limiting to takeaway while China was already recovering.

For most other companies we have to rely on estimates and make several assumptions about the business, revenue and earnings per share. In case of Starbucks and due to the 8-K released on April 8, 2020, there are numbers we can already rely on. For China, Starbucks confirmed that the business is on its way to improvement:

Our March 5 letter shared evidence of the China recovery that began in late February. That recovery continued at a slightly faster pace through the month of March, where comparable store sales declined by 64% compared to a 78% decline for the month of February. Each week, we see more evidence reinforcing our belief that the business will fully recover over the next two quarters. For example, in the last week of March, comparable store sales declined by 42%, representing not only the seventh consecutive week of sequential improvement but also the approximate midpoint of recovery from a weekly low of -90% in mid-February.

In the last quarter, the business disruption related to COVID-19 in China had an adverse impact to Starbucks’ GAAP as well as non-GAAP EPS in the range of $0.15 to $0.18. And while many investors hoped for several months, that the problem was isolated only on China, we now know this is not true. Although most European countries are also affected, we will especially focus on the United States, as it is the most important market for Starbucks. In the 8-K management wrote:

Comparable same store sales in the U.S. began to decline on March 12 and steadily worsened as we temporarily closed more stores and traffic slowed in response to the rise in “shelter-in-place” mandates and “social distancing” requirements across the country. During the last week of the month, comparable store sales declines stabilized in the range of -60% to -70%, with 44% of U.S. company-operated locations operating, most under modified store hours, primarily through the drive-thru channel.

As a result, Starbucks not only withdrew its guidance for the full-year, but also reported horrible preliminary second quarter results, which were not only negatively affected by the Chinese business (as many hoped for a long time), but also by the business in the United States. In the 8-K management is stating:

As a result, Starbucks preliminary estimates for Q2 FY20 GAAP and non-GAAP EPS are approximately $0.28 and $0.32, respectively. These estimates reflect the impact of lost sales for the period as well as incremental expenses for partner wages and benefits, store operations and other activities related to the COVID-19 outbreak. This includes inventory write-offs, honoring supplier obligations, store safety-related items, asset impairments and preliminary estimates of certain government stimulus program benefits.

Compared to the same quarter last year, the preliminary estimates reflect a decline of about 47% for GAAP EPS as well as non-GAAP EPS. Management is also expecting the negative financial impact in the third quarter being significantly greater than it was in the second quarter. The negative effects will also extend into Q4. According to Seeking Alpha Earnings Revisions, analysts downgraded expectations for the following quarters, but the numbers are still way too optimistic. For the third quarter, expectations for earnings per share are still $0.46 while Starbucks’ statement is rather indicating that earnings per share will be $0.30 or lower. As I have mentioned already in case of McDonald’s, I think analysts are still too bullish. Other estimates are already lower – according to Nasdaq – but even these estimates are expecting earnings per share for the quarter from October and December to be similar as in the year before.

If we assume that most countries around the world – including China and the United States – can go back to “normal” in the next few weeks, these estimates might be realistic. But considering that we won’t have a vaccine for COVID-19 and many virologists assume confirmed cases to start rising rapidly again if the current measures are loosened, such a scenario seems to be rather unrealistic. Additionally, we have to take into account that the US economy – as well as many other countries around the world – will enter a recession (or rather: is already in a recession) and hence, we also have to take into account the negative aspects from a recession on Starbucks’ business.

Impact from Recession

Aside from the impacts due to COVID-19 on the business model, an upcoming recession will also have a negative impact on Starbucks’ business model. And while a recession has several negative consequences for different sectors, in case of Starbucks, we have to focus on the individual consumer and his spending.

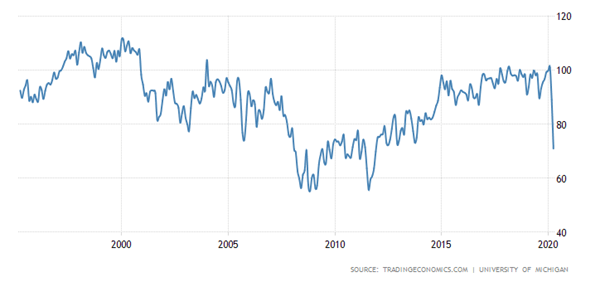

And although Starbucks is selling food and beverages, which have to be consumed all the time, Starbucks is selling very expensive food and expensive beverages. And it could very well happen, that customers will drink less coffee, buy their cup of coffee at some place else (where it is cheaper) or drink coffee at home. If people are pessimistic about their economic future, they will cut spending and the consumer confidence might therefore be an important number to look at.

