naphtalina/iStock via Getty Images

Introduction

CoreCivic, Inc. (NYSE:CXW) came to mind after Michael Burry announced he was buying shares in The GEO Group, Inc. (GEO). Like GEO, CoreCivic also operates private prisons and detention centers.

CoreCivic existed as a real estate investment trust (“REIT”) from 2013 to 2020 and has been transformed into a C-Corp company to reduce their high debt burden. That has worked well. The company is now in a strong financial position and has launched a generous share buyback program to reward shareholders.

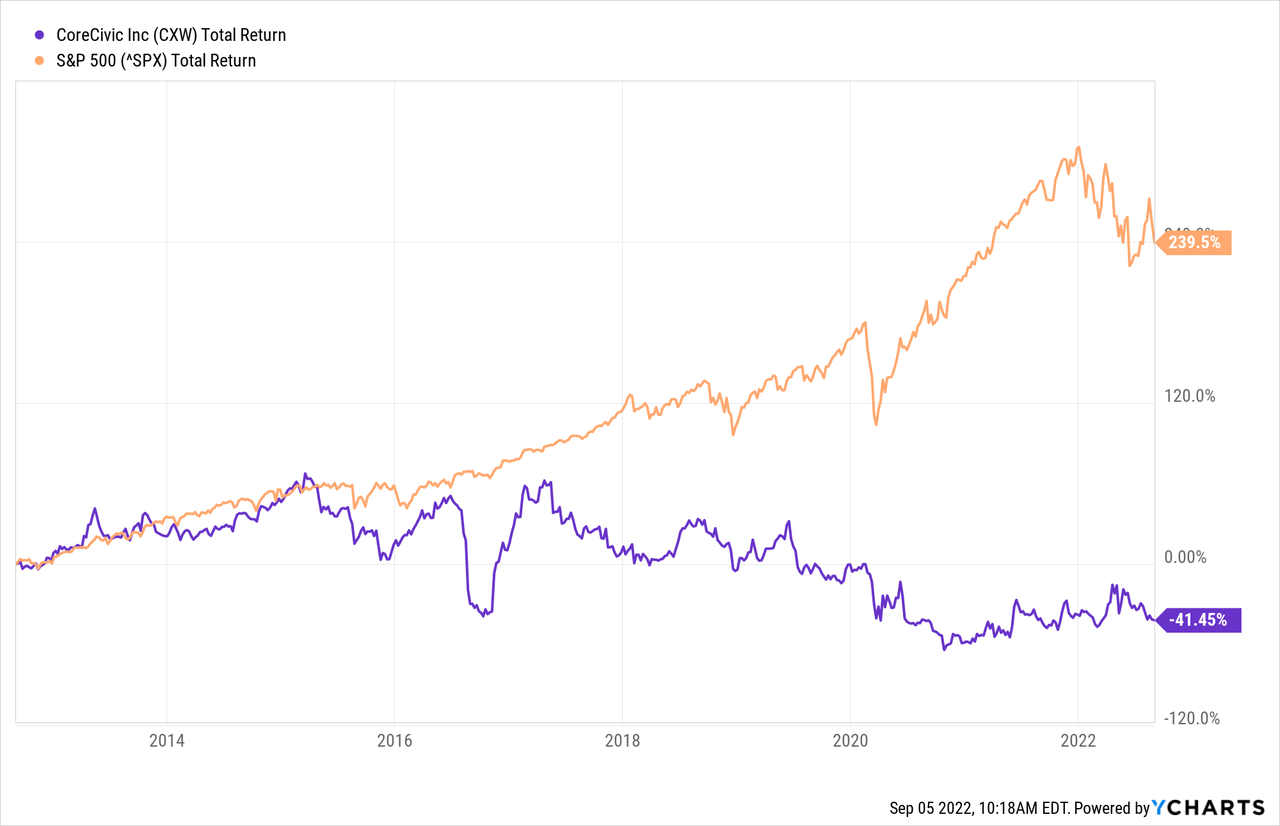

Don’t let their negative historical stock return mislead you. It is true that investors who bought CoreCivic stock 10 years ago have seen a negative return of 42% versus a positive return of 240% for the S&P500. The decline was due to the company’s skyrocketing debt that it struggled to pay off as a REIT, and ESG-conscious investors shunning stocks in prisons. This is a trend that I expect to continue.

