BeeBright

Cognyte Software Ltd. (NASDAQ:CGNT) is a small-cap tech and analytics company. It provides primarily software-based services to help substantially government and financial services companies to track and predict activity of potential cyber threats and crimes that can be detected on networks. While a cool idea, involving some buzzword concepts like AI and “cybersec,” Cognyte Software Ltd. has been performing poorly as customers delay massively the deployment of Cognyte’s systems. Moreover, the profile of customer creates really long receivable days.

With recent net losses and high working capital intensity, the cash flows are bad and debt will be needed at the current high rates, even after a divestiture of a business responsible for 10% of the company’s previous run-rate revenue. Overall, Cognyte Software Ltd. is unpredictable and needs to mature for it to suit our risk appetite.

Q3 Notes

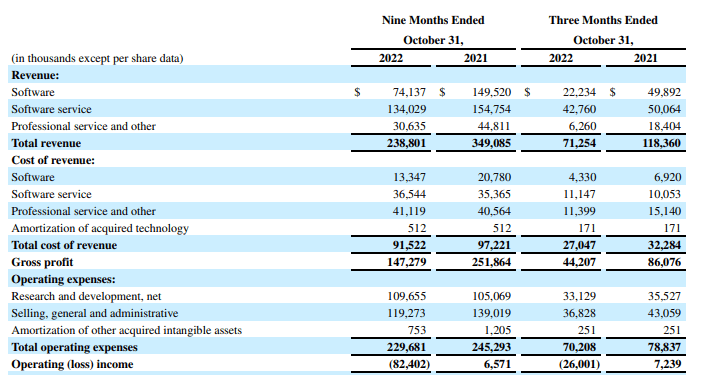

The situation with CGNT has been that due to the macroeconomic conditions, budgeting by customers has put CGNT and deployments of their software in the backburner. This is the crux of CGNT’s current problems, which shows substantial declines in revenues and concurrent stability in OPEX leading to losses.

IS (Q3 2022 PR)

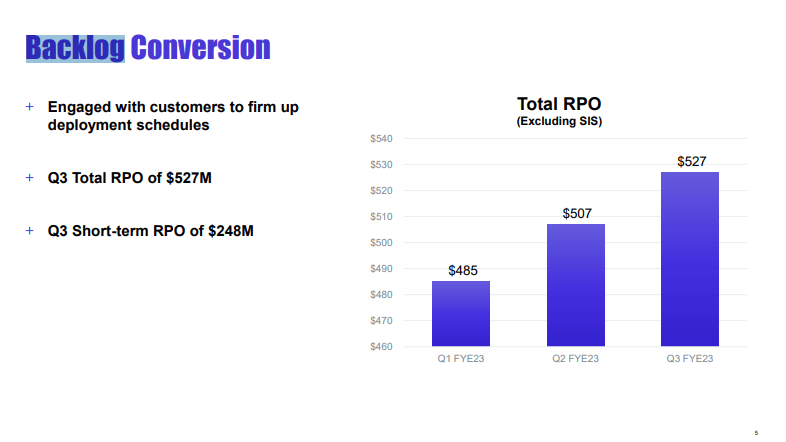

Sequentially the company is now guiding for growth in revenues, as backlog converts into sales, and the company has been able to grow backlog substantially despite delays by current customers. 5% growth is expected hereafter into fiscal 2024.

Backlog (Q3 2022 Pres)

An issue has been the operating leverage. OPEX had barely declined, including cost of revenue, despite the serious declines in revenues of more than 30%. The declines in OPEX, limited as they are, were the consequence of the current salvo of cost-control measures. It is concerning that not more could be done to reduce OPEX burden, but that’s part of the issue with a slowdown in backlog conversion. The engagements still exist, it’s just the compensation isn’t coming in.