Usually I don’t pay much attention to consumer confidence when talking about the economy as it is usually a lagging indicator. But in case of Starbucks, consumer confidence can be important as people will buy more if they are confident about the future and cut back if confidence is dwindling away. And the chart below shows, how sudden consumer confidence dropped to low levels we haven’t seen for several years.

(Source: Trading Economics)

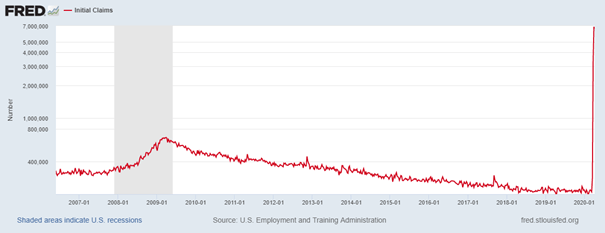

While consumer confidence is rather a “soft” number, which has to do with feelings and sentiment (which can change very quickly as we have seen in the past few weeks), there are also “harder” numbers which can’t be changed so easily and quickly. One of the important aspects for “ordinary” people, that will have a huge effect on the spending is the question whether they have a job or not.

During the last three weeks 16,780,000 people have claimed unemployment insurance, which is more than 10% of the US labor force (in March 2020, the number of all nonfarm employees was 151.8 million people). The unemployment rate increased from 3.5% to 4.4% in March 2020 (but the number doesn’t include the millions of initial claims of the last weeks). And even if a huge part is only furloughed, it seems a little moronic to assume the US economy won’t suffer in the months ahead. And we can assume, that the upcoming recession will also have a negative influence on Starbucks’ business.

(Source: FRED)

And when looking at the past recession, the reported numbers of Starbucks are also confirming this – but only when looking at the last recession (Financial Crisis). The recession during the Dotcom bubble paints a different picture.

In the years 2000 till 2004, Starbucks could not only increase its revenue every single year, but could almost double its revenue from $2,177 million in 2000 to $4,075 million in 2003. Earnings per share also increased every single year and between 2000 and 2004, earnings per share almost quadrupled from $0.24 in 2000 to $0.95 in 2004. But these numbers were during a stage, where Starbucks was growing with a really high pace and might therefore not be representative for the performance during future recessions. Between 2000 and 2004, Starbucks increased the number of total stores from 3,501 at the end of fiscal 2000 to 8,569 at the end of fiscal 2004.

When looking at the performance during the financial crisis, the picture is not looking as bright. In 2009, total net revenue declined about 6% compared to the previous year. The following year, revenue could already increase 10.5% again. Earnings per share declined in 2008 (about 50% compared to 2007), but could increase again in 2009 (more than 20% higher than in 2008).

In 2020, Starbucks’ business will probably be hit twice: on the one side by the global measures due to COVID-19 as well as the negative effects from a global recession (high unemployment and decreased spending).

Balance Sheet

During such times with high uncertainty and probably declining revenue and declining profitability, the financial health of a company (liquidity and solvency) becomes extremely important. We are therefore looking at the company’s balance sheet and especially the debt levels.

In December 29, 2019, Starbucks had $3,040 million in cash and cash equivalents on its balance sheet and in the recent 8-K, management informed us that cash and cash equivalents had decreased to $2.5 billion right now. Similar to many other companies, Starbucks has executed a $1.75 billion bond issuance on March 10, 2020, to free up additional liquidity. And to further enhance the financial flexibility, Starbucks also has temporarily suspended the share repurchase program (like many other companies) and is trying to reduce discretionary spending.

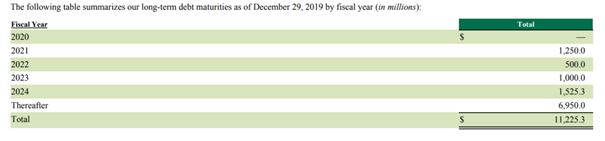

Liquidity doesn’t seem to be the problem for Starbucks as the available cash seems to be enough, but solvency is also important. In December 20, 2019, Starbucks had $10,653 million in long-term debt and $498 million in short-term debt. Due to its negative shareholders’ equity (which is not good), we can’t calculate a D/E ratio (at least not one that makes sense). But when comparing the outstanding debt to the operating income (which was $3,915 million in 2019), it would take Starbucks less than three years to repay the outstanding debt, which is acceptable.

And I am very well aware of the fact that operating income will be lower in 2020, but Starbucks doesn’t have to repay all the debt in the next few years. In fact, according to the last 10-Q, Starbucks has to repay no debt in 2020, $1.25 billion in 2021 and $500 million in 2022.