However, CoreCivic’s debts have been significantly reduced and the maturities of the debts are well into the future. Liquidity is strong for the coming years. Management now rewards shareholders with a massive share repurchase program, which will drive the share price up. The stock now is a “buy.”

CoreCivic Is In A Strong Financial Position

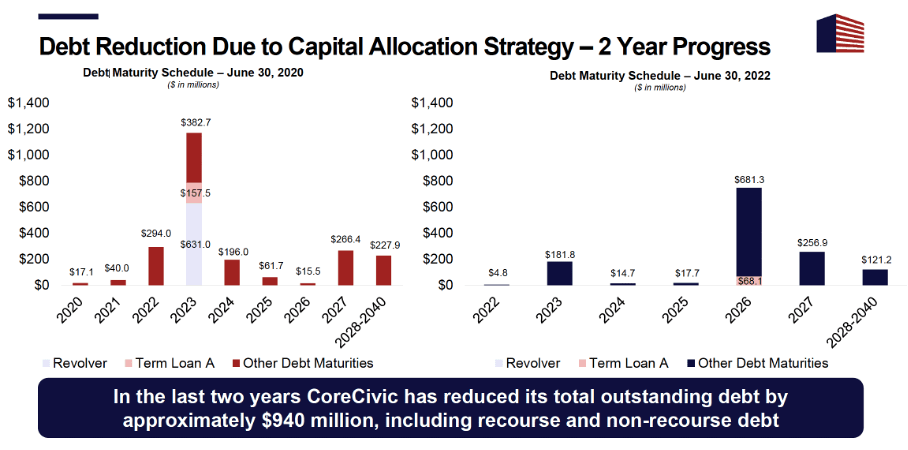

CoreCivic has significantly reduced their debt over the past 2 years. The high debts for 2023 have been refinanced, so there are no major debt repayments in the short term. A major repayment will be made in 2026, which will also have to be refinanced in the coming years.

Debt Reduction Due to Capital Allocation Strategy (CoreCivic 2Q22 Investor Presentation)

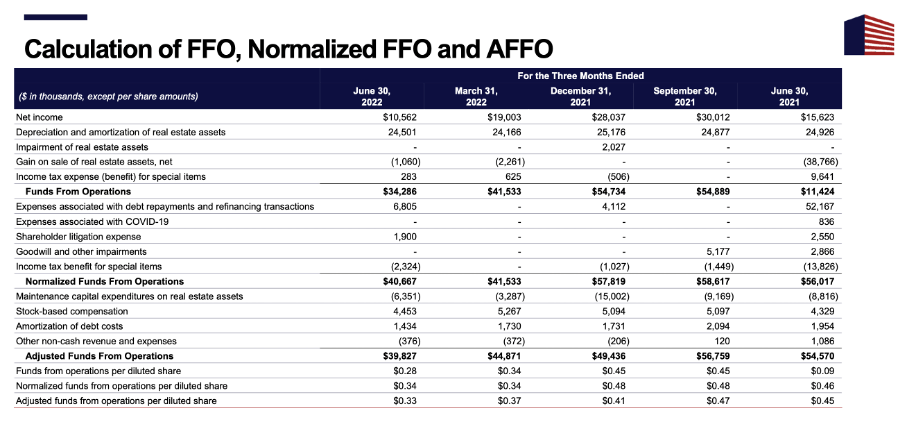

CoreCivic is experiencing labor shortages and wage pressures across the country, and they have increased wages to stay competitive. Financial results were also impacted by the transition at the La Palma Correctional Center in Arizona (CoreCivic’s second largest facility), from ICE population to Arizona population as a result of a new contract award. The ramp-up of the new contract, the largest to be awarded to the private sector by a state in more than a decade, began in April 2022 and is expected to be completed in the first quarter of 2023.

Adjusted FFO (2Q22 investor presentation)

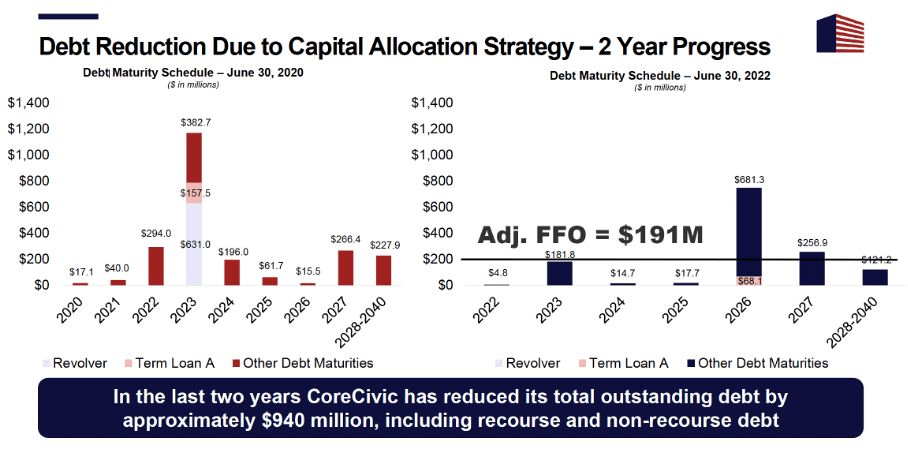

Recent quarterly figures come in on YTD-adjusted funds from operations of $191 million. I compared the adjusted funds from operations (“FFO”) in the image below to their upcoming debt maturities. This shows that CoreCivic has ample room to meet its obligations until 2026.

Debt Burden Compared to Adjusted FFO (2Q22 Investor Presentation and Authors Own Modification)

CoreCivic has greatly improved their financial position in recent years. Previously, CoreCivic rewarded shareholders by paying a large dividend. In 2021, the payment of the dividend has been stopped to reduce their debt burden. But now that CoreCivic’s financial position has greatly improved, it has the opportunity to reward investors again. Instead of paying a dividend, it has decided to launch a generous share buyback program.

Share Repurchases and Valuation

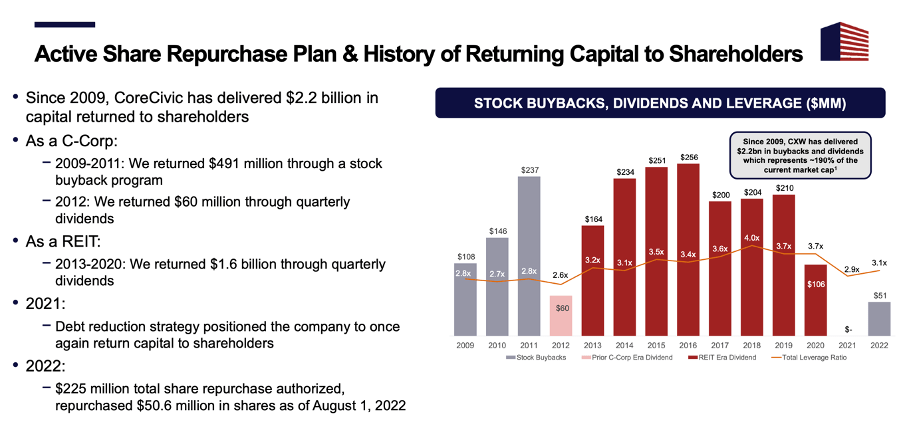

Since 2009, CoreCivic has paid out $2.2 billion (190% of current market cap) to shareholders in the form of a dividend or share repurchase program.

Active Share Repurchase Plan (2Q22 Investor Presentation)

This year, CoreCivic announced to buy up $225 million worth of shares, of which $174 million is still available as of August 1, 2022. CoreCivic’s market cap is $1.12 billion, bringing its buyback yield to a solid 16%. The share repurchase program reduces share supply and increases demand, causing the share price to rise. A buyback yield of 16% is huge, the share price is expected to take off strongly.

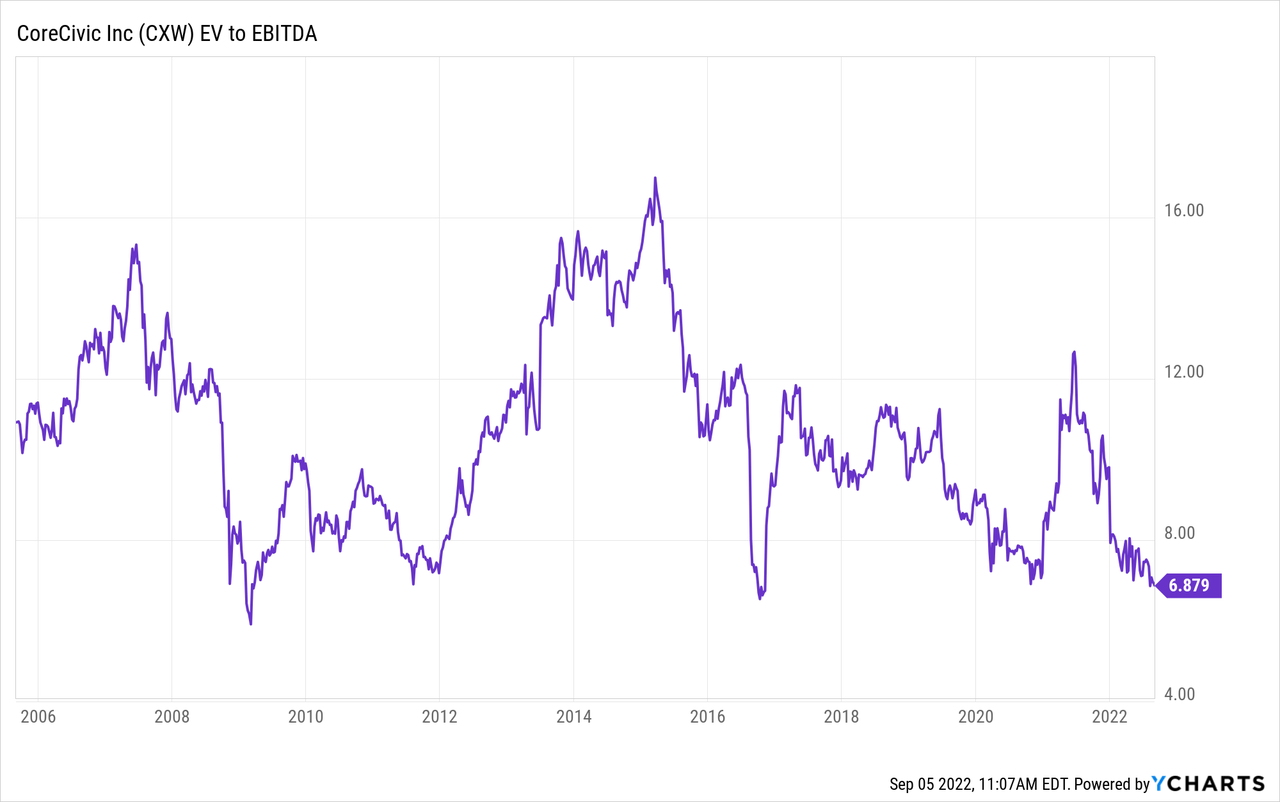

What about the valuation? To map the valuation, I take the EV/EBITDA ratio. This ratio takes into account not only the market capitalization, but also the amount of cash and debt on its balance sheet, this is compared with their EBITDA.

The EV/EBITDA data shows that CoreCivic is trading in the lower range of the historical EV/EBITDA ratio. The stock price is therefore positioned very cheaply in the market. The improvement in the financial position, the generous share repurchase program and the low valuation make the stock a “buy.”

Conclusion

CoreCivic existed as a REIT from 2013 to 2020, but had to undesirably transform into a C-Corp company in order to meet their high debt obligations. This was successful, the company is now in a strong financial position and their debts have been refinanced to a later period. This ensures that CoreCivic has sufficient liquidity.

Management has announced that they will be rewarding their investors with a generous share repurchase program. The buyback yield is calculated around 16%. This generous buyback program will drive the share price sharply. However, there is also a downside to CoreCivic stock. ESG-conscious investors avoid stocks in companies that operate private prisons and detention centers. More and more (large) investors are opting for these principles, which reduces the potential to increase the share price.

Be the first to comment