Bottom Line

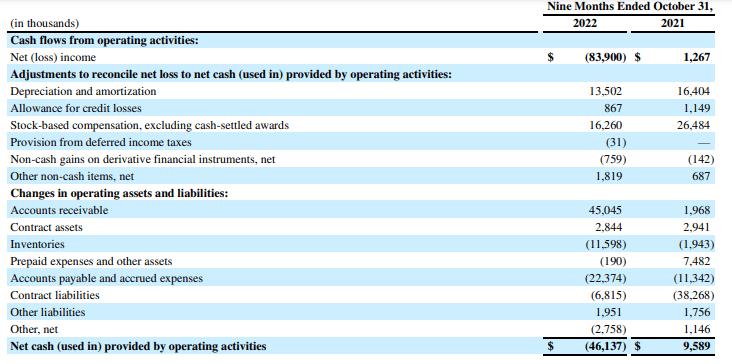

There’s more to comment on regarding Cognyte Software Ltd. financial status. Firstly, the receivables days are massive, with receivables remaining bloated despite the fact that their sales have slowed down. We’ve noticed similar receivables dynamics in other companies that have as customers Israeli government entities. It appears that very slow settling of receivables is somewhat normal in these businesses. Nonetheless, the receivables days remain almost half a year, which is a huge working capital commitment and shows in their cash flow statements.

Cash Flow Statement (Q3 2022 PR)

The company is not very cash generative, and incremental sales are likely to be dragged down by receivables bloat working capital commitments limiting the cash conversion. In a market where scope of growth would ordinarily be the selling point (were it not for the backlog issues), this isn’t a great structural factor to have.

Furthermore, the negative operating cash flow driven by the sales declines and operating leverage have actually drawn down cash balances to zero levels, until the company divested its SIS business, which explains the entirety of their $43 million of cash on hand.

The sale of the SIS business was a merit mark to the company. At a $47 million consideration, and considering SIS was 10% of CGNT’s historical run-rate revenue, it appears they got a price of about 4.5x P/S. This is definitely in line with multiples of even strong growth cybersec companies. This was a well-done acquisition as far as shareholders should be concerned.

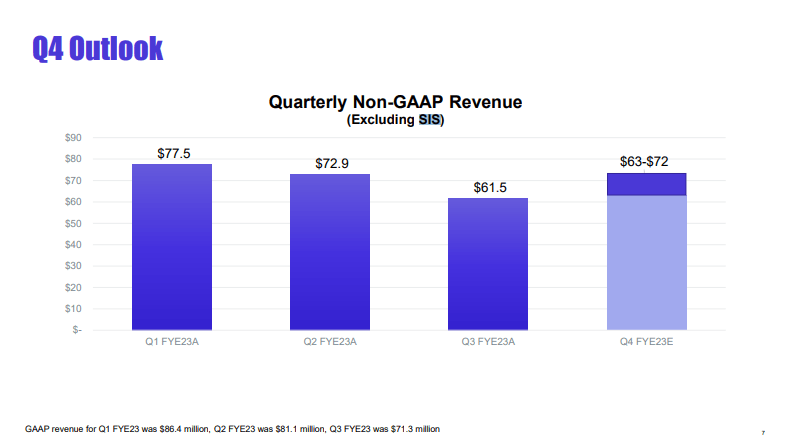

Nonetheless, the guidance doesn’t see a particularly positive increment in sales such that income could become restored. A 30% discount from last quarter’s sales figures are going to be needed to shore up the balances.

Guidance (Q3 2022 Pres)

If cash burning continues like this, CGNT will have to take on more debt. In fact, short term maturities are already almost assuredly going to be nixing the current cash balances within the next year. While CGNT is likely to have debt capacity, and probably won’t have to resort to equity markets, the interest expenses are going to grow if they’re raising in the current environment. It’s not a terribly good position to be in.

Cognyte Software Ltd. is low-multiple at less than 1x P/S for a reason. This backlog conversion is not picking up very quickly, and it raises concerns about what macro factors can do to this company. A not very cash generative model is another issue for Cognyte Software Ltd. to generate incremental shareholder value on eventual sales growth. Overall, Cognyte Software Ltd. is not a strong proposition.

Be the first to comment