(Source: Starbucks 10-Q)

Moody’s Corporation is rating Starbucks with Baa1, which is still investment grade, but on the lower end of the investment grade range and for Starbucks it means, that investors shouldn’t be concerned about the financial health, but the company has to be cautious in the next few quarters and not spend too much money on share buybacks or the dividend, which is also an important aspect for many investors.

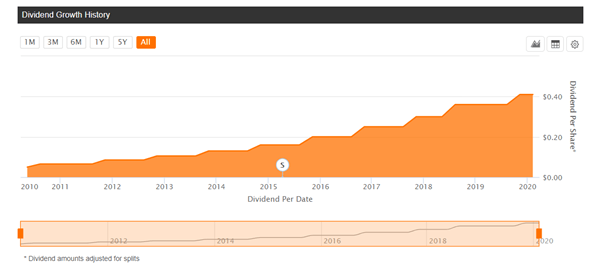

Dividend

Starbucks has neither joined the ranks of dividend aristocrats nor does Starbucks have an extremely high dividend yield. Right now, the annual dividend is $1.64, which is resulting in a dividend yield of 2.22%. Starbucks is paying a dividend since 2010 and has increased its dividend for 10 consecutive years. The reason why Starbucks could be interesting for dividend investors is not the long timeframe for which it increased its dividend, but rather the high growth rate. During the last 5 years, Starbucks increased its dividend with a CAGR of 22% and although we can assume dividend growth to slow down, it could still be a good investment for dividend growth investors.

(Source: Seeking Alpha Dividend History)

The current payout ratio of 56% seems rather high, but we shouldn’t be concerned and consider the dividend as safe. In the above-mentioned 8-K, management wrote, that is does not plan to reduce the quarterly dividend and many other restaurant stocks have rather high payout ratios as well.

Intrinsic Value Calculation

In a final step, we are trying to calculate an intrinsic value for Starbucks and therefore have to estimate what the free cash flow in the years to come will be. In the last recession, earnings per share declined about 50% and for 2020, a decline of 50% also seems likely. In the second quarter, earnings declined about 50%, the third quarter will be worse and for the rest of the year, it is difficult to make predictions. This time, I assume the impact will be worse and therefore I will calculate with a similar low free cash flow as in 2020 for the following year.

For 2022, let’s assume free cash flow will be similar as in 2019 again and Starbucks recovered from the crisis. Going forward, I assume 10% growth till the end of the first decade and then 6% growth till perpetuity. Only a few months ago, management was still holding on to its long-term growth target of at least 10% earnings per share growth annually for the foreseeable future. It is expecting revenue to grow between 7% and 9% annually and operating income growing between 8% and 10%. When looking at the performance during the last decade, management’s goal seems to be realistic as Starbucks could increase its revenue 10.6% annually during the last decade and earnings per share could grow even 18.8% annually on average.

(Source: Starbucks Annual Investor Meeting 2019)

Starbucks will achieve these long-term growth targets due to a combination of higher traffic, higher prices, higher revenue per customer as well as new additional stores. And we can be pretty confident that Starbucks will return to its former growth path (from 2022 going forward).

When using the numbers from above, we get an intrinsic value of $72.87 for Starbucks. And like with all other companies, I will take a margin of safety of 20% although Starbucks seems like a pretty stable business. But we don’t know what will happen and the margin of safety is supposed to reflect mistakes and false assumptions (and due to extreme high level of uncertainty, false assumptions seem to be likely). This leads to an entry point of $58.30 for Starbucks.

Conclusion

Starbucks will be affected by COVID-19 as well as the upcoming recession and we will see declining revenue and steep declines for earnings per share in 2020 and probably also in 2021. The higher debt levels of Starbucks are also not ideal, but we shouldn’t worry about the financial health of Starbucks. But I am confident about the long-term potential of Starbucks and not later than 2022, Starbucks should be able to return on its former growth path again.

(Source: Author’s own work)

Stay safe, stay healthy, don’t panic!

If you enjoyed the article and like to learn more about wide moats, please check out my marketplace service: Moats & Long-Term Investing.

Subscribers get access to extensive background information on wide-moats, at least weekly exclusive research, a watchlist of wide moat companies and a chatroom where members can ask questions and exchange opinions about long-term investing and companies with a competitive advantage.

For investing in companies that can beat the market over the long term and create a portfolio with companies you can (almost) hold forever, please check out my marketplace service. You can also take advantage of a free trial offer.